David Bassanese

6 minutes reading time

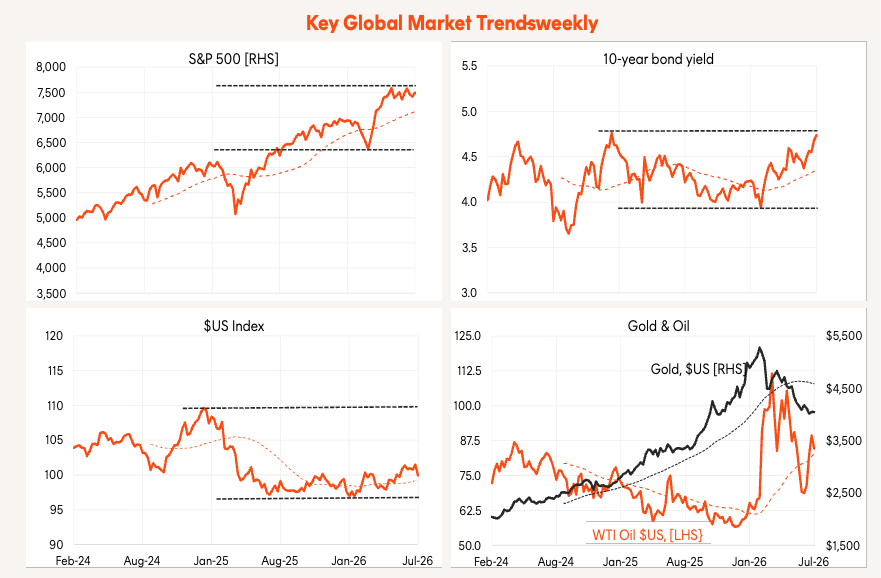

Global week in review: Peace hopes and earnings

US equities rebounded last week amid tentative hopes of a renewed US-Iran ceasefire and solid US corporate earnings. Bond yields continued to edge higher, though not enough to yet weigh heavily on equities.

Source: Betashares, Bloomberg.

It was a mixed week on the Iran front. Early hopes of a sustained ceasefire gave way to renewed conflict, before fresh hopes for peace talks emerged over the weekend. President Trump again stepped back from threats of more intense bombing, apparently after urging from several Middle East countries, including Iran.

Iran appears unfazed by the threat of heavier bombing and remains capable of retaliating against US bases and other Middle East targets. As such, US hopes for a face-saving deal appear to be fading. But Trump’s demands that any deal include reopening the Strait of Hormuz and containing Iran’s nuclear threat at least still leaves enough wiggle room in any deal for him to claim victory. With global oil inventories still falling, a deal remains important to limit the risk of higher oil prices. For now, lingering peace hopes are helping contain oil prices – ironically reducing pressure on Trump to strike a deal.

The Q2 US earnings season is off to a strong start, with Microsoft’s earnings beat helping revive confidence in the AI trade. Microsoft reported stronger-than-expected Azure revenue growth and greater take-up of its Copilot AI services.

That said, cloud revenue growth is not all AI-related; it also reflects the long-running shift by corporates from on-premise systems to the cloud. Microsoft’s earnings beat also partly reflected an upgraded valuation of its equity investment in Anthropic. The key question remains whether heavy AI investment will ultimately generate enough revenue from governments, corporates and consumers, especially as parts of the AI ecosystem become more competitive and commoditised.

Even so, according to FactSet 86% of the 60% of S&P 500 companies that have reported Q2 results so far have beaten earnings estimates – well above the 10-year average of 76%. Good earnings are helping equities grind higher, even with the Iran war and AI concerns.

The US Federal Reserve also reassured markets by leaving rates on hold, despite a 40% market-implied chance of a hike. Still, three of the 11 voting members favoured raising rates, and Fed Chair Warsh maintained his tough inflation rhetoric.

Markets now price a 74% chance of a September rate hike, expecting Warsh’s rhetoric to soon translate into action. June inflation data at least helped: both the core personal consumption deflator released last week and the core CPI released a few weeks ago surprised on the downside.

Global week ahead: US payrolls

The US labour market will be in focus this week, with job openings data on Wednesday and payrolls on Friday. After signs of softening in late 2025, conditions have rebounded reassuringly so far this year.

The market expects an 88k employment gain in June, enough to keep unemployment steady at 4.2%. If the labour market remains healthy, investors are likely to keep worrying about further US rate rises until inflation eases more convincingly.

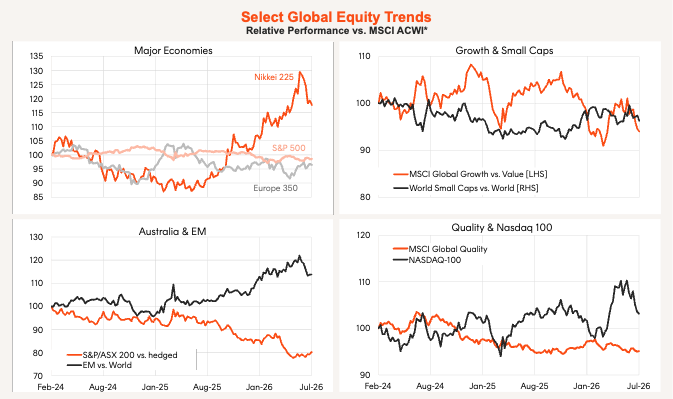

Global equity trends: Technology unwind

The main global trend remains the unwinding of technology’s earlier outperformance as AI concerns fluctuate. Japan, emerging markets, growth stocks and the Nasdaq 100 have underperformed in recent weeks, while Europe has strengthened and Australia’s long underperformance has at least stabilised.

Note the US market has held up reasonably well, with investors merely rotating from technology into non-technology sectors. Among global sectors, energy and financials have led over the past month.

*All but value factors. Local currency basis. Source: Betashares, Bloomberg.

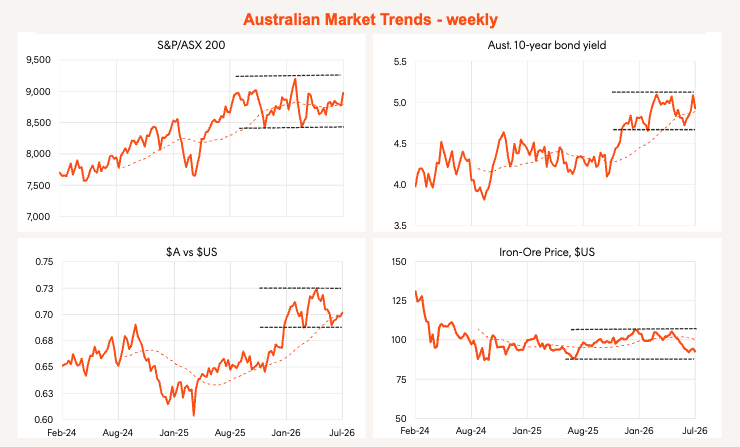

Australia week in review: Better-than-feared CPI

Local stocks bounced last week, helped by firmer global markets and a softer-than-expected Q2 inflation report.

Source: Betashares, Bloomberg.

Most critical last week, the trimmed mean inflation measure rose 0.8% over the quarter – still firm, but below the RBA’s May forecast of 1.0% and the market’s 0.9% expectation. My fear of a 1.0% gain was also unrealised, despite the expected strength in housing and market services inflation.

Overall, the result likely rules out an RBA rate rise at next month’s meeting. I am also reverting to my earlier call that the RBA will remain sidelined this year, with the next move a cut in H2’27. Weakening growth and house prices should help inflation ease gradually in coming quarters.

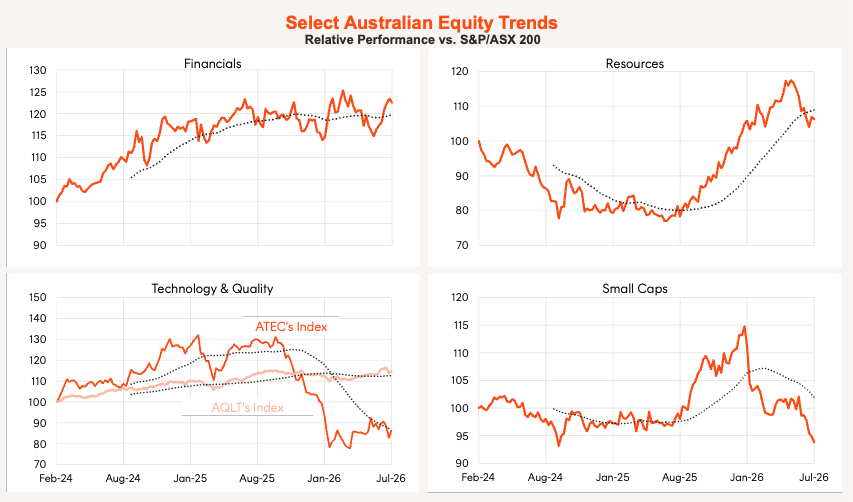

Local equity market trends: Technology stabilising

High-beta exposures led last week, with consumer discretionary and technology returning 4.2% and 8.5% respectively. Health care also performed well, up 5.7%, while small caps continued to lag.

Among major sectors, financials’ relative performance remains choppy and broadly sideways, while resources’ underperformance has bottomed in recent weeks. The beaten-up technology sector also appears to be stabilising, with a tentative recovery underway.

Source: Betashares, Bloomberg.

Australia week ahead: Consumer spending

There is little local data this week apart from June consumer spending via the still relatively new household spending indicator, which is likely to show spending remains subdued.

The August earnings season also begins this week. As with the economy, results are likely to be subdued, with businesses reporting weak local demand and cost pressures.

We learnt today that house prices also continue to ease, with national prices down 0.7% in July and 2.0% from their earlier peak. Sydney and Melbourne prices are around 5.5% below peak.

Overall, it remains hard to be optimistic about the local economy or equity market. One relative support is Australia’s underweight exposure to technology, which remains under pressure globally amid AI boom concerns.

Have a great week!