Investing in the space economy – from launch pad to commercial reality

Key points

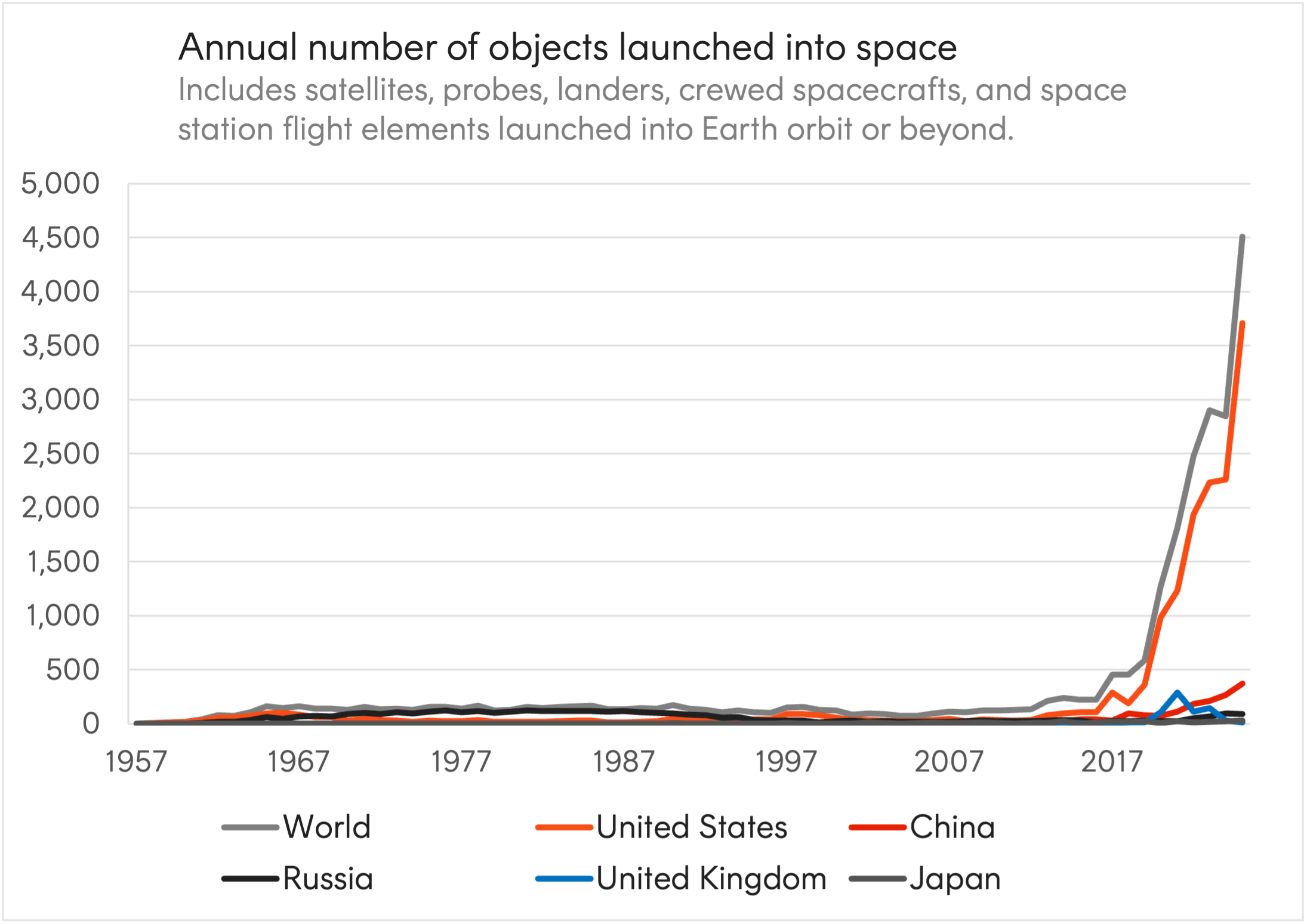

The number of objects being launched into space has skyrocketed in recent years.

Source: United Nations Office for Outer Space Affairs (2026)

While rocket and satellite technologies have been around for many decades, we have seen a resurgence in interest around space this year. The upcoming SpaceX IPO and NASA’s successful Artemis II mission have certainly created a lot of excitement for the industry, but this article will explore some of the technological innovations and real-life use cases making space an increasingly viable commercial opportunity for investors.

Source: NASA. Earthset captured through the Orion spacecraft window at 6:41 p.m. EDT, April 6, 2026, during the Artemis II crew’s flyby of the Moon.

The LEO revolution

According to the World Economic Forum, the global space economy was valued at US$630 billion in 2023 and is projected to reach US$1.8 trillion by 2035[2], with a large part of this growth driven by the development of low Earth orbit (LEO) satellites.

These types of satellites provide low-latency communication services, and a number of companies are now generating meaningful revenues from this technology.

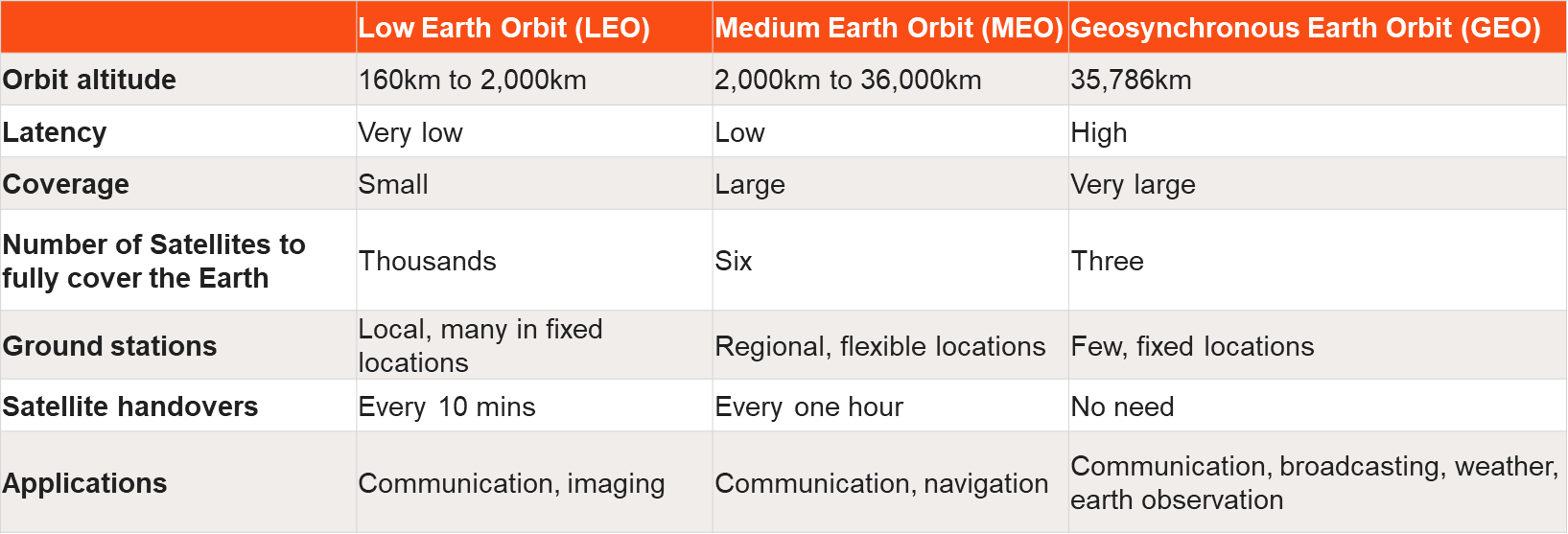

What’s the difference between LEO, MEO and GEO satellites?

Source: Goldman Sachs Global Investment Research

Lower latency means faster, more responsive connectivity. Because LEO satellites are so much closer to the earth’s surface than GEO satellites, the time taken from for a signal to make the return trip is more than 10X faster[3]. Speed matters in an increasingly digitalised and connected world. The trade-off for being closer to the earth is that a satellite’s field of view is narrower, and you therefore need many more satellites operating in a coordinated network or ‘constellation’ in order to provide constant connectivity.

SpaceX’s Starlink is the most prominent example with a constellation comprising over 10,000 LEO satellites, or roughly 65% of all active satellites in orbit, and serves more than 10 million subscribers globally[4]. The satellite internet division is highly profitable, contributing ~60-70% of SpaceX’s total revenue[5].

Most of these revenues stem from monthly consumer internet subscriptions, government and defence agencies, but also maritime and aviation companies.

In Ukraine, Starlink became a cornerstone of civilian and military communications within hours of Russia’s 2022 invasion, supporting hospitals, railways, and frontline operations after terrestrial networks were destroyed. By mid-2022, over 150,000 Ukrainians were relying on the service daily[6].

Additionally, over 40 million passengers have used Starlink on airlines and cruise ships last year[7]. Major carriers including United, Emirates and British Airways are replacing outdated legacy GEO-satellite Wi-Fi across their fleets with Starlink, delivering passengers internet speeds equivalent to home broadband.

Locally in Australia, Telstra and NSW Rural Fire Services are actively using Starlink for satellite broadband and mobile services.

Mobile coverage: the next frontier

While Starlink requires a dedicated terminal, an equally significant parallel technology is emerging: space-based mobile networks that connect directly to standard smartphones. The leading pure-play company here is AST SpaceMobile (ASTS).

In October 2025, the company signed a definitive commercial agreement with Verizon to provide direct-to-mobile service starting in 2026, following Verizon’s US$100 million strategic investment the prior year[8]. The deal was announced after successful demonstrations, including voice and video calls between standard phones via satellite.

AST SpaceMobile has also secured agreements with AT&T and Vodafone and plans to deploy 45–60 next-generation satellites in LEO by the end of this year[9]. Although currently unprofitable, AST is expected to become profitable next year as subscriber revenue and commercial services ramp up.

Space Data as a Service: Planet Labs

Beyond the infrastructure layer, space data as a service (SDaaS) is becoming increasingly viable as sectors like defence and agriculture seek on-demand, scalable data sets to inform critical decision-making.

Planet Labs (PL) is a key leader in this sector, operating the largest commercial earth observation constellation in history with over 200 satellites imaging the Earth’s entire landmass every 24 hours. PL overlays AI to generate valuable insights from this image data that are sold as a subscription, generating over 90% of revenue on a recurring basis. Its client mix spans agriculture, forestry, defence, insurance, and financial services.

In its most recent fiscal year, Planet Labs posted revenue of approximately US$308 million and achieved full-year adjusted EBITDA profitability for the first time, with a backlog reaching US$900 million[10]. Defence and intelligence have been the key growth drivers — including a €240 million multi-year German government contract[11].

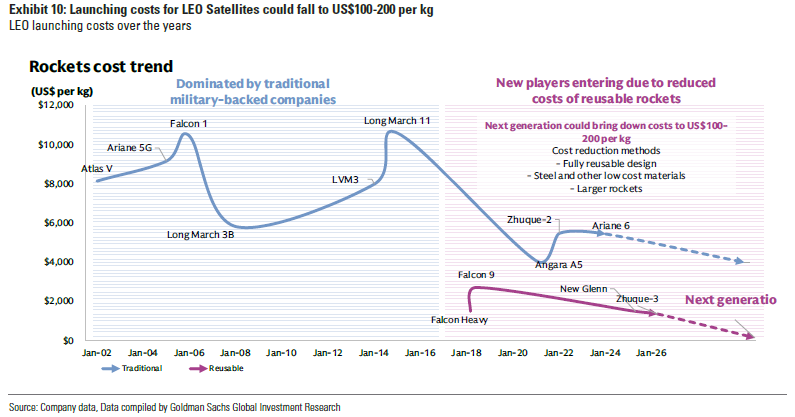

The enabler: falling launch costs

None of the above would be commercially viable without the dramatic decline in the cost of reaching orbit – a key metric underpinning the entire industry’s expansion.

Traditional launch vehicles have cost upwards of US$12,000 per kilogram to LEO. SpaceX’s Falcon 9, through reusable first-stage boosters, brought this to US$2,000–4,000 while next-generation vehicles like SpaceX’s Starship could push costs as low as US$100–200 per kilogram[12]. Importantly, both the cost per kilogram and the cost per mission have fallen.

This dynamic is self-reinforcing: lower launch costs enable larger constellations, which create more data and connectivity capacity, which attracts more commercial customers, and therefore funds further launches.

With launch capacity still a key bottleneck, vertical integration is becoming more common – traditional launch providers like Rocket Lab and Firefly Aerospace are now building their own satellites as well.

Investment implications

The Betashares Space Industry ETF (ASX: RCKT) is a first of its kind, aiming to provide targeted exposure to the space theme.

The fund seeks to track the Solactive Space Industry Index which includes up to 30 pure-play space companies weighted by their float adjusted market capitalisation, with a single-stock weight cap of 10%. Where the Index contains companies with a total market capitalisation above US$250 billion, the largest such company may carry a maximum weight of 25%.

Unlike broader aerospace indices that include conglomerates like Boeing or Lockheed Martin — where space may represent a small fraction of total revenue — the index also targets companies for which space is the primary business. Top holdings include names discussed throughout this article: Planet Labs, Viasat, EchoStar (which holds a minor stake in SpaceX), Rocket Lab, Globalstar, MDA Space, and AST SpaceMobile.

A notable design feature is the index’s fast-entry of eligible major IPOs into the index shortly after listing (generally two trading days), such as that anticipated for SpaceX.

“The space economy is supported by long term structural tailwinds — including by falling launch costs, expanding satellite constellations, and deepening commercial demand across broadband, mobile, data, and defence.”

Investors can now invest in this theme through RCKT in one single trade on the ASX.

There are risks associated with an investment in RCKT, including market risk, index methodology risk, international investment risk, thematic concentration risk, small and mid-cap company risk and currency risk. Investment value can go up and down. An investment in the Fund should only be considered as part of a broader portfolio, taking into account your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Fund, please see the Product Disclosure Statement and Target Market Determination at www.betashares.com.au.

The information contained in this article is general information only and does not take into account any person’s financial objectives, situation or needs. Investors should consider the appropriateness of the information taking into account such factors and seek financial advice. This article is provided for information purposes only and is not a recommendation to make any investment or adopt any investment strategy.

Future outcomes are inherently uncertain. Actual outcomes may differ materially from those contemplated in any opinions, estimates or other forward-looking statements given in this article.

Past performance is not indicative of future performance. No assurance is given that any of the companies in a Fund’s portfolio will remain in the portfolio or will be profitable investments.

1. Orbital Radar, ‘Launch Cost Trends’, March 2026; NASA Technical Reports Server.

2. World Economic Forum & McKinsey & Company, ‘Space: The $1.8 Trillion Opportunity for Global Economic Growth’, April 2024.

3. Goldman Sachs Global Investment Research

4. SpaceX; Jonathan McDowell, Jonathan’s Space Report.

5. Sacra Research; The Information.

6. CNBC, May 2022; Belfer Center, Harvard Kennedy School, March 2023.

7. Starlink Progress Report, December 2025.

8. AST SpaceMobile press release via BusinessWire, 8 October 2025.

9. AST SpaceMobile Q2 2025 Business Update, 11 August 2025; SEC Form 8-K filing.

10. Planet Labs FY2026 Earnings Release, 19 March 2026.

11. Planet Labs press release via BusinessWire, 1 July 2025.

12. NASA Technical Reports, ‘The Recent Large Reduction in Space Launch Cost’, 2020; SpaceNexus, ‘Space Launch Cost Comparison 2026’.