CGT changes: How to avoid the triangle of sadness

The 2026 Budget proposal to replace the 50% CGT discount with cost-base indexation reintroduces an old structural problem: capital gains and capital losses are calculated on different cost bases. For investors holding a portfolio of direct shares, that asymmetry can result in tax being paid on a real economic gain that simply isn’t there. Pooled investment vehicles, including ETFs, could potentially mitigate the problem.

The Government’s framing is that investors will only be taxed on their real capital gain. In a static, single-asset world that framing holds. But in the real world many Australians hold more than one stock or single investment, and the way indexation works in practise has a quieter consequence that the headline numbers don’t capture: gains and losses are no longer measured against the same yardstick.

“Under the proposed reversion to pre-1999 indexation, a capital gain is calculated by reference to the indexed cost base. A capital loss is calculated by reference to the original (nominal) cost base. The two never meet in the middle.”

The current rules: a level playing field

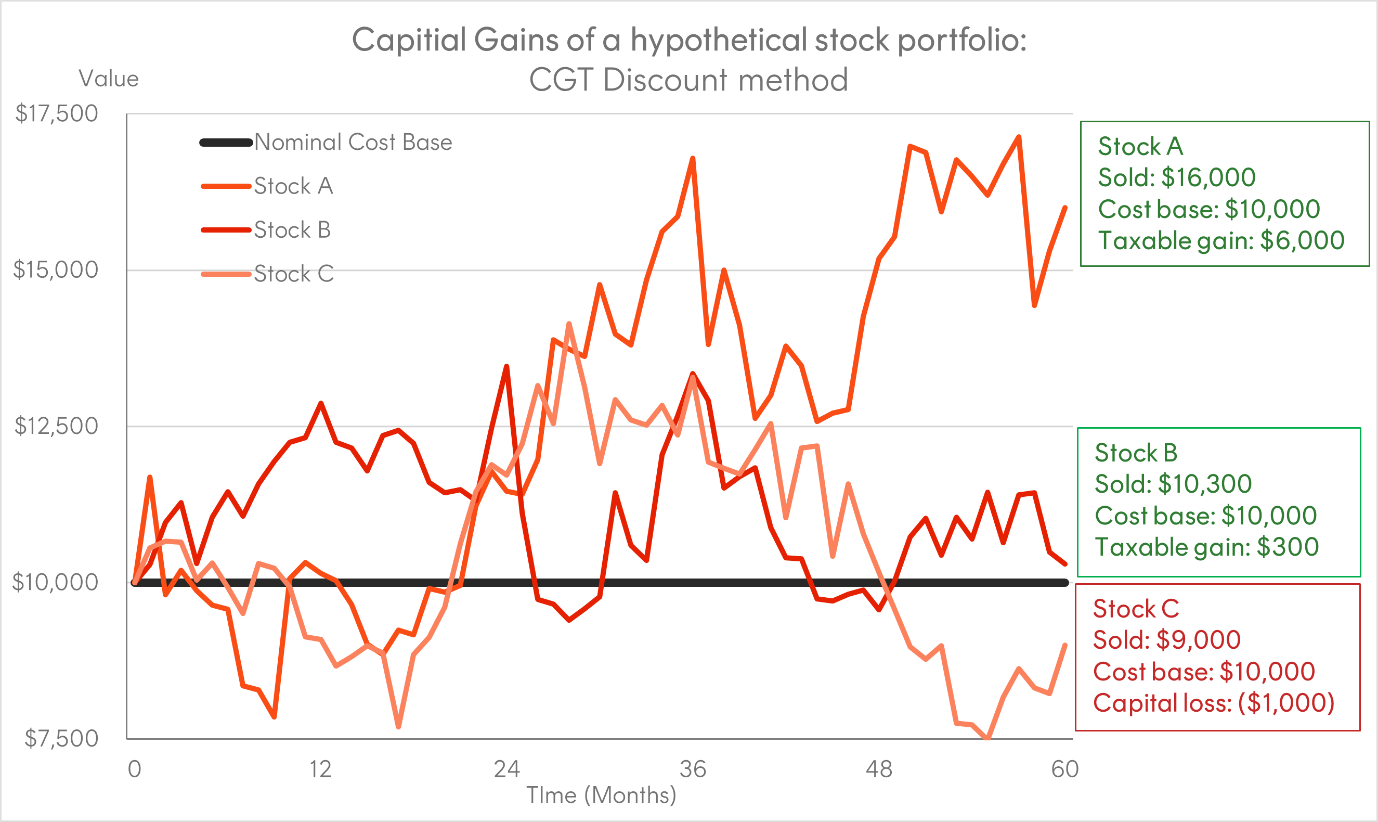

Under the existing 50% discount regime, every share in a portfolio is measured against the same mark – its original cost base1. The economic gain at the portfolio level and the taxable gain at the portfolio level are identical.

To demonstrate this, take the following hypothetical 3 stock portfolio example, where Stock A and B are sold for a profit and Stock C are sold for a loss.

Hypothetical example only. Assumes purchase price of each stock holding is $10,000, all held on capital account for 5 years and sold at the figures shown. Calculations illustrate the effect of the existing 50% CGT discount available to Australian resident individuals. Actual tax outcomes will vary depending on individual circumstances. This is not financial, tax or legal advice.

The calculation of both capital gains and losses are from a common starting point, in this case $10,000. In other words where a capital loss exists it can be used in full to offset the tax that might otherwise be payable on all or part of a capital gain. As a result, the net taxable capital gain ($6,000 + $300 – $1,000) matches the net economic gain at a portfolio level, being $5,300. Then, under the discount method CGT is applied on half of that amount ($2,650) to provide an offset for inflation.

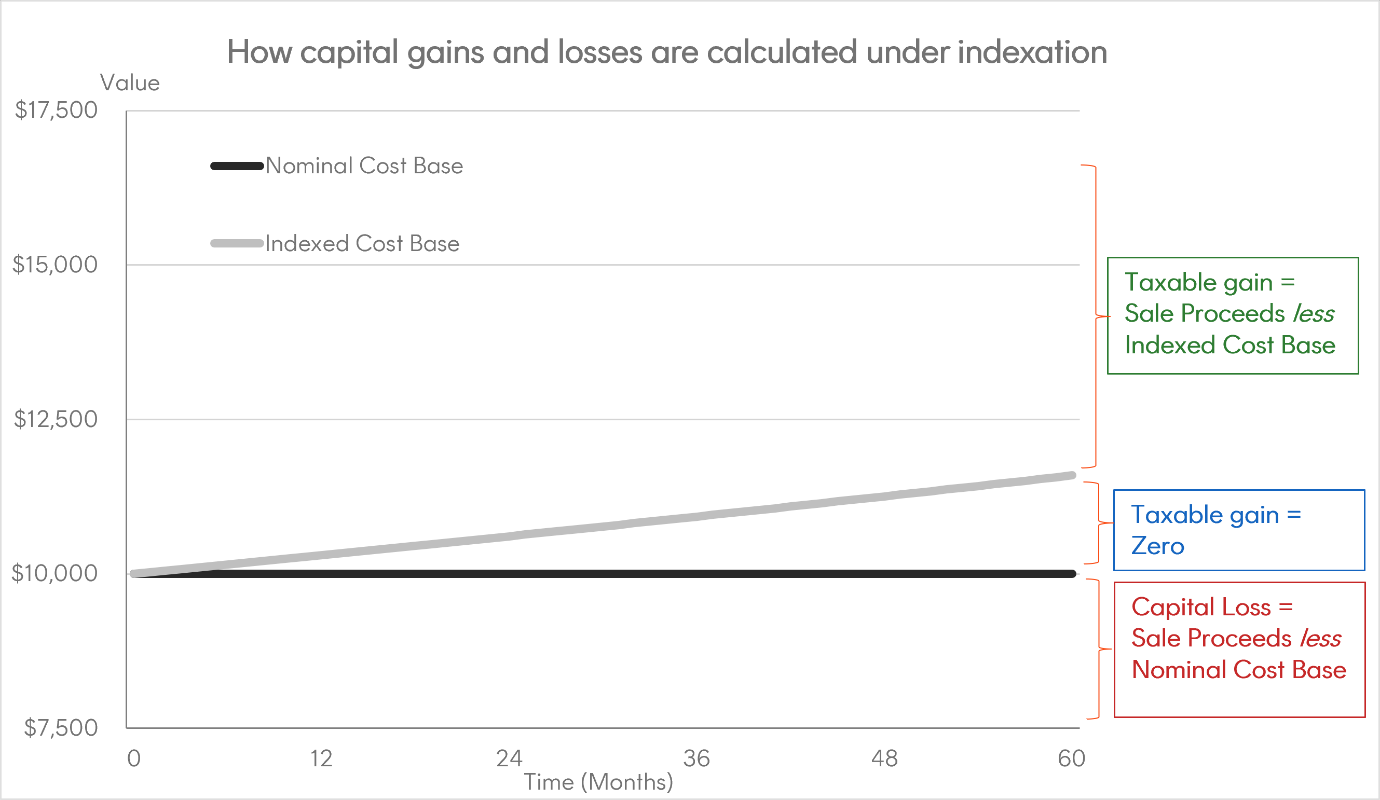

Proposed reversion to CGT indexation: the triangle of sadness

Under the pre-1999 CGT indexation regime, the cost base of each asset is uplifted in line with CPI over the holding period. However the calculation of a capital gain or loss is different depending the value of each individual asset at disposal. If an individual asset or share is sold for:

– Greater than its indexed cost base: a taxable capital gain is recognised, calculated as sale proceeds less the indexed cost base

– Between the original and indexed cost bases: there is no recognised taxable capital gain or loss

– Less than the original cost base: a capital loss is recognised, calculated as sale proceeds less the original cost base. Indexation does not apply to losses.

Hypothetical example only, assumes cumulative indexation factor of 1.15 over five years. Indexation shown as a linear increase for simplicity. Actual tax outcomes will vary depending on individual circumstances. This is not financial, tax or legal advice.

The middle zone in the chart above is the problem – the triangle of sadness, if you will. It is the gap between the two cost bases, and it widens every year the asset is held. Real economic losses that fall inside the gap are invisible to the tax system, so they cannot be used to offset real economic gains elsewhere in the portfolio.

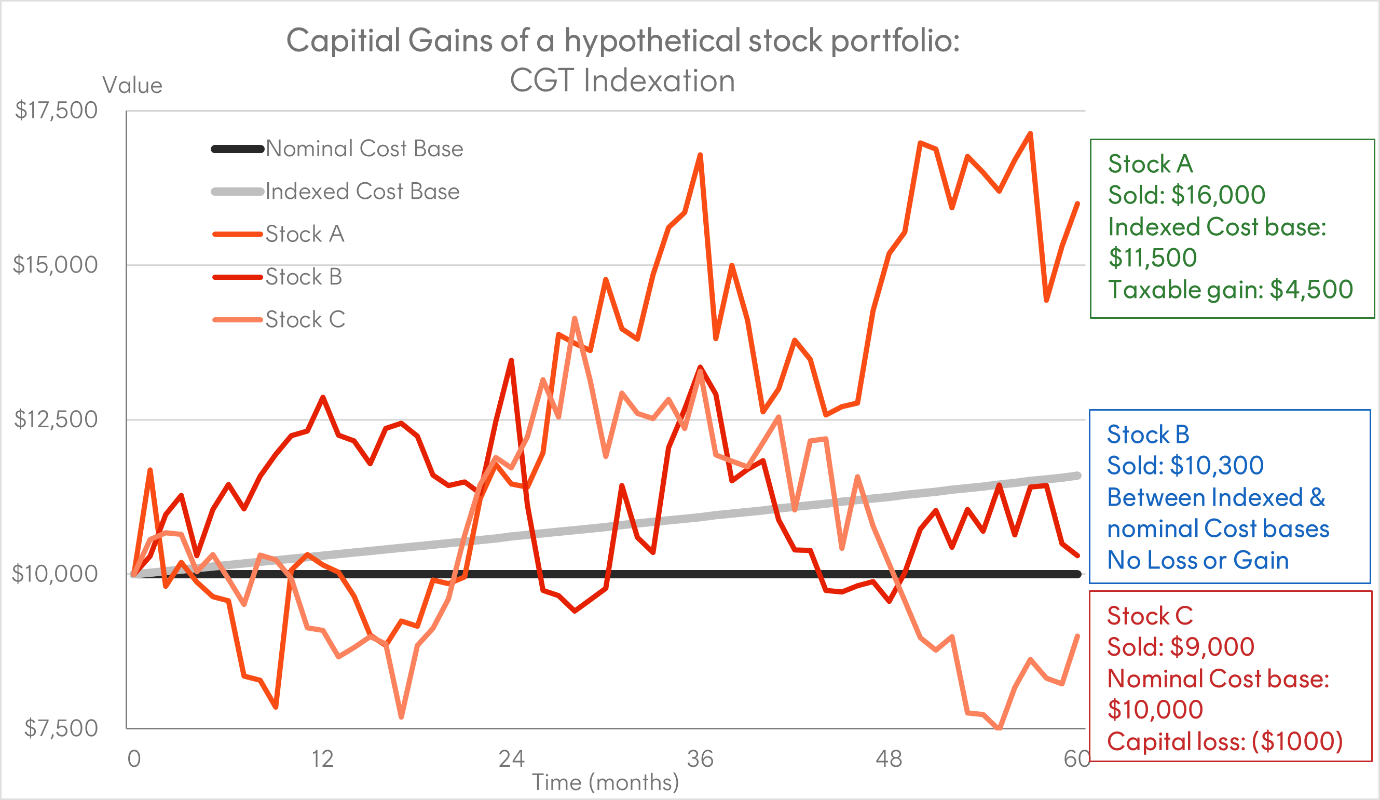

Applying the proposed rules to the three-stock portfolio

Below we show the outcomes under CGT indexation for that same three stock portfolio, assuming that the cumulative inflation of 15%. On the surface, the proposed regime produces a lower taxable gain for the stocks A and B that are sold for more than their purchases prices. That is the headline the Government wants you to see. But strip out the 50% discount that the current regime then applies to look at the real return outcomes on a portfolio level, and the comparison changes.

Under pre-1999 CGT indexation a “real” loss (a loss after adjusting for inflation) is not recognised and therefore cannot be used to offset the tax that might otherwise be payable on capital gains. In our example, the worse-than-inflation returns of the Stock B and Stock C do little to shield the tax payable on Stock A. From a tax perspective the capital losses on Stock A and B are either eliminated entirely or materially diminished by measuring them against the lower notional, not the higher indexed, cost base.

Hypothetical example, assuming a reversion to pre-1999 CGT indexation treatment, purchase price of each stock holding is $10,000 and all are held on capital account for 5 years with a cumulative indexation factor of 1.15, before being sold for the figures shown. Actual tax outcomes will vary depending on individual circumstances. This is not financial, tax or legal advice.

As result the taxable net capital gain for the portfolio is $3,500. Yet the investor’s real gain at a portfolio level is only $800, after accounting for cumulative inflation of 15% over 5 years on the $30,000 initial investment. Assuming the investor’s marginal tax rate is 47%, they would pay approximately twice as much in tax as the real gain, leaving them significantly behind after inflation.

See how your investments will be impacted with our CGT Calculator.

Why a pooled vehicle structurally avoids the problem

Now consider the same three stocks held inside a single pooled investment vehicle, whether a managed fund, an ETF or a listed investment trust. The investor’s cost base is the unit price they paid, not the prices of the underlying stocks. The fund itself is the CGT asset.

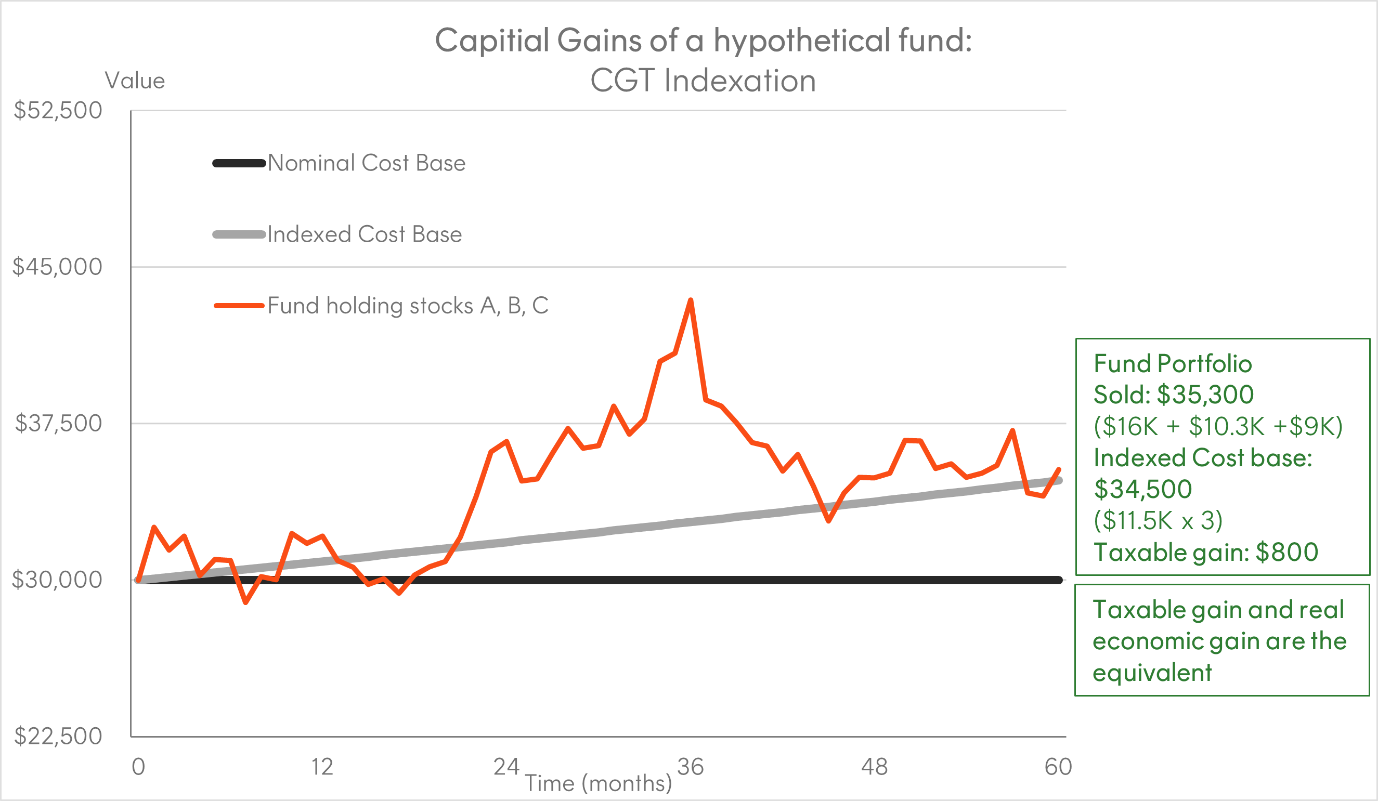

Hypothetical example only, assuming a reversion to pre-1999 CGT indexation treatment, purchase price for the fund is $30,000, which is held on capital account for 5 years with a cumulative indexation factor of 1.15, before being sold for the figure shown. Actual tax outcomes will vary depending on individual circumstances. This is not financial, tax or legal advice.

In our example, the investor buys units at a cost base of $30,000 (the sum of the three $10,000 stock holdings) and redeems at $35,300 (the sum of final portfolio value). The fund’s cost base of $30,00 is indexed up to $34,500. The taxable gain is $800, matching the portfolio level real economic gain. The investor is not penalised with a higher tax bill as a result of some of the stocks within the portfolio underperforming inflation.

One important caveat is that this example assumes the fund or ETF simply buys and holds those three stocks – there is no turnover within the fund over the 5-year period.

Why this gets worse over time for investors holding direct shares

The gap between the indexed and nominal cost bases is small in year one. By year five it is 15 percentage points wide in the scenario above. By year ten it could be 25 to 30 percentage points wide. Long-term investors who hold diversified direct share portfolios, sit fully exposed to this widening asymmetry. Holding through a market drawdown is rewarded by the current rules and are likely to be quietly penalised by the proposed ones.

The AFR has reported analysis suggesting that people with a diversified portfolio of individual shares directly could face tax rates up to 50% more tax than Treasury’s own estimates imply. The asymmetric loss treatment described here is a meaningful part of that gap.

Why ETFs may be a better solution in a world of CGT indexation

There was one important caveat within the arguments above for a pooled vehicle, such as an ETF or unlisted managed fund. The comparison above assume that the ETF or fund had no turnover during the 5-year hold period.

Turnover within the portfolio held by a fund leads to capital gains being distributed to the investors in that fund, and at the margin this tax drag that detracts from after-tax performance. However index tracking ETFs are generally more efficient at reducing ongoing CGT than unlisted funds, as discussed here.

As we have said before, the proposed CGT changes are not a reason in themselves to change your asset allocation. But structure matters more than ever. The new rules strengthen the case for holding growth assets in tax-efficient structures. Superannuation, investment bonds and ETFs held outside super are materially more efficient than alternatives such as direct stock investing or unlisted funds.

Betashares is not a tax adviser. This information should not be construed or relied on as tax advice and investors should obtain professional, independent tax advice before making an investment decision. Hypothetical examples are for illustrative purposes only. Assumptions used may not reflect actual market conditions or individual circumstances. This information does not constitute financial, tax or legal advice. Past performance is not indicative of future performance.

The Australian Government has announced proposed changes to the operation of the capital gains tax (CGT) regime. These proposals are not yet enacted and may change. If implemented, they may affect the taxation outcomes for investors, including in respect of capital gains arising on the disposal of assets and any capital gains attributed to investors by the Fund. The proposed changes may alter the current treatment of capital gains (for example, by modifying the CGT discount or introducing alternative methods for calculating capital gains).

The potential impact of these proposals will depend on the final form of the law and the circumstances of each investor. Investors should obtain professional independent tax advice in relation to these proposals and their potential application.

The information contained in this article is general information only and does not take into account any person’s financial objectives, situation or needs. Investors should consider the appropriateness of the information taking into account such factors and seek financial advice. This article is provided for information purposes only and is not a recommendation to make any investment or adopt any investment strategy.

Future results are impossible to predict. Actual events or results may differ materially, positively or negatively, from those reflected or contemplated in any opinions, projections, assumptions or other forward-looking statements. Opinions and other forward-looking statements are subject to change without notice. To the extent permitted by law Betashares accepts no liability for any errors or omissions or loss from reliance on the information herein.

1. Subject to AMIT related adjustments and adjustments for incidental costs (e.g. brokerage).