Tom Wickenden

6 minutes reading time

Financial intermediary use only. Not for distribution to retail clients.

Key takeaways:

- After years of strong returns, global defence stocks have paused over the past six months. European defence stocks in particular have de-rated, resetting valuations to more attractive levels.

- The pause comes despite major defence contractor order books growing by US$100 billion in 2025, now exceeding US$1 trillion for the first time in history.

- For long-term investors, these conditions may represent a compelling entry point into a sector that is being used by some investors as a “geopolitical hedge” amid ongoing global conflict and uncertainty.

- Investors seeking access may consider targeted exposure to the defence sector via ARMR.

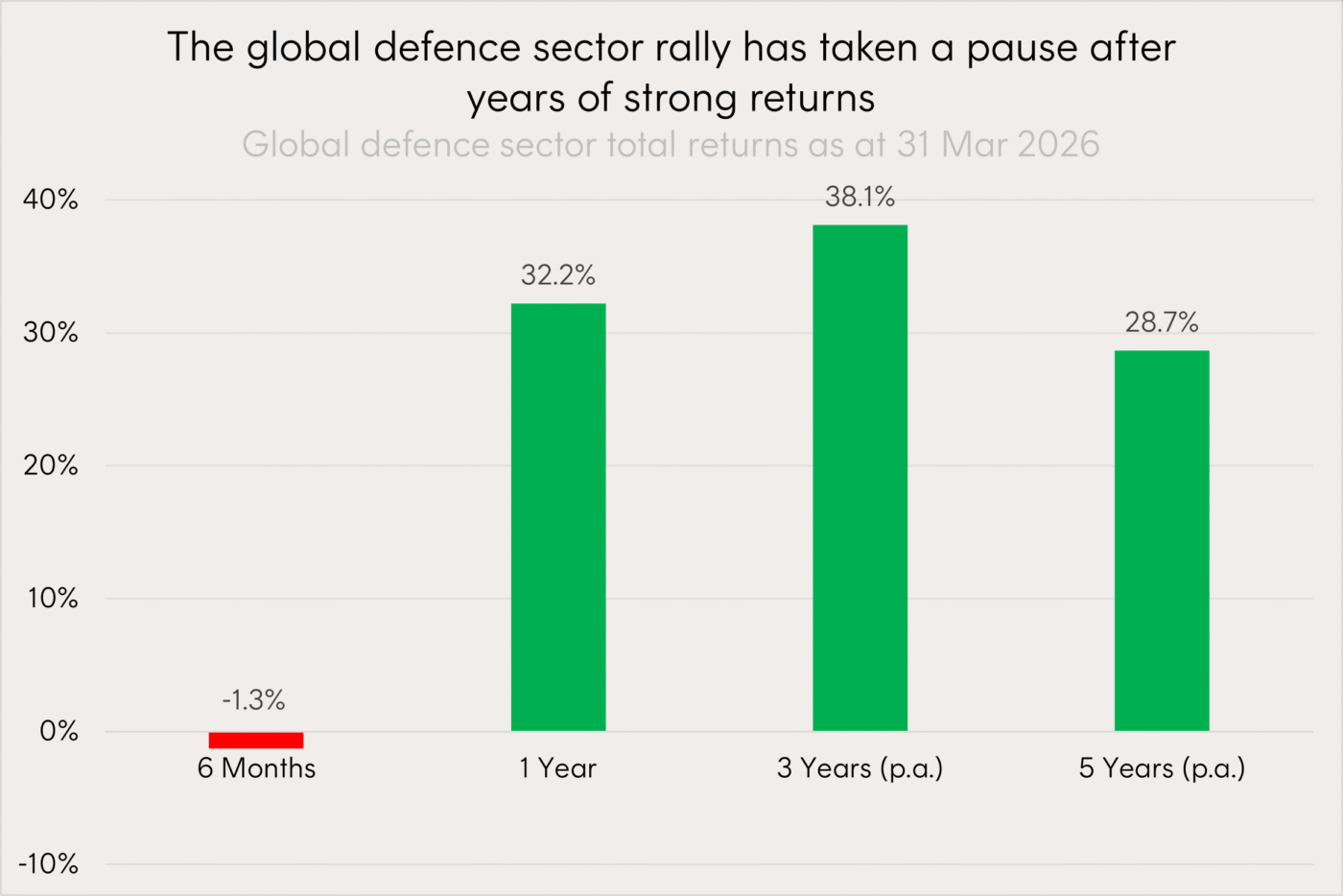

Having returned 29.0% p.a. over the past 5 years, the global defence sector’s performance has more recently plateaued, returning -1.8% over the past 6 months[1].

The performance slump comes at a counterintuitive time as the US’s war in Iran depletes American stockpiles and emphasises Europe’s self-security needs.

Source: Bloomberg. As at 31 March 2026. Returns of the VettaFi Global Defence Leaders Net Total Return Index. You cannot invest directly in an index. Past performance is not an indicator of future performance.

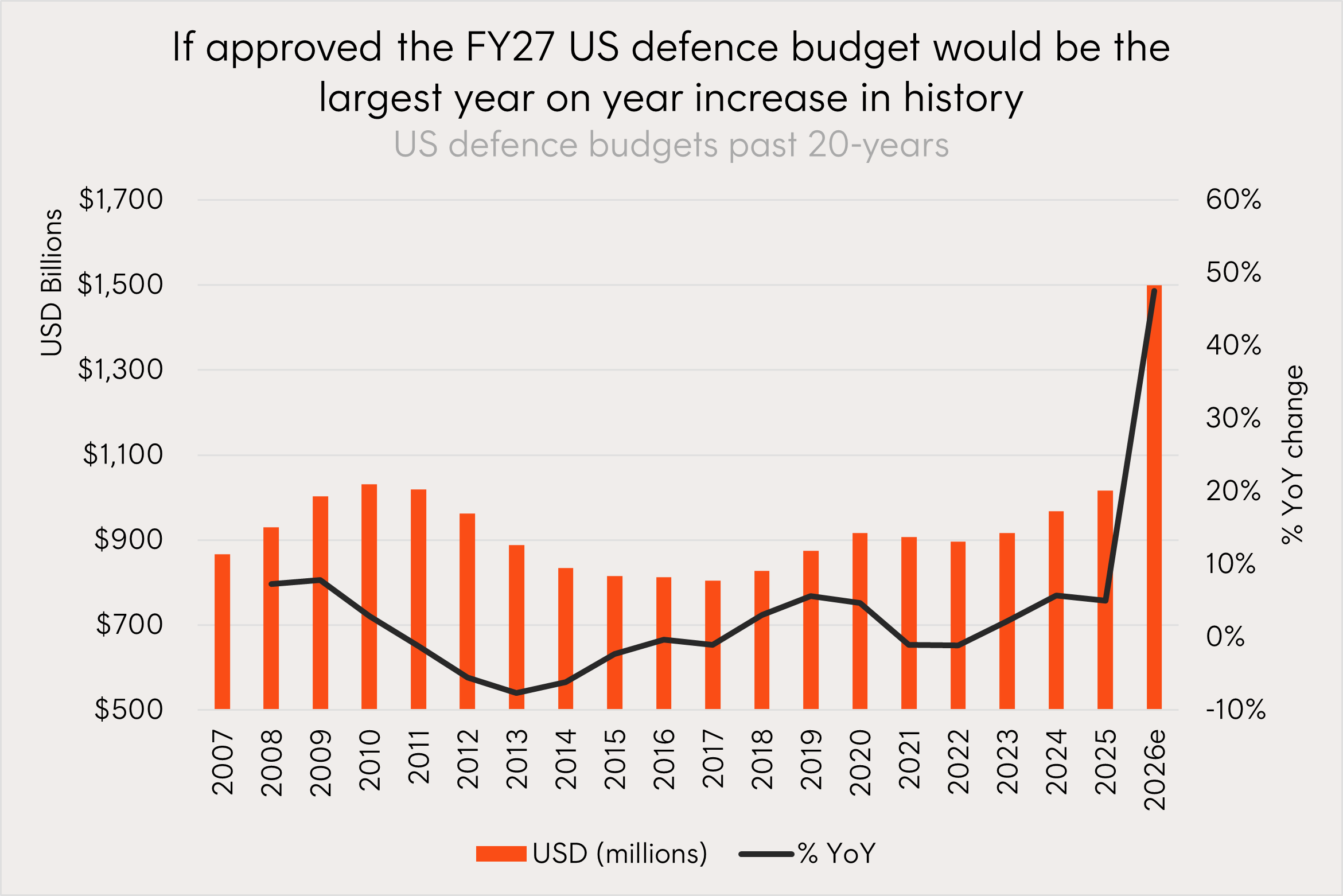

The Center for Strategic and International Studies (CSIS) estimated the first 12 days of Operation Epic Fury cost the US approximately US$16.5 billion[2], accelerating the US administration’s already ambitious defence spending plans. The FY27 budget released in April calls for ~US$1.5tn in defence spending representing ~44% growth from FY26. If approved this would represent both the largest nominal request and most significant year-on-year defence budget growth in history[3].

A budget of this magnitude would support both the existing US defence primes and emerging disruptors necessary for the future of warfare which will require advanced hardware, AI-enabled software, autonomy, cyber capabilities, and scaled manufacturing processes.

Source: SIPRI Military Expenditure Database, Betashares. 2007 to 2025. 2026e reflects proposed budget. Actual results may differ materially from forecasts.

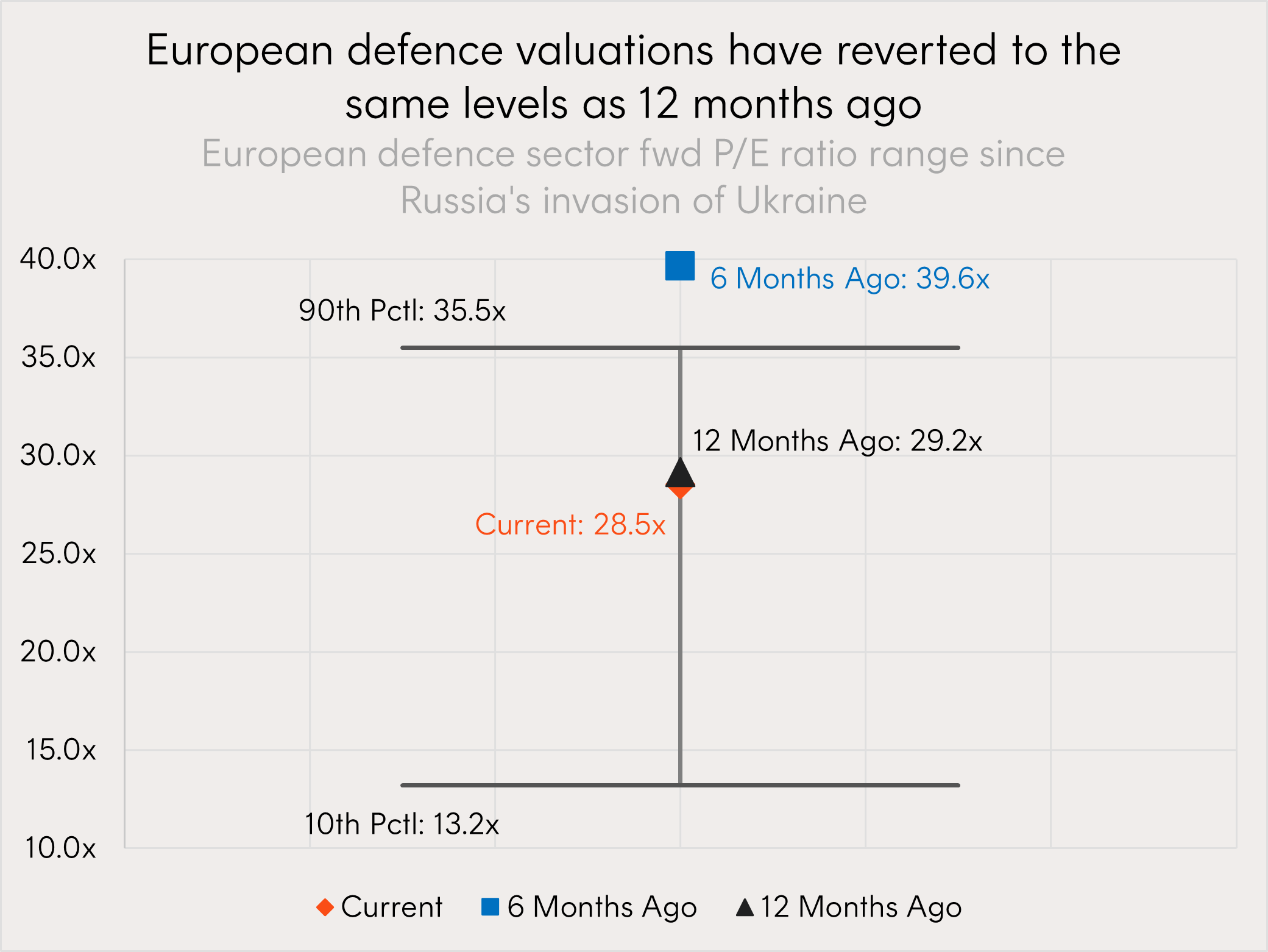

European defence companies have been the main contributors to the recent performance drag for the global sector. Following significant gains last year on increased spending plans, including NATO’s 5% of GDP commitment and Germany’s historic debt reform, investors have taken a pause noting high valuations and the time lag between spending plans and earnings realisation.

The necessity for Europe to increase defence spending for security self-sufficiency has only been heightened during the Iran conflict with renewed threats of the US leaving NATO. Further, European defence contractor valuations are now 26% lower than six months ago, having reset to levels they were trading at this time last year[4].

The current pullback may offer long-term investors an attractive entry point into a sector with durable earnings drivers and growing relevance as a potential “geopolitical hedge”. While valuations remain elevated these multiples increasingly reflect the market’s expectation of sustained earnings growth rather than speculative premium.

Source: Bloomberg, Betashares. 24 February 2022 to 31 March 2026. 10th and 90th percentile range. Past performance is not an indicator of future performance.

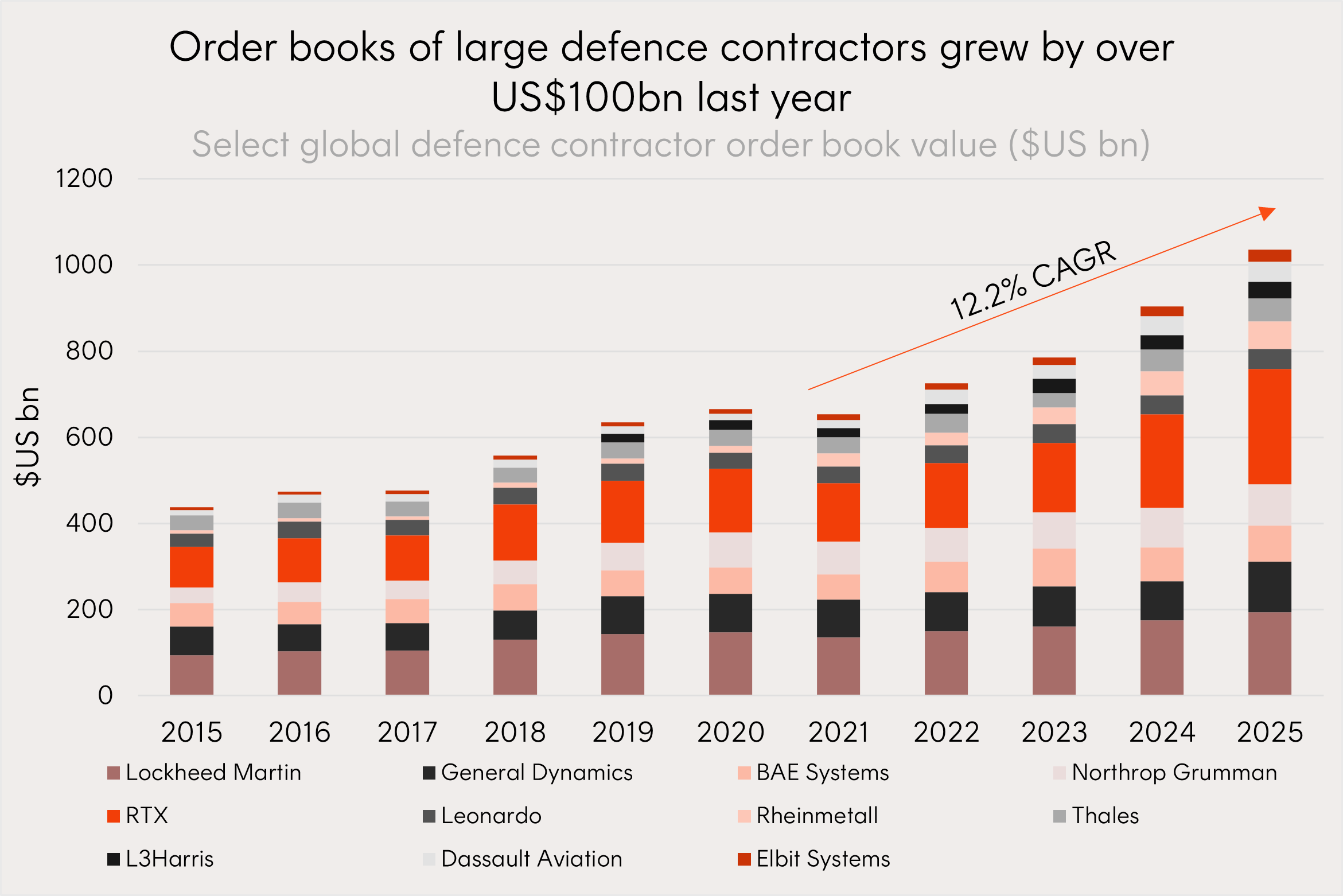

As a result of global spending developments, for the second year in a row, major defence contractors saw their order books grow by over US$100bn[5]. The defence contractor order books we track now collectively exceeded US$1 trillion for the first time in history [6]. Record levels of contracted future orders are a leading indicator of earnings growth supporting prospects for a longer-term structural rally in defence companies.

Source: Bloomberg, Betashares. Backlog order book value of select global defence contractors 2015 to 2025.

Investment implications

While the Iran war should lead to an increase in spending to restock US inventories and re-highlights the necessity of Europe to get serious about defence spending it may be the longer-term implications that matter most for investors, long after any resolution in Iran.

Russia’s invasion of Ukraine accelerated defence spending, Trump coming back into power fractured the US security umbrella, and now the Iran conflict is embedding these geopolitical trends as a potential structural driver of asset prices, rather than an episodic risk to be faded.

For investors, that argues for long term allocations to select exposures such as defence companies going forward, as part of a broader equities allocation.

ARMR Global Defence ETF is a simple way for Australian investors to gain exposure to the potential long term structural growth in the global defence sector.

ARMR’s index seeks to provide pure-play exposure to leading companies that are headquartered in NATO or closely aligned countries, and which derive more than 50% of their revenues from the development and manufacturing of military and defence equipment as well as defence technology.

ARMR currently holds 13 of the top 20 defence contractors in the world by defence revenue[7], including US and European defence leaders like Lockheed Martin, Palantir Technologies, BAE Systems, Rheinmetall, and Thales (the 7 companies in the top 20 not held are either not ‘pure-play’ or not headquartered in NATO-aligned countries).

There are risks associated with an investment in ARMR, including market risk, sector risk and concentration risk. Investment value can go up and down. An investment in the Fund should only be considered as a part of a broader portfolio, taking into account your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Fund, please see the Product Disclosure Statement and Target Market Determination, both available on this website.

- Source: Bloomberg. As at 31 March 2026. Returns of the VettaFi Global Defence Leaders Net Total Return Index. You cannot invest directly in an index. Past performance is not an indicator of future performance. ↑

- Source: 13 March 2026. Center for Strategic and International Studies. Iran War Cost Estimate Update: $11.3 Billion at Day 6, $16.5 Billion at Day 12 ↑

- Source: Budget of the U.S. Government, The White House. 4 April 2026. ↑

- Source: Bloomberg. As at 31 March 2026. ↑

- Source: Bloomberg, Betashares. Backlog order book value of select global defence contractors 2015 to 2025. ↑

- Source: Bloomberg. Based off company filings. As at 31 March 2026. ↑

- Source: Defense News, Top 100 for 2025 list. Data for the Top 100 list comes from information Defense News solicited from companies, from companies’ earnings reports, from analysts, and from research by Defense News, the International Institute for Strategic Studies and SPADE Indexes. ↑