David Bassanese

5 minutes reading time

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Key global developments in May

- On-again, off-again US-Iran ceasefire talks continued to support risk assets in May. Oil prices dropped despite the Strait of Hormuz remaining effectively closed.

- Ongoing strong demand for AI-related computer chips and data centres continued to support the ‘AI trade’. This is no longer just a US tech story, with good gains evident in Japan, Korea and Taiwan.

- In Australia, optimism remains subdued due to another RBA rate hike in the month and a major lift in capital gains tax on both property and non-property assets in the Federal Budget.

Interest rates

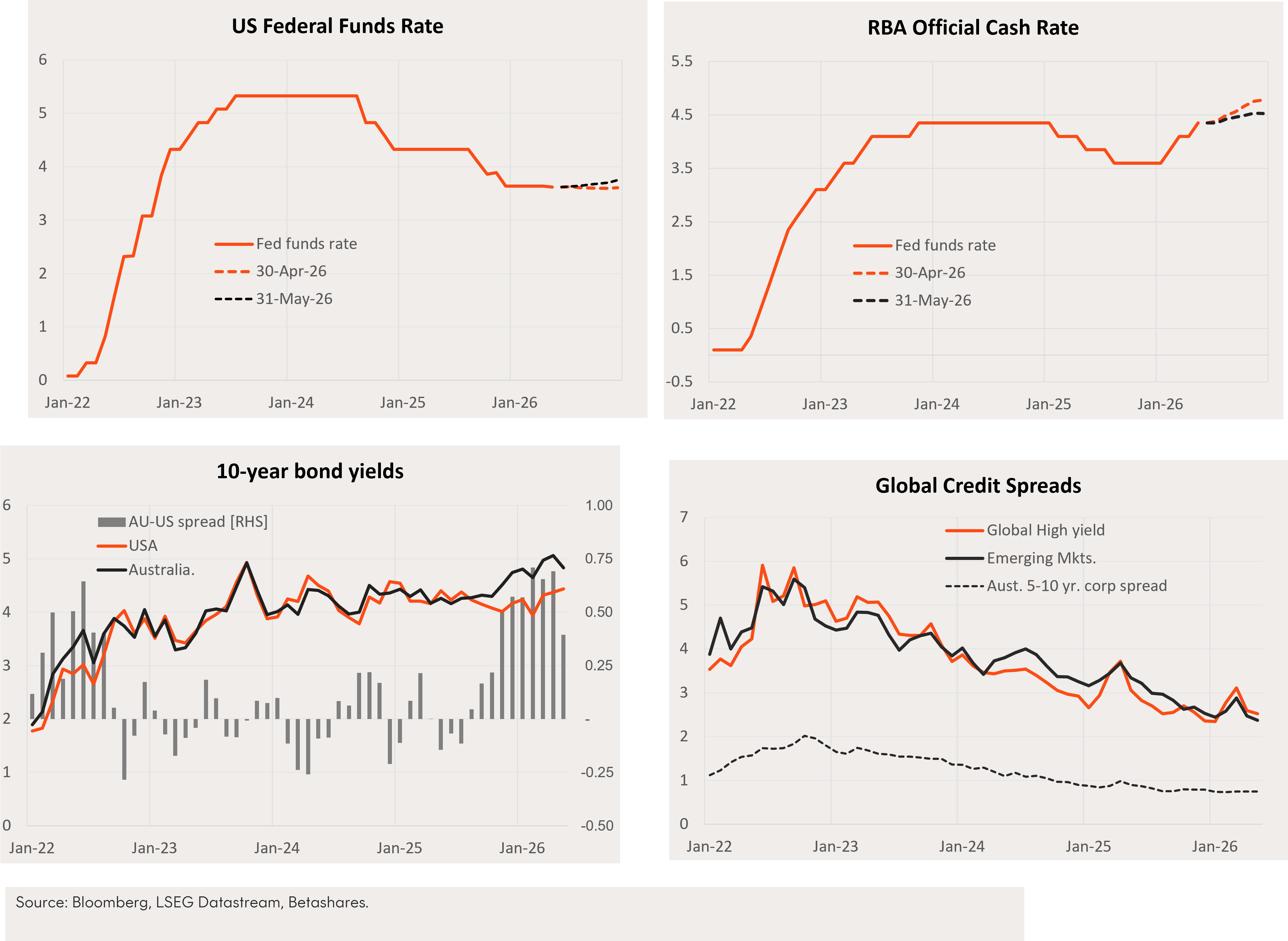

- There was a modest shift in US and Australia monetary policy expectations in May.

- The US market moved to price in a higher chance of a rate hike by year end, reflecting persistent high inflation reports and a hawkish tilt in Fed rhetoric. The Australian market lowered the risk of more than one hike by year end, reflecting a tamer than feared April CPI report and weak labour market report.

- US 10-year bond yields edged up by 0.07% to 4.4%, whereas Australian 10-year yields slumped 0.23% to 4.89% – resulting in a notable narrowing in the Australian-US 10-year bond yield differential. Bond yields in both markets have been trending modestly higher since late 2025.

- After widening in March, global credit spreads tightened a little further in May and local credit spreads remain contained.

Commodity prices

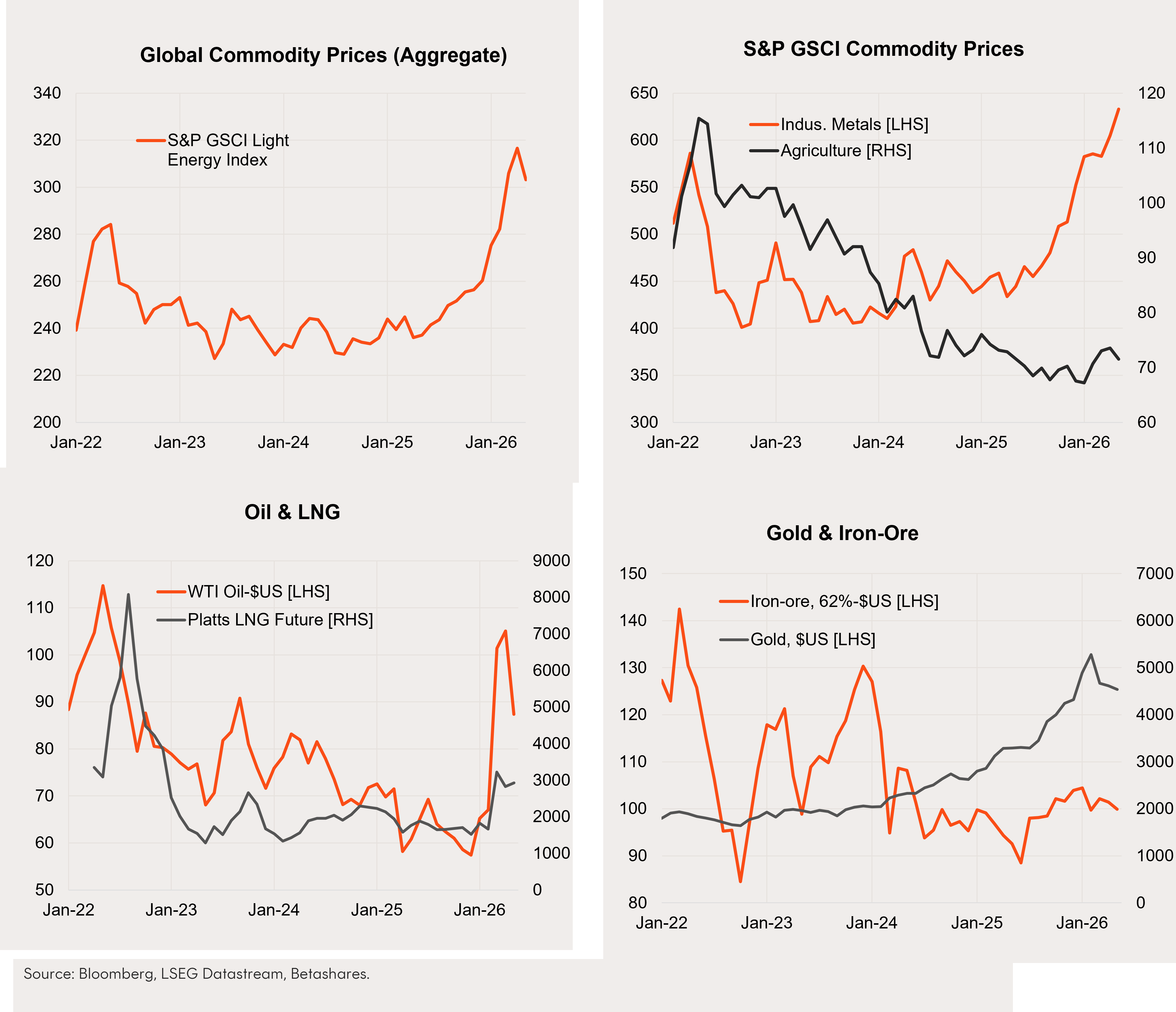

- After very strong gains since mid-2025, the benchmark index of global commodity prices* eased back in May, largely reflecting a steep fall in oil prices on the back of US-Iran peace-talk hopes.

- Industrial metal prices rose strongly again, underpinned by strong AI-related demand. Gas prices remained high, while gold, iron ore and agricultural prices eased.

*Defined as the S&P GSCI Light Energy Index, which includes a range of prices covering energy, metals, agriculture and livestock.

Exchange rates

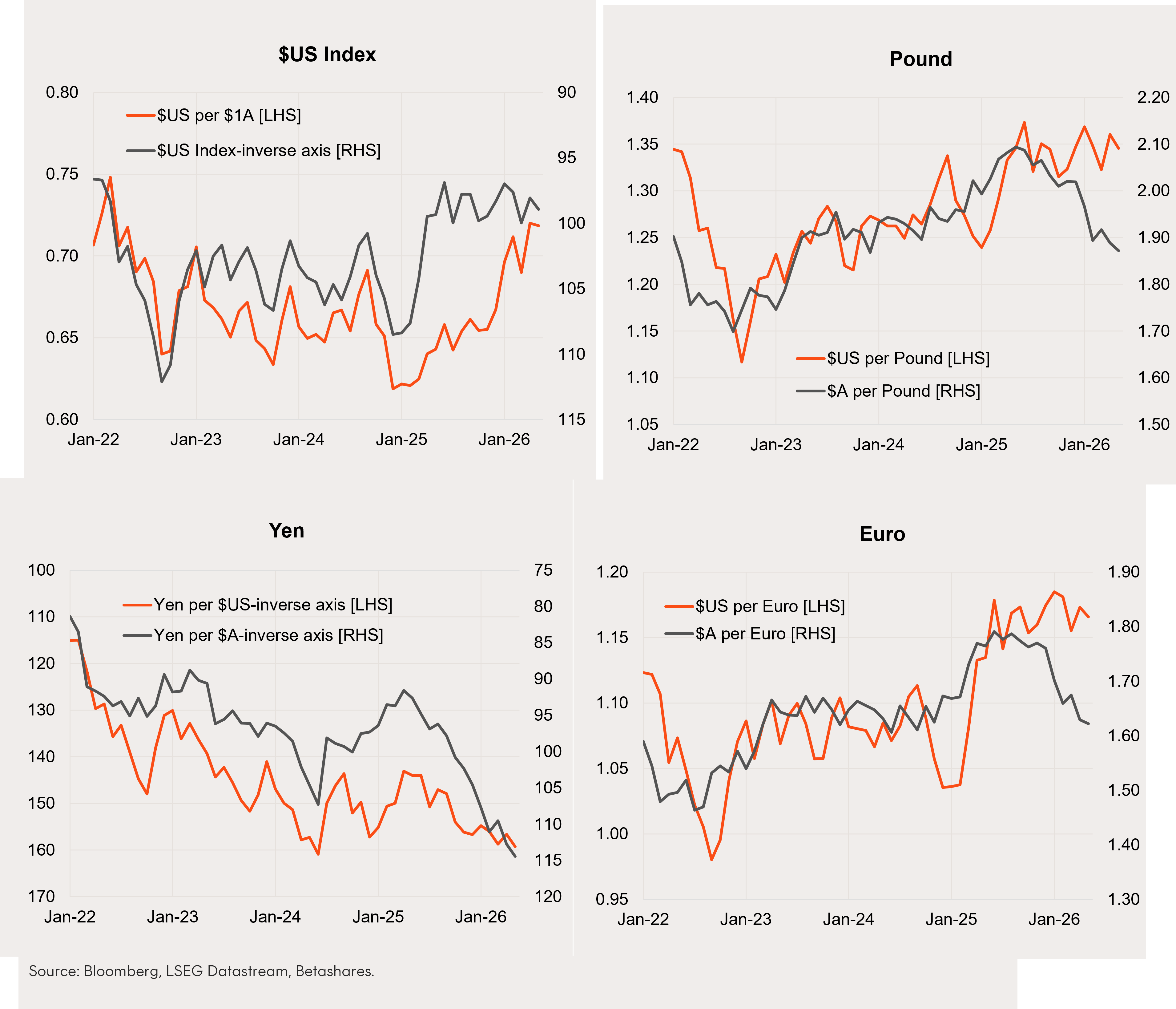

- The Australian dollar eased slightly in May, from US72.0c to US71.9c, though remains well up on year-ago levels. The $A has been in a solid uptrend since early 2025 against most major currencies, reflecting firmer commodity prices, a softer $US and local rate hike expectations.

- The US dollar strengthened a little in May, but is still within its choppy sideways range since mid-2025. While range bound against the Euro and Pound, the $US – like the $A – has been generally strengthening against the Yen.

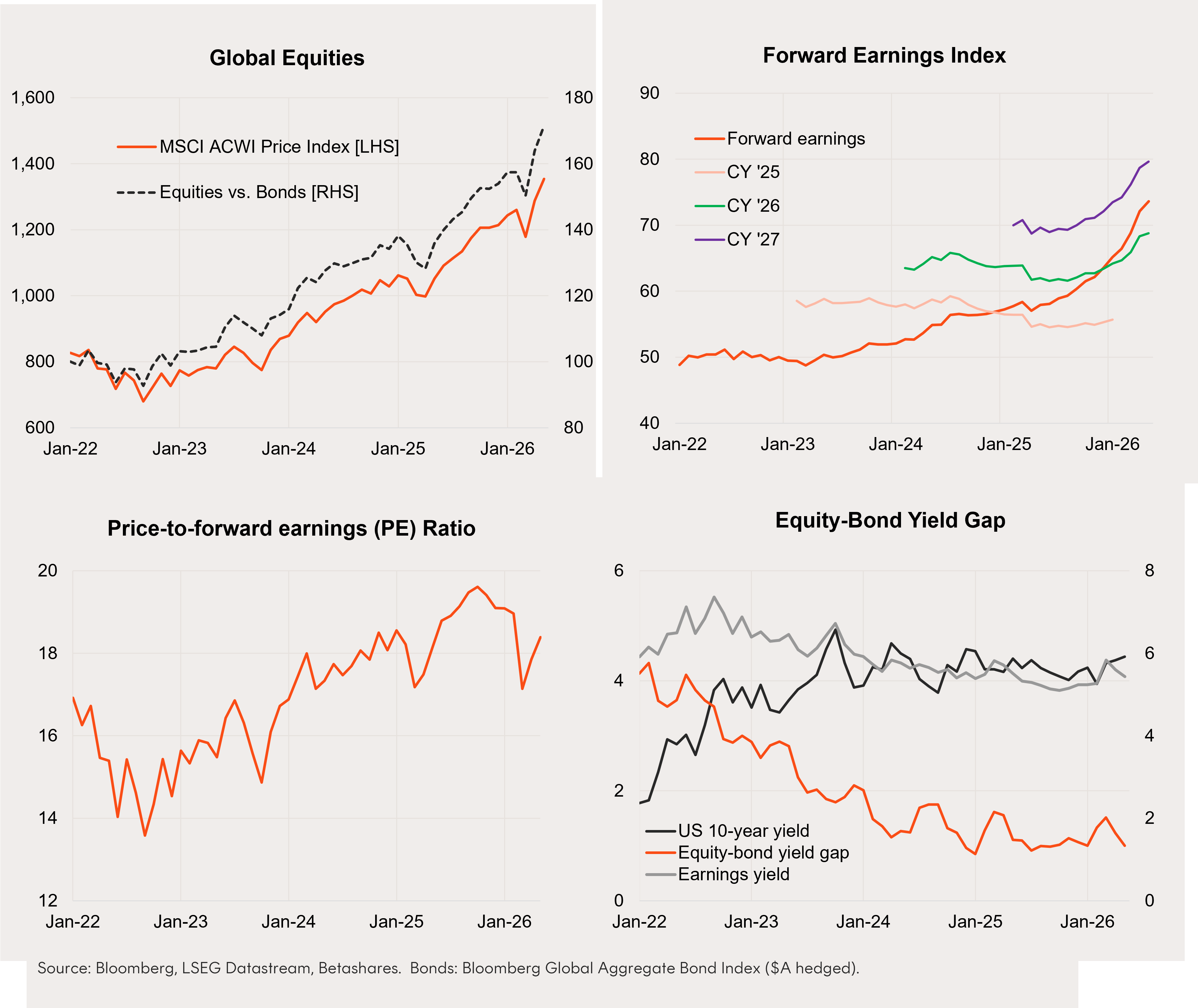

Global equities

- Global equities rose further in May, reflecting hopes for a US-Iran peace deal and AI-related optimism. The MSCI ACWI Index returned 5.3% in local currency terms, following a rise of 9.4% in April.

- Despite war concerns, global earnings expectations remain upbeat and forward earnings continue to rise with 8% expected growth by year-end.

- Although it has lifted in the past two months, the global forward PE ratio of 18.4 by end-May remains below its recent peak of 19.6 in October 2025 – despite share prices being at record highs. This reflects continued good gains in forward earnings.

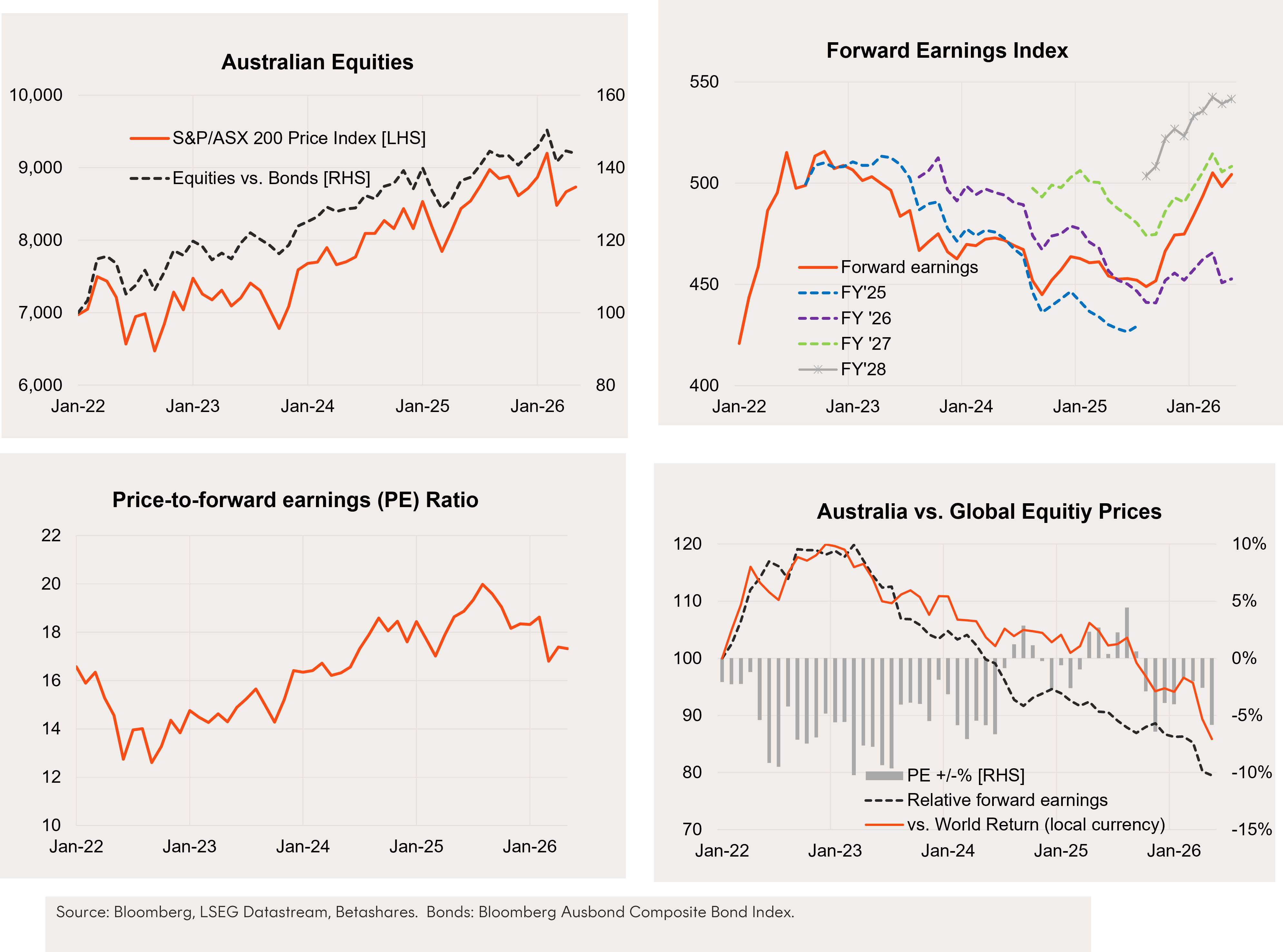

Australian equities

- The Australian equity rebound has lagged that of global markets in recent months, with the S&P/ASX 200 returning only 1.1% in May following a 2.2% gain in April.

- After declining in April, earnings expectations stabilised in May. Current expectations are consistent with 4% growth in forward earnings by year-end – half that expected by the global market.

- A solid upturn in forward earnings since mid-2025 has helped improve local equity valuations, with the forward PE ratio ending May at 17.3 – down from a recent peak of 20 in August last year. Local stocks are trading at a modest 6% discount to global stocks.

Equity themes/trends

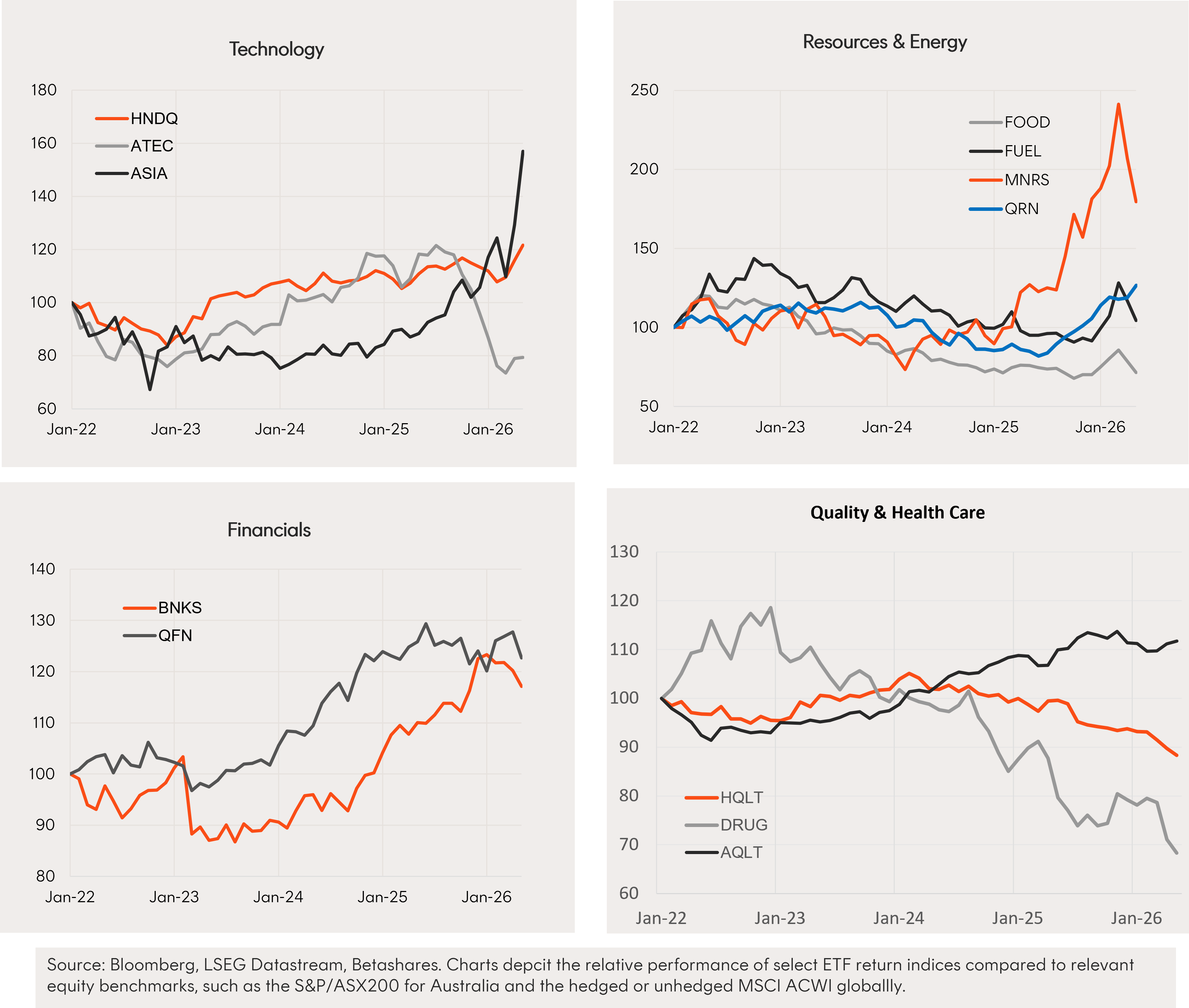

- The fall back in oil and food prices over May led to a correction in the relative performance of some commodity ETF exposures in the month, such as FUEL and FOOD. MNRS also weakened due to the easing in gold prices. In Australia, however, QRN’s relative performance held up.

- Meanwhile, the AI boom continued to support technology ETF exposures, especially ASIA, which contains major technology hardware companies in the AI supply chain.

- Elsewhere, financials have tended to underperform so far this year, as has been the case for health care and the ‘quality’ factor.