Key points

SpaceX’s share market debut on 12 June 2026 was monumental in many ways.

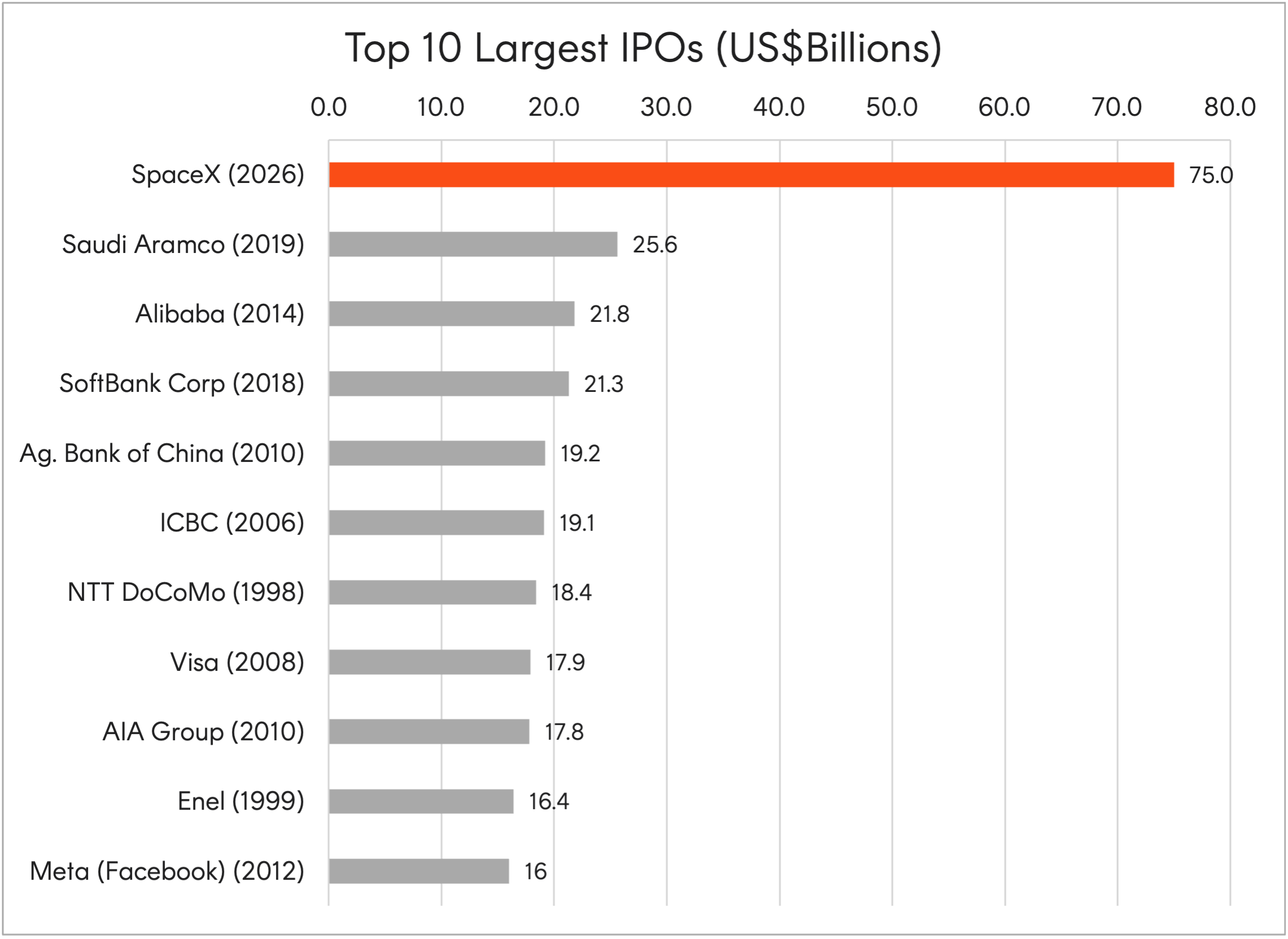

Listing on the Nasdaq under the ticker SPCX, the rocket, satellite and AI business raised US$75 billion at a valuation of approximately US$1.8 trillion. This would make it the world’s largest IPO in stock market history.

Source: Visual Capitalist

Shares closed their first day of trading at US$160.95, up 19% from the initial IPO price, taking the company’s market capitalisation to US$2.1 trillion, which rivals the size of some of America’s largest US technology companies including Amazon and Microsoft.

The listing marks a landmark moment for the space economy with the sheer size of the IPO alone highlighting the commercial opportunities available for investors seeking new revenue streams from untapped markets such as orbital data centres.

The trillion-dollar question, however, remains whether Musk can make SpaceX just as successful as he did for Tesla when the latter IPO’d on June 29, 2010. To that end, while a true leader in the space race, it’s worth noting that there are other companies operating across the industry detailed below.

Mobile coverage: AST SpaceMobile (ASTS)

For example, while Starlink generates more than 60% of SpaceX’s total revenues, its service offering differs from other satellite connectivity providers.

Starlink requires a dedicated terminal, but a company like AST SpaceMobile (ASTS) operates a ‘direct to mobile’ service which bypasses the need for a dish terminal. ASTS works closely with major telco providers to distribute their offerings to end customers.

In October 2025, ASTS signed a definitive commercial agreement with Verizon to provide direct-to-mobile service starting in the second half of 2026, following Verizon’s US$100 million strategic investment the prior year1. The deal was announced after successful demonstrations, including voice and video calls between standard phones via satellite.

AST SpaceMobile has also secured agreements with AT&T and Vodafone and plans to deploy 45–60 next-generation satellites in LEO (Low Earth Orbit) by the end of this year2. Although currently unprofitable, AST is expected to become profitable next year as subscriber revenue and commercial services ramp up.

Space Data as a Service: Planet Labs

Beyond the infrastructure layer, space data as a service is becoming increasingly viable as sectors like defence and agriculture seek on-demand, scalable data sets to inform critical decision-making.

Planet Labs (PL) is a key leader in this sector, operating the largest commercial earth observation constellation in history with over 200 satellites imaging the Earth’s entire landmass every 24 hours. PL overlays AI to generate valuable insights from this image data that are sold as a subscription, generating over 90% of revenue on a recurring basis. Its client mix spans agriculture, forestry, defence, insurance, and financial services.

In its most recent fiscal year, Planet Labs posted revenue of approximately US$308 million and achieved full-year adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortisation) profitability for the first time, with a backlog reaching US$900 million3. Defence and intelligence have been the key growth drivers, including a €240 million multi-year German government contract4.

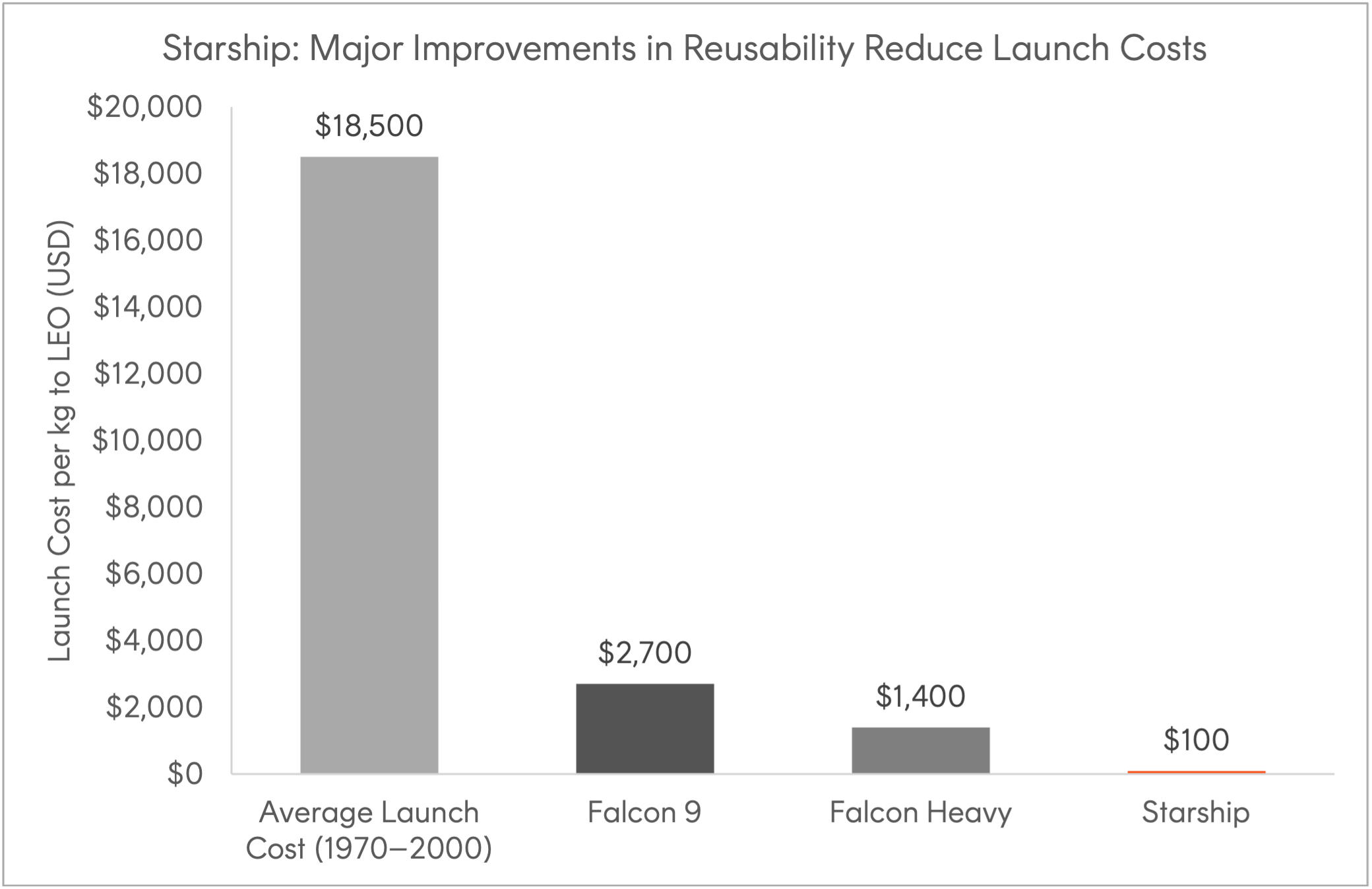

The enabler: falling launch costs

None of the above would be commercially viable without the dramatic decline in the cost of reaching orbit – a key metric underpinning the entire industry’s expansion.

Traditional launch vehicles have cost upwards of US$18,000 per kilogram to LEO. SpaceX’s Falcon 9, through reusable first-stage boosters, brought this to US$2,000–4,000 while next-generation vehicles like SpaceX’s Starship could push costs as low as US$100–200 per kilogram.

Source: SpaceX Roadshow Presentation.

This dynamic is self-reinforcing: lower launch costs enable larger constellations, which create more data and connectivity capacity, which attracts more commercial customers, and therefore funds further launches.

With launch capacity still a key bottleneck, vertical integration is becoming more common. Traditional launch providers like Rocket Lab and Firefly Aerospace are now building their own satellites as well.

An ASX first of its kind

The RCKT Space Industry ETF was the first of its kind in Australia, aiming to provide targeted exposure to leading companies in the global space economy.

The fund seeks to track the Solactive Space Industry Index which includes up to 30 pure-play space companies weighted by their float-adjusted market capitalisation (the proportion of a company’s shares available for public trading), with a single-stock weight cap of 10%.

Where the Index contains companies with a total market capitalisation above US$250 billion, the largest such company may carry a maximum weight of 25%. That said, the weight of such company may exceed this maximum cap between rebalance dates due to rising market movements as we’ve seen recently with Space Exploration Technologies.

The company, trading under the ticker SPCX on the Nasdaq exchange, entered RCKT on Wednesday 17 June 2026 and holds a weight of approximately 30% at time of writing.

SPCX was included into RCKT’s portfolio in accordance to the index’s fast-entry of eligible major IPOs shortly after listing (generally two trading days).

Other top holdings beyond SPCX include names discussed throughout this article such as AST SpaceMobile and Planet Labs, but also other companies like Viasat, EchoStar (which holds a minor stake in SpaceX) and Rocket Lab.

Investors can now participate in the exciting space theme through RCKT Space Industry ETF given its stake in SpaceX but also other companies across the space industry, in just one single trade on the ASX.