Annabelle Dickson

Dollar cost averaging is a simple investing strategy that assists in mitigating market timing risk and can help you gradually accumulate wealth. Like all investing strategies, dollar cost averaging does not guarantee profit, but over time, can help in reducing the effect of market fluctuations.

Summary

- Similar to a regular savings plan, dollar cost averaging involves investing the same amount of money at set intervals over a long period – whether market prices are up or down

- Dollar cost averaging can be useful in helping investors to focus on their long-term investment goals by avoiding trying to time the markets

- If you’re a member of a superannuation fund you’re already practising dollar cost averaging indirectly via the regular concessional contributions being made by your employer

How does dollar-cost averaging work?

Dollar cost averaging involves investing the same amount of money at regular intervals, for example monthly or quarterly – without regard to market movements. Investing a fixed dollar amount means that when prices are higher, your money buys fewer shares/ETF units, and when prices are lower, your money buys more.

The theory behind this strategy is that you reduce market timing risk – instead of investing your entire allocated amount in one lump sum, you can spread your investment out over a period of time. Depending on market movements, spreading out your entry points potentially can achieve a lower average cost base.

Realistically, almost all Australians practise dollar cost averaging via their superannuation. For most of us, a percentage of our salary automatically gets sent to our superannuation account of choice, and is then invested into ETFs, managed funds, direct stocks etc. This is a prime example of dollar cost averaging – consistent, regular amounts being invested regardless of how markets are performing.

Does dollar-cost averaging really work?

As a general rule, when compared to investing all your funds at the outset, dollar cost averaging is most effective when markets subsequently fall. As prices decrease, your regular ‘instalment’ buys you a greater number of shares/ETF units.

In a rising, or bull market environment, a dollar cost averaging strategy is not as effective as if you had tipped all your funds in at the start. Obviously, the lump sum investment would be optimal if you managed to time your purchase on the day when the price was lowest – but how does one know exactly when that day is? None of us has a crystal ball.

Some investors might use dollar cost averaging because their personal view is that the market is set for a pullback. They may be concerned that market valuations are high and worried about putting all their money in at the very top.

However, the point of dollar cost averaging is not to try and pick whether the market is going to rise or fall – rather, it is to take the timing question out of the equation.

If that is the case, then dollar-cost averaging provides a straightforward strategy for investors to gradually deploy their equity, without being overly concerned about market volatility.

Benefits of dollar-cost averaging

If you don’t have a large single sum to invest or like the discipline of investing small amounts regularly, then dollar-cost averaging can assist in mitigating market timing risk and can help you gradually accumulate wealth.

When prices are up, your fixed dollar amount will buy fewer units or shares. When they are down, your regular investment will buy more. The point of dollar cost averaging is not to try and pick whether markets are going to rise or fall but rather to remove the concept of speculating from the equation.

Example of dollar-cost averaging

Let’s look at a simple example.*

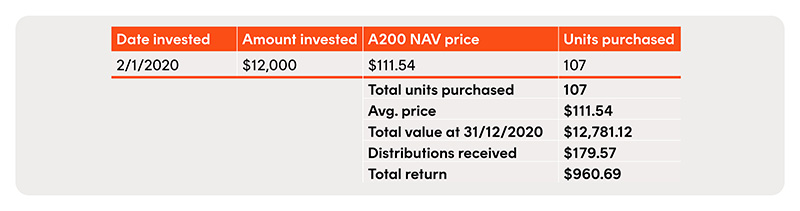

Take a low cost, index tracking fund, like the A200 Australia 200 ETF.

Let’s pretend it’s the beginning of 2020, and at the end of 2019, you made a New Year’s resolution to start investing in the sharemarket.

You check your bank account, and you have $12,000 to invest. Looking back over the year you notice the Australian market was up over 23% and has been trending higher for the last few years.

You’re worried that as markets approach all-time highs, you might be getting in at the top.

Rather than trying to pick ‘the best time to invest’, let’s assume you started dollar cost averaging from the first investible day of the year and made the same, equal investment, each month after that.

Contrast that with the result you would have achieved had you invested the entire $12,000 in A200 units at the start of the year.

* Example does not account for any transaction costs, such as brokerage. Past performance is not an indicator of future performance.

In this situation, a dollar cost averaging strategy would have produced a better result, with more units purchased, at a lower average cost base. More importantly, it avoided the risk of putting all your eggs in one basket in terms of timing.

Implementing dollar-cost averaging

Betashares Direct’s Auto-invest can help you to put a dollar cost averaging strategy in place. Auto-invest allows you to set recurring investments into up to five Betashares ETFs brokerage-free, making it simple to automate a DCA strategy.

You can also set up a recurring transfer from your bank account to your Wallet to ensure sufficient funds for Auto-invest transactions.

You retain control over your investments. You can pause, adjust or stop contributions at any time, making it easy to tailor your investment routine as needed. Auto-invest also provides clear tracking, so you can monitor your investment’s performance.

Automate your investing

with Auto-invest