David Bassanese

6 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the player below:

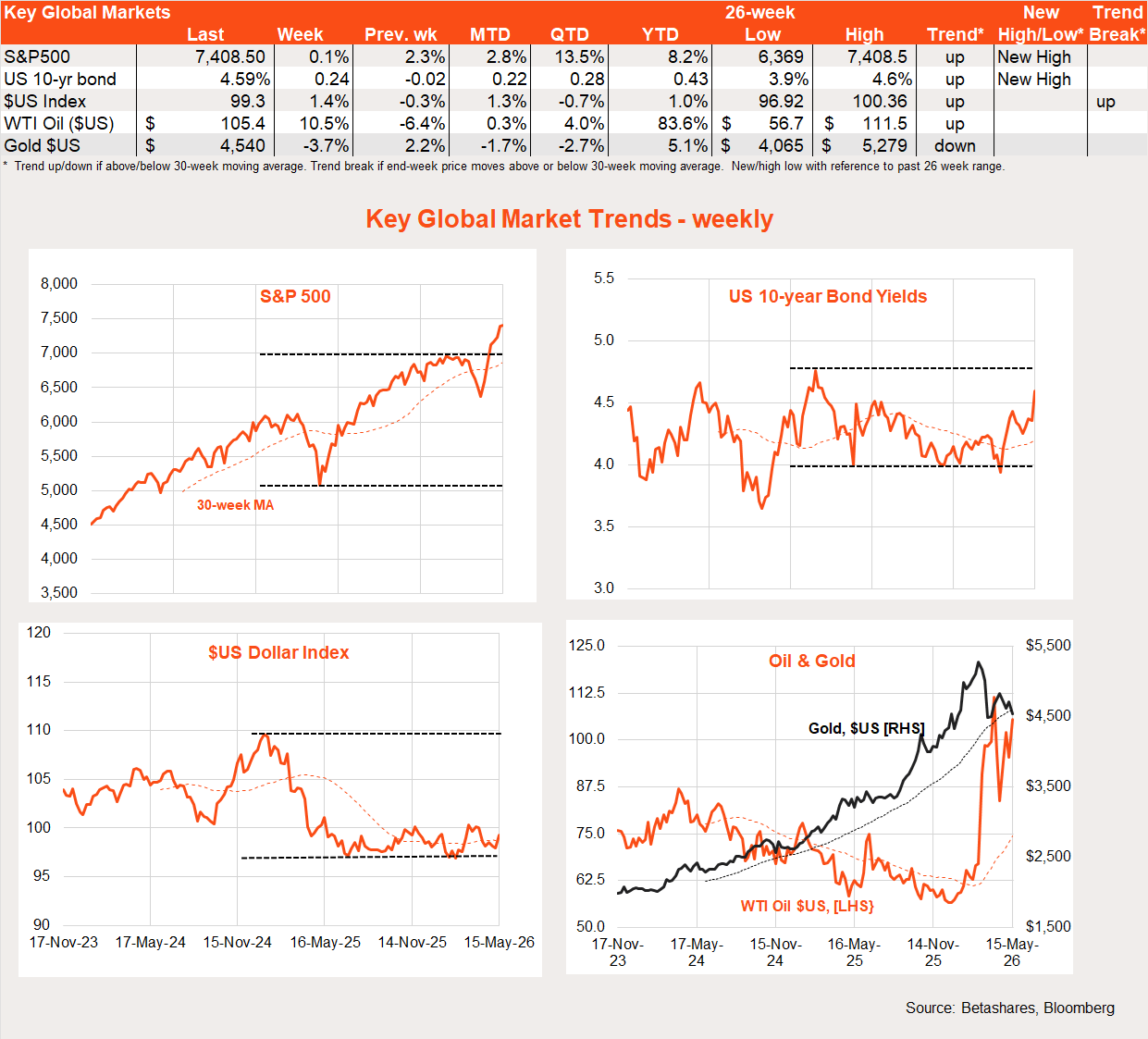

Global week in review: clinging to hope

US stocks inched ahead a little further last week – the 7th weekly gain in a row – despite a lift in bond yields and the ongoing blockage of the Strait of Hormuz.

Last week began with US President Trump rejecting Iran’s latest peace deal, meaning the Strait of Hormuz would remain closed. Yet while oil prices did rise a modest 10% last week, they remain below their initial peak when the Iran war broke out. The oil market remains strangely becalmed; with inventories being drawn down, supply shortages must surely build yet there’s a surprisingly distinct lack of panic in near-term futures prices.

The lack of panic in the oil market allowed stocks to rise further last week, focusing instead on still-solid US corporate profits and the AI boom. That said, Wall Street did take a hit on Friday, with the S&P 500 down 1.2% as US 10-year bond yield spiked 0.11% to 4.6%.

Unnerving the market a little was last week’s higher-than-expected CPI report, with core prices up 0.4% in April (market +0.3%), taking the annual rate to 2.8%. Although most of the recent lift in US inflation reflects the direct and indirect effects of higher oil prices, the market has given up on US rate cuts this year and is now flirting with the idea of rate hikes in early 2027. That saw the $US also tick up last week. It promises to be a baptism of fire for new Fed chair Kevin Warsh, who was narrowly confirmed by the Senate last week.

Trump says the “clock is ticking” for Iran to make a deal. Iran could say the same thing, as the upward pressure on oil prices and downward pressure on Trump’s polling will only intensify the longer the Strait remains closed. There appears a growing risk that the US will end the cease-fire and launch new missile attacks, but whether this changes much remains to be seen – Iran has demonstrated a remarkable ability to withstand the attacks thus far.

Of course, there was also the US-China talks last week, with not much to show for it, apart from the latter’s usual promise to buy yet more farm products.

Global week ahead: Iran and FOMC minutes

Apart from the Iran stand-off, there are little major global economic events this week. Minutes from the latest Fed meeting are released (the last with Jerome Powell as Chairperson) along with another likely weak reading on consumer sentiment.

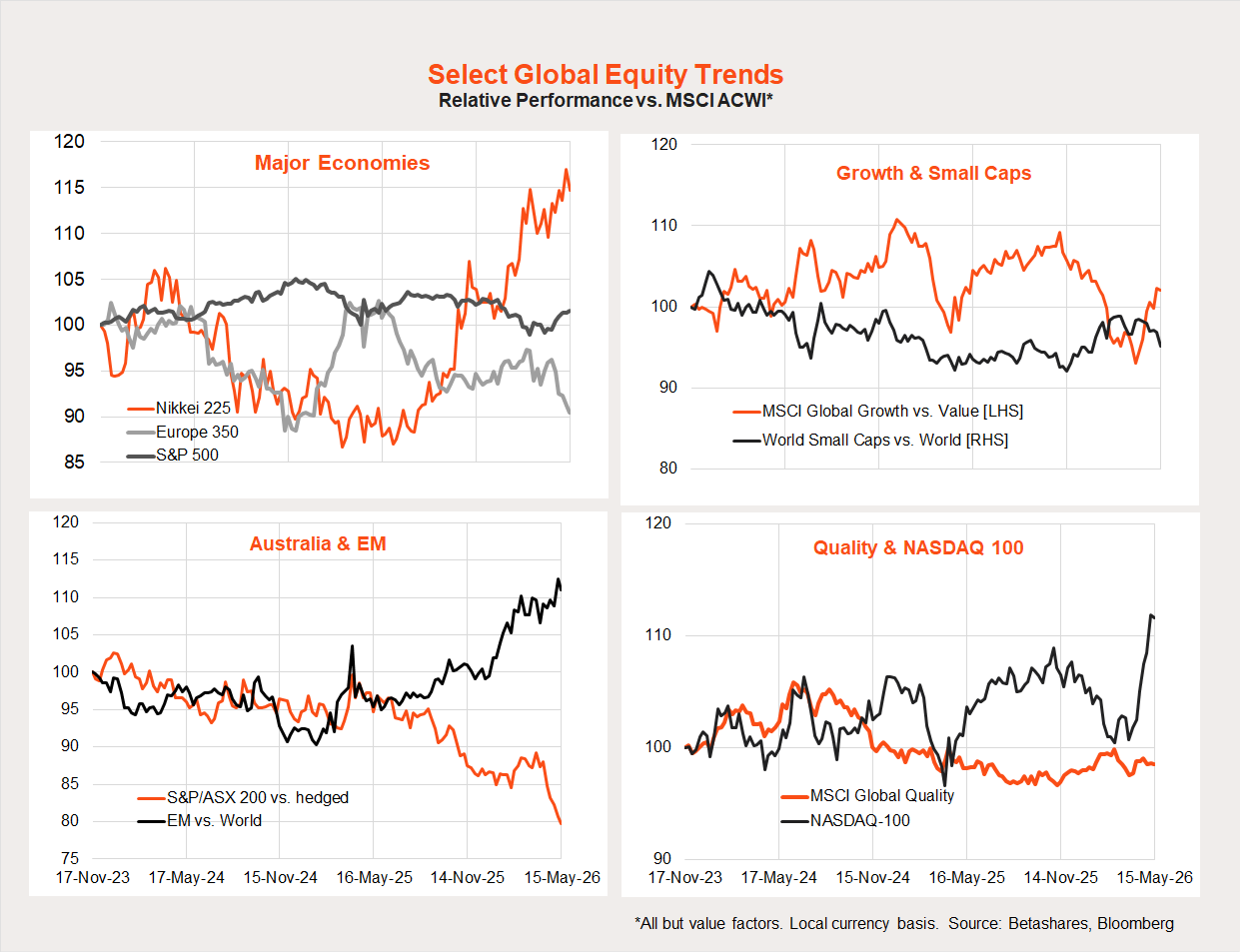

Global equity trends: US outperforms

US stocks, technology and energy tended to fare best last week. All up, the US, Japan and emerging markets continue to do best in the rebound so far, whereas Europe, Australia and small caps have not. The Nasdaq 100 has shot the lights out.

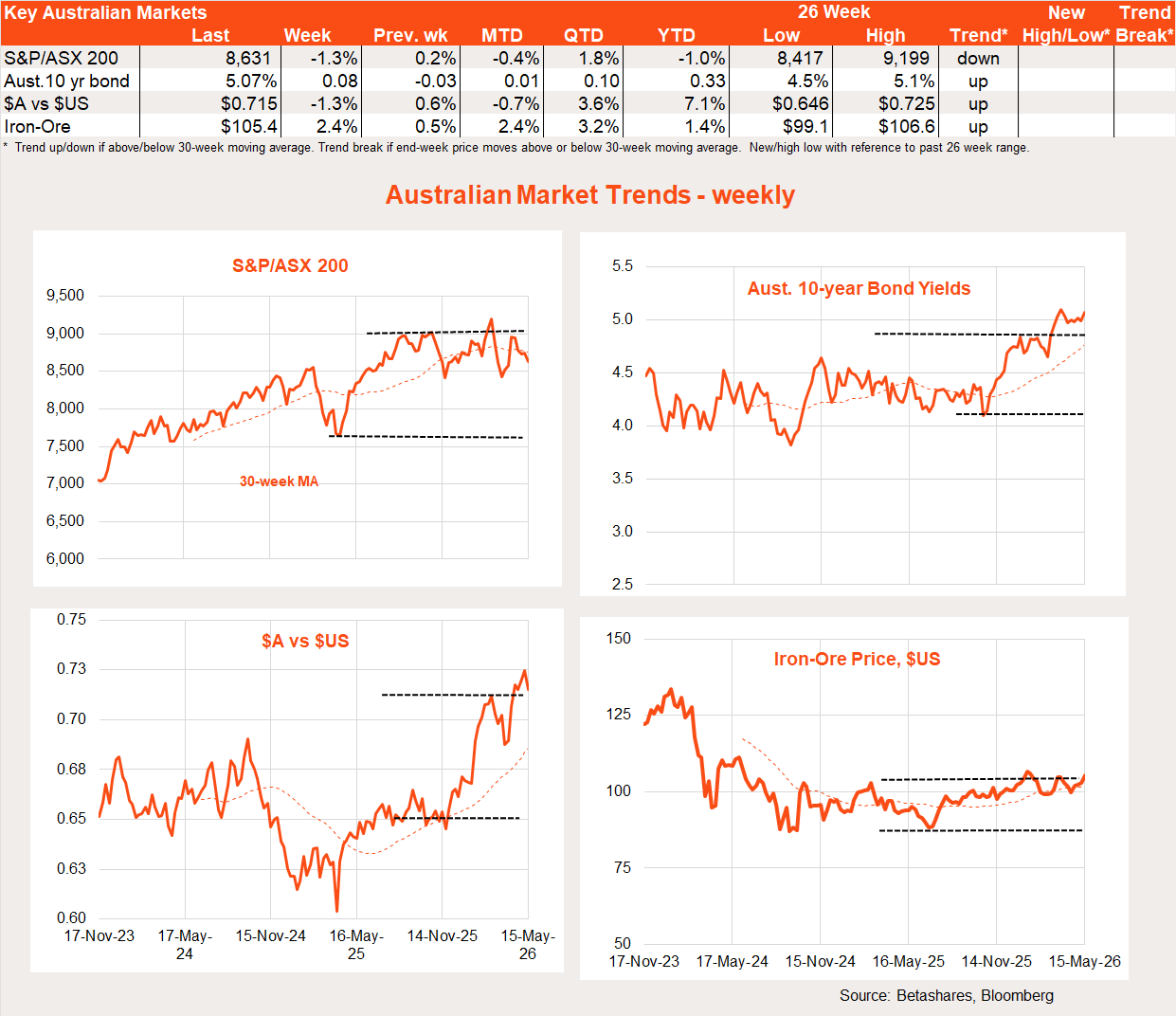

Australia review: Budget downer

Local stocks again underperformed last week, not helped by the Federal Budget confirming tax increases on capital gains and the abolition of negative gearing on newly-purchased existing residential properties.

Let’s not sugar coat this: there is very little to be optimistic about with regard to the local economy or investment markets for some time. The RBA is bearing down on the economy, keen to snuff out any signs of growth lest it keep inflation high. The RBA is targeting a return to below-trend growth and a lift in unemployment.

Then there’s the Federal Government, which has used a sledgehammer to crack the housing nut. Although the shift back to inflation indexing of capital gains on residential property was couched in terms of making it easier for first home buyers to compete with investors, questions are being asked why the change applied to all investments, including shares and small-business start-ups.

There’s no reason why different forms of investment should not be taxed differently – especially if they produce different degrees of added benefit to the economy.

As I’ve been at pains to point out, the changes imply an effective doubling in the tax on entrepreneurs when selling (and their staff with share options) from 25% to a world-record 47%. Either Treasury did not appreciate this change or did not care – I don’t know which is worse!

The Budget also increased the tax on those investing in the share market generally (even low-income earners face a minimum capital gains tax of 30%!). Indeed given the retention of dividend imputation, we’ve now got the weird outcome of dividends being more favourably taxed than capital gains. This will only encourage locally listed firms to pay out dividends rather than re-invest for growth.

As for the argument that taxes on capital and income should be treated similarly, there’s one big difference. Unlike labour income, capital is mobile and competes in a world market. A lack of mobility could also help justify a higher investment tax on local property over listed shares and start-ups.

I’ve said my piece! Further details of my Budget review are here.

Local economic data last week was also hardly inspiring. Home lending dropped 3.8% in Q1, with weakness across investors and home buyers, which is likely only the start of a longer downtrend. The NAB business survey, meanwhile, revealed a drop in conditions to below average levels and a surge in cost pressures – a stagflationary combination that pleases no-one.

The one solace was the wage price index, which rose 0.8% in Q1 and suggests there’s at least a gradual easing in wages growth underway reflecting the gradual easing in labour market tightness.

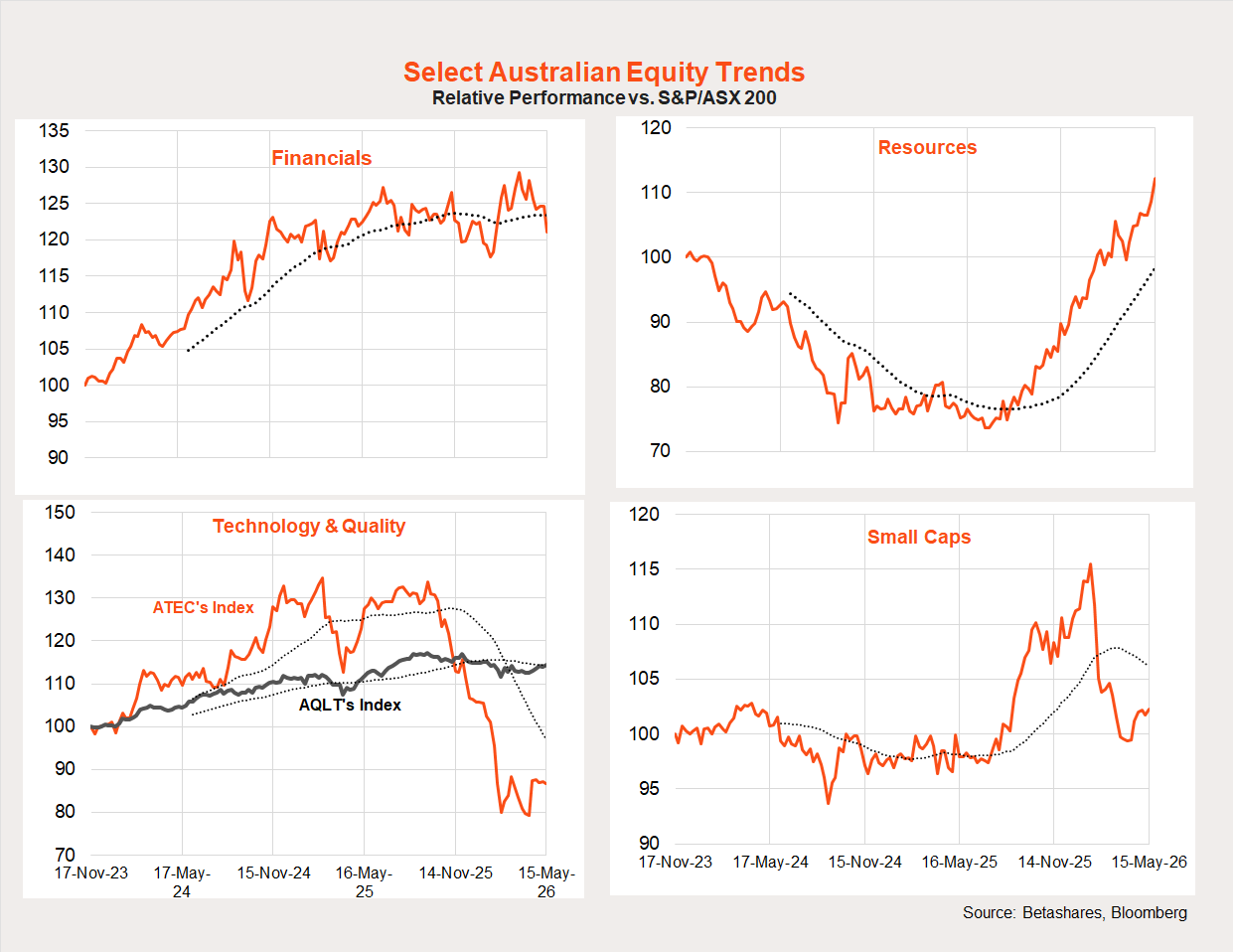

Local equity market trends: Technology/small caps bottoming out?

Energy and material stocks were the local standouts last week, with banks and health care (thanks CSL!) down.

The Iran war initially was not kind to high-beta local exposures such as technology and small caps. That said, the relative performance of both these areas has bottomed out in recent weeks, while resource company relative performance has resumed at the expense of financials. The RBA/Budget double act is likely to see stocks exposed to the local economy struggle relative to globally exposed resource stocks.

Australia week ahead: Labour market

There’s a smattering of local economic events this week, with minutes to the recent RBA meeting and consumer confidence tomorrow. Confidence is likely to sink lower given the Budget and RBA blues. I doubt we’ll learn much more from the minutes given extensive recent RBA commentary.

A mixed blessing should be Thursday’s employment report, with a reasonable 15K gain in employment expected and a steady unemployment rate of 4.3%. That would suggest the labour market continues to hold up well – which is nice, but also keeps upward pressure on interest rates.

Have a great week!