When cyclical meets structural: Japan’s golden opportunity

Key points

Many regional markets are enjoying a cyclical uplift from the AI capex boom, Japan amongst them. Unlike other regions, Japan’s cyclical boost comes during a multi-year structural shift underpinned by macro reflation, corporate reform, and a pro-growth fiscal agenda. As many portfolios remain underweight and foreign flows into the region pick up, Japan stands out as a developed ex-US investment opportunity.

When cyclical meets structural

It is arguable that heading into the AI capex and future technology supercycle, Japan is one of the best placed regions to capitalise.

Having undergone decades of corporate deleveraging and underinvestment following the 1980s asset price bubble, the Japanese corporate system has been forced out of dormancy. A new, but to many familiar, corporate model prioritising shareholder returns, enforcing board independence and ownership, and requiring improved capital efficiency has seen Japanese corporates begin to think and act more like their successful US counterparts.

The easiest way to appreciate this fundamental shift is through the results to date:

– Over 70% of Prime-market firms have published or updated cost of capital and capital efficiency plans, with explicit return on equity (ROE) and payout targets becoming standard.1

– Share buybacks, a centrepiece of the US markets’ success, have risen more than sixfold over the past decade from US$27bn to US$180bn.2

– Dividends have increased by 9% p.a. since 2015.3

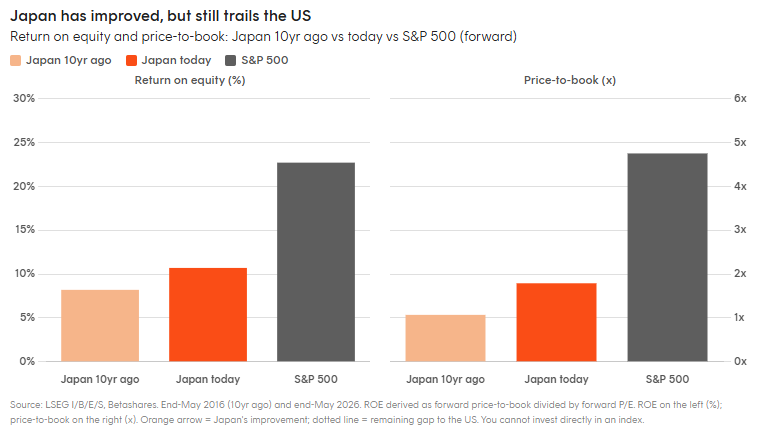

– ROE has improved from 8.2% to 10.7% over the past decade.4

The direction of travel has been encouraging, but Japan still has further to go relative to more mature markets such as the US, leaving a lot of potential still to be unlocked if the reform momentum continues.

Japan’s corporate reforms have not stood alone in the policy mix to revive the economy and capitalise on growth opportunities.

After 30 years of deflation, accommodative monetary policy has helped deliver structural reflation, rewarding cash deployment over hoarding and fostering investment and wage growth.

Meanwhile, Japan’s Prime Minister Sanae Takaichi’s overwhelming public support has come from her desire to further Japan’s economic growth and corporate profitability. Her agenda: a record fiscal stimulus, targeted state investments in strategic technologies (AI, robotics, semiconductors and space), an accelerated defence build-up, and a multi-decade industrial vision, is built around growth, economic security, strategic alliances, and national resilience.

These policies are helping to usher in the next era of investment and growth for Japan. As an example, corporate Japan is now spending to lead the AI build-out, not just to reward shareholders. SoftBank has now committed more than US$60 billion to OpenAI over the next four years to support the US$500 billion Stargate project5, while Tokyo Electron, whose tools the world’s chipmakers depend on, has lifted capital spending to a record6. Japanese mergers and acquisitions reached US$350bn in 2025, with first-half deal value alone exceeding the total for any full year from 2008 to 20237, and private-equity buyouts up around twelvefold over the prior year.6

In effect, for the first time in a generation, Japan has aligned the incentive to deploy capital (reflation), the obligation to deploy it efficiently (governance reform) and a more defined, state-supported, destination to deploy it into (Takaichi’s future-tech and economic-security agenda).

Investment implications

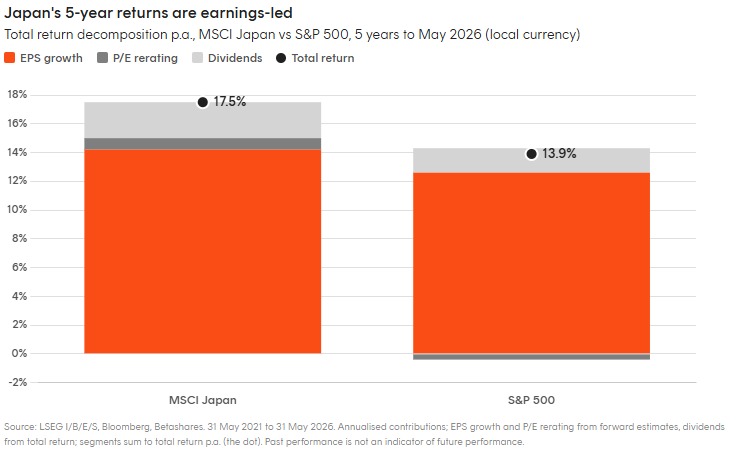

Those who have been in tune with Japan’s transformation have already been rewarded. The confluence of structural and cyclical factors has seen Japan’s equity market perform strongly in recent years with returns driven by underlying earnings growth rather than significant valuation expansion.

For the many who remain underexposed, the investment opportunity remains compelling. Japan’s revival, underpinned by shareholder returns of capital to date, is shifting towards strategic investments placing Japan at the centre of allied future technology supply chains.

In this vein, investors could consider prioritising higher exposure to the exporters, technology and financial leaders at the heart of Japan’s new investment cycle. HJPN Japan Currency Hedged ETF invests in the largest globally competitive Japanese exporters, currently holding around a quarter of the portfolio in the semiconductor and AI supply chain, well above the Topix weight9, alongside Toyota, Sony and the major banks, with the currency hedged to Australian dollars.10

A soft yen has also been part of Japan’s growth settings, supporting exporter earnings and the exit from deflation, so policymakers have little reason to reverse it, and a debt-constrained Bank of Japan has little room to do so. For Australian investors that has made currency hedging particularly valuable over recent history. Not only has it minimised the impact of the yen’s depreciation, but it has also gained from the FX hedging “carry” – the additional return generated from the interest-rate differential that has existed between Japan and Australia (which currently sits around 3.3% p.a.11

For more information on HJPN, visit the fund page here.

For investors who do not typically allocate to region specific ETFs,

EXUS

Global Shares Ex US ETF

currently holds a 25% weight to Japanese equities, its largest country allocation. EXUS was designed specifically for Australian investors offering an efficient, low-cost building block to developed markets excluding Australia and the US.

For more information on EXUS, visit the fund page here.

The information contained in this article is general information only and does not take into account any person’s financial objectives, situation or needs. Investors should consider the appropriateness of the information taking into account such factors and seek financial advice. This article is provided for information purposes only and is not a recommendation to make any investment or adopt any investment strategy.

Future results are inherently uncertain. The information above may include opinions, views, estimates, projections, assumptions and other forward-looking statements which are, by their very nature, subject to various risks and uncertainties. Actual events or results may differ materially, positively or negatively, from those reflected or contemplated in such forward-looking statements. Forward-looking statements are based on certain assumptions which may not be correct. You should therefore not place undue reliance on such statements. Betashares does not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date such statements are made or to reflect the occurrence of unanticipated events. There are risks associated with an investment in the Funds HJPN, including market risk, country risk (in the case of HJPN) and international investment risk, medium sized companies risk and currency risk (in the case of EXUS). Investment value can go up and down. An investment in the Funds should only be considered as a part of a broader portfolio, taking into account your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Funds, please see the relevant Product Disclosure Statement and Target Market Determination, both available on this website.

1. Tokyo Stock Exchange data, as at March 2025.

2. Japan Exchange Group data, as at December 2024.

3. Refinitiv Datastream, as at December 2024.

4. Refinitiv Datastream, as at December 2024.

5. SoftBank Group press release, as at January 2025.

6. Tokyo Electron investor relations, as at March 2025.

7. Refinitiv, as at December 2025.

8. Bain & Company, Global Private Equity Report 2026.

9. Based on HJPN portfolio holdings, as at May 2026. Topix weight refers to the Tokyo Stock Price Index sector weighting.

10. Currency hedging removes exposure to movements in the Japanese yen relative to the Australian dollar.

11. Based on the interest rate differential between Japan and Australia, as at May 2026.