David Bassanese

5 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the below player:

Global week in review: AI and ceasefire wobbles

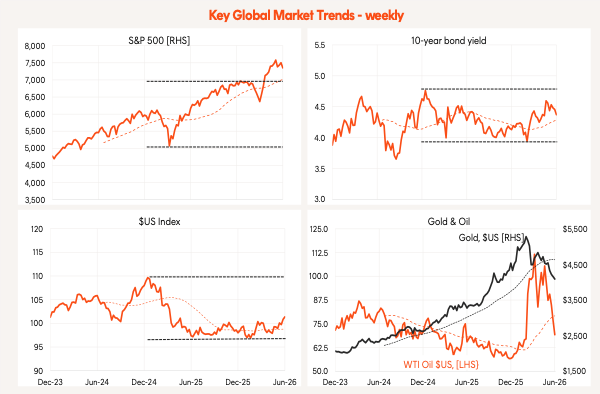

US equities dropped back last week reflecting the fragile US-Iran ceasefire and renewed concerns around technology valuations. Despite ceasefire doubts, oil prices dropped further with signs of more ships passing through the Strait of Hormuz. US bond yields also eased while the $US firmed. The gold price continued to ease.

Source: Betashares, Bloomberg.

The on-again/off-again US-Iran ceasefire deal remained a key focus of markets last week. While ship traffic through the Strait has picked up, Iran saw fit to attack one ship on Thursday and both the US and Iran launched strikes over the weekend. By this morning, however, both sides had agreed to a renewed tentative ceasefire. Despite the lingering tension, oil markets seem convinced the worst is over, with WTI oil futures down a further 9.6% last week to $US69.2 a barrel.

The other major story remains the AI trade, with technology stocks sinking again last week (which some dubbed “Chip wreck”) due to a range of concerns. For starters, reports that OpenAI might delay its IPO unnerved sentiment. Rising memory and chips costs also fanned concerns that this could crimp AI/technology demand and squeeze margins. Last but not least, sticky US inflation has investors nervous about possible US rate rises later this year.

On Friday, the May gain in the headline US private consumption deflator was a touch softer than expected (+0.4% versus +0.5% market expectation) but core prices were in line with expectations posting a 0.3% gain – which dragged up core annual inflation from 3.3% to 3.4%.

Global week ahead: US payrolls

Focus will no doubt remain on the US-Iran peace talks and AI concerns this week.

On the data front, the key highlight will be the US May payrolls report, with a moderate 114k jobs gain expected which would keep the unemployment rate steady at 4.3%.

Global equity trends: Tech pullback

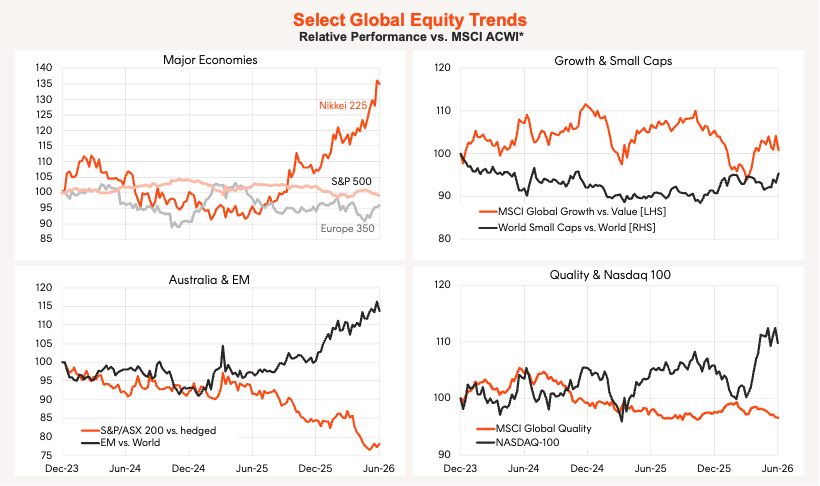

Last week’s AI jitters saw a setback in the AI trade, with the NASDAQ-100 underperforming the S&P 500. Emerging markets also took a hit, with hardware stocks across Asia – especially in South Korea – suffering a correction.

Whether this is just a correction in what has been a strong rebound in tech relative performance since early March remains to be seen.

*All but value factors. Local currency basis. Source: Betashares, Bloomberg

Australia week in review: Sticky inflation

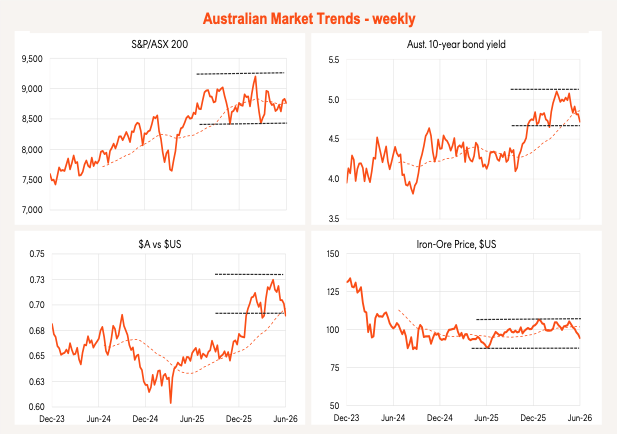

The local equity market also pulled back last week, but less so than global markets. A seemingly benign May CPI report and US rate fears combined to push the $A back below US70c.

Source: Betashares, Bloomberg.

The local highlight last week was the May CPI report. Although the headline drop in monthly prices was a bit stronger than expected, this largely reflected the fall back in petrol prices. Trimmed mean “underlying” inflation remained sticky, with a 0.4% gain resulting in annual underlying inflation of 3.4%. Housing inflation, both rents and the cost of new homes, is the main factor keeping underlying inflation high.

The irony is that recent Federal Budget changes – which encourage new home builds and reduce investor activity in the market – could add to further upward pressure on both rents and new housing costs over coming months.

The other highlight was the labour market report, with a firm 40k gain in employment during May, allowing the unemployment rate to ease from 4.5% to 4.4%. That said, revisions saw a larger decline in April employment, and looking through monthly (holiday-distorted) volatility, a modest underlying easing in labour market strength seems evident.

Fury around the recent Federal Budget tax changes is dying down, with investors now seemingly resigned to an increase in capital gains tax on share market investing and start-up businesses. Whether there’ll be any further tweaks to the tax package in the 2nd round of legislation also remains to be seen – we can only hope!

Local equity market trends: technology sags

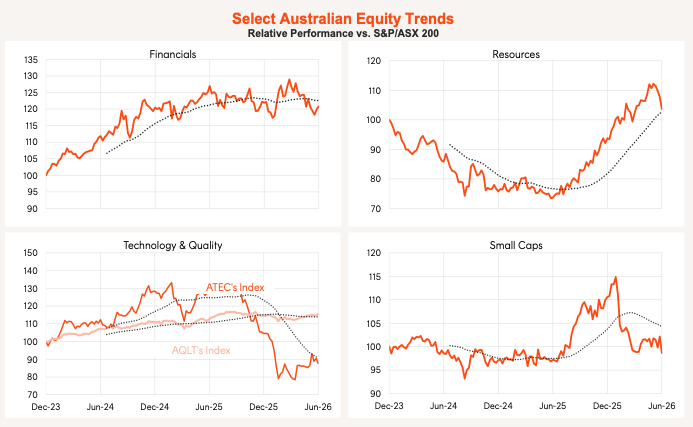

Financials outperformed last week with both resources, small caps and technology underperforming. Global AI concerns have checked the recent rebound in local technology outperformance, while the strong performance of resources has also come off the boil of late.

Source: Betashares, Bloomberg.

Australia week ahead: RBA minutes & house prices

We’ll get minutes to the recent RBA policy meeting tomorrow and June house prices on Wednesday. Despite leaving rates on hold this month, the RBA minutes are likely to confirm the Bank retains a clear tightening bias.

Based on already known daily data, Wednesday house prices news is likely to show a dip in national house prices in June, led by declines of around 1% in both Sydney and Melbourne. We should expect further house price weakness in the month ahead, with my expectation of a national decline in prices of around 7% over the coming year – and closer to 10% in both Sydney and Melbourne.

Have a great week!