David Bassanese

5 minutes reading time

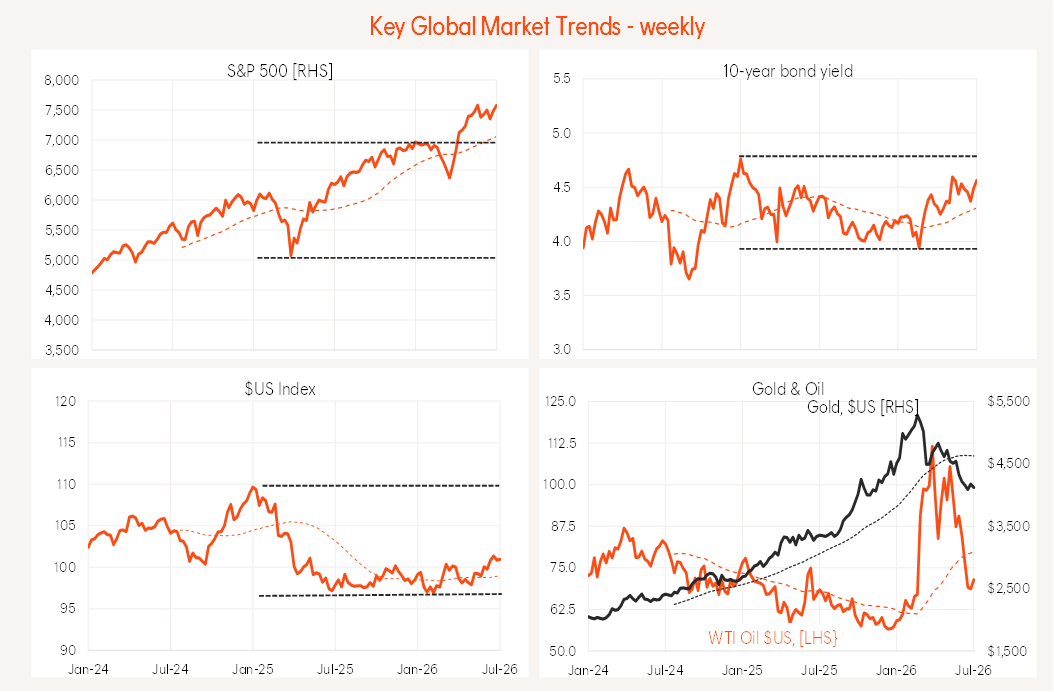

Global week in review: Peace deal falters

US equities lifted over the past week, reflecting renewed confidence in the AI trade and hopes that the latest breakdown in US-Iran negotiations won’t last long.

Source: Betashares, Bloomberg.

As regards the Iran war, last week I was encouraged by the fact that “neither side attacked the other over the past week and ship traffic through the Strait of Hormuz is gradually recovering”. We can’t say that about the past week, with a resumption of attacks by both sides and Iran declaring over the weekend that the Strait of Hormuz was again effectively closed.

What led to the breakdown? Apparently, Iran considered its recently-signed peace deal had authorised it to manage ship traffic through the Strait. Iran did not like some ships taking a new unauthorised “southern route” through the Strait, which goes through Omani territorial waters and hence is under less direct Iranian control. Iran fired on a few ships and the US then struck back.

What’s clear here is that Iran is keen to now assert ultimate control of ship traffic through the Strait of Hormuz – in agreement with Oman. And it was willing to break the peace deal to assert this right. This is the new sticking point, and the issue is whether Trump will also accede to this demand to get the war behind him and global oil supply flowing again. I suspect he probably will, but we’ll learn more this week.

In other news, optimism around AI also tentatively returned last week, with SK Hynix successfully cross-listing its shares on the NASDAQ and Samsung Electronics reporting strong earnings results. That said, Asian-based technology stocks are still enduring significant volatility following their very strong run-up over the past year. While the NASDAQ-100 returned 1.7% last week, the now tech-heavy MSCI Emerging Markets Index fell 1.9%.

Global week ahead: US CPIs

Apart from the Iran war, key global events this week include the US consumer price index and Congressional testimony by the newly installed Fed chair Kevin Warsh.

Annual growth in the core CPI is expected to hold steady at a still uncomfortably high 2.9%. What Fed chair Warsh currently thinks about this will be evident in testimony before both the House of Representatives and the Senate. His recent commentary has been mixed, affirming the Fed’s determination to get inflation down but also suggesting inflation risk had eased recently.

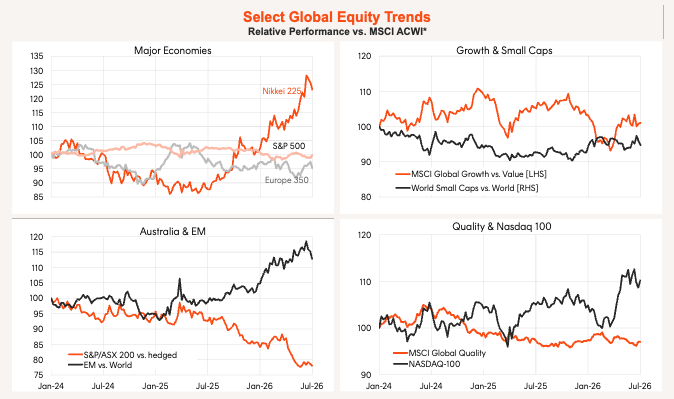

Global equity trends: Tech wobbles continue

Global equity trends are quite mixed at present, with a choppy pullback in the relative performance of global technology still seemingly underway. What is replacing this trade is less clear, with materials and energy also under pressure. So far financials, health care and global quality seem to be holding up the best.

*All but value factors. Local currency basis. Source: Betashares, Bloomberg

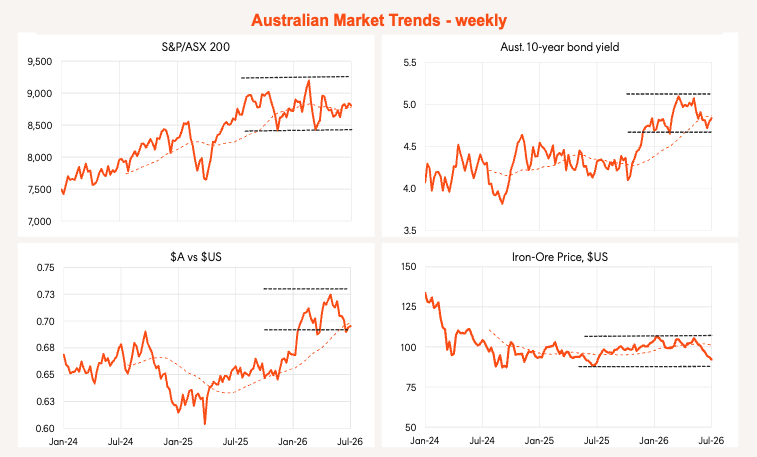

Australia week in review: Hawkish RBA

Local stocks underperformed again last week in what was a relatively quiet week on the economic data front.

Source: Betashares, Bloomberg.

The local highlight was a speech by RBA chief economist Sarah Hunter, which reaffirmed the Bank’s still generally hawkish tone.

Dr Hunter noted that the frequency of supply shocks had increased, which may make it more difficult for central banks to simply “look through” what historically had been short-run hits to both inflation and economic growth. Ominously, she warned that if supply shocks were to be considered more persistent, central banks might need to raise interest rates – even at the risk of hurting economic growth further – if there was a risk of inflation expectations becoming unanchored.

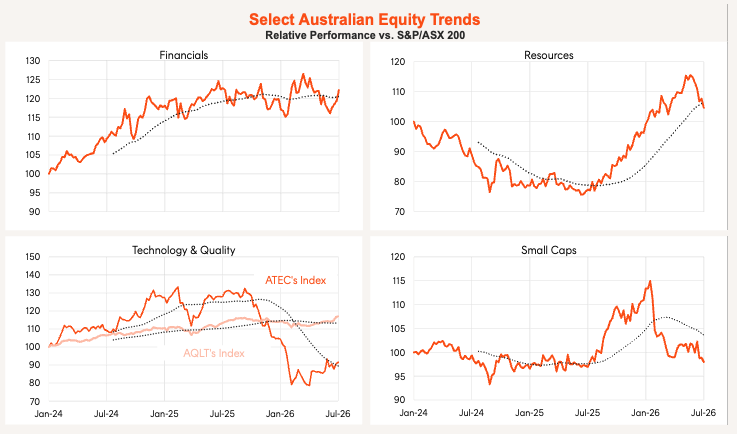

Local equity market trends: Health care & quality

As might be expected due to renewed Iran tensions, the energy sector fared best locally last week, though materials suffered a heavier pullback. Among major sectors, a bounce in the relative performance of financials compared with resources is evident over recent weeks, with health care also doing well (which is helping the quality factor). Small caps are sagging once again, though technology’s shaky relative performance recovery continues.

Source: Betashares, Bloomberg.

Australia week ahead: Business and consumer confidence

There’s little in the way of major economic data locally this week, with highlights being the National Australia Bank and Westpac surveys of business and consumer confidence, respectively. Both are likely to show a continued chilling of local economic confidence following the May Federal Budget.

Have a great week!