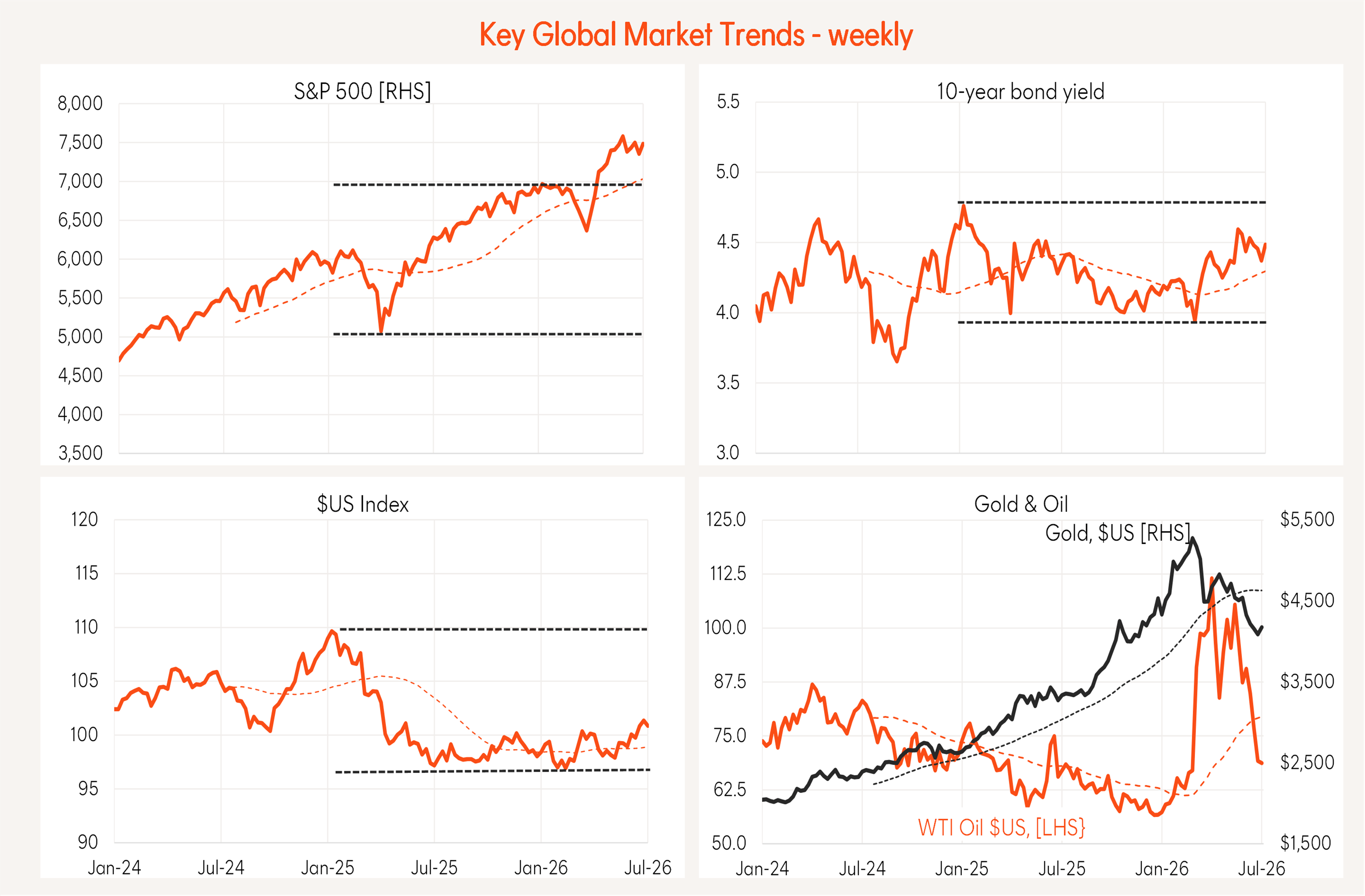

US equities lifted over the past week reflecting ongoing US-Iran ceasefire hopes, reduced fears of a near-term US interest rate increase and a degree of stability in the AI trade. The $US edged lower, helping the gold price to tick up.

Source: Betashares, Bloomberg.

Source: Betashares, Bloomberg.

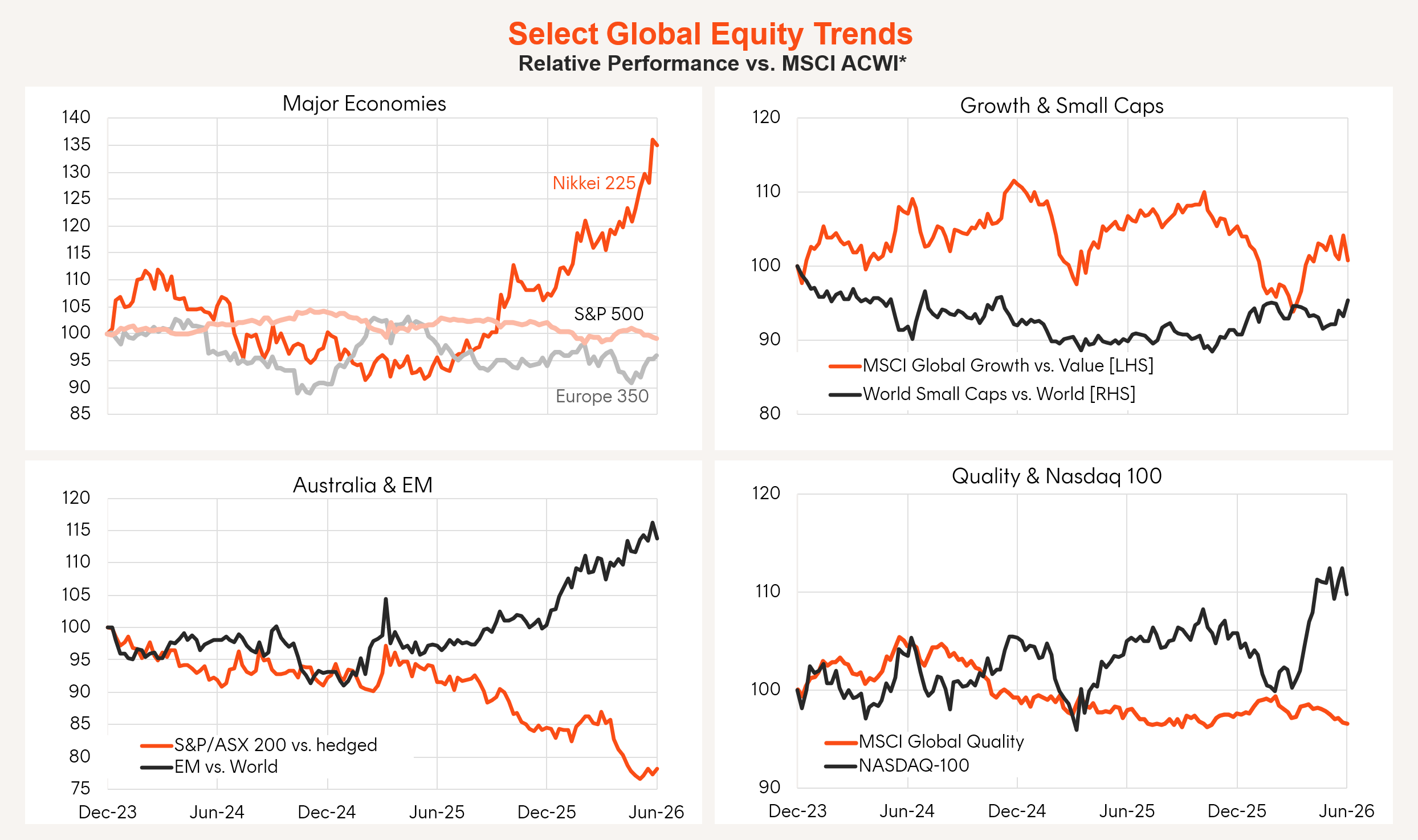

Although final details of the US-Iran peace deal are yet to be agreed, neither side attacked the other over the past week and ship traffic through the Strait of Hormuz is gradually recovering. Let’s take that as a win! Oil prices eased further, to be virtually back to where they were pre-war. From a market perspective, the US-Iran war appears to be fast becoming old news, which is perhaps a little premature given there’s yet to be clear agreement on 1) Iran’s stockpile of enriched uranium 2) release of Iran’s seized offshore assets and 3) Iran’s ability to impose tolls on ship traffic going forward. Iran appears to be playing a waiting game – waiting for the US to grow tired of the dispute and just cut and run. In other news, a softer-than-expected June US payrolls report – along with dovish comments from Fed chair Kevin Warsh – eased fears of a near-term US rate increase. US June employment rose only 57k, or about half the market’s expectation, although a decline in the participation rate meant the unemployment rate eased to 4.2%. All up, a good deal of the slowing in US employment appears to reflect reduced labour supply, rather than a slump in demand, as evident from the still low weekly jobless claims and unemployment rate. The good news is that wage growth, despite low unemployment, remains reasonably benign. Having been spooked two weeks ago by hawkish comments from newly installed Fed Chair, Kevin Warsh (reiterating the Fed’s determination to get inflation down), markets were happy to hear last week that he thought “inflation risks have come down” – presumably because of the decline in oil prices. Markets reckon there’s an 80% chance rates will remain on hold at the July Fed meeting, although they are still pencilling in the risk of one rate hike in the coming year. The third major factor driving global markets remains the AI trade. Meta’s announcement that it would sell cloud storage services had mixed effects on the market: it was a boost for Meta but hurt other cloud providers like Alphabet and Microsoft. There’s also a suspicion that Meta’s move may reflect the fact it has overbuilt its data centre capacity – playing into AI bubble fears. The AI bubble debate seems likely to continue to wax and wane. There’s little major global data this week, with a focus likely to be the minutes from the recent Fed meeting due out Wednesday night. With the “dot plot” of that meeting suggesting a majority of Fed members felt rates should be higher by year-end, markets are bracing for potential hawkish accompanying commentary. Although global technology bounced back a little last week, it still underperformed, with better gains in a range of sectors like health care, financials, consumer discretionary, industrials and materials. Overall, the once strong trend of technology/AI outperformance appears to be wavering, with investors seeking shelter in more defensive exposures.

All but value factors. Local currency basis. Source: Betashares, Bloomberg.

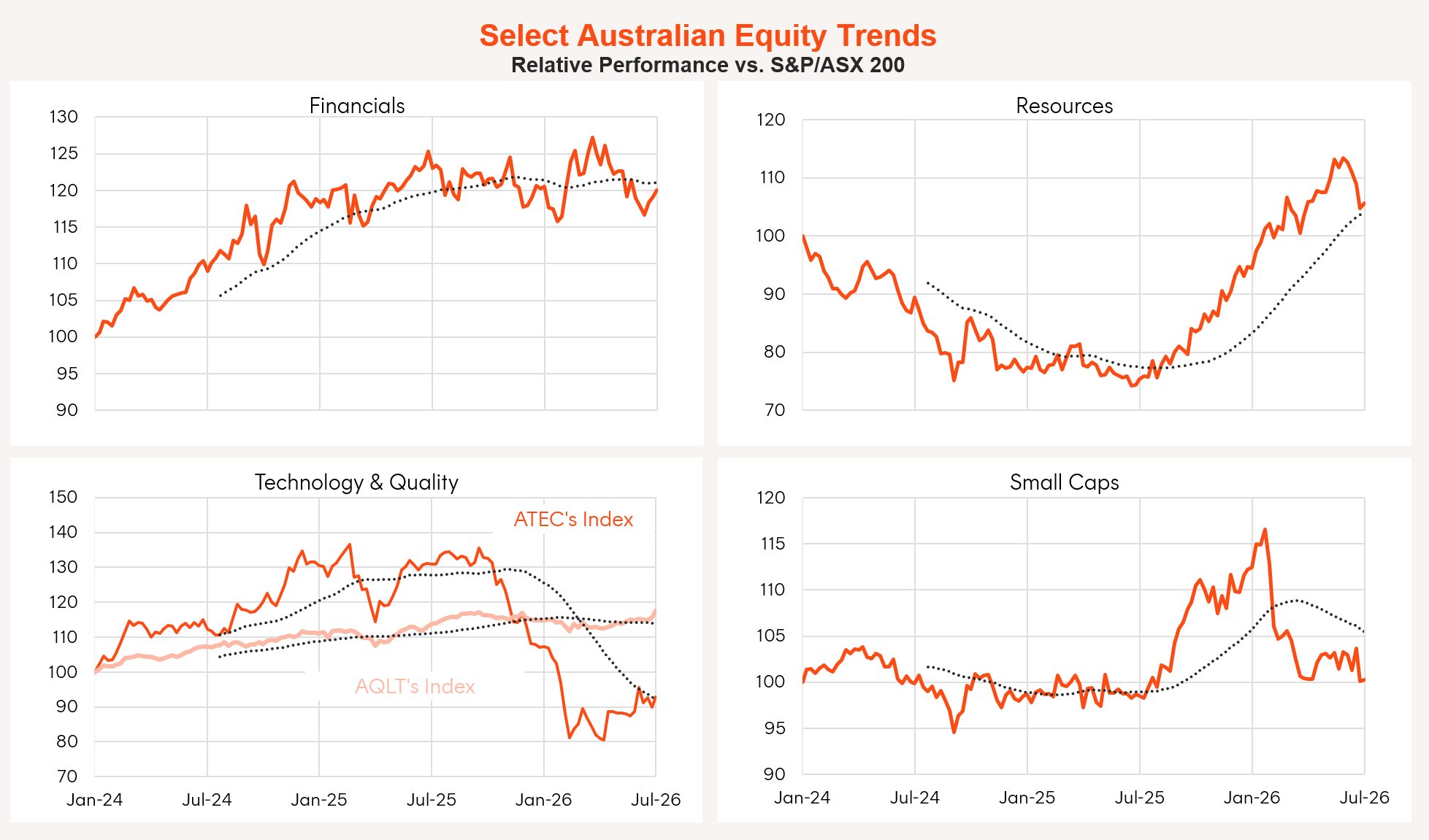

The local equity market also lifted last week but underperformed the global market once again. The $A firmed a little as easing US interest rate fears dented the $US. The local highlight last week was June house price data, confirming what subdued auction clearance rates were already telling us: namely, house prices are retreating. National prices edged 0.4% lower in the month, with 1% declines in the major markets of Sydney and Melbourne. With one third of the market – investors – deserting the market, fear of missing out or “FOMO” among non-investors has given way to “FOBE” or fear of buying early. If there’s any saving grace, it’s that the added negative impact of the Federal Budget on the housing sector, and business/consumer sentiment in general, has lessened the chances of further Reserve Bank rate hikes this year. In last week’s minutes from the June RBA policy meeting, the Bank did retain a firm tightening bias, although “members noted that conditions in the housing sector had eased by more than expected”. As regards the Federal Budget, recent government commentary now suggests there were two objectives: 1) even the playing field between housing investors and first home buyers and 2) even the tax playing field between workers and those who rely on income from capital. As regards the former, my main grumble is that it was pretty heavy-handed – removing all tax benefits with regard to investing in established property rather than limiting those benefits to maybe only one or two properties. This could still have allowed younger investors opportunities, through strategies such as “rent-vesting”. As regards the latter, my grumble is that the Government has levelled the playing field, but by simply extending the very onerous tax regime on labour income to capital income, and both are now very heavily taxed by global standards. It’s also arguable that income from active capital investments (e.g. start-up businesses) produces more positive externalities in terms of employment and innovation, justifying somewhat more generous tax treatment. Either way, although the Government has dealt with concerns over implied “death” and “widower” taxes, there still appear several oddities with the newly installed system: Health care was a standout performer last week, which in turn helped the quality factor (AQLT ETF). More broadly, financials appear to be bouncing back relative to resources, while the underperformance of small caps and technology seems to be bottoming out.

Source: Betashares, Bloomberg.

There’s little in the way of major economic data locally this week, with a highlight likely to be a speech from RBA Assistant Governor Sarah Hunter on Wednesday. Have a great week!

Global week in review: Iran and interest rate hopes

Global week ahead: Fed minutes

Global equity trends: Tech wobbles

Australia week in review: House price weakness

Lingering budget thoughts – I can’t help myself!

– Borrowing to buy new properties is now banned within SMSFs, but it’s OK outside of them.

– The inability to net-off real capital losses against real capital gains will result in a potentially prohibitively high effective tax rate on diversified investment portfolios.

– An arbitrary “innovativeness” test will be applied by bureaucrats to decide which start-up business will get special treatment through more favourable capital gain tax treatment.

– Even though it may take years to earn a capital gain from the sale of a business, there’s no provision for tax averaging to lessen the tax bill – the gain is treated as if it was earned in a single year.

– A minimum 30% CGT means that, for some on low incomes, taxes on capital will be higher than those on labour income.

– A mad rush for valuations on millions of assets now seems necessary at the end of this financial year.

Local equity market trends: Health care & quality

Australia week ahead: RBA speak

This content is for financial adviser use only.

By clicking on 'Financial professional', you certify that you are an Australian financial services licensee or authorised representative, and are authorised to provide personal advice to retail clients in relation to managed investment schemes.