We tested three investing strategies over 26 years. The winner surprised us.

What happens when you pit perfect market timing against the simplest strategy in investing?

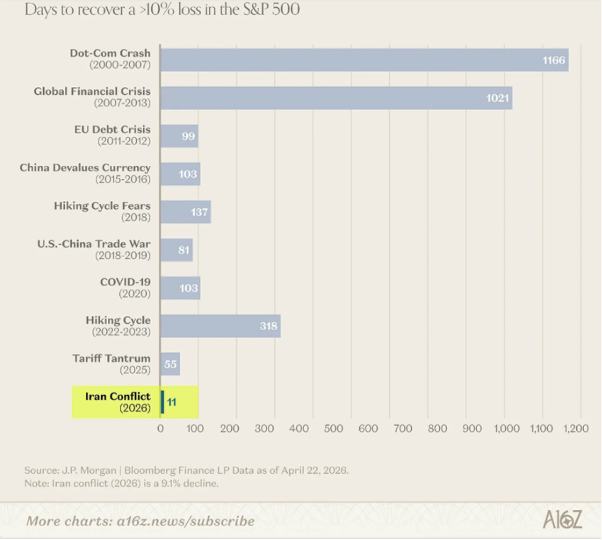

We’ve just seen one of the fastest US market recoveries in recent history. Despite the Strait of Hormuz still being closed and a US-Iran ceasefire nowhere in sight, US investors have shaken off their worries and the S&P 500 is back at all-time highs.

In March 2026, the index dropped more than 9%. In April, it came storming back in just 11 days.

Source: a16Z.news

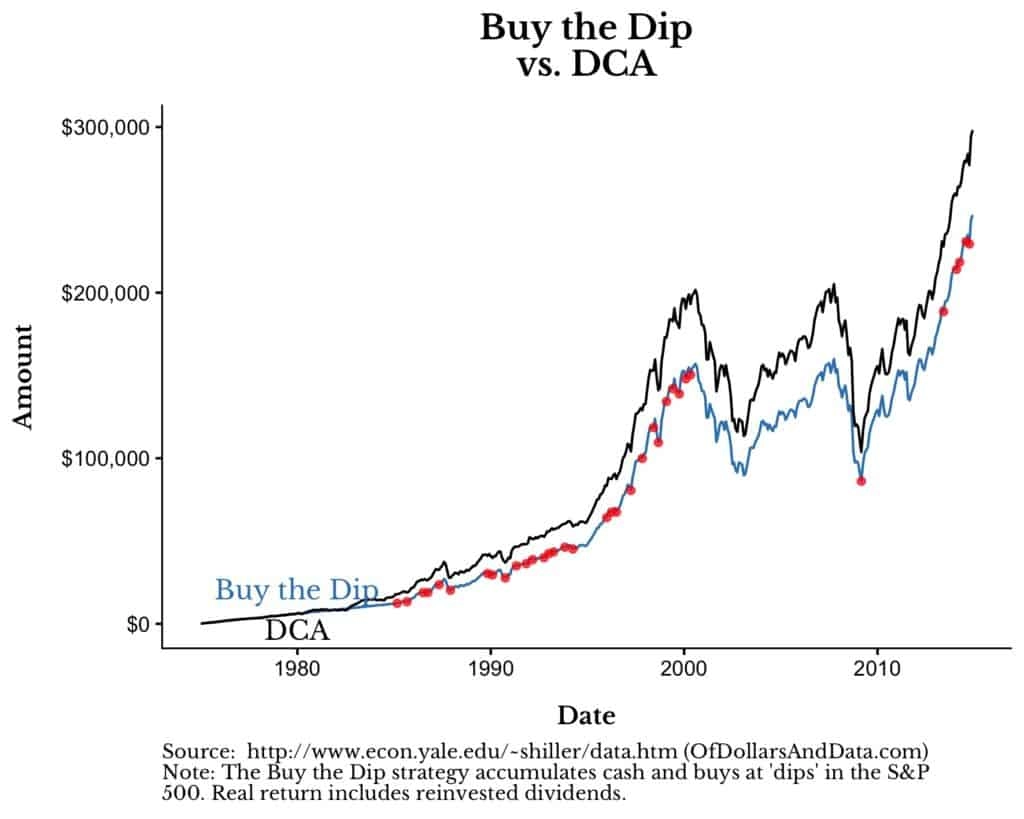

Timing the market has always been hard and, with markets moving this quickly, it’s even harder. But there’s good news for investors: historical simulation suggests that perfect market timing may not beat the simple strategy of dollar-cost averaging.

Even with perfect hindsight about where the bottom is, a strategy that waits in cash can still end up behind regular investing because it stays out of the market longer. In his now-famous article ‘Even God Couldn’t Beat Dollar-Cost Averaging’, Nick Maggiulli proposed his bold thesis: “Buy, buy, buy” beats “Buy the dip”.

His hypothetical historical performance simulation showed that an investor simply buying $100 of the S&P 500 every month, referred to as dollar-cost averaging, would have beaten an omniscient investor, who he refers to as God, who managed to invest at the exact market bottom (also referred to as ‘perfectly timing the market’).

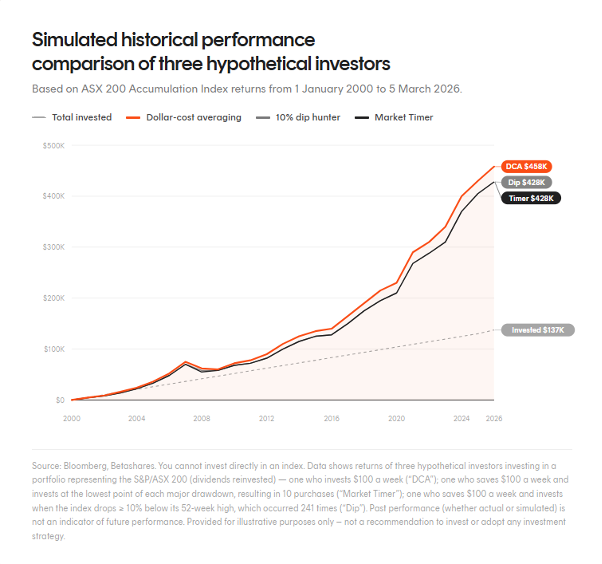

Our analysis suggests the same holds true in Australia

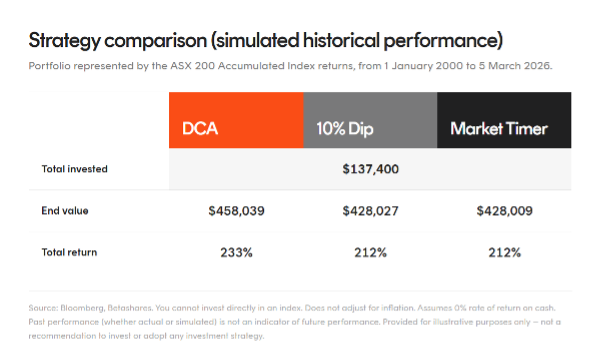

We set out to see if the same holds true in Australia by modelling a hypothetical historical performance simulation. To do this, we looked at three hypothetical investors using different investing strategies to invest in a portfolio representing the ASX 200 accumulation index – capturing returns from both dividends and price growth – from the start of 2000 to May 2026.

Of course, it’s important to remember that past performance (whether actual or simulated) is not indicative of future performance, and actual outcomes will vary.

Let’s look at three strategies:

1. Dollar-cost averaging: Simply investing $100 a week into the ASX 200 (at the start of each Monday).

2. Perfectly buying the dips: Maggiulli’s “God” makes another appearance here, accumulating cash and then investing all of it into the market at the perfect time, being the lowest point between two all-time highs.

3. 10% dip hunting: We’re adding a third strategy that doesn’t require any divine foresight but still attempts to buy the dip. In this strategy, we are accumulating cash, then investing it all into the market as soon as it dips 10% below its highest point in the past 52 weeks.

Our results show that a weekly Dollar-cost averager over this period would have walked away victorious over both the 10% and the omniscient dip buyers. Dollar-cost averaging would have returned $30,000 more than both dip buyers, outperforming them by approximately 21% over the 26-year period:

Equally interesting: the 10% dip buyer actually beat the market timer by $18, simply due to the fact that they invested earlier and more often. Our results supports the position that time in the market beats timing the market. What’s the harm in holding out?

Why is dollar-cost averaging so powerful? The opportunity cost of waiting for the bottom is that you miss out on the powerful wealth-building force that is compounding.

In our hypothetical example, the perfect market timer may have perfectly timed the market, but the cost of waiting meant that they ended up with less. That is a textbook example of cash drag on a portfolio.

Meanwhile, our dollar-cost averager benefited from the power of compounding.

The longer you’re in the market, the longer your money can grow and the more dividends you’re paid. More dividends mean more compounding, creating more wealth.

Australian stocks have traditionally paid high dividends relative to the rest of the world, meaning there is a higher opportunity cost for not investing. The ASX has consistently averaged dividends around 4% ( and between 5% and 6% when factoring in franking credits)1, significantly better than the 2% to 4% averaged by peers like the UK, US, Germany, Canada and France2.

This is all a long way of stating a simple fact: the data suggests the longer you’re not investing, the longer you’re not receiving the benefits of compounding.

1. It’s important to note that not all Australian investors will be able to receive the full value of franking credits, with the benefit of franking credits depending on an investor’s individual tax position and eligibility.

2. Morningstar – Australia has the highest dividend yields in the world, so why the endless chase for even higher yields?