Sticky inflation and the income challenge facing investors

This time last year, we were all confidently feeling the end of a higher rate environment. The RBA had just made its second rate cut and was priming for a third.

It’s taken less than half of 2026 for all that to be undone. The economy is running hot and oil prices are elevated with a fifth of the world’s supply still stranded on the wrong side of the Strait of Hormuz. Inflation, to use the widely popular term, is sticky, and the RBA has made it clear they’re not expecting that to budge until at least mid-next year.

For investors seeking income within their portfolios it can seem like there’s a silver lining here: cash and term deposit rates have gone up, with some climbing over 5%1 in recent weeks – their highest in at least a year.

Yet before rushing into cash and term deposits, investors may want to stop and think: what is the real return I’m getting?

One of the biggest pitfalls I see is investors only looking at the headline figure of income, not income above inflation, or what we call positive real income.

Imagine you had put $100 into a term deposit 10 or 20 years ago. Yes, you would have received income, but that $100 is still $100. How much of your grocery and fuel bill would it have covered then versus today? That is, in very simple terms, the impact of inflation on your core investment.

And so while it may be attractive to put more money into cash when interest rates are higher, you can in fact end up with a negative or very low real return. After all, the very reason that central banks raise rates in the first place is to control inflation, so if you’re getting a good return on cash, your money is likely getting eaten up by inflation at the same time.

I’ll come back to other options that offer both growth and income, but first I want to address a point that you might already be thinking: the allure of cash and term deposits is not just headline yields, but safety. This is particularly pertinent today, when geopolitical tensions seem never-ending, and the resulting market volatility can daunt those who simply want a place to invest their money for income.

When it comes to investing, there are always market jitters. I’m often asked how to avoid so-called black swan events — unexpected, high-impact market disruptions — and my answer is always the same: you can’t. By definition, they’re unpredictable. Rather than trying to anticipate every possible shock, investors should consider managing risks they can see, such as inflation, and diversifying their portfolios to buffer against the ones they cannot.

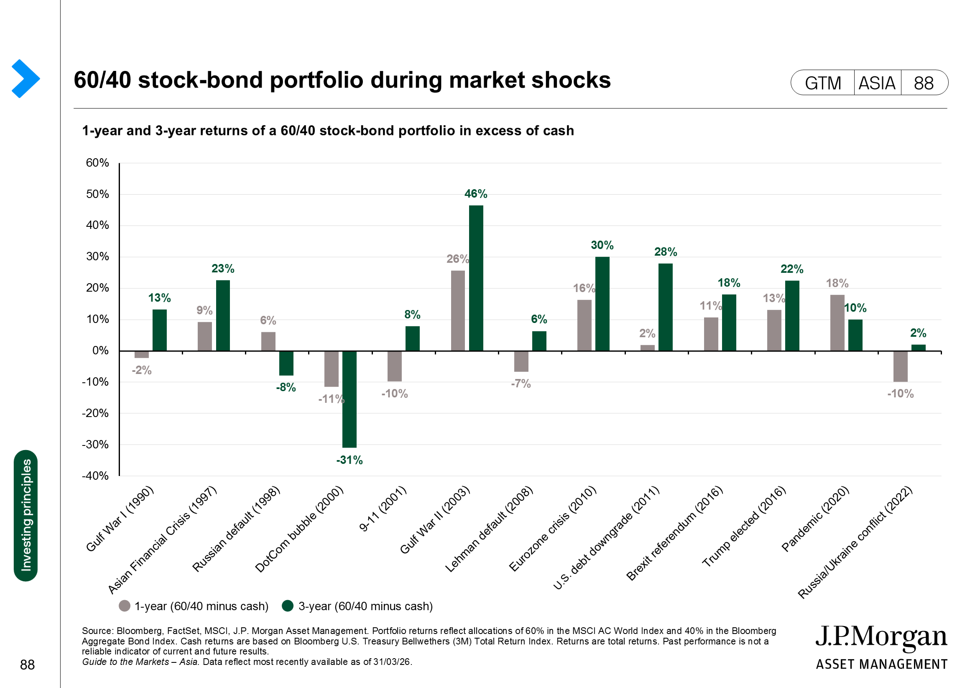

According to our own analysis, a portfolio that is 60% equities and 40% bonds has often outperformed cash over the three years following market shocks, although not in every case. The graph below shows the one- and three-year returns of such a portfolio over cash through events including the Russia-Ukraine conflict, the pandemic and the GFC. It’s a useful reminder that staying invested for the long term is often a better strategy than reacting to every bout of uncertainty.

Which brings us back to the question of building income-producing portfolios. If cash alone isn’t the answer, where should investors be looking to build this diversified portfolio that delivers income, growth and risk management?

It’s useful to remember what sits behind rising inflation: an economy that is still growing strongly. While that is a challenge for central banks, it can also create opportunities for investors. This is one reason why some equities are attractive, because a strong economy usually means strong corporate earnings, which can in turn support both dividend payments and capital growth, providing an income stream that has the potential to grow over time, with the added benefit of franking credits for Australian equities.

Another area is fixed income. Government bonds are offering more attractive yields than they have for years, while corporate bonds and selected areas of the high-yield market can provide additional income opportunities. Together, they form the basis of a broader toolkit for generating income and when it comes to high quality bonds they offer a cushion if the worst case scenario does play out and the black swans take flight.

Of course, opportunities like these shift across different asset classes and income sources over time. In a stable, low-rate environment, a more passive approach to income can work well. But when inflation is moving and central banks are responding to events beyond our borders, the case for active management becomes clearer: the ability to adjust where income is being sourced as conditions change, rather than holding a fixed allocation.

For investors who want this kind of exposure without spending their days analysing bond markets and credit conditions, the JPMorgan Managed Portfolios provide access to active management and experienced portfolio managers and are available through the Betashares Direct platform.

The suite includes the JPMorgan Income Portfolio, which is managed by our firm’s multi-asset solutions team and draws on global research capabilities across equities, fixed income, alternatives and currencies, with periodic rebalancing in response to changing market conditions and our team’s forward-looking views. The current trailing 12 month yield is 6.24% (as at 4 June 2026)2.

Sticky inflation, oil crises, black swan events. There’s little we can do to avoid them. Yet putting all your money into term deposits and cash because they feel safe and offer seemingly attractive rates can, in fact, erode purchasing power over the long term than many investors realise. The challenge is not simply generating income today but ensuring that income keeps pace with inflation and preserves wealth over time.

Diversification does not guarantee investment returns or eliminate the risk of loss. Investments involve risks and are not similar or comparable to deposits. Not all investment ideas referenced are suitable for all investors. Provided for information only, not to be construed as investment advice.

This material has been prepared by JPMorgan Asset Management (Australia) Limited (ABN 55 143 832 080) (AFSL No. 376919) being the model portfolio manager of the JPMorgan Active Income (J.INC) and JPMorgan Active Growth (J.GROW).

This material does not constitute an offer or solicitation to invest in any financial product, nor does it constitute any specific legal, tax, or accounting advice. The information contained herein is of a general nature and does not take into account your individual objectives, financial situation, or needs. Before acting on this information, you should consider its appropriateness, having regard to your own circumstances, and seek personalized financial advice.

J.P. Morgan Asset Management model portfolios are not funds issued by JPMorgan Asset Management (Australia) Limited. The model portfolios are offered through, and issued by, third-party platform providers and responsible entities who are not affiliated with J.P. Morgan Asset Management. Please obtain the relevant product disclosure statement and target market determination from these platform providers and responsible entities and consider these documents before making any investment decision.

The model portfolios included in these materials are for illustrative and educational purposes only. They do not constitute research, personalized investment advice, or an investment recommendation from JPMorgan Asset Management (Australia) Limited to any client of a licensed financial adviser. These model portfolios are intended for use by licensed financial advisers as a resource to help build a portfolio or as an input in the development of investment advice for their own clients. Such financial advisers are responsible for making their own independent judgement as to how to use the J.P. Morgan Asset Management model portfolios. JPMorgan Asset Management (Australia) Limited is not responsible for determining the appropriateness or suitability of any J.P. Morgan Asset Management model portfolios, or any of the securities included therein, for any client of a financial adviser.

Past performance is not a reliable indicator of future performance. Investments are subject to investment risks, including possible delays in repayment and loss of income and principal invested. JPMorgan Asset Management (Australia) Limited does not guarantee the success, performance, or return of capital from any investment strategy or model portfolio. J.P. Morgan Asset Management model portfolios include investments in funds and investors may indirectly bear fund expenses in respect of portfolio assets allocated to funds.

Forward-looking statements, opinions, and estimates in this document are based on assumptions and are subject to change without notice. Actual results may differ materially from those anticipated in such statements. To the maximum extent permitted by law, JPMorgan Asset Management (Australia) Limited and its directors, officers, employees, agents, and affiliates disclaim any liability for any loss arising from the use of this document or its contents.

1. Source: Publicly available deposit rates published by Australian financial institutions. As of date: June 10, 2026.

2. Distribution yield is calculated by summing the 12-month trailing distribution yields for the underlying ETFs in the portfolio in proportion to the underlying ETF weightings, except for Betashares FTSE Global Infrastructure Shares Currency Hedged ETF (ASX: TOLL) (which has an inception date of 28 Oct 2024 and does not have a 12-month trailing distribution yield), for which an index yield has been used (calculated based on TOLL’s index for the prior 12-month period). It does not take into account the impact of any withholding taxes on distributions received from offshore investments. Future distribution yields may differ due to various factors, including changes to the unit price and number of units on issue, as well as changes in market conditions. Yield may be lower at the time of investment. You cannot invest directly in an index. Past performance is not indicative of future performance.