Defensive assets are finally earning something again. After years of near-zero rates, a savings account is paying a bit more, and that may have made cash feel like the natural home for this part of your portfolio.

But cash has quiet costs over a horizon longer than a year.

Overnight savings is usually the lowest-earning rung. A term deposit pays a little more, but it locks your money away to a set date, and you need to do the legwork reinvesting it.

When it comes to investing, for the defensive dollar there is a step up from cash that still seeks to provide capital stability.

Bank bonds sound intimidating, but the idea is simple

A bank bond is just a loan. When you buy one, you are lending money to a borrower, in this case a bank, and in return they pay you regular interest and give your money back at the end.

The difference is that bonds are standardised and can be traded, so you are not locked in; you can buy and sell them day to day, and their price moves in between. What moves that price is the interest rate. A fixed-rate bond locks its rate in, so if official rates rise, the price of that bond falls (a new bond now pays more, making the old one worth less). A floating rate bond resets its rate in line with the cash rate, so the price barely moves and the income rises and falls with rates instead. Fixed rate bonds have much more interest rate risk than floating rate bonds and tend to be more volatile.

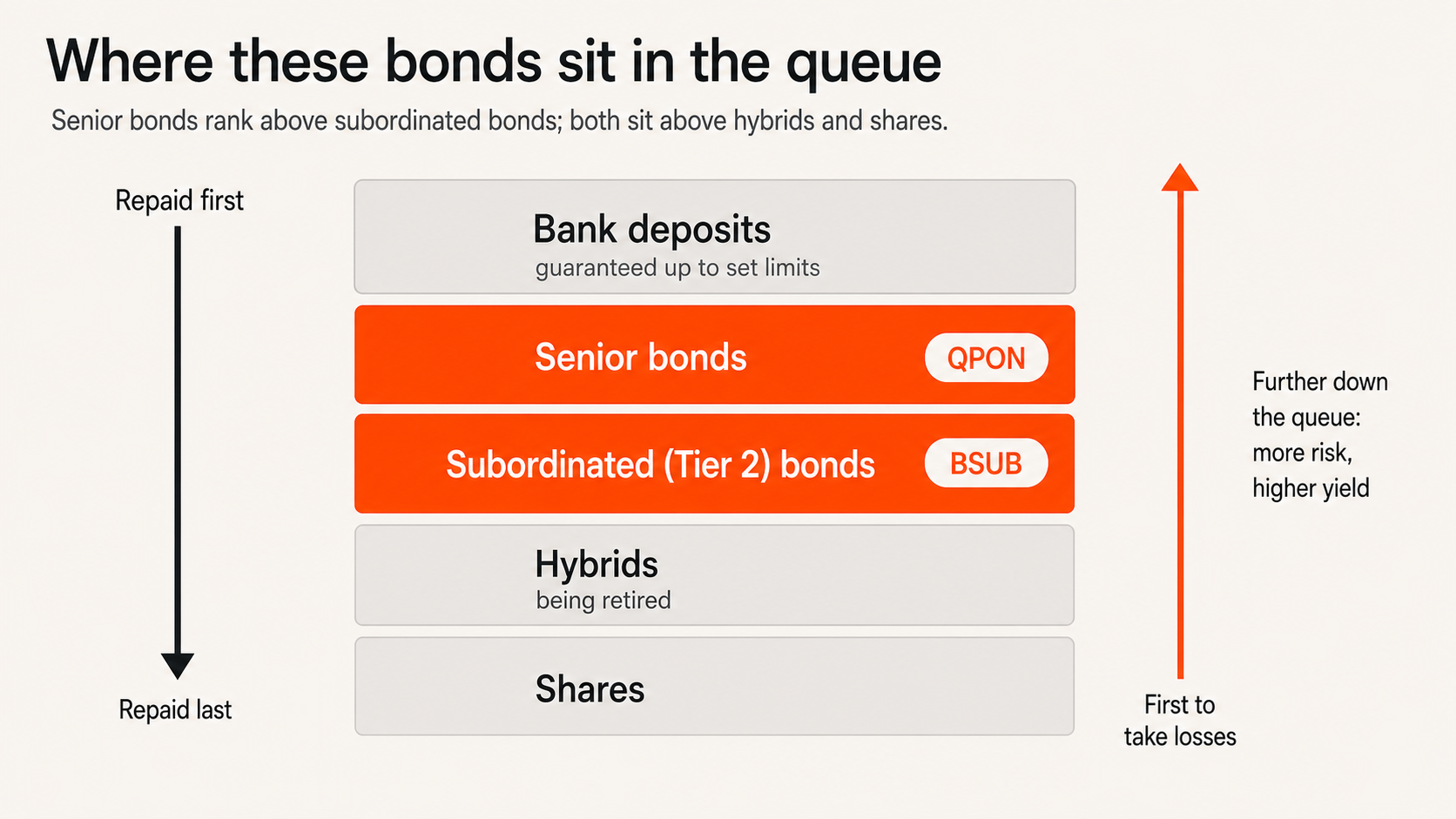

How to think about it: the bank capital structure

Picture a queue to get paid if a bank ever ran into trouble and became insolvent. Bank deposits sit at the top and are government-guaranteed up to set limits. Senior bank bonds are next, then subordinated (Tier 2) bonds, then hybrids, with shares right at the bottom. The further down the queue, returns and yields typically increase as compensation for the higher risk.

That queue is one dimension of risk: credit risk, being the risk that borrowers may default on their obligations. The other, interest rate risk, refers to the possibility that the value of a bond may change due to rising or falling interest rates. This depends on whether the bond is fixed or floating. Floating rate bonds protect you from rising interest rates. Where a bond sits in the queue is a separate thing, about who gets repaid first if a bank ever got into trouble. Senior bonds sit near the top and subordinated bonds are below, which is why they pay a bit more.

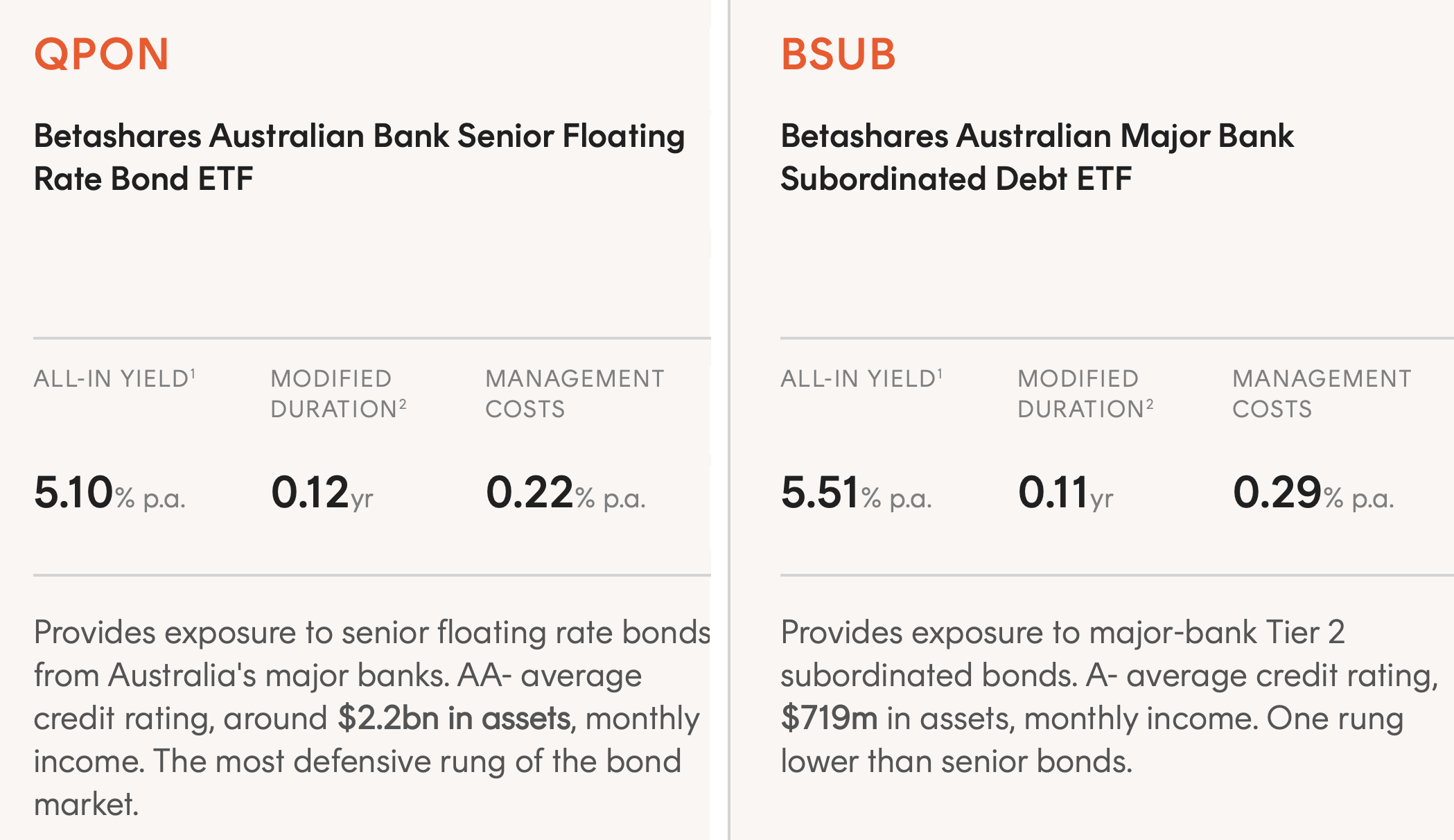

QPON: the first step

QPON Australian Bank Senior Floating Rate Bond ETF holds senior floating rate bonds from the ‘big 4’ banks you already deal with, with around 80 per cent in the big four and the remainder in other large Australian banks. These are the most defensive rung of the bond market, near the top of the queue.

It is Australia’s first floating rate bond ETF, with a track record of nearly a decade across rate rises, cuts and on-hold periods. It pays income monthly, has management costs 0.22% p.a., and is currently offering an all-in-yield of around 5.10% p.a. (as at 7 July 2026). Because the interest payments are floating rate and benchmarked to the 3-month bank bill swap rate (BBSW), that figure should be expected to move with the cash rate.

BSUB: a step up for those ready for it

BSUB Australian Major Bank Subordinated Debt ETF holds subordinated bonds which are one rung down the queue. As Tier 2 subordinated debt, it is loss-absorbing bank capital, designed to take losses before depositors and senior bondholders if a bank ever reached the point of non-viability.

That makes it suited to a holding of three years or more. BSUB holds only subordinated bonds issued by the ‘big-four’ banks and like QPON has next to no sensitivity to rate moves. It has management costs of 0.29% p.a., and reflecting its lower ranking in the capital structure hierarchy, currently has a higher yield than QPON to compensate for the higher risk. As bank hybrids retire, Tier 2 is where much of that role is moving.

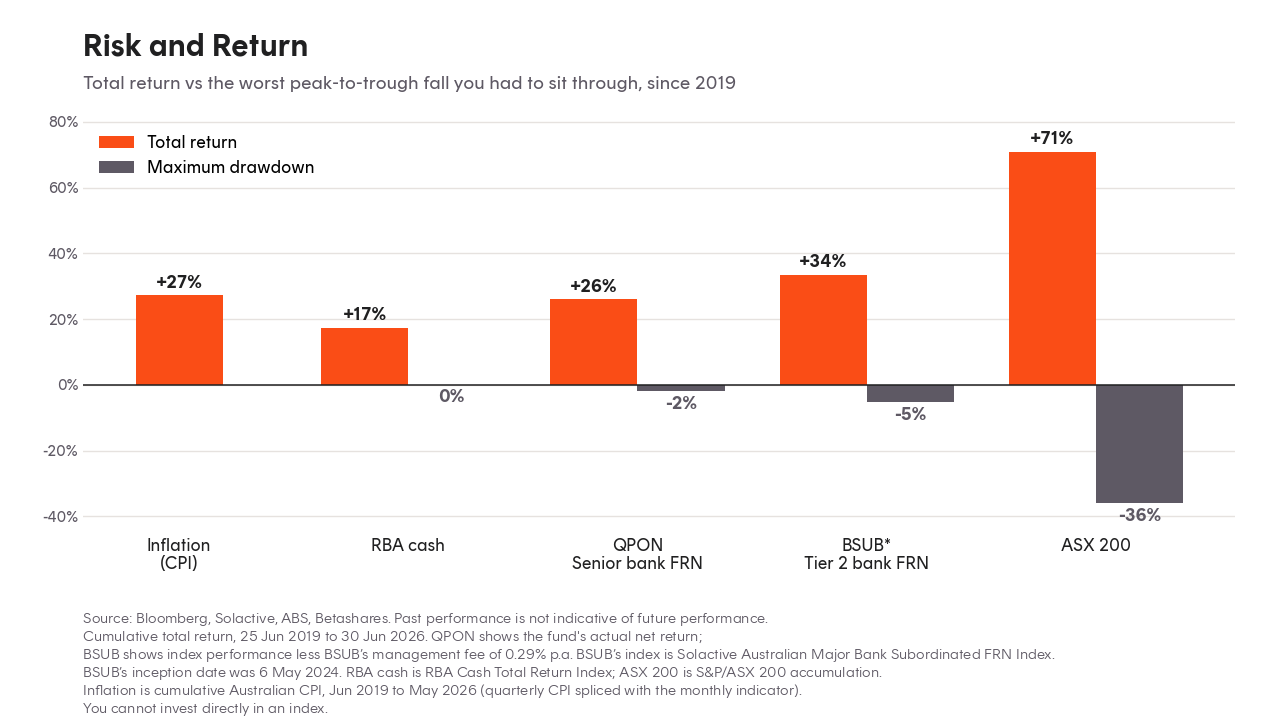

The past seven years show the trade-off: the defensive rungs have displayed limited capital variability, while shares paid the most but fell the hardest.

What these Funds are, and what they are not

QPON and BSUB carry investment risk and, unlike bank deposits are not covered by any government guarantee. Risks include interest rate, credit risk and, in the case of BUSB, subordinated ranking risk and subordinated bond risk. The unit price moves day to day with changes in credit spreads, and your capital is not guaranteed. What you get in return is a yield typically above cash and term deposits, daily access on the ASX with no lock-up and no break costs, and monthly income. The admin is light, with one annual tax statement, no maturity to track and no reinvestment to organise. Unlike a term deposit, you are not tied to a maturity date, and if your plans change, you can sell on any trading day.

For investors comfortable with the risk, floating rate bank bonds may be worth considering as a meaningful upgrade to cash and term deposits.

QPON and BSUB at a glance

As at 7 July 2026

1. ‘All-in Yield’ refers to the sum of a Floating Rate Note’s (FRN) Discount Margin and its reference benchmark rate. The Fund’s all-in yield is the weighted average of its underlying securities’ all-in yields. Discount Margin (DM) refers to the difference or spread between the expected return of a FRN security and that of its underlying index, expressed as a margin above the underlying reference benchmark rate. The Fund’s DM is the weighted average of its underlying securities’ DMs. For AUD FRN securities, the reference benchmark rate is the Bank Bill Swap Rate (BBSW). For securities with optionality, this is the DM to first call, where the calculation replaces the security maturity date with its first call date.

2. ** Modified duration is a measure of the sensitivity of the portfolio’s value to a change in interest rates, e.g. modified duration of 0.15 years implies a 1% rise in the reference interest rate will reduce portfolio value by 0.15%.