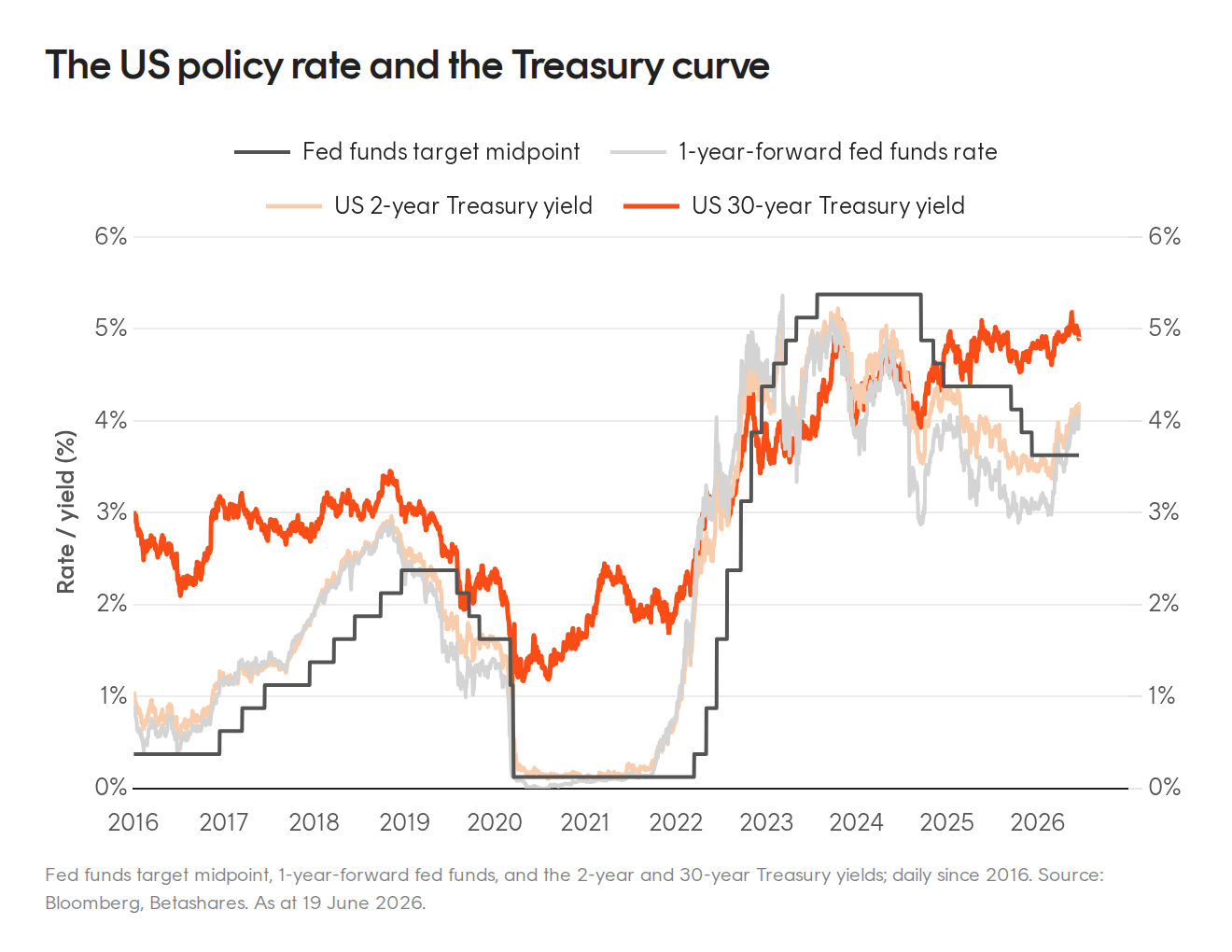

Kevin Warsh’s debut as Fed chair marked a regime change. The meeting itself was read as hawkish and the curve flattened hard, with the 2-year yield jumping 13 basis points and the 30-year yield ending the day marginally lower, though that owed more to the dot-plot revisions from the 18 participants who submitted than to anything Warsh said. However, his agenda carries the more profound implications, especially over the longer term.

The US policy rate and the Treasury curve

The first tell that something was different was the statement itself, cut to around a third of its previous length, at roughly 130 words. Consistent with his long-standing criticism of forward guidance, Warsh declined to submit his own fed funds projection (the “dots”). And perhaps most interestingly, he announced five task forces to modernise the Fed and how it sets policy.

Kevin Warsh’s five task forces

In the press conference Kevin Warsh outlined that the task forces would consist of both Fed officials and outside experts from industry and academia, focusing on five key areas:

1. Fed communications, including changes to the Summary of Economic Projections and the dot plot. Based on Warsh’s comments, we’ll likely see less communication from the Fed.

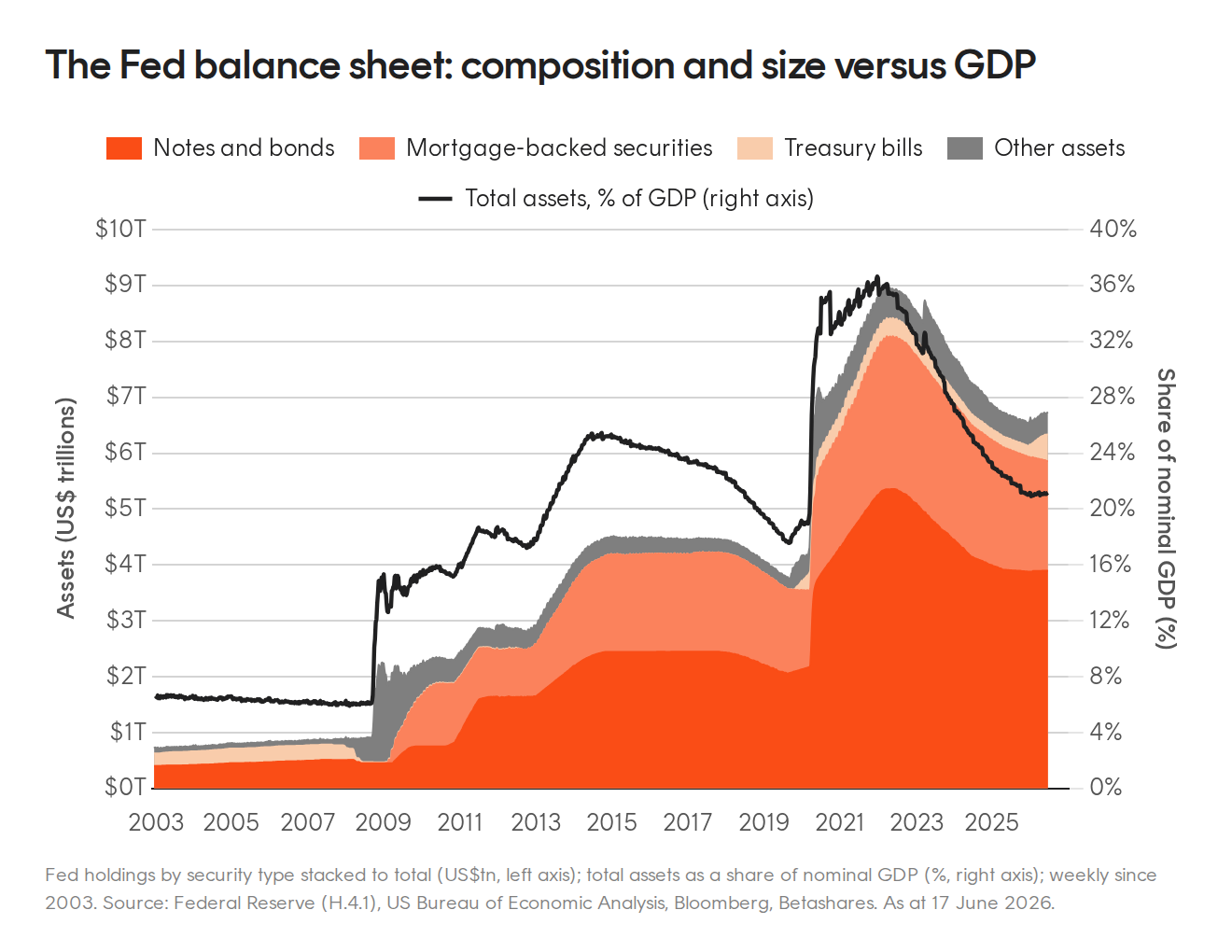

2. The balance sheet, weighing the costs of today’s ample-reserves regime against alternative operating frameworks. The assumption is we’ll see a smaller balance sheet, based on Warsh’s views on the topic.

3. Data sources, leaning more on timely information and less on revised official statistics. We’ll probably see alternative data sources being used, including a range of private sector inflation measures.

4. Productivity and jobs, examining what new technologies, including AI, mean for the dual mandate. An increased focus on supply-side factors will probably result from this exercise.

5. Inflation frameworks, a first-principles look at what drives inflation and how to deliver price stability. Possible we’ll see Core PCE replaced as the Fed’s preferred measure, with Warsh highlighting a preference for trimmed mean PCE in his Senate confirmation hearing.

Longer-term implications

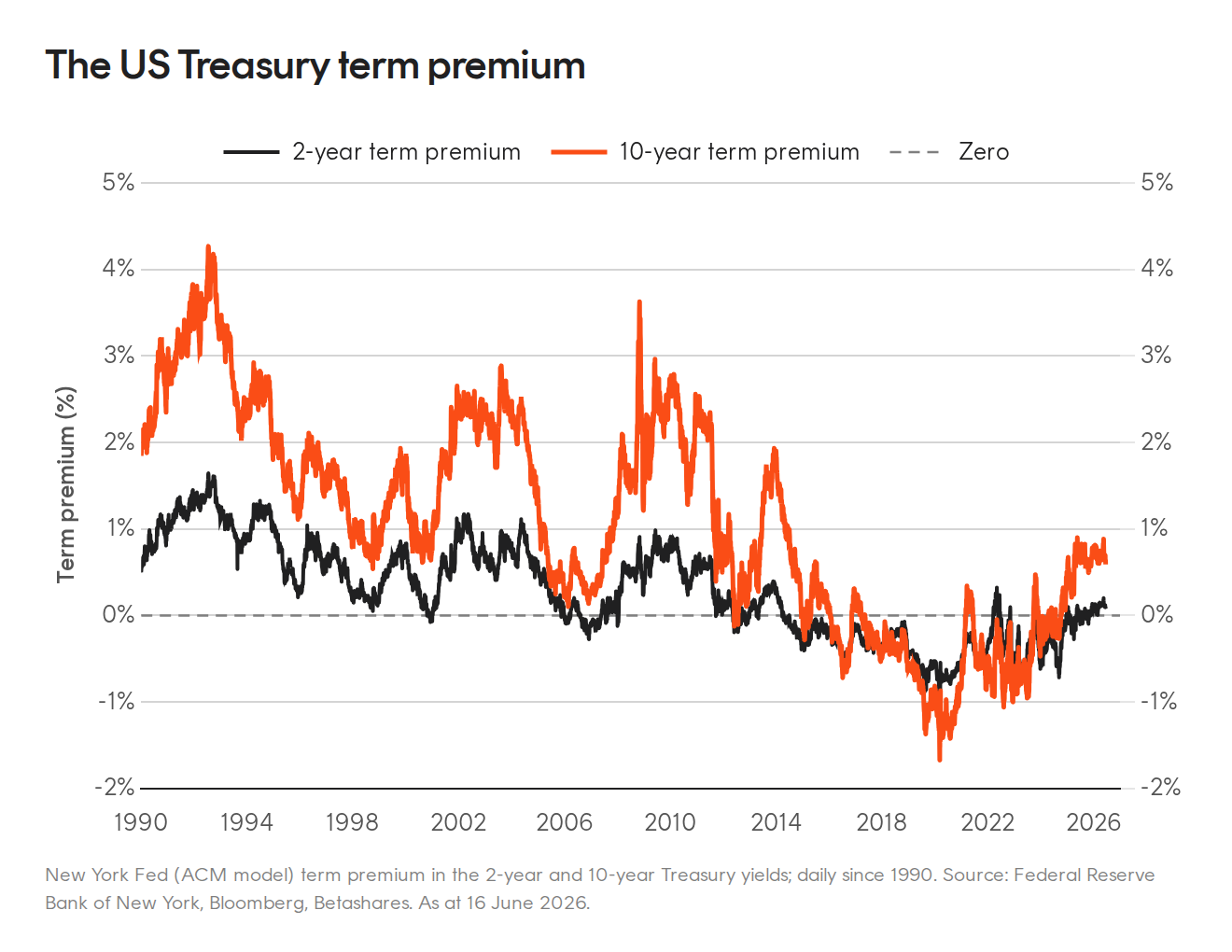

A smaller balance sheet, with bank reserves shrinking relative to GDP, leaves funding markets more prone to liquidity squeezes and wider funding spreads. Stepping back from forward guidance hands the job of pricing the path back to the market, which widens the term premium, the extra yield investors demand for bearing uncertainty, and probably steepens the curve overall. And a wider net for real-time data lifts the number of releases that markets, and the Fed, treat as first-tier.

The US Treasury term premium

The Fed’s reaction function will change, but how it changes will only become clear in time. With the market handed more of the job of pricing the path, a modest pick-up in US rate volatility over the coming months would be no surprise. For Australians with global bond portfolios, this matters, not just due to the weight of US bonds in the global benchmark (around 45%), but also the spillover to other central banks globally, if they adopt Warsh’s preferred approach of scaling back forward guidance. Closer to home, an easing RBA against a Fed that appears more hawkish has compressed the Australia-US 10-year spread to around +32 basis points, about 50 basis points tighter than earlier this year, driving continued outperformance of Australian bonds recently.