Build strong financial foundations today for a child's tomorrow.

Kids Accounts Invest in their future

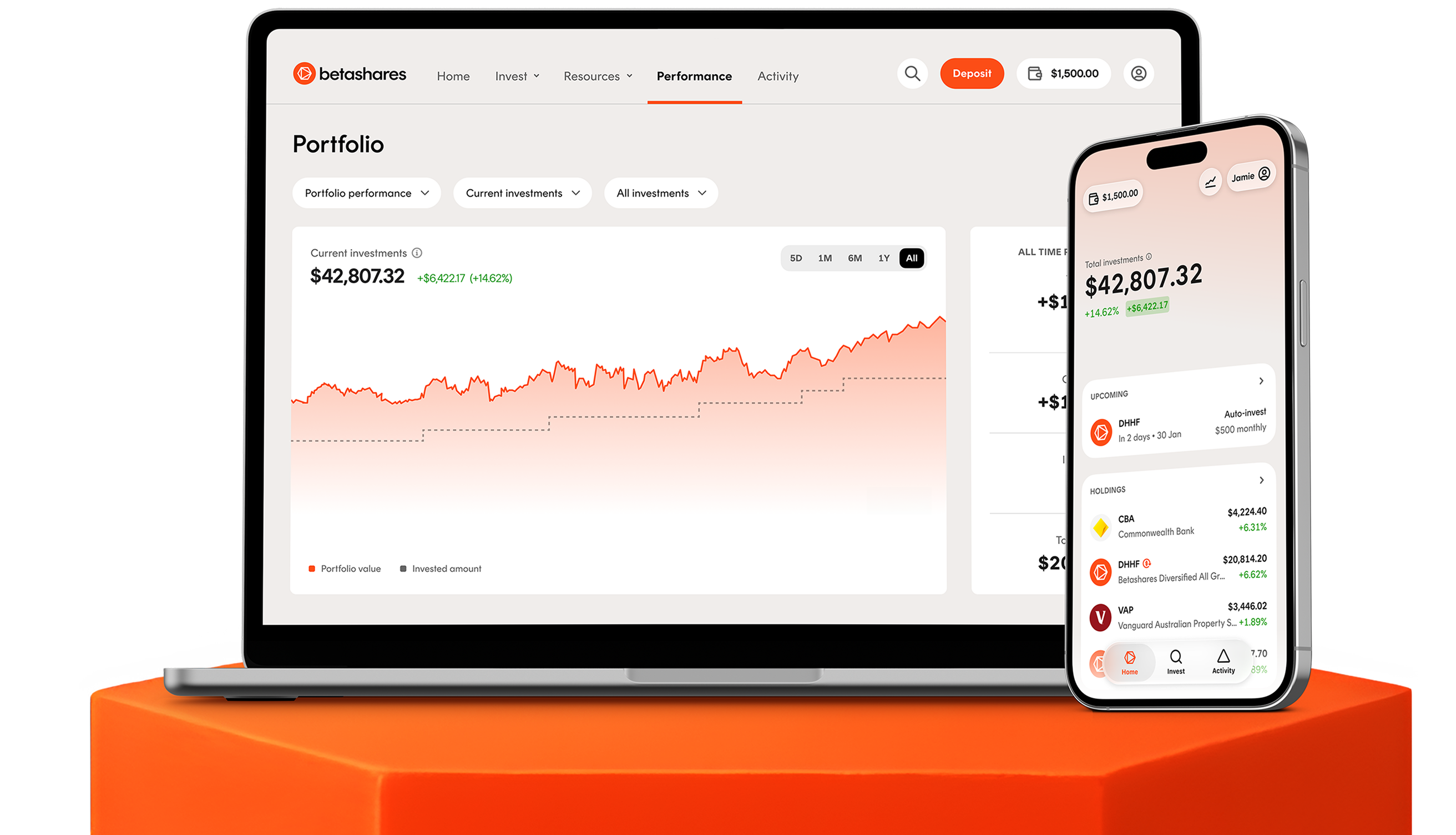

Join thousands of Australians who have switched to Betashares Direct

Lay the foundations

for investing success

Whether you’re a parent, grandparent or loved one, Betashares Direct makes investing for children simple and cost-effective, and helps build good habits into your investing strategy from day one.

Start small

Invest as little as $10. With $0 brokerage and fractional investing, you never waste a cent.

Automated investing

Make regular, automatic contributions to build wealth for your child over the long term.

Learning toolbox

Resources to help your child develop investing skills that last a lifetime

Start small

Invest as little as $10. With $0 brokerage and fractional investing, you never waste a cent.

Automated investing

Make regular, automatic contributions to build wealth for your child over the long term.

Learning toolbox

Resources to help your child develop investing skills that last a lifetime

Start small

Invest as little as $10. With $0 brokerage and fractional investing, you never waste a cent.

Automated investing

Make regular, automatic contributions to build wealth for your child over the long term.

Learning toolbox

Resources to help your child develop investing skills that last a lifetime

Gift the power of compounding

Starting your child’s investing journey early means you get the most out of compounding. Small, regular contributions can grow into something big by the time your child reaches adulthood.

Help them build a bigger future

Open an account today and give your kids a financial head start.

Everything you need, in one place

Use Managed Portfolios, high-growth ETFs, or shares as the building blocks for your child's portfolio.

Managed & Custom Portfolios

Choose from 12 Managed Portfolios or build your own Custom portfolio from scratch.

ASX shares and ETFs

Invest in all ETFs and [[shares]]+ shares traded on the ASX, with no minimum investment.

Focused Portfolios

Choose from a range of portfolios designed to meet a specific investing goal or strategy.

Wealth Builder ETFs

A range of cost-effective internally leveraged ETFs providing convenient exposure to the market.

Managed & Custom Portfolios

Choose from 12 Managed Portfolios or build your own Custom portfolio from scratch.

ASX shares and ETFs

Invest in all ETFs and [[shares]]+ shares traded on the ASX, with no minimum investment.

Focused Portfolios

Choose from a range of portfolios designed to meet a specific investing goal or strategy.

Wealth Builder ETFs

A range of cost-effective internally leveraged ETFs providing convenient exposure to the market.

Managed & Custom Portfolios

Choose from 12 Managed Portfolios or build your own Custom portfolio from scratch.

ASX shares and ETFs

Invest in all ETFs and [[shares]]+ shares traded on the ASX, with no minimum investment.

Focused Portfolios

Choose from a range of portfolios designed to meet a specific investing goal or strategy.

Wealth Builder ETFs

A range of cost-effective internally leveraged ETFs providing convenient exposure to the market.

The ins and outs of investing for kids

Everything you need to know about investing for children, how a Betashares Direct Kid's Account works, tax, and getting your child involved.

The parent's guide to investing for children

Investing is one of the most powerful ways to give a child a financial head start.

Whether you're putting aside a gift for a newborn or teaching your teenager how the share market works, this guide will help you navigate the options, tax rules and best practices involved in investing for kids in Australia and building long-term wealth for the next generation.

Why start investing for kids?

Children have one of the greatest financial advantages on their side: time. By starting to invest for them early, you can harness the power of compounding returns and teach them valuable money lessons along the way. Investing for kids isn't just about future financial security — it's also a chance to build financial literacy, discipline and a sense of ownership from a young age.

Ways to invest for kids in Australia

There's no one-size-fits-all approach to investing for kids. Each of the following options has its own mix of costs, tax rules and how much control you keep.

- Informal trust (minor trust): The most popular option. You (the trustee) open and control the account, with the child listed as the beneficiary. When they turn 18, you can transfer the investments to them. It's simple, low-cost and is the approach used in Betashares Direct's Kids' Accounts.

- In your own name: You invest under your name, but with the intention that the funds will eventually benefit the child. It's straightforward, but income and capital gains are taxed at your marginal rate — and transferring ownership later could trigger capital gains tax.

- Formal trust: A more advanced setup involving a legal trust deed. It gives you greater control and flexibility but comes with higher costs and a more complex tax compliance burden.

- Investment bonds: Long-term, tax-paid investment vehicles. Earnings inside the bond are taxed at 30% and, if held for over 10 years, withdrawals are generally tax-free.

- Superannuation for kids: Contributions can be made into a child's super fund, but the money is locked away until their retirement.

How to build an investment portfolio for your child

A kid's investment portfolio doesn't need to be complex. You might:

- Handpick a range of ETFs to gain exposure to a range of asset classes

- Invest in a diversified managed portfolio

- Add individual shares from brands your child recognises and is curious about

With a Betashares Direct Kids Account, you can build a portfolio using 350+ ASX-listed shares and ETFs, professionally built Betashares Managed Portfolios, and Auto-invest and reinvestment tools to keep things simple.

Why time and compounding matter

When investing for kids, the single most powerful force on your side is time. Even small, regular investments can grow substantially over time.

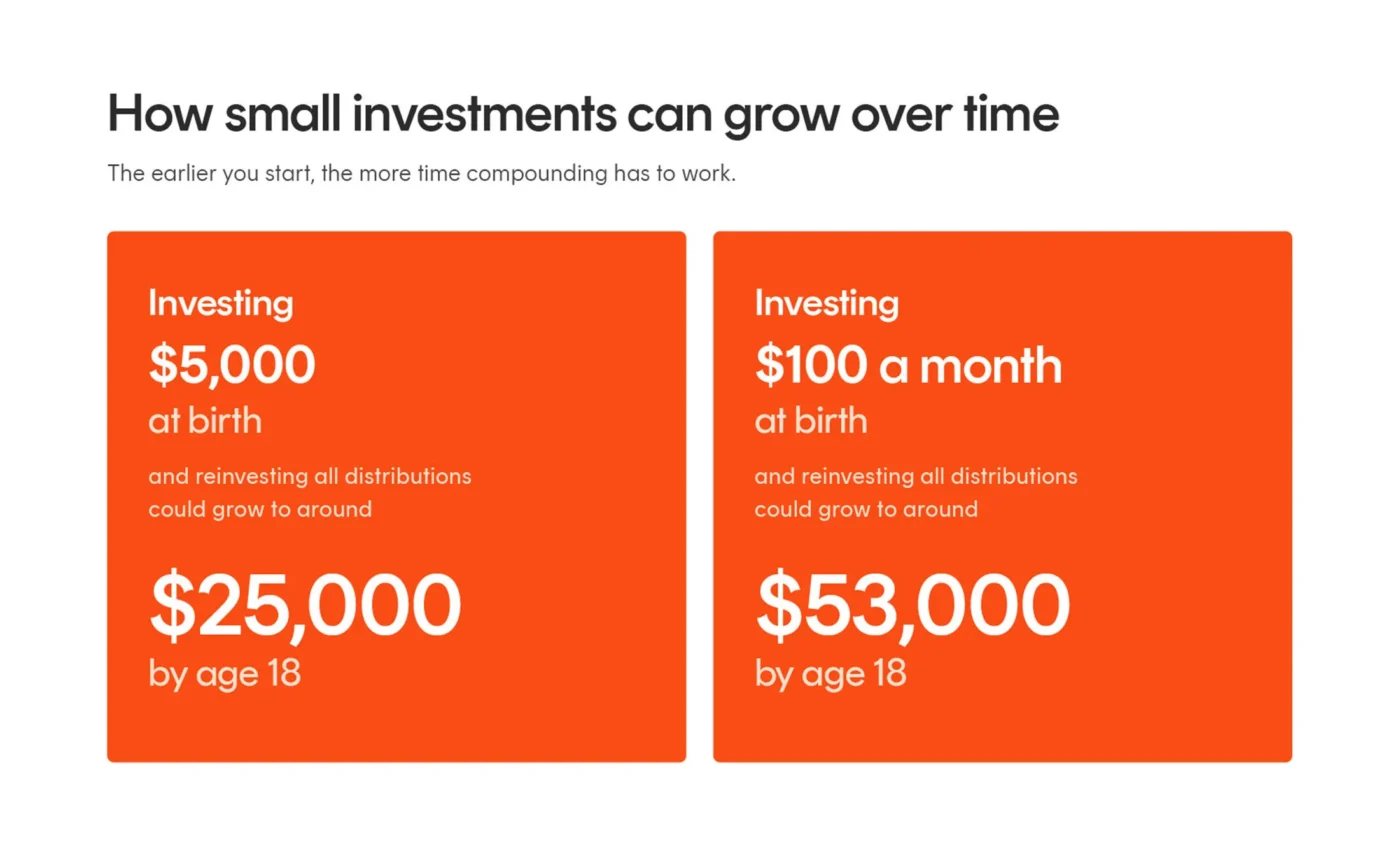

As a hypothetical example, imagine investing $5,000 at birth and achieving a 9% average annual return. By age 18, that one-off investment could grow to over $23,500. Or consider investing $100 a month from birth to age 18 — with an average 9% annual return, that could grow to over $53,600.

How to automate investing using dollar-cost averaging

Consistency is key to long-term investing. Dollar-cost averaging (DCA) — investing a fixed amount at regular intervals — can help smooth out volatility and remove the pressure of trying to time the market.

Automate in 3 easy steps:

- Choose your ETF(s): Select up to five Betashares ETFs that suit your child's goals.

- Set your contribution: Decide how much you want to invest and how often.

- Turn on Auto-invest: Let it run and build your child's future, one contribution at a time. Auto-invest is brokerage-free into up to five Betashares ETFs.

Fees matter when investing for kids

Keeping fees low is especially important when investing for kids, since small differences compound over time. Even a 1% difference in annual fees can lead to significantly different outcomes over decades.

With Betashares Direct, you can invest brokerage-free with as little as $10 in all ETFs and [[shares]]+ shares traded on the ASX.

Tax rules for investing for kids in Australia

Minors can't legally own investments outright, so parents or guardians typically invest on their behalf. Betashares is not a tax adviser — investors should obtain professional, independent tax advice before making an investment decision.

If the investment is for the child's benefit, the child is the beneficial owner. If their income exceeds $416 a year, special tax rules for minors apply — income between $417 and $1,307 attracts a tax rate of 66%, and any income above $1,307 is taxed at 45%.

Getting started: a simple checklist

- Choose your structure: Pick an investment structure and set up a bank account for income.

- Open the account: Create a Kids Account for each child and make your first deposit.

- Select investments: Choose from ETFs, Managed Portfolios or ASX-listed shares.

- Set up automation: Turn on Auto-invest and consider reinvesting distributions.

- Keep records: Track contributions, ownership and tax info.

- Involve your child: Include them in decisions as they grow to build financial literacy.

Investing for your child is more than a financial decision. It’s a long-term gift that teaches resilience, planning and the power of small actions over time.

With the right structure, strategy and support, you can help set your children up for a future of financial confidence – and give them the resources to shape their own future.

Ready to start investing for your child?

Ready to start investing for your child?

Betashares Capital Limited (ABN 78 139 566 868, AFSL 341181) is the issuer of Betashares Invest, being the IDPS-like scheme available through the Betashares Direct platform. Before opening an account or making an investment decision, read the Product Disclosure Statement and the Target Market Determination for Betashares Invest, available at www.betashares.com.au/direct or by contacting Customer Support by email at [email protected]or by phone on 1300 487 577, to consider whether the product is right for you. Betashares is not a tax adviser. This information should not be construed or relied on as tax advice and investors should obtain professional, independent tax advice before making an investment decision

How to talk to your kids about investing

Investing is one of the most powerful money lessons you can pass on to your child, and the earlier it starts, the better.

While many kids are taught to save, few learn how to make their money grow. Investing often feels too complex or too adult — something they'll 'figure out later'. But by then, the chance to build good habits early, or benefit from compounding, may have already passed.

Why start now?

Children form their core money habits as early as age seven1, according to researchers from the University of Cambridge. At that age, many already understand concepts like saving, planning and making trade-offs, based on what they see and hear at home.

Teaching kids about investing early helps them:

- Understand the power of compounding

- Think long term, not just about what they want now

- Build confidence and a healthy relationship with money

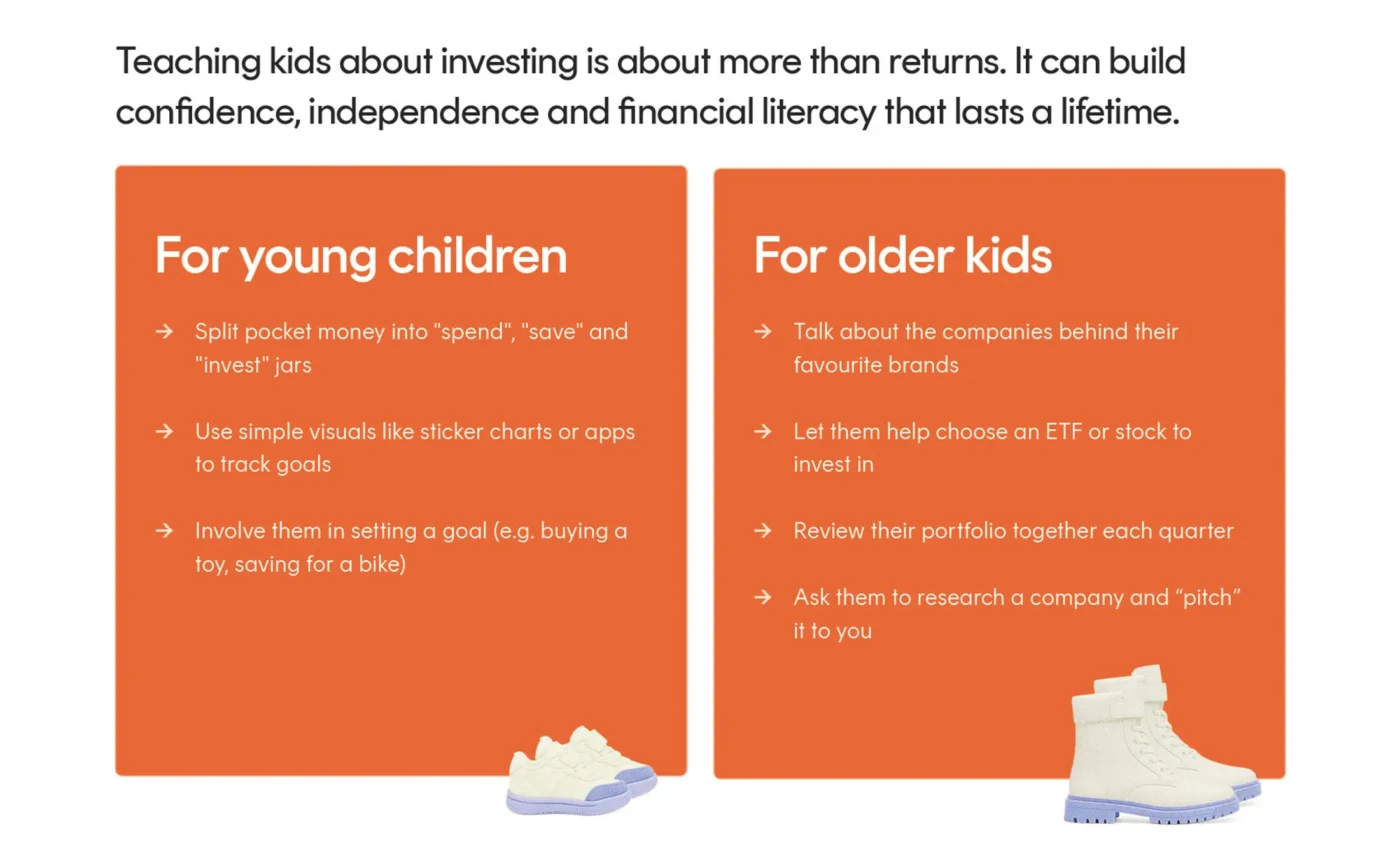

Early years to tweens (ages 7–12)

At this stage, it's less about dollars and cents and more about building the right mindset. Focus on simple, hands-on experiences that make growth, patience and trade-offs feel fun and meaningful.

Try this:

- Use jars or envelopes labelled 'Spend', 'Save' and 'Grow'. Let them add coins and see how each pile changes over time.

- Offer small trade-offs: "You can spend this now or wait a week and have double."

- Ask which companies they like and explain how investing lets you own part of a business.

- Link their favourite brands to real-world investing: Roblox for gaming stocks, Netflix for tech stocks or Lovisa for retail stocks.

- Encourage your child to save a portion of any pocket money they receive.

Tweens to teens (ages 12–17)

As they begin to earn their own money or plan for life after school, teenagers are more ready to understand goals, trade-offs and even risk.

Try this:

- Set a long-term goal together: "Let's see how much your investments could grow by age 18."

- Match their birthday money if they choose to invest it.

- Explore big themes — climate, innovation, equality — and help them find ETFs that align with their values.

- Introduce the idea of risk and reward. Explain that markets rise and fall, and patience matters.

- Let them co-manage a real account in small ways, making choices together.

- Share your own investing story (the wins and the mistakes).

- Use the news as a learning tool. Ask "Why do you think this happened to the market?"

Make investing part of everyday life

Your children are already learning from you how you handle money. When it comes to investing, you don't need a perfect script — you just need to bring them into the picture.

These small, real-life moments help investing feel familiar, not abstract or intimidating. Over time, it can become part of how they see the world, and how they shape their own future.

Tools and resources

- Investment account for kids — A real investment account held in your name but designed to benefit your child.

- Kids Account calculator — An easy way to show how small amounts can grow over time.

- Investing courses — Short, practical lessons covering ETFs, diversification and long-term thinking.

You don't need to be an expert. Just showing up and having the conversation is what matters most.

Want to start today?

Explore the Betashares Kids Account or use the calculator to begin your child’s investing journey.

What happens when your child turns 18?

Investing for your child is more than a nice idea – it could be one of the most important financial decisions you make. A small amount invested early could have decades to grow, to help pay for education, a first car or even a house deposit one day.

However, children under 18 can’t own shares or ETFs in their own name. This means their investment account needs to be set up differently. Here’s how a Betashares Direct Kids Account works, from trust structures and tax rules to what happens when the child turns 18.

Importantly, this article should not be construed or relied on as tax advice and investors should obtain professional, independent tax advice before making an investment decision.

The structure: Informal trust, formal responsibilities

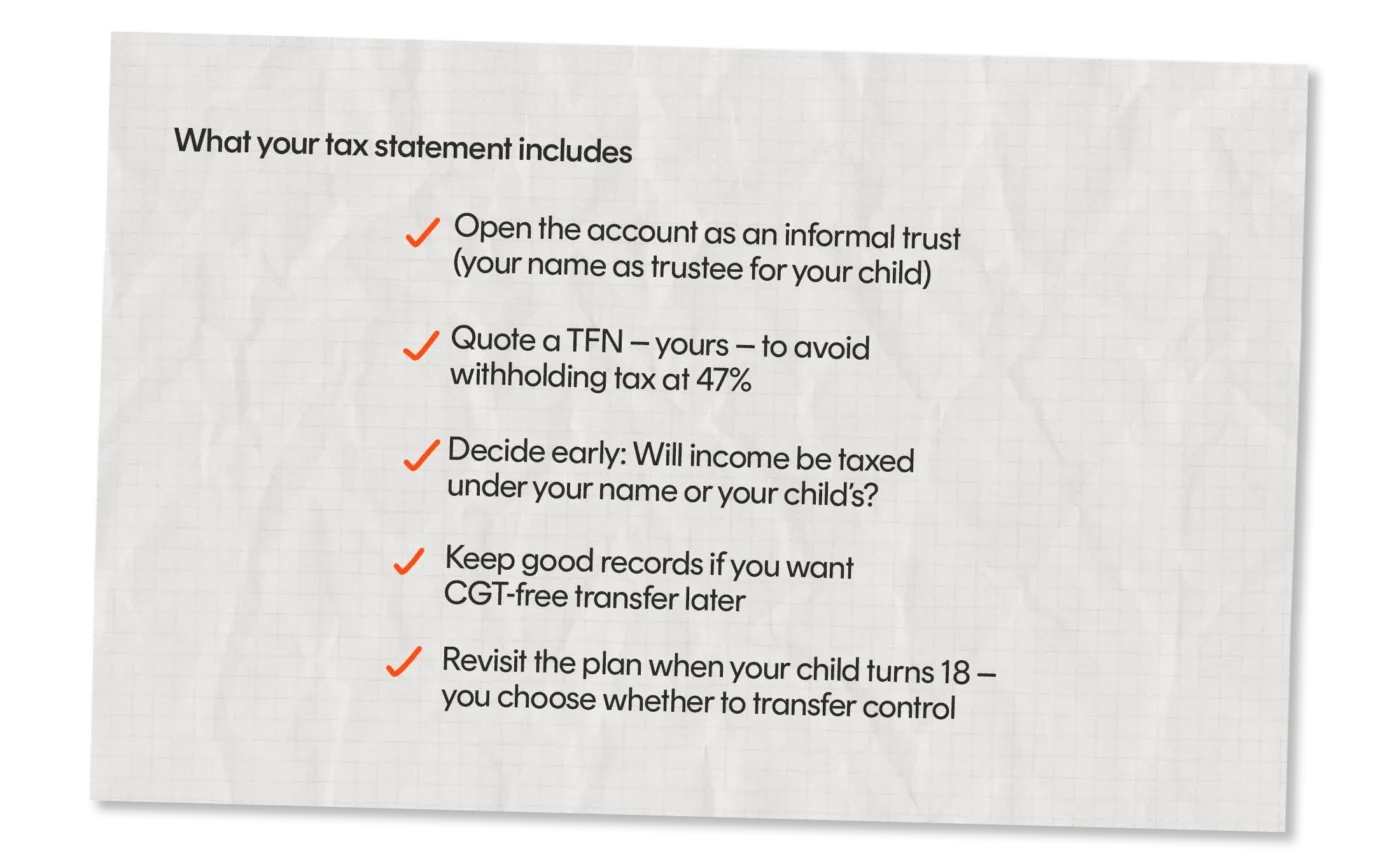

When you open a Kids Account on Betashares Direct, you're setting up what’s commonly referred to as an informal trust. That means you (the adult) are the trustee while your child is the beneficiary.

- You're in control: As the trustee, you make all the decisions – what to invest in, when to buy or sell and whether or not to withdraw any money.

- The account is in your name: It’s legally yours, although it’s usually labelled as “[Your name] A/C [Child’s Name]”..

- Your child is the beneficial owner: They don’t hold or control the account, but the investments are held for their benefit. And once they turn 18, you can choose to hand over control.

That last part is important: you don’t have to transfer the investments when your child turns 18. The decision – and the timing – is up to you.

Tax and TFNs: what you need to know

Tax matters – especially when investing for someone under 18.

Withholding tax on investment income

Because the investments in a Kids Account are held in your name as the trustee under the informal trust structure, you should consider providing your Tax File Number (TFN) when setting up the account. If you don’t, the ATO requires that a 47% withholding tax be applied to the investment income.

Income tax on investment income

Other than the withholding tax matter, you might consider setting up a TFN for your child as there is no minimum age to do so, if you're planning to declare the investment income in their name (see below).

It’s important to consider who owns and uses the funds in relation to a Kids Account to determine who is liable for income tax:

- If you declare income on your own tax return, you are considered the beneficial owner of investments. This has a capital gain tax consequence when the investments are transferred to your child in the future.

- If you treat the income as your child’s – declaring it on their tax return, not using it for your own expenses – they are considered the beneficial owner of the investments. Any future transfer of investments from the Kids Account to your child (i.e. into an account held in their own name, after they become 18 years of age) is unlikely to be subject to capital gains tax.

Just keep in mind that if you declare investment income in your child’s name, they’ll be taxed under special rules for minors. The tax-free threshold is lower than it is for adults, and higher tax rates can apply once investment income adds up. But if you’re investing small amounts or focusing on long-term capital growth rather than income, the impact can be minimal.

Handing over the reins: What happens when your child turns 18

First things first, there’s no automatic transfer when your child becomes an adult. You can choose to hand over control whenever the time feels right.

To do that, your child will need to open their own individual account on Betashares Direct. Then, you can arrange an ‘in-specie transfer’ – meaning the investments are moved over to the account held in the child’s individual name without having to be sold.

This can happen without triggering capital gains tax (CGT), as long as the trust arrangement for your child is preserved. There are a few conditions to consider (noting this is not an exhaustive list):

- The account must have been genuinely held for your child’s benefit

- Any investment income was declared on their tax return

- You haven’t used any income generated from the child’s account for yourself.

If the applicable requirements are met, the transfer should be CGT-free. If not, the ATO may treat it as a ‘disposal’ of assets, and CGT could apply. We suggest you speak to your tax adviser about your personal circumstances to determine if CGT will apply to such a transfer.

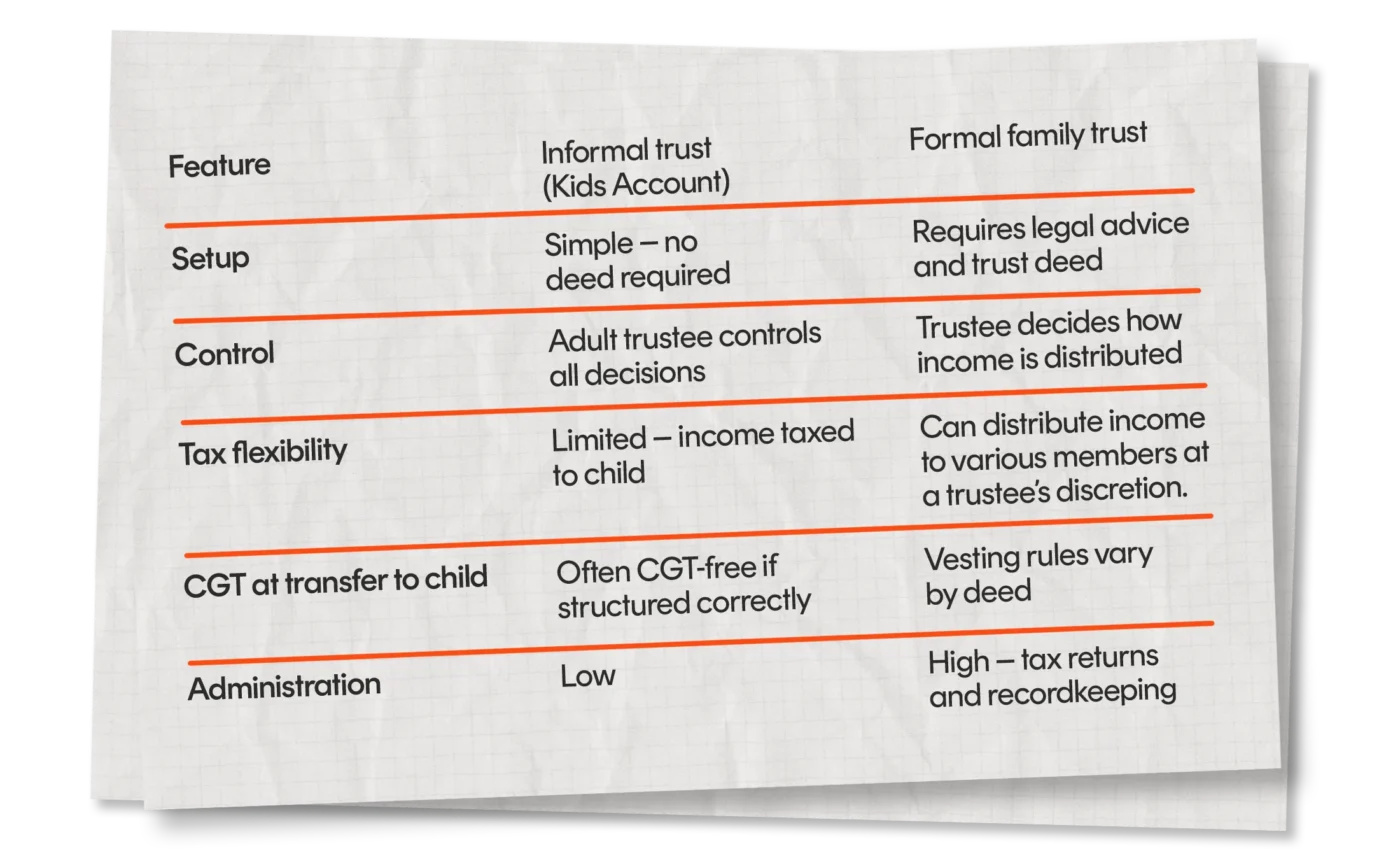

A note on formal trusts

For many families, a kid’s investing account – structured as an ‘informal trust’ – can be a simple way to invest on behalf of a child.

But in some cases, families may consider setting up a ‘formal trust’ (usually set up as a family or discretionary trust). These require formal trust documentation to set up, come with more administration and are usually used as part of broader estate planning or family wealth structures.

The following table offers a comparison of the two formats.

Unless you already have a formal trust in place, need tax flexibility across multiple beneficiaries or have other specific requirements, a Kids Account that is an ‘informal trust’ can often be a more simple and straightforward option.

Ready to get started?

A Kids Account on Betashares Direct can be a simple, low-cost way to invest for your child. It provides a structure that can help to ease the administration burden (including when it comes to tax), as well as control over when to transfer assets to the child after they turn 18, so the account works for you today and for them in the years ahead.

A Betashares Kids Account can make it easy to invest on behalf of a child.

Open an account in minutes, with low fees and a range of investment options designed for long-term growth.

Learn more and open a Kids Account on Betashares Direct.

Why invest for your kids?

As the cost of independence rises, early investing gives your child a meaningful head start, and you a quiet sense of progress.

When you imagine your child at 18, 25 or 30, what do you see?

Maybe it’s them moving into their own place, studying something they love or simply having the freedom to choose their next step with confidence.

But flexibility takes planning, and many of the milestones once associated with adulthood now come with a significant financial hurdle.

A high HECS debt is no longer uncommon, median weekly rents recently topped $650 a week1 and house prices in Australia’s largest cities have almost doubled2 in the past 10 years. That may be why, according to Mozo, more than 60% of first-home buyers in Australia now receive some form of financial help from their parents, with the average gift in 2025 over $74,0003.

One way to shift that dynamic is by investing early. Whether or not you plan to help your child with a house deposit, having an investment fund for them can be a way to quietly build a future buffer, giving your child a gift when they need it most.

The case for starting early

You don’t need a finance degree or a large income to invest for your child. What you need is time – and consistency.

That’s because of compounding: the snowball effect where your investment earns returns, and then those returns earn returns of their own. It’s one of the most powerful forces in long-term investing, and the earlier you begin, the more powerful it becomes.

To really understand the benefits of investing early, it helps to look at how small, consistent contributions can grow over time. Here’s what that could look like, assuming an annual return of 8.65% (the 10-year annualised return of the S&P/ASX 200)4

- Contributing $50 a month from birth to age 18 could grow to over $25,000

- Left untouched until age 30, that same investment could grow to over $69,000

- A $5,000 one-off investment at birth could be worth over $22,000 by the time your child turns 18 – and more than $60,000 by the time they are 30

These are modest investment amounts but, when given time to grow, can open up real opportunities, while reducing the future financial pressure on both you and your child.

More than a deposit: the gift of opportunity

For some young Australians, the first big expense won’t be a mortgage – it might be life itself.

A full-time degree without time to work. A gap year spent volunteering. An internship that opens the right doors. Or simply a chance to move out and start fresh.

These experiences can shape who your child becomes, but they often come with a cost.

Early investing can help fund these moments (or at least reduce the financial strain). A financial head start might allow your child to say yes to the things that matter, without relying on credit cards or loans – one of the most practical benefits of investing early.

Building a mindset, not just a balance

Perhaps most importantly, investing for your child can help them understand how to build and maintain their own wealth over their lifetime.

When you invest on behalf of your child, you’re not just building their portfolio. You’re shaping how they think about money, how to plan ahead and the importance of consistency. Both you and your child may even learn how to ride out market uncertainty – especially if your money will be invested for a long time.

These are habits that extend well beyond finances.

It’s well documented that a child who grows up financially literate is more likely to have healthy financial behaviours later in life and to see money as a tool for freedom, not stress. That mindset is often fostered by parents who involve their children in the money decisions of the household and, when done well, can last longer than the money itself.

The quiet benefits of investing early

There are many benefits of investing early, financial and beyond. Many people assume investing for kids is only for the wealthy or financially savvy. In reality, it’s never been easier to start small and start early.

With a Betashares Direct Kids Account, you can begin with as little as $10 or as much as you like. Choose from a range of diversified ETFs or Betashares Managed Portfolios, set up automatic contributions and let compounding do the rest.

As the cost of independence continues to rise, early investing can offer something subtle but significant: a financial head start that grows quietly in the background. It won’t solve every challenge your child will face – but it can ease a few of them, and widen the path ahead.

Sometimes, that’s all it takes to make a meaningful difference.

Sources:

Tax and investing for children

Investing on behalf of a child can be a powerful way to build long-term wealth for your child’s future. However, doing so effectively – and with proper regard to Australian tax law – requires a clear understanding of ownership structures, reporting obligations and ATO expectations.

In Australia, many investments for children are held in the name of a parent or guardian, but for the child’s benefit. These arrangements are often referred to as informal trusts. While simple to set up, they come with specific tax implications that are often misunderstood, especially when it comes to ownership, income and capital gains tax.

This guide explains how informal trusts work, what the ATO looks for and how to manage tax and compliance with confidence as your child’s investments grow.

Please note this information is general in nature only and should not be relied on as tax advice. Investors should consider obtaining professional tax advice before making an investment decision.

A quick note on capital gains tax (CGT)

Before diving into how tax works for children’s investments, it’s important to understand how CGT applies to investors in Australia. CGT is the tax you pay when you sell an investment, like shares or ETFs, for more than you paid (e.g. the cost at which you acquired the investment). The difference between the purchase price (called the ‘cost base’) and the sale price is the capital gain. Your cost base is typically your purchase price adjusted by things such as any returns of capital since you have held the shares or ETFs.

If you hold the investment for less than 12 months, the full capital gain is added to your taxable income. But if you’ve held the investment for more than 12 months, you may be eligible for a 50% CGT discount. This means you only pay tax on half the gain.

For example, say you bought $5,000 worth of units in an ETF and sold it five years later for $9,000. That’s a capital gain of $4,000. Because you held the investment for more than 12 months, you only need to pay tax on $2,000 of that gain. If your marginal tax rate is 32%, your CGT bill on the sale of the investment would be $640 - or 32% of $2,000.

Understanding how CGT works can help you make better long-term decisions, including how and when to transfer investments to your child.

What is an informal trust?

An informal trust is a simple way for parents to invest on behalf of their child without setting up a formal legal structure. The investments are held in the parent’s name, but the child is the ‘beneficial’ owner, meaning they’re entitled to the earnings and value.

It’s a common approach for families wanting to build wealth for a child without the complexity of having to establish and administer a formal trust.

CGT benefits: A key advantage

One of the biggest potential benefits of a trust arrangement is how CGT is handled when you want to transfer the funds to the child at any point after they turn 18.

As long as your child has always been the beneficial owner, you can generally transfer the investments into their name (through an ‘in-specie’ transfer) without triggering a CGT event. In other words, no tax is payable at the time of transfer, either by you or by your child.

Instead, your child takes on the original cost base and acquisition date for the investment - the amount you paid when you bought the investment. This means no CGT is triggered at the time of transfer from the trust to the child’s individual account (after they turn 18 years of age). If your child sells the investment in the future for more than the purchase price, CGT will be payable on the gain.

Legal vs beneficial ownership: What the ATO looks at

With an informal trust, the investment account is held in the parent’s name.

But if the investments are held for the child’s benefit, the child is the beneficial owner, i.e. the one who earns the income and ‘owns’ any capital growth.

For tax purposes, the ATO cares most about beneficial ownership. That’s what determines who should pay tax on income and whether the investment can be transferred tax-free after the child turns 18.

One of the most important requirements for this to occur is to be able to show that your child has been the beneficial owner since the acquisition of the relevant investment(s). The ATO considers several factors when assessing this, including where the funds to acquire the investment came from, who made investment decisions, and where any income earned from the investment was paid to (and by or for whom it was spent).

They also look at the intent and documentation around any gift or trust arrangement. For substantial amounts or more active trading, the ATO could apply additional scrutiny.

Why the source of funds matters

The source of the money used to invest plays a big role in deciding who the ATO sees as the beneficial owner of the relevant investment:

- Child’s own money: If the money comes from the child – like birthday gifts, pocket money or a part-time job – the child is the beneficial owner.

- Money gifted by a parent: If the parent gives money to the child, and that money is then used to invest, the child is the beneficial owner. To avoid any uncertainty, the nature and recipient of the gift should be clearly documented.

- Money still owned by the parent: If the parent invests their own money without formally gifting it to the child, the parent may still be regarded as the beneficial owner. This applies even if the intention is to use the money for the child later.

Tax File Numbers: How to get it right

When setting up an investment account for your child, you’ll need to quote your Tax File Number (TFN). This tells the ATO who the legal owner of the investment is and helps avoid unnecessary withholding tax. However, depending on the source of funds, there are different rules on who will be taxed on the income.

It’s more straightforward than it sounds. Here’s how to choose the correct TFN based on who beneficially owns the investment.

Declare the income under your child’s TFN if the money belongs to them

If the investment is genuinely for your child’s benefit, and the money came from them or was clearly gifted to them, you should consider including the income received from the investment on your child’s tax return.

To lodge a tax return, you need to obtain a TFN for your child. There is no minimum age to get a TFN. Parents or guardians can apply on behalf of a child, including babies, by completing a paper form through the ATO.

Declare the income under your own TFN if the money is still yours

If the funds you’re investing haven’t been formally gifted to your child, they’re still considered yours for tax purposes. This means the income should be declared under your TFN, even if (for example) the account is set up to help teach your child about investing.

This may apply if you plan to:

- Keep the investments in your name until your child turns 18, then transfer the assets to them, or

- Sell the investments later and gift the cash instead.

In either case, transferring the assets or cash to your child may trigger a CGT liability for you at the time of transfer.

What happens if no TFN is quoted?

If a TFN is not provided, the ATO requires that 47% tax be withheld from income derived from the investment.

Tip: If your goal is to invest on your child’s behalf and transfer the investment to them in the future without triggering CGT, it is important to ensure you keep clear records regarding the investment.

Income tax: What applies to children

If your child earns income from investments, like dividends or capital gains, that income usually needs to be reported to the ATO. The person who benefits from the investment (the beneficial owner) is responsible for declaring it. So, if the investment is held for your child, the income should generally be declared in their name, not yours.

Children under 18 are taxed differently to adults when it comes to investment income. The first $416 they earn from investments each year is tax-free. After that, higher tax rates apply, up to 66% and then 45%, depending on how much they earn. These special rules are designed to prevent the shifting of income into a child’s name to pay less tax.

If your child earns more than $416 in a year from investments, they’ll need to lodge a tax return. Even if they earn less than that, it can still be worth lodging to claim back any tax withheld or franking credits.

It’s worth noting that these tax rates only apply to passive income like investments held on behalf of a child. If your child has a job, that income is taxed at normal rates and is subject to the standard tax-free threshold.

Managing the transfer after your child turns 18

One of the biggest benefits of using an informal trust is what happens after your child turns 18.

As mentioned earlier, if they’ve always been the beneficial owner, you can generally transfer the investments into their name without triggering CGT.

The transfer, also known as an ‘in-specie’ transfer, is completed off-market (for listed or exchange-traded investments) and no tax is payable by you or your child. They also inherit the original cost base, which means any future capital gains (or losses) are based on what you originally paid to acquire the investment, not the value when you transfer the investment to your child.

Keeping good records helps ensure this process runs smoothly.

To establish beneficial ownership and ensure a smooth transfer, maintain thorough documentation, including:

- Evidence that the child was always the beneficial owner

- Records of dividend/distribution reinvestment plans

- Bank account statements showing the payment of any investment income into the child's account

Important considerations

Keeping clear records and separating finances can help ensure your child’s investments get the right tax treatment – and make it easier to provide supporting documentation for any CGT exemptions that may apply later on.

- Keep clear documentation: Record where the investment money came from, whether it was your child’s own savings or a gift from you. Supporting evidence like gift notes, bank statements or income records help show your child has always been the beneficial owner.

- Use a separate bank account: Set up a bank account in your child’s name, with you as trustee, and direct all investment income there. Keeping your child’s income separate from any income you receive helps to provide evidence that the income genuinely belongs to your child.

- Act in your child’s best interest: Make investment decisions with your child’s goals and time frame in mind. This includes reinvesting dividends or distributions where appropriate to support long-term growth.

Common pitfalls to avoid

A few small missteps can create tax issues or affect your ability to transfer investments to your child without attracting CGT later on.

- One common error is mixing funds. For example, when you combine money you’ve gifted to your child with money you intend to keep. To avoid uncertainty, clearly document when a gift is made and keep it separate.

- Another is declaring income in the wrong name. If your child is the beneficial owner, the income must be declared in their name, not yours.

- Lastly, not quoting the right TFN can lead to 47% tax being withheld from the investment’s income. This can usually be claimed back, but it adds extra complexity.

Avoiding these simple mistakes helps keep things on track and ensures the correct tax treatment in the long term.

The intent and documentation around gift or trust arrangements are also closely examined. For substantial amounts or regular trading, additional regulatory scrutiny may apply to determine beneficial ownership.

Getting it right for the long term

Investing for your child through an informal trust can be a simple and effective way to build long-term wealth, but it does require a clear understanding of tax rules and ATO expectations.

Clearly documenting beneficial ownership, using the correct TFN, reporting income properly and avoiding common pitfalls can help you stay compliant and ensure the correct tax treatment of investments in the long term.

For more complex arrangements or larger investments, it may be worth seeking advice from a qualified and registered tax adviser.

Common questions.

Clear answers.

A Betashares Direct Kids account is an account opened and operated by an individual (adult) on behalf of a person under the age of 18. It is structured as an informal trust, which allows the adult (as the trustee) to hold investments on behalf of a child (as the beneficiary).

Any adult (aged 18 years or older) can open a Kids account, such as a parent, grandparent, other relative or family friend.

As the account holder (being the trustee) and owner of the investments held in the account, you can choose to provide your TFN for withholding tax purposes. If you do not provide your TFN in relation to the account, we’ll need to deduct tax on any income at the highest marginal rate plus the Medicare levy.

Please note this is not tax advice, and we recommend consulting with your tax adviser.

At any time after your child turns 18, you can choose to transfer the assets in the Kids Account to the beneficiary. There are no obligations to transfer the investments to them, and you can continue to hold and operate the account if preferred.

Have more questions? Go to Betashares’ Help Centre for more information.

Built by Betashares

Open an account in minutes and start investing

[[aum]]

Assets under management

[[etfs]]+

ETFs across Australia/NZ

14+

Years serving clients

1M+

Australian investors served