Why the Budget makes ETFs’ tax advantage even more important

One of the most reliable drivers of long-term wealth creation is simply staying invested. Allowing capital to compound over years and decades is what turns a reasonable return into a meaningful one, and anything that interrupts that compounding, whether market timing, behavioural mistakes or unnecessary tax leakage, has an outsized impact on terminal wealth. Tax efficiency therefore matters at every step of the journey, not just at the point of exit. Every dollar of tax paid on income or realised capital gain distributed out of an investment vehicle erodes capital base of the investors in that vehicle, leaving less to compound from the following year onward. Over a multi-decade horizon, the drag from a tax-inefficient structure can be measured in tens of percentage points of final outcome.

With that as the backdrop and given the potentially higher capital gains tax rates facing Australian investors, it is worth restating a point that does not always get the airtime it deserves:

“When it comes to capital gains tax, index-tracking ETFs are structurally more efficient than actively managed unlisted funds.”

This is not a marketing claim, it is a function of how the two vehicles are built. There are two main drivers.

What drives this structural efficiency

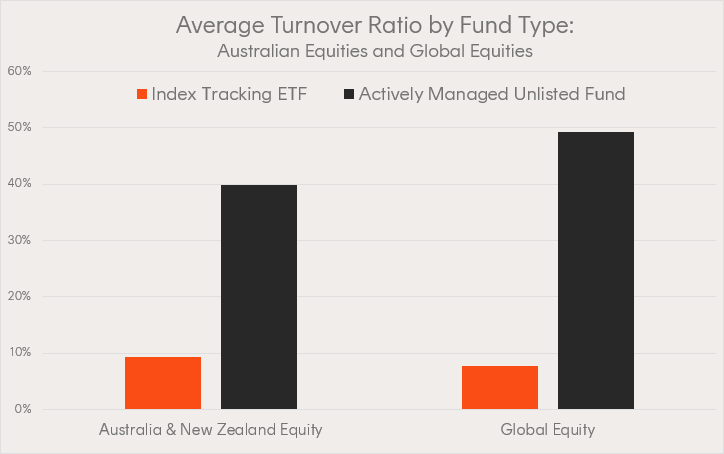

The first is lower strategy turnover. Index-tracking strategies typically turnover a small fraction of what active strategies do, because trading is driven by index changes, corporate actions and cash flows rather than by discretionary views. The lower the turnover, the lower the realisation of capital gains inside the fund, and the smaller the tax obligation passed through to investors in any given year. That matters because an investor’s time horizon is often far longer than the trading horizon of the manager. In an active unlisted fund, an investor can find themselves taxed each year on gains crystallised by trading activity they would not have undertaken themselves, well before they have any intention of selling their own units.

Source: Morningstar, Betashares. Based on data extracted on 15 May 2026. Universe limited to funds that have published a turnover ratio. Weighted average turnover is calculated based on each fund’s FUM, and is a per annum figure.

The chart above highlights the magnitude of the difference in average strategy turnover between index tracking ETFs and unlisted actively managed funds.

The second driver is less widely understood, and that is the ability to stream capital gains away from continuing investors. When an investor redeems units in an unlisted managed fund, the responsible entity often has to sell underlying assets to fund the redemption, crystallising capital gains in the process. The tax law permits an RE to stream those gains to the redeeming investor rather than spread them across the remaining unit holders. In theory that protects continuing investors. In practice, in an unlisted fund with thousands of individual applications and redemptions every day, attribution at that level of granularity is close to impossible to implement. The result is that continuing investors frequently wear CGT obligations triggered by someone else’s exit decision.

ETFs work differently. End investors do not transact directly with the responsible entity, they buy and sell units on market. Only a small number of Authorised Participants (essentially market makers) apply for and redeem units in the primary market, and any capital gains arising from in-specie or cash redemptions can be streamed cleanly to that handful of counterparties. Continuing investors are therefore largely insulated from the tax consequences of other investors’ selling decisions, in a way that is simply not practical to replicate in an unlisted fund structure.

These structural advantages have always tilted the after-tax playing field in favour of index ETFs over unlisted active funds, particularly for long-horizon investors who derive most of their return from compounding rather than from current income. The 2026-27 Federal Budget sharpens that advantage. From 1 July 2027, the 50% CGT discount will be replaced by cost base indexation for assets held more than 12 months, with a 30% minimum tax rate on net capital gains applying to individuals, trusts and partnerships. The interaction effects will vary by holding period, marginal tax rate and the real versus nominal split of any gain, but the direction of travel is clear: in most realistic scenarios the after-tax cost of an unnecessary realisation event has gone up, not down.

In that environment, vehicles that defer and minimise realisation events become structurally more valuable. The ETF structure was already doing real work for investors on this front. The Budget changes mean it is doing more of it.

For more information, see our article Explaining capital gains tax on ETFs (which reflects current rules, prior to proposed changes). See how your investments will be impacted with our CGT Calculator or visit our ETF tax resources hub.

Disclaimer

Betashares is not a tax adviser. This information should not be construed or relied on as tax advice and investors should obtain professional, independent tax advice before making an investment decision.

The information contained in this article is general information only and does not take into account any person’s financial objectives, situation or needs. Investors should consider the appropriateness of the information taking into account such factors and seek financial advice. This article is provided for information purposes only and is not a recommendation to make any investment or adopt any investment strategy.

Cameron Gleeson

Prior to joining Betashares, Cameron was a portfolio manager at Macquarie Asset Management, Head of Product at Bell Potter Capital, working on JP Morgan’s Equity Derivatives desk and at Deloitte Consulting.