David Bassanese

5 minutes reading time

Key global developments in June

- Optimism regarding a US-Iran peace deal intensified over the month, leading to a slump in oil prices and support for equity markets – especially outside of the US.

- A strong May US payrolls report and hawkish post-meeting commentary from the Federal Reserve raised US rate hike fears, which briefly pushed up bond yields and hurt tech stocks. The $US firmed.

- High-flying AI related stocks – in both the US and Asia – came under bouts of selling pressure as bubble fears waxed and waned.

- In Australia, a soft Q1 GDP report and easing headline inflation further modestly reduced rate hike expectations. Economic sentiment in the wake of the May Federal Budget tax increases remained subdued.

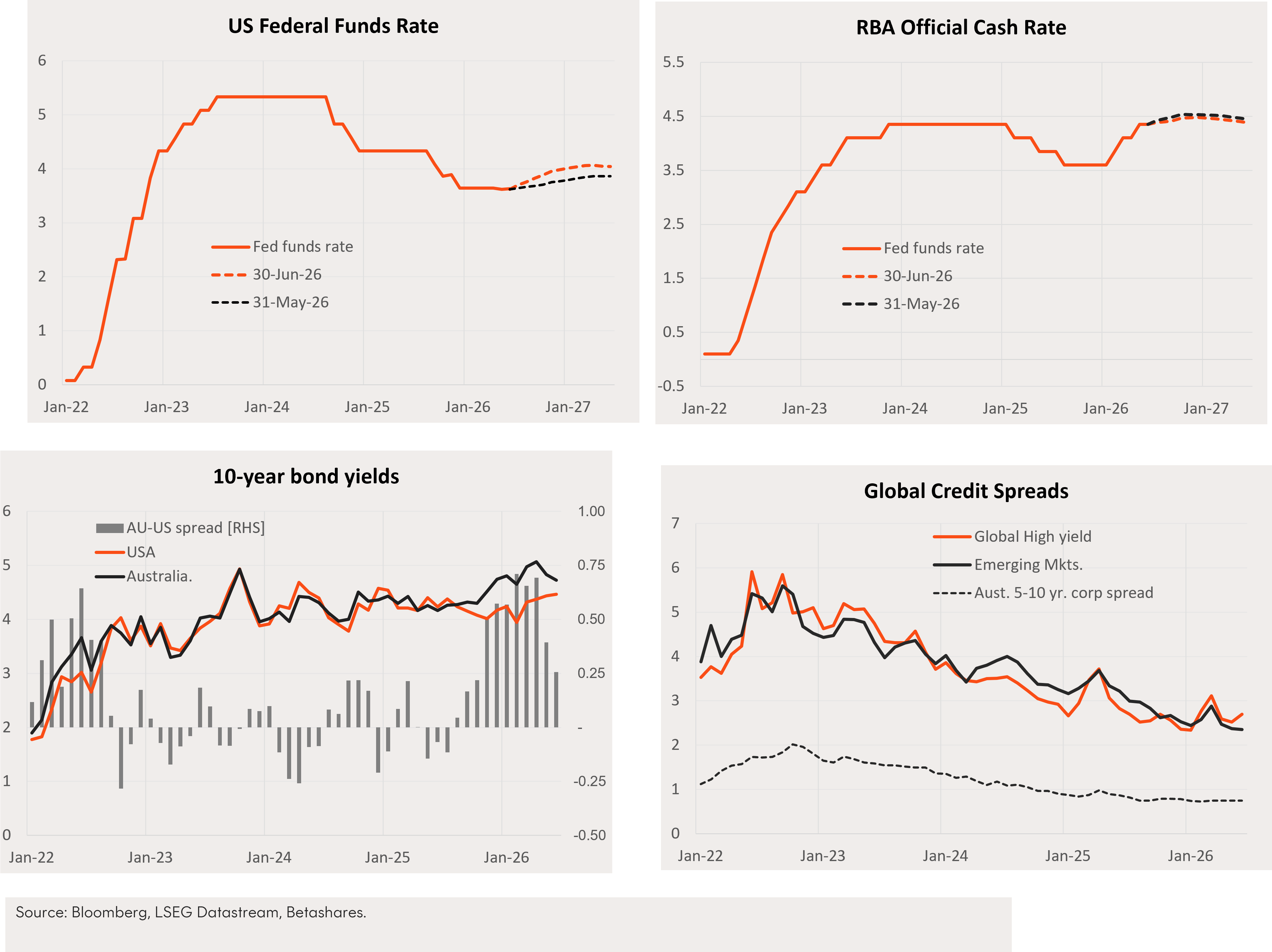

Interest rates

- There was a modest further shift in US and Australia monetary policy expectations in June, with expectations of higher US rates rising while they eased in Australia. Markets are pricing 0.4% of policy tightening by mid-2027 in the US, and 0.1% in Australia.

- US 10-year bond yields edged up by 0.03% to 4.47%, whereas Australian 10-year yields eased by 0.11% to 4.72%, resulting in a further narrowing in the Australian-US 10-year bond yield differential. Bond yields in both markets have been trending modestly higher since late 2025, due to a shift from rate cut to rate hike expectations. Assuming the worst is priced in terms of rate hike expectations, bond yields are likely to move sideways to down in coming months.

- Global high-yield spreads ticked up in June, while emerging market and local corporate spreads remained contained. Ongoing resilient global economic growth bodes well for continued tight credit spreads.

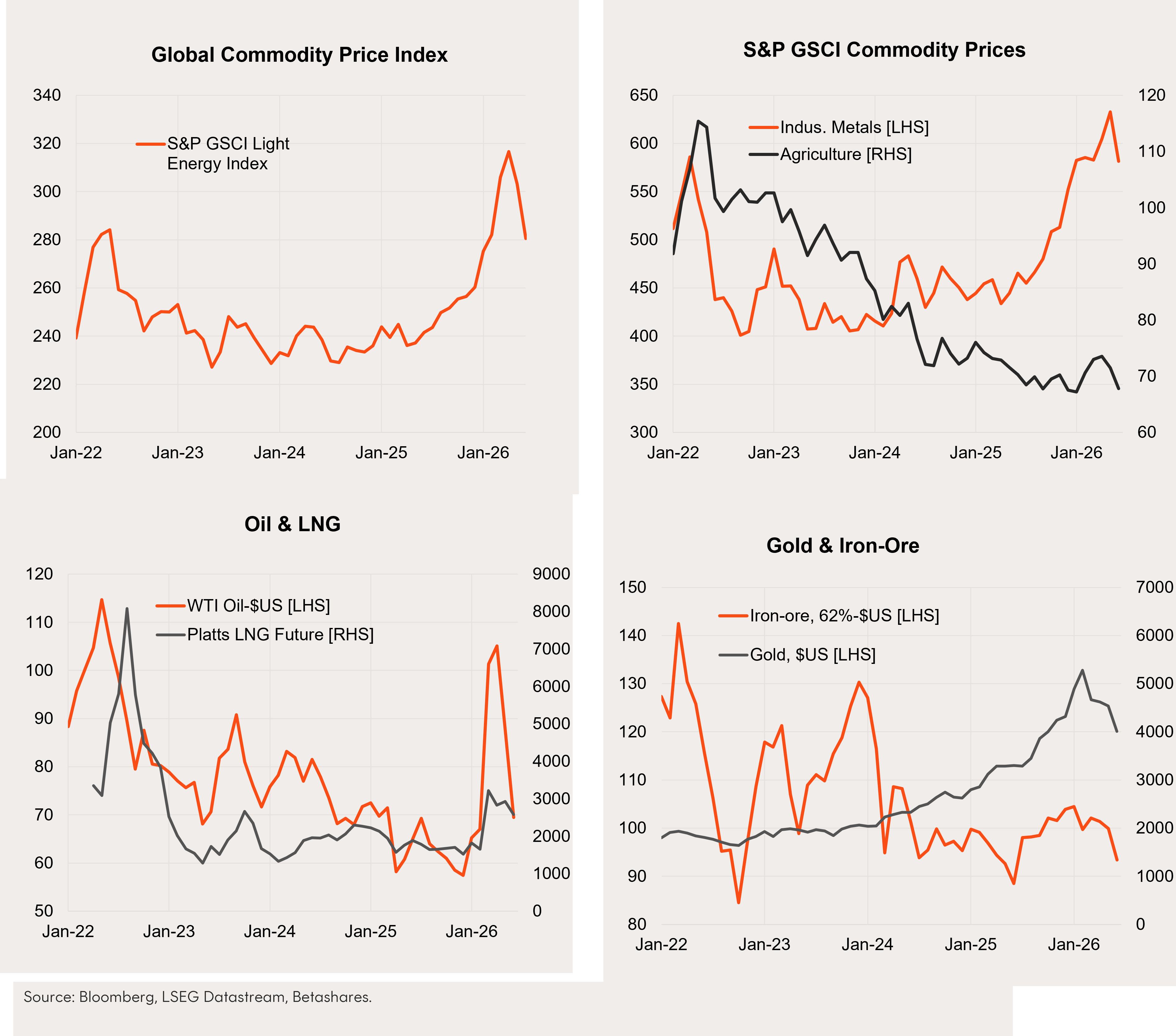

Commodity prices

- Optimism concerning the Iran war led the benchmark index of global commodity prices* to fall a further 7.5% in June.

- Oil prices fell sharply further, with weakness also evident in gold, industrial metals and agricultural prices. Assuming an enduring peace-deal is reached in Iran, commodity prices may ease further in coming months.

*Defined as the S&P GSCI Light Energy Index, which includes a range of prices covering energy, metals, agriculture and livestock.

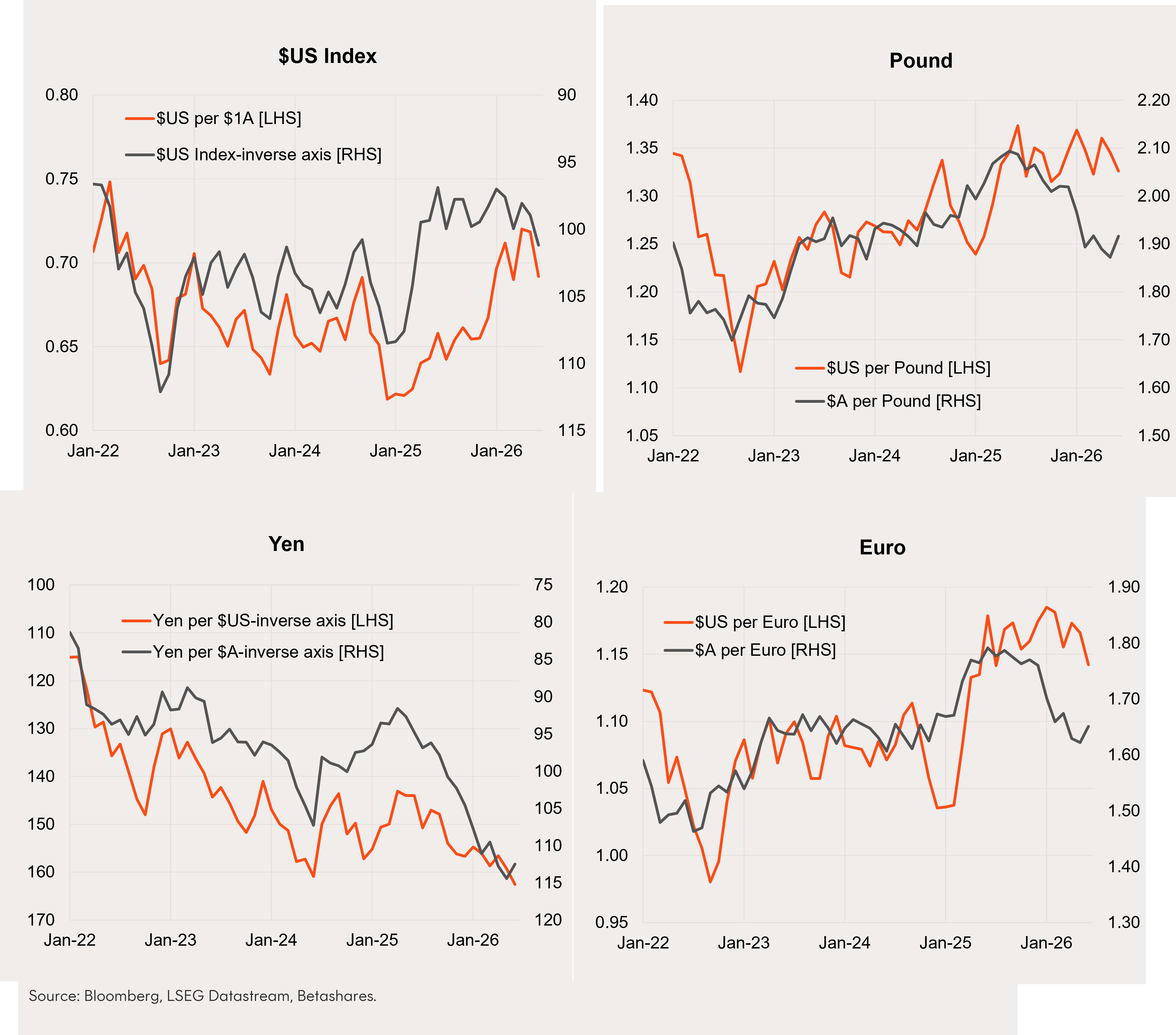

Exchange rates

- US rate hike fears led to a firmer $US in June, and a decline in the $A from US71.9c to US69.2c.

- A shift in the relative US-Australian interest rate outlook has checked the $A’s strength in recent months, though upward pressure on the $US could wane if the Fed – as I still expect – resists pressure to raise interest rates this year.

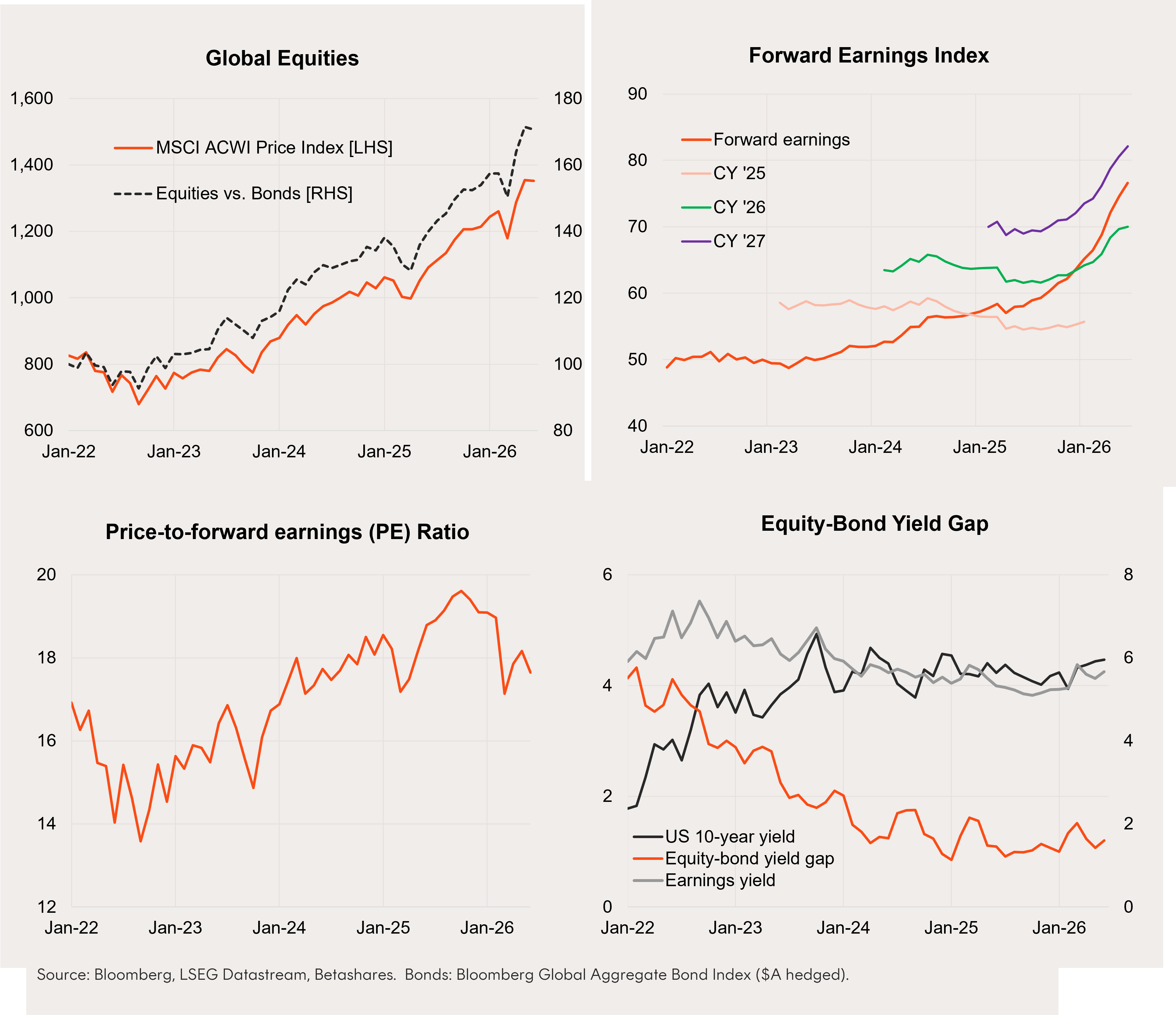

Global equities

- Global equity returns dipped 0.1% in June in local currency terms, but returned 3% in unhedged $A terms due to weakness in the $A.

- The flat global equity performance reflected a pull back in valuations, offset by a further lift in forward earnings. At 17.6, the global forward PE ratio is now down 11.2% from its recent end-month peak of 19.6 in October last year. More than offsetting this, forward earnings are up 25.5% over the same period.

- Global earnings expectations remain upbeat, with 7.2% expected further growth in forward earnings by year-end. PE valuations are at the lower end of their range over the past three years. Assuming relatively stable bond yields and continued strength in corporate earnings, the global equity outlook remains encouraging.

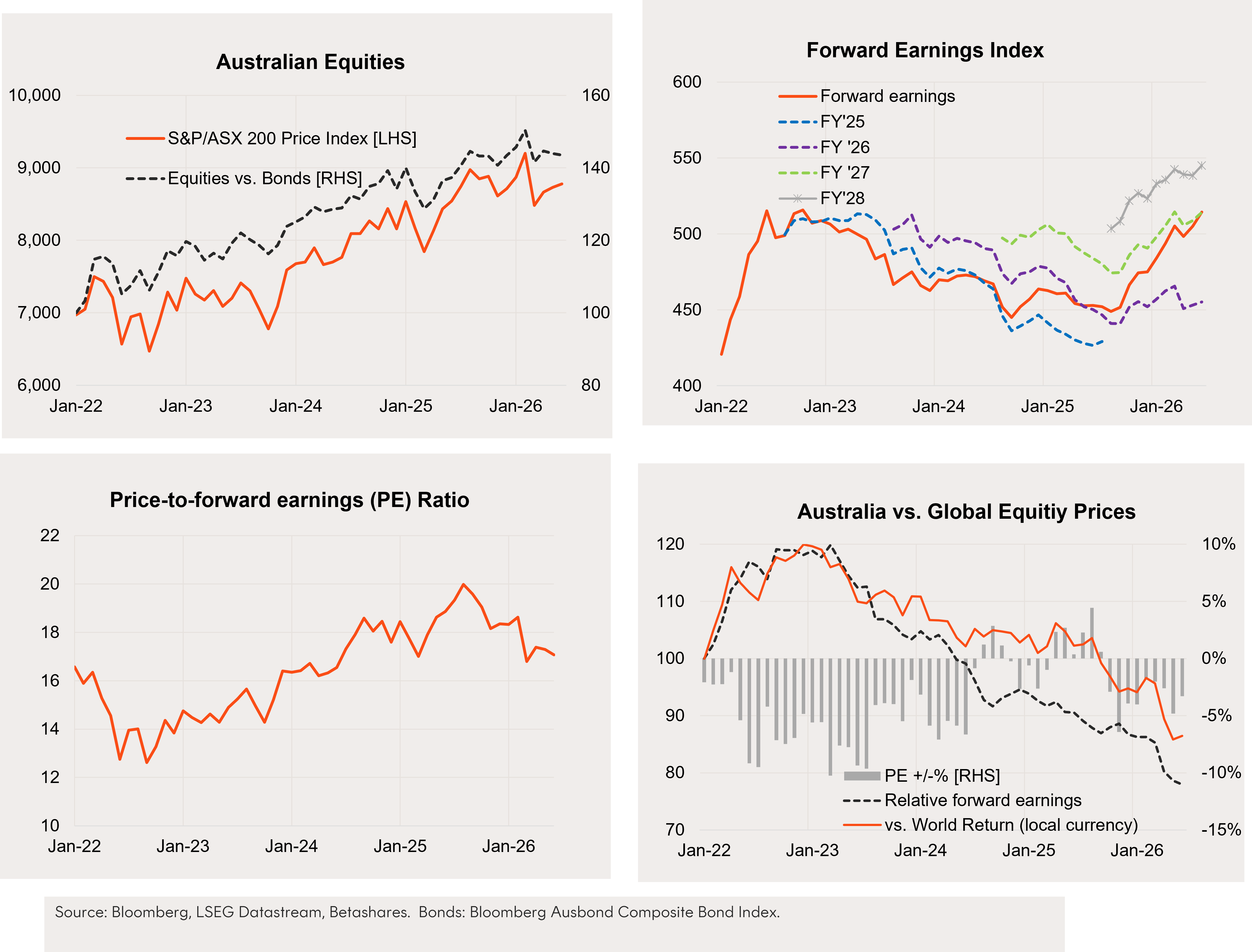

Australian equities

- Australian equities lifted modestly in June, with the S&P/ASX 200 returning 0.7% following a 1.1% gain in May.

- As was the case globally, a pull back in valuations held back returns though forward earnings lifted a solid 1.9%. Earnings expectations rose modestly in the month – largely reflecting materials – after some weakness in the prior two months.

- That said, current earnings expectations are consistent with only 3% growth in forward earnings by year-end – half that expected by the global market.

- At 17.1, the forward PE ratio ended June trading at a modest 5% discount to global markets and down from its recent peak of 20 in August last year. Australia’s weaker earnings outlook and likely subdued economic growth suggests a continued trend of equity underperformance versus global peers.

Equity themes/trends

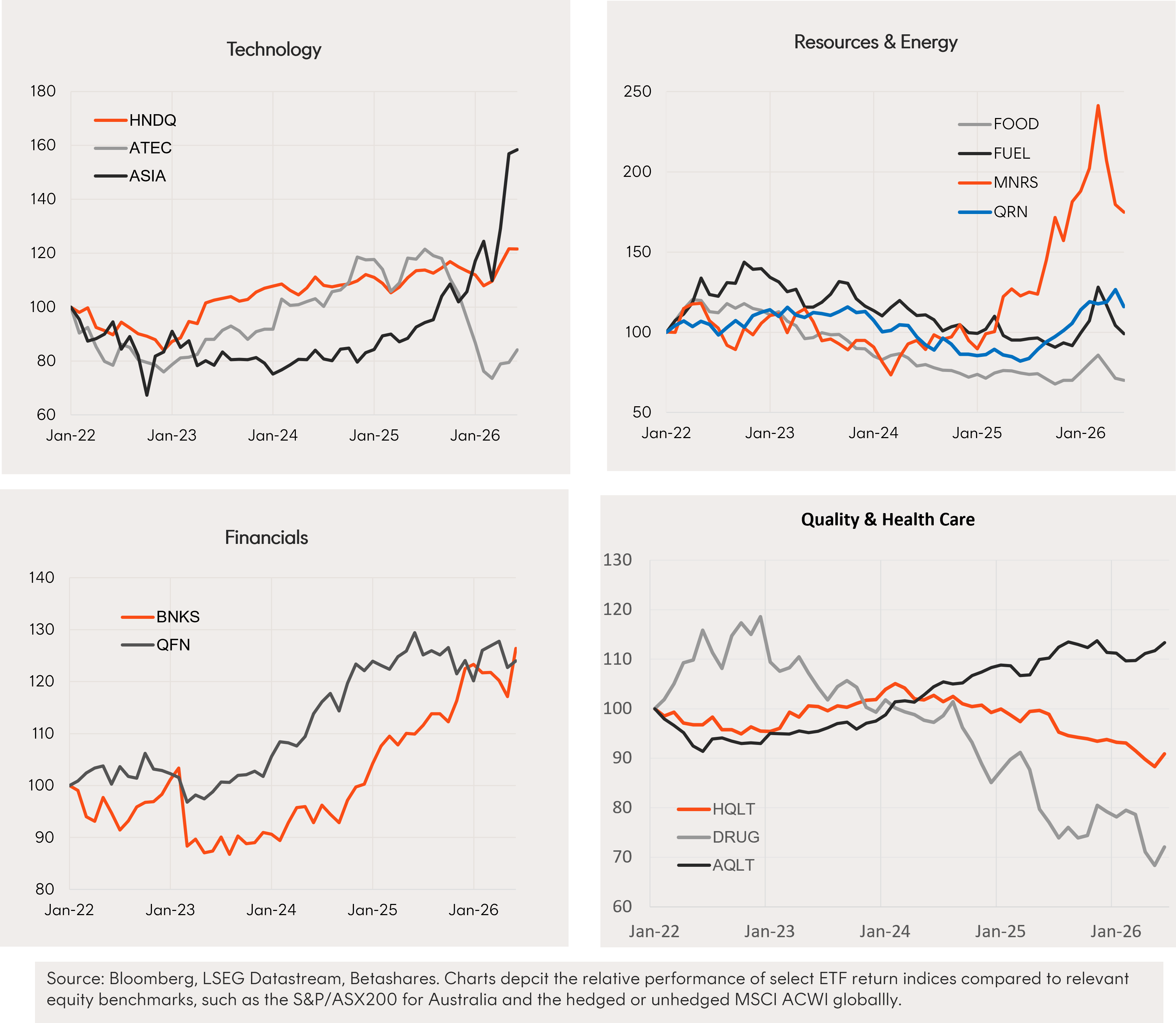

- Technology and commodities fared the worst over June reflecting both the fall back in oil prices on Iran optimism and the ongoing AI related tech concerns. By contrast, financials and health care did better, with the latter supporting a bounce back in the quality factor. In Australia, the ATEC technology ETF bucked global tech shakeout, delivering a 6.7% gain.

- Should an enduring peace deal in Iran be struck, this may support further weakness in commodity-related themes. The fate of technology exposures continues to wax and wane, though my expectation is that optimism in the AI trade will ultimately hold up for a good while longer.

Explore

Markets