What will the long-term portfolio takeaways from the Iran war be?

Key points

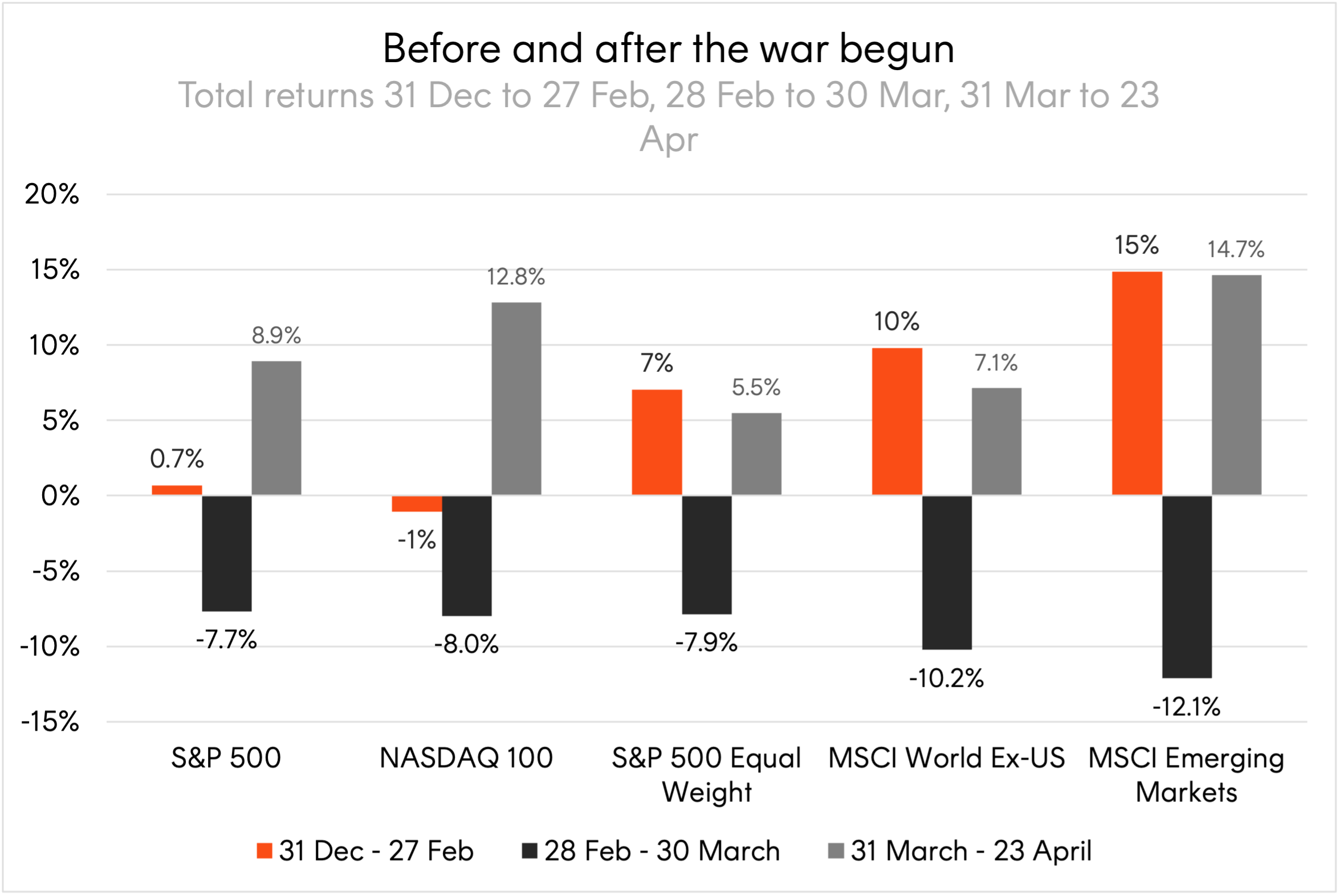

In the first two months of 2026, markets followed the playbook. Developed market equities outside the US, and emerging market equities, were outperforming with a strong global growth outlook and a weakening US dollar. Gold was trading above US$5,000 an ounce for the first time while US indices were treading water on AI jitters.

Then, on the last day in February, the US invaded Iran and began a war that remained ongoing towards the end of April.

What Trump may have hoped would be a swift operation, toppling the existing leadership and spurring protesters to install a new government, has instead become his trickiest geopolitical entanglement yet. Equity markets pared their early year gains to be trading down across the world over March – they have more recently rebounded on hopes of a resolution.

Source: Bloomberg. Total returns of select indices from 31 December to 27 February, 28 February to 30 March, 30 March to 23 April. You cannot invest directly in an index. Past performance is not an indicator of future performance.

The short-term threat is the hit to global growth and the inflationary pressure from higher oil prices. Given the recency of the shock, its impact will only show up in hard economic data with a lag. Put simply, the longer the war runs, the greater the risk of global recession. Our base case assumption remains a timely de-escalation without a severe shock to the global economy.

But in any case, it may be the longer-term implications that matter most for investors, long after any resolution in Iran.

Re-thinking portfolio satellites in a fracturing world

Portfolio satellites are used by investors alongside their main holdings to achieve specific goals. More than ever, some investors may consider using these satellites as hedges to geopolitical events.

Russia’s invasion of Ukraine accelerated defence spending and European energy diversification. The Iran conflict is now doing the same for global energy self-sufficiency while further fracturing the US security umbrella and embedding geopolitics as a structural driver of asset prices, rather than a short-lived disruption that markets quickly move past.

For investors, that may support the case for considering select hedges in portfolios to help reduce volatility through a potentially prolonged period of geopolitical tension and global order reshuffling. These include:

Defence contractors

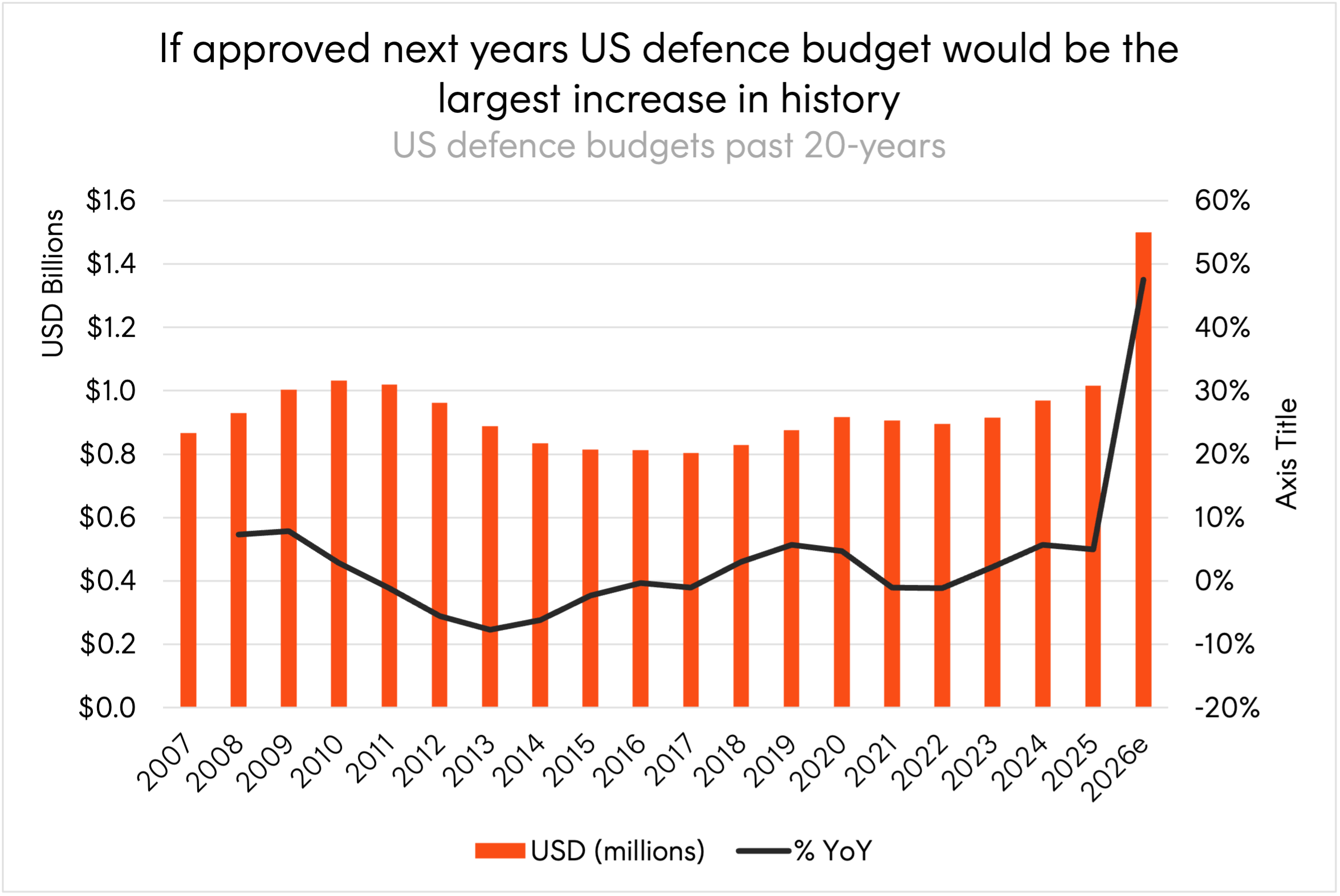

Global defence stocks have been among the best performing since the start of Trump’s second presidential term. In April of 2026 the US proposed a US$1.5 trillion defence budget for FY27, the largest in history and a 50% increase on FY26.

Source: SIPRI Military Expenditure Database, Betashares. 2007 to 2025. 2026e reflects proposed budget. Actual results may differ materially from forecasts.

Across the Atlantic, Europe’s rearmament is accelerating. EU defence budgets have nearly doubled from €218 billion in 2021 to a projected €392 billion in 20251, marking the first year all EU-NATO members have hit the 2% of GDP threshold. To unlock additional fiscal room, 17 member states have activated the EU’s national escape clause, permitting defence spending above Stability and Growth Pact limits through 20282. Germany alone has committed to €162 billion by 20293.

The direction of travel is clear, and defence contractors globally could be structural beneficiaries and a potential hedge to geopolitical threats that can cause broader equity market disruption.

ARMR Global Defence ETF is a simple way for Australian investors to gain exposure to the potential long term structural growth in the global defence sector.

ARMR’s index seeks to provide focused exposure to companies that are predominantly involved in defence, specifically those which derive more than 50% of their revenues from the development and manufacturing of military and defence equipment as well as defence technology.

ARMR currently holds 13 of the top 20 defence contractors in the world by defence revenue1, including US and European defence leaders like Lockheed Martin, Palantir Technologies, BAE Systems, Rheinmetall, and Thales (the 7 companies in the top 20 not held are either not ‘pure-play’ or not headquartered in NATO-aligned countries).

Uranium and energy security

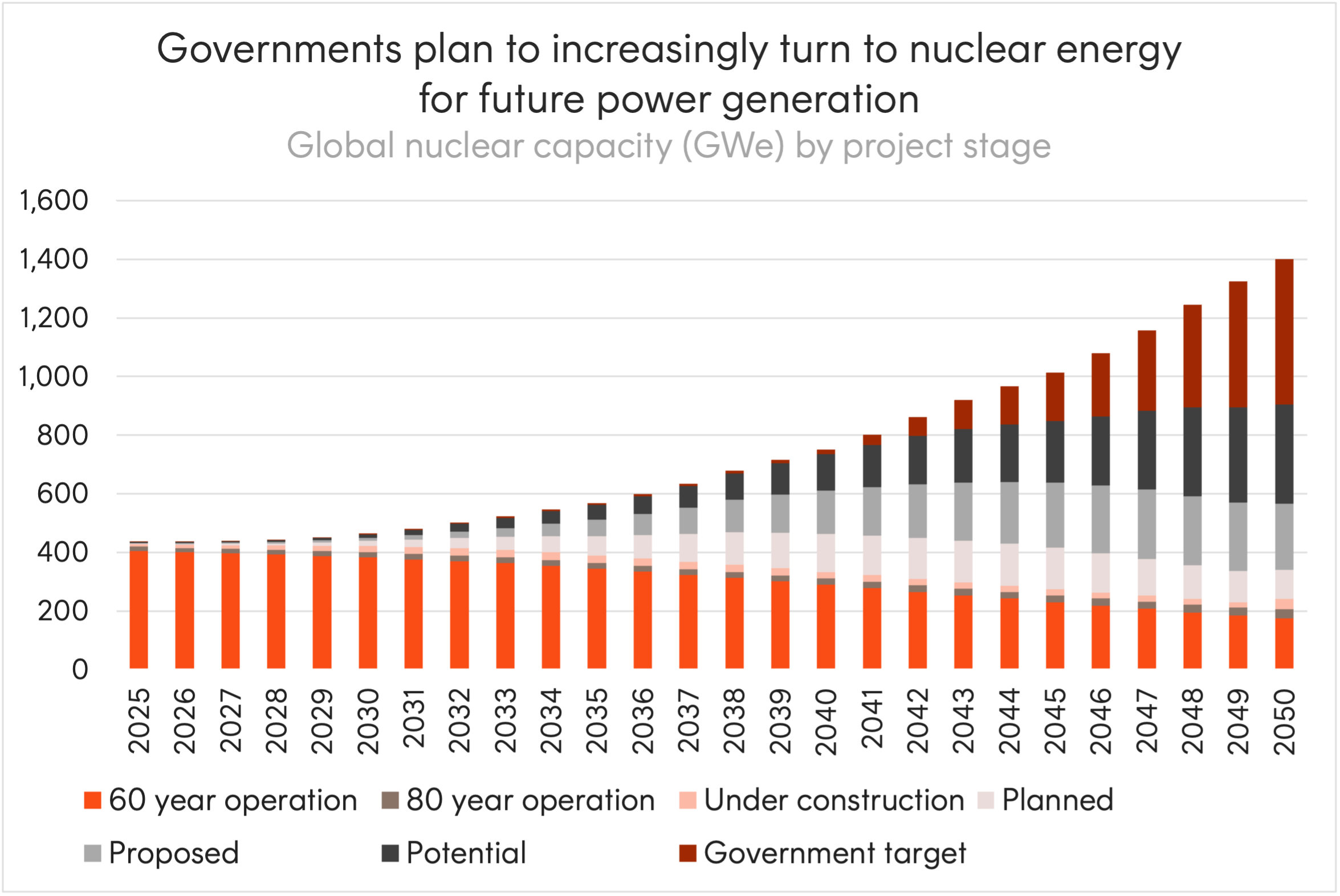

Russia’s invasion of Ukraine and the subsequent scramble to wean Europe off Russian oil and gas thrust energy security to the top of the policy agenda. The Iran conflict has now re-ignited energy self-sufficiency concerns globally. As governments reassess their baseload power (the minimum level of electricity a grid needs around the clock) and seek to reduce dependence on hostile suppliers, nuclear energy has re-emerged as a cornerstone of the solution.

As of the most recent COP30 (the United Nations annual climate change conference), 33 countries, including the US, France, UK, Japan, South Korea, Canada and the UAE, now back the pledge to triple global nuclear capacity by 2050.

Source: World Nuclear Association (WNA). Assessment of global nuclear capacity (GWe) up to 2050.

With nuclear increasingly recognised as essential for energy independence, decarbonisation and AI-driven electricity demand, the uranium supply chain may be entering a period where demand outpaces supply, which could favour producers in allied nations.

URNM Global Uranium ETF provides exposure to a portfolio of leading companies in the global uranium industry.

URNM was the first uranium-focused equities ETF traded on the ASX. It provides exposure to a portfolio of global companies involved in the mining, exploration, development and production of uranium, plus companies that hold physical uranium or uranium royalties.

Investing in URNM can reduce stock-specific and geographic risk compared to investing in individual uranium companies – an important consideration given the risks associated with individual projects in the uranium industry.

Critical minerals

Critical minerals, inputs essential for AI data centres, EVs, renewable energy and defence technology, are at the intersection of future technologies and geopolitics.

China controls over 60% of global refined critical mineral supply and 90% of rare-earth magnets. In response, estern allies are moving decisively: in February, ministers from 54 countries discussed a US proposal to reduce dependence on Chinese supply, while the EU, Japan, Mexico and the US agreed to create price support mechanisms and capital backing for critical mineral projects.

Both the US and Australia have established strategic mineral reserves, and the latest US defence budget dramatically expands investment in domestic critical mineral supply chains. Selected producers from allied nations, Australia, Canada, Peru and Chile, could be well positioned to benefit from this government-backed push for supply chain resilience.

XMET Energy Transition Metals ETF provides Australian investors with targeted exposure to global companies at the heart of the critical minerals supply chain.

XMET focuses on companies predominantly involved in the production of eight key energy transition metals – copper, lithium, nickel, cobalt, graphite, manganese, silver and rare earth elements – as well as companies involved in the recycling and processing of these raw materials.

With geopolitical competition intensifying around mineral supply chains and demand accelerating from both the energy transition and AI-driven infrastructure, investing in a diversified basket through XMET reduces the single-stock and project-specific risks that come with investing in individual critical mineral companies.

There are risks associated with an investment in ARMR, URNM and XMET, including market risk, sector risk and concentration risk. Investment value can go up and down. An investment in the Funds should only be considered as a part of a broader portfolio, taking into account your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Funds, please see the Product Disclosure Statement and Target Market Determination, both available on this website.

The information contained in this article is general information only and does not take into account any person’s financial objectives, situation or needs. Investors should consider the appropriateness of the information taking into account such factors and seek financial advice. This article is provided for information purposes only and is not a recommendation to make any investment or adopt any investment strategy.

Future outcomes are inherently uncertain. Actual outcomes may differ materially from those contemplated in any opinions, estimates or other forward-looking statements given in this article.

Past performance is not indicative of future performance. No assurance is given that any of the companies in a Fund’s portfolio will remain in the portfolio or will be profitable investments.

1. European Defence Agency, Defence Data 2024-2025; European Parliament Research Service, ‘EU defence funding’, October 2025.

2. European Commission, Readiness 2030 / ReArm Europe plan, March 2025.

3. European Parliament Research Service, ‘EU Member States’ defence budgets’, March 2026.

4. Source: Defense News, Top 100 for 2025 list. Data for the Top 100 list comes from information Defense News solicited from companies, from companies’ earnings reports, from analysts, and from research by Defense News, the International Institute for Strategic Studies and SPADE Indexes.

5. IEA, Global Critical Minerals Outlook 2025.