Key points

While investors are understandably focused on the Middle East and SpaceX this month, one ETF has quietly grown to become one of the largest in Australia, having been launched a little over 8 years ago. In some ways the popularity of Betashares A200 Australia 200 ETF is no surprise; it is the lowest cost Australian equity index ETF, with management fees of only 0.04% p.a. Yet there is now another, arguably more important reason for investors to consider A200, especially those that own a portfolio of Australian shares in their own name.

The Federal Senate passed the government’s negative gearing and CGT reform bill on Thursday 25th June. That process included a Senate inquiry to investigate the impacts of the CGT changes. Concerns were raised about housing supply, the impact on entrepreneurialism and the imposition of a minimum 30% CGT tax rate. However, given the tight two-day timeframe, the inquiry was rushed and lacked rigorous consideration of the true impacts of these taxes on everyday Australians who invest in the stockmarket.

The shift to CGT indexation creates an asymmetric tax treatment of winners and losers within a stock portfolio that significantly increases the overall tax rate paid by an individual investor. To understand this, you need to look beyond how the tax works on a single asset, to consider how it works across a portfolio of assets, particularly a share portfolio where there is typically high dispersion in performance.

The concept of indexation is to only tax gains above inflation. Yet, where you have a stock holding that has fallen in value or failed to outrun inflation you are not allowed to fully offset that real loss against the real capital gains of other winners in your portfolio. Across a portfolio of winners and losers, the ‘wasted’ tax relief on the losers adds up, leaving the investor taxed more heavily than someone who holds a single asset with the same overall return.

This deeper level of consideration did not see the light of day during the Senate inquiry, and the basic functioning of CGT indexation will now likely become law, applying to capital gains that accrue from 1 July 2027. The new regime is therefore not yet in effect, and the figures below illustrate how it will work for the taxation of gains from that point. The CGT discount method will still apply to gains prior to 1 July 2027.

What does CGT indexation do to the after-tax returns on a real stock portfolio?

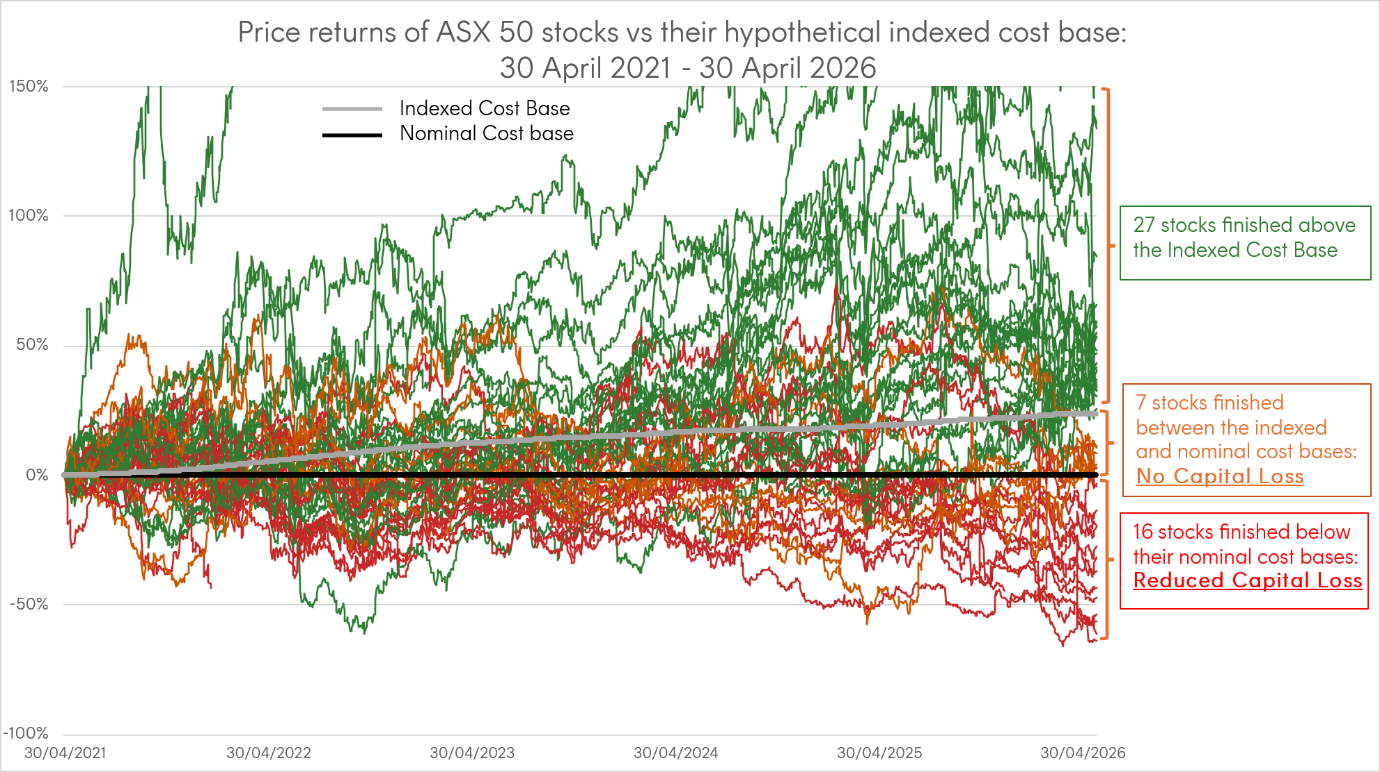

The chart below shows how 23 of the stocks within the ASX 50 index would have been adversely impacted for the 5-year period to 30 April 2026, had the proposed CGT indexation been applicable over that time. To see a simplified numerical example of the mechanics, please read this explainer.

Sources: Bloomberg; ABS. The chart shows the stock price returns of the ASX 50 constituents in the index at the start date of 30 April 2021. Stock price returns exclude any dividends paid. Historical ASX 50 constituents shift over time. The indexed cost base reflects the cumulative total CPI over the 5 year period. Some stocks that gained more than 150% are not displayed in full on the chart due to scale, but are included in the totals shown. Past performance is not an indicator of future performance. You cannot invest directly in an index.

As a hypothetical example, had a taxpayer on a 47% tax rate held these 50 stocks in an equally weighted portfolio over this 5-year period before disposing of them:

– The aggregate pre-tax capital gain would have been 6.57% p.a.,

– The post-tax capital gain under CGT discounting reduces return to 5.16% p.a.,

– But the post-tax capital gain under CGT indexation is lower still, at 4.82% p.a.

That is an additional tax drag of 0.34% p.a.

There is an irony worth drawing out here. Had that same investor instead held a single asset with capital gains of 6.57% p.a. over the period, their post-tax capital gain under CGT indexation would have improved to 5.56% p.a., versus 5.16% p.a. under CGT discounting. Furthermore, under CGT indexation the single asset owner would have been 0.74% p.a. better off than the direct stock investor, in our example. The total post-tax capital gain for the 50-stock portfolio under CGT indexation was 26.6% over the five years, but for a single asset with the same pre-tax return, the post-tax capital gain improves to 31.1%. The difference in outcomes is stark, especially after compounding.

Unlike disposing of a stock portfolio, when you sell a single pooled asset like an ETF, there are no internal losers whose real losses are stranded, so the asymmetry that penalises the stock portfolio never arises. What is left is indexation doing what it is meant to do: taxing only the real gain. It is the spread of outcomes across the directly held stock portfolio, not indexation in isolation, that drives the extra tax drag.

One way an investor can seek to reduce the CGT indexation tax drag that stems from holding a portfolio of stocks in their own name is to invest in a market-capitalisation index tracking ETF instead. A pooled managed investment scheme, like a managed fund or an ETF, will invariably have some capital gains that need to be distributed on an ongoing basis. But index ETFs, such as A200, are already very tax efficient at minimising those ongoing tax consequences. And now they have the additional benefit of being able to effectively offset winners and losers within the ETF. When an investor disposes of an ETF, the capital gain is calculated based on the ETF on-market price they buy and sell at, not at the underlying stock level.

Betashares Australia 200 ETF (ASX: A200)

A200 Australia 200 ETF is best known as the lowest cost Australian equity index ETF. For investors holding shares in their own name, its tax efficiency may now matter more.