Tom Wickenden

8 minutes reading time

David Bassanese is taking a well-earned two-week break from work. In his absence Betashares Investment Strategist Tom Wickenden will continue Bass Bites weekly commentary.

Global week in review: Taking a breather

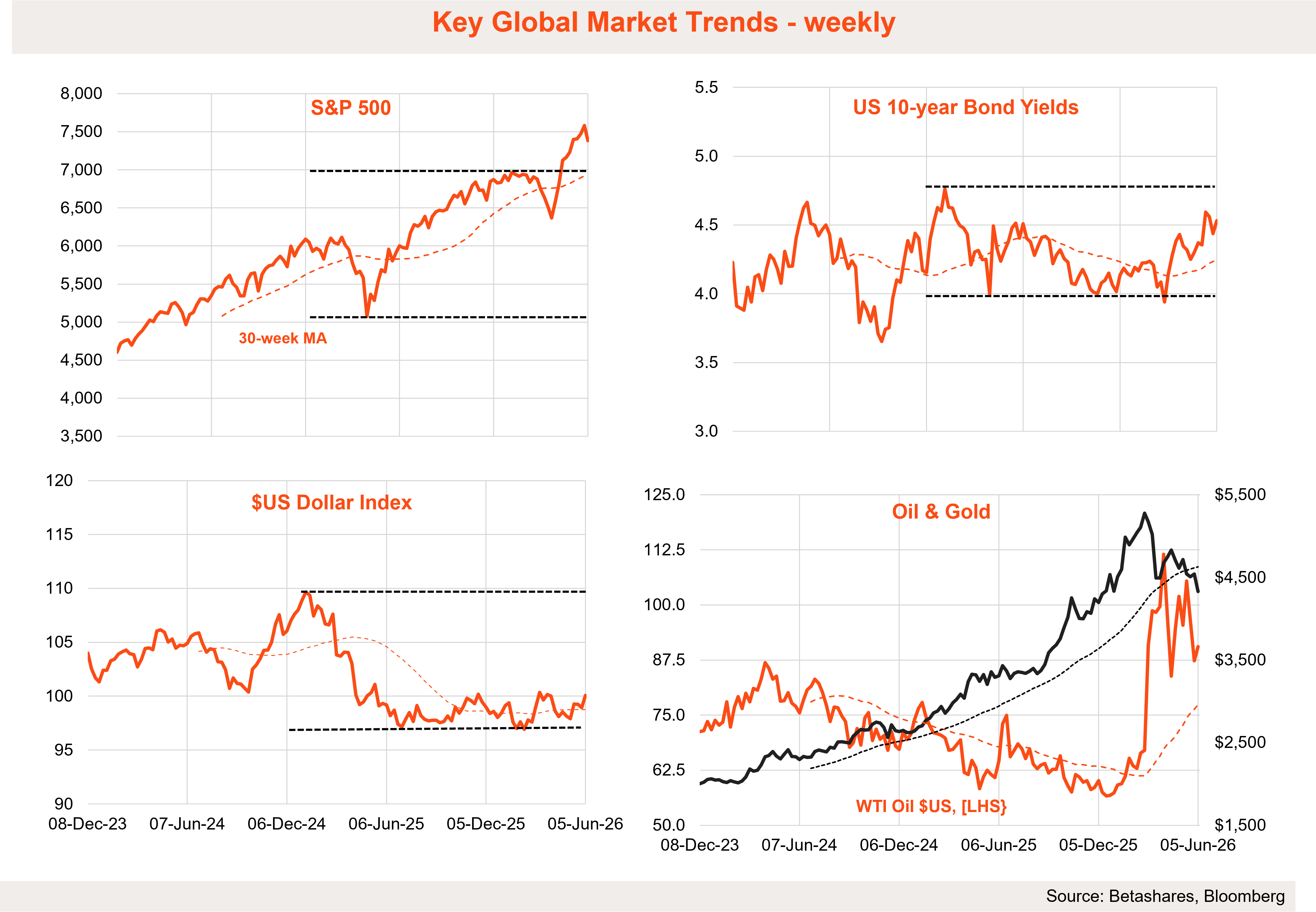

After nine straight weeks of gains, and floating towards a SpaceX IPO-driven liquidity vaccum, US markets were reconnected with ground control last week, brought back to the realities of macroeconomic and geopolitical risk.

Technology companies led US markets to their largest one-day sell-off in over a year last Friday, triggered by a blowout May payrolls report. The US economy added 172,000 jobs against a consensus forecast of 80,000, alongside a combined upward revision to March and April of 93,000. Leisure and hospitality led gains, partly reflecting hiring for the Football World Cup starting at the end of this week.

The stronger than expected employment figures drove US 10-year yields back over 4.5%, resurrecting fears that the Fed will remain on hold for longer, or potentially even need to hike, during 2026. Given market technicals were stretched from the rally through April and May, trading well above 200-day moving averages, and valuations had reset to 2026 highs, Friday’s spectacular sell-off has been called a healthy breather by many market analysts.

The past week also saw a deterioration in the Middle East conflict with Iran launching missiles at Israel over the weekend, the first such attack since April, in retaliation to ongoing Israel activity in Lebanon. Despite Trump’s pleas for restraint after the strikes Israel struck back hitting Iranian military sites. The escalation comes as Hezbollah rejected ceasefire terms proposed by Lebanon and Israel. Oil initially jumped more than 4% however has since eased back after all sides signalled a pause and Trump called for calm. The risk-off sentiment also saw the US dollar gain 1.1% but saw gold fall a further 4.7%.

While a peace agreement could still come at any time, removing the key geopolitical risk to markets, the weekend’s flare-up highlights the ongoing complexity of the war and the downside risk it still poses.

Global week ahead: Iran, US CPI and Kevin Warsh’s Fed on the horizon

As has been the case for months, the Middle East remains in primary focus. The weekend’s missile exchange has put the ongoing ceasefire on life support as Trump pushes for a 60-day extension to the truce as a bridge to permanent negotiations. Oil prices, the key indicator for markets, remain contained below US$100 per barrel as of this morning.

The key macroeconomic report will be this Wednesday’s US May CPI print. April came in at 3.8% year-on-year, the highest since 2023, driven largely by energy due to higher oil prices with consensus expectations of an increase to 4.2% for May. The print comes on the back of the significant market reaction to last week’s payrolls report. A soft print will take pressure off the Fed while a hot print could see markets begin to price in a higher chance of hikes in the US this year.

For markets the key event will be SpaceX’s Nasdaq IPO on Friday, raising $US75 billion at a valuation of US$1.8 trillion marking the largest IPO in history.

A pivotal CPI print, fragile Middle East ceasefire and historic IPO coming in the same week will test market composure. These events also come at a pivotal time for the Fed as Kevin Warsh is set to chair his first meeting as the new Federal Reserve Chair next week.

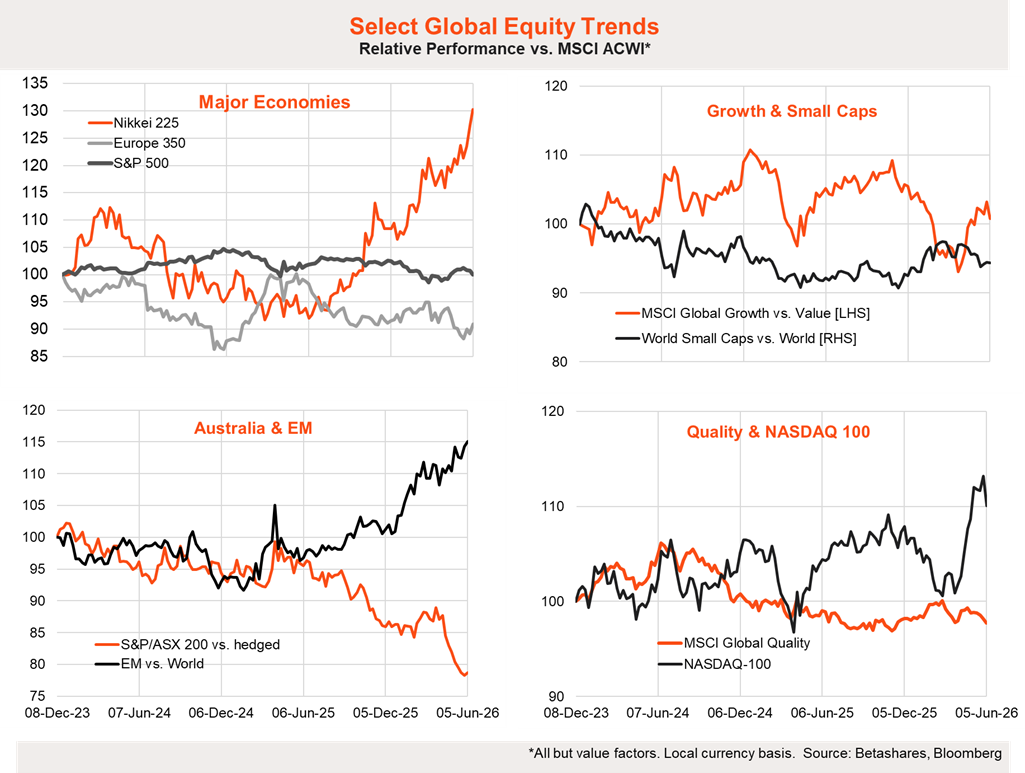

Global equity trends: Tech consolidation

Technology companies and chip and semiconductor manufacturers were the hardest hit in Friday’s sell-off, which had been the biggest winners in the market rally since April. This drove the Nasdaq 100 to its largest loss in over a year of 4.2% and saw South Korea’s Kospi fall 5.5% with Samsung and SK Hynix pairing some of their recent gains.

Nevertheless, the AI driven bull run remains intact. Related markets remain well above 200-day moving averages and the underlying hyperscaler spending catalyst for the capex boom has not changed as AI use skyrockets. The US markets rebounded modestly in Monday’s trading as sentiment steadied. A pause in the market’s rally would not be unwelcome over the coming weeks, given the significance of macro and market events, before climbing higher with greater certainty.

Australia review: Weaker growth and higher wages

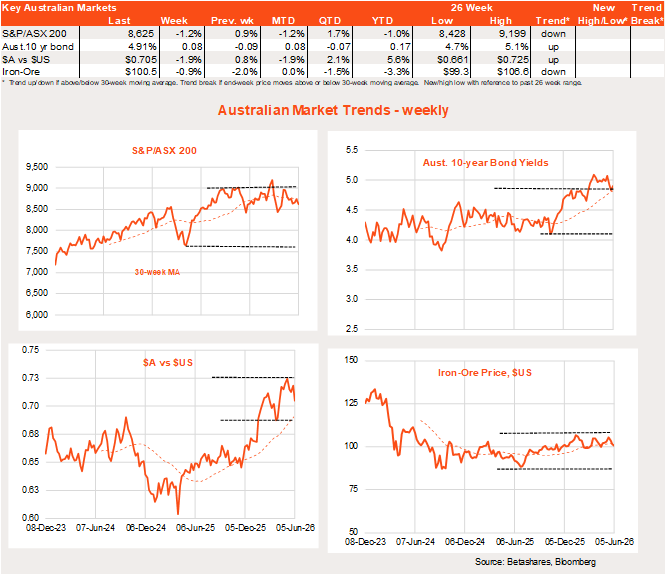

Local stocks were spared the worst of the global stock correction due to a Monday public holiday, however a below consensus GDP result and a productivity warning from Governor Bullock confirmed that Australia’s growth and inflation challenge is becoming harder.

Australia’s Q1 GDP came in at 0.3% quarter-on-quarter growth, below the 0.5% consensus and a sharp deceleration from Q4 2025 which was revised upwards to 0.9%. The weakness was concentrated in net trade, which subtracted 0.8% from growth as coal and iron ore exports were disrupted by adverse weather while imports surged driven by a record rise in automatic data processing equipment. Household consumption remains subdued and government spending was flat.

The saving grace was private investment, which contributed 0.7%, underpinned by Australia’s data centre construction boom.

Australia household consumption grew 0.5% however the increase was driven by essential spending led by an 11.7% jump in electricity, gas and fuel costs as energy rebates ended. Discretionary spending was near flat at 0.1% while the savings rate fell to 6.2% from 7.0% because income growth was outpaced by a rise in nominal consumption costs, mostly energy. Higher mortgage payments also weighed on disposable income. While the headline consumption figure appeared positive, the reality is that Australian consumers are not loosening up, they are being squeezed.

Last week the Fair Work Commission handed down its decision to lift the national minimum wage by 4.75% from 1 July. The increase sits above both headline inflation and current wage growth and will directly impact 21% of the workforce. According to Morgan Stanley the direct mechanical impact of the minimum wage rise on aggregate wage growth is modest at around 0.1%, but the expectations channel is the real risk. If above-inflation wage settlements become entrenched, the RBA’s job gets considerably harder.

Governor Bullock’s Senate testimony last week framed the RBA’s longer-run challenge starkly: with productivity falling 0.6% in the March quarter, the worst result since mid-2024, the economy risks stagflation if energy-driven inflation persists while growth continues to slow. Bullock noted that the flow of data since May had not been materially different to RBA expectations, that inflation is likely to rise further in the near term, and that having raised rates three times, monetary policy is now well placed to respond to developments.

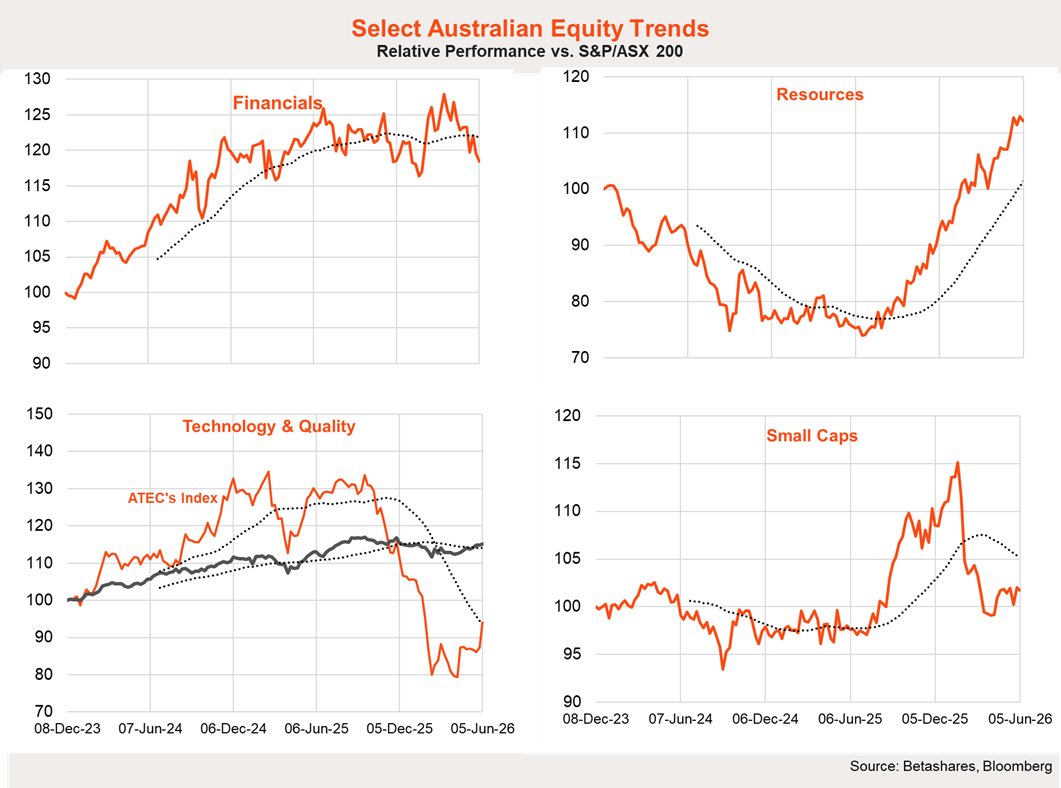

Local equity market trends: Delayed sell-off mirroring US consolidation

Last week’s ASX performance was relatively contained, with the index down 1.2%, its first weekly decline in three weeks, as energy held up on the Iran oil spike while real estate lagged and the banks softened modestly.

The global tech sell-off that drove Friday’s Nasdaq decline of over 4% landed after Australian markets had closed for the week, with Monday’s public holiday delaying the local reaction further. As markets open Tuesday morning, the ASX 200 is down 1.2%, with both materials and technology the hardest hit sectors, materials off more than tech, with iron ore retreating towards US$100 per tonne and gold having repriced lower.

The pattern echoes what played out on Wall Street Friday. Recent market leaders have borne the brunt of the pullback, suggesting consolidation of stretched positions rather than a broad-based deterioration. Globally exposed resource stocks and tech had been among the ASX’s strongest performers in recent months, making them natural targets when sentiment shifts. Whether this is a healthy consolidation or the start of a broader reassessment remains the key question for the week ahead.

Australia week ahead: Sentiment health check

The domestic data calendar is light this week, with consumer and business sentiment for June and May respectively the key local releases, both out today.

Consumer sentiment is expected to remain soft. Households continue to face restrictive mortgage rates, elevated energy costs and growing uncertainty around the Budget’s capital gains changes, with lower fuel prices providing only modest offset.

Business sentiment is expected to stabilise modestly after April’s sharp deterioration, though employment conditions and capex intentions, both of which stepped down sharply last month, will be the key components to watch as a read on whether the domestic slowdown is broadening.

Have a great week!

Tom