Tom Wickenden

6 minutes reading time

- Australian shares

With just a 4% weight in the S&P/ASX 300 Index[i] (ASX 300), Australia’s technology companies punch above their weight in terms of investor interest.

A small but dynamic part of Australia’s equity market, technology companies have delivered periods of significant outperformance against the broader Australian market and global technology peers, alongside sharp drawdowns.

Despite the current drawdown – and what some have dubbed a global ‘SaaSpocalypse’ in software – Australian investors are continuing to allocate to the sector. The ATEC S&P/ASX Australian Technology ETF has attracted $193.7 million in net inflows so far this year to 15 April 2026, already exceeding the $156.5 million gathered in 2025.

These flows suggest that, rather than stepping away during volatility, many investors continue to view Australian technology as a long-term structural growth opportunity.

Australian technology, no stranger to selloffs

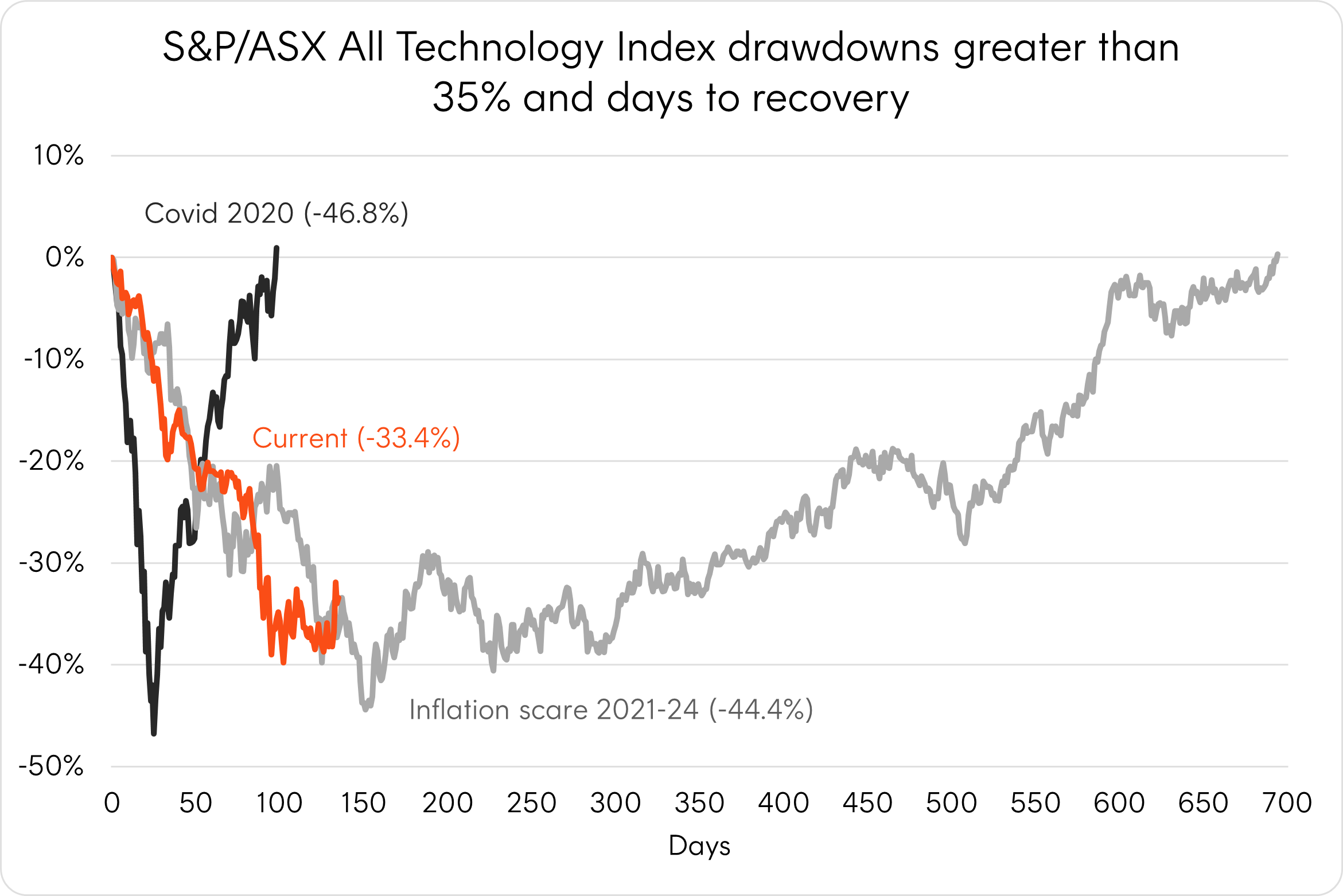

While a drawdown of 35% might seem like a dramatic statistic for more ‘traditional’ sectors, it is not necessarily an anomaly for Australian technology. For example, over the period from March 2014 to March 2026, the sector has experienced six drawdowns of 20% or more, with three drawdowns greater than 35% since 2020.

Despite these historical pullbacks, and the Index has tended to rebound strongly as can be seen in the chart below (remembering of course that past performance isn’t indicative of future performance).

The recent rebound in April underscores how quickly sentiment can shift. Since the end of March, the sector has rallied approximately 14%[ii], and while it remains in drawdown, the pace of the rebound highlights the speed at which Australian technology can reprice.

Source: Bloomberg. Since index inception 21 March 2014. Covid drawdown: 18 February 2020 to 2 July 2020. Growth scare drawdown: 19 November 2021 to 17 July 2024. Current drawdown: 6 October 2025 to 10 April 2026 (not yet recovered). You cannot invest directly in an index. Past performance is not an indicator of future performance.

Being a high beta sector (meaning share prices tend to move more than the overall market, up or down), Australian technology has historically experienced larger drawdowns than the broader market during growth scares, such as the March 2020 selloff due to the Coronavirus outbreak.

Additionally, attracting high valuations due to typically strong earnings growth expectations and future upside potential, the Australian technology sector is also sensitive to interest rate expectations.

There is, however, a factor unique to the current selloff. AI’s threat to software has made the Australian technology sector particularly vulnerable and seen its performance decouple from other regions, like the US’s Nasdaq 100.

Unpacking Australia’s technology sector

Examining the Australian technology sector’s composition helps to explain the current selloff.

79% of the Index’s holdings are software companies, with just 17% classified as hardware. Of the software companies, 69% operate business to business (B2B) models[iv].

Compare this to the Nasdaq 100, with only 37% of current holdings classified as software companies and 42% hardware. The Nasdaq also has an almost even split of B2B versus business to consumer (B2C) models[v].

|

S&P/ASX All Tech |

Nasdaq 100 |

|

|

Sub-Type |

||

|

Software |

79% |

37% |

|

Hardware |

17% |

42% |

|

Other |

3% |

21% |

|

Customer Type |

||

|

B2B (software) |

69% |

45% |

|

B2B (all holdings) |

76% |

56% |

|

B2C (all holdings) |

24% |

44% |

Source: Betashares, Bloomberg. As at 13 March 2026. Sub-Type and Customer Type as identified by Betashares by index weight.

Current concerns around AI disruption are being directed at B2B software companies as investors face uncertainty around their future profitability. The rapid advancement of AI capabilities is seen as a core threat to existing software moats that could be breached by cheaply created and implemented alternatives.

Additionally, B2B software companies relying on seat-count subscription models face the threat of job cuts reducing licence volumes across core business functions like finance (Xero Limited (ASX: XRO)) and HR/recruitment (SEEK Limited (ASX: SEK)). Hardware companies, as the picks and shovels of AI infrastructure, have largely been spared this pressure.

The result is a sector composition that has made Australian technology particularly vulnerable to the current sell-off.

Australian technology, stronger together

The honest caveat is that current investor uncertainty is not misplaced. Disruption risk is a permanent feature of technology investing. But disruption also presents opportunity, for incumbents to integrate and adapt and new entrants to grow. In a sector as dynamic and small as Australian technology, this points to the benefits of an indexed ETF approach.

Rather than concentrating risk in individual names, index ETFs can provide exposure to a broad basket of companies across a sector. As leading companies or new disruptors grow, their weight within an index increases naturally and investors gain greater exposure to emerging winners over time while reducing exposure to those that do not adapt.

Long-term investors seeking diversified exposure to Australian technology may wish to consider the ATEC S&P/ASX Australian Technology ETF Betashares S&P/ASX Australian Technology ETF (ASX: ATEC), which aims to track the S&P/ASX All Technology Index (before fees and expenses).

There are risks associated with an investment in ATEC, including market risk, technology sector risk and concentration risk. Investment value can go up and down. An investment in the Fund should only be considered as a part of a broader portfolio, taking into account your particular circumstances, including your tolerance for risk.

Any Betashares Fund that seeks to track the performance of a particular financial index is not sponsored, endorsed, issued, sold or promoted by the index provider. No index provider makes any representations in relation to the Betashares Funds or bears any liability in relation to the Betashares Funds.

No assurance is given that any of the companies in ATEC’s portfolio will remain in the portfolio or will be profitable investments.

[i] Source: Bloomberg. As at 16 March 2026. Weight of S&P/ASX All Technology Index constituents in the S&P/ASX 300.[ii] Source: Bloomberg. 31 March to 17 April 2026. Sector represented by Betashares S&P/ASX Australia Technology ETF (ASX: ATEC). Past performance is not an indicator of future performance.[iii] Source: Bloomberg, Betashares. Analysis of relationship between Australian 10-year government bond yields and S&P/ASX All Technology Index performance during historical episodes. Past performance is not an indicator of future performance.[iv] Source: Betashares, Bloomberg. As at 13 March 2026. Sub-Type and Customer Type as identified by Betashares by index weight.[v] Source: Betashares, Bloomberg. As at 13 March 2026. Sub-Type and Customer Type as identified by Betashares by index weight.

1 comment on this

[email protected]