Reading time: 3 minutes

The adoption of the cloud is arguably one of the most significant business transformations we have seen since the early days of the world wide web.

Given ongoing growth in online activity, and the sizable share of the world’s digital data and software applications still maintained outside of the cloud, continued strong growth in cloud-related services has been forecast.

This week’s launch of CLDD Cloud Computing ETF , the first ETF traded on the ASX to focus on the cloud computing market, represents an exciting opportunity to benefit from the cloud computing megatrend, and what it means for global commerce in a post-pandemic world.

What is cloud computing?

Cloud computing is the technology driving the outsourcing of digital data storage and online software accessibility, freeing corporate and household consumers from these traditionally cumbersome tasks.

In the early days of computing, both digital data and software applications typically were stored and maintained by the end user either by buying and downloading software or by accepting software pre-bundled into the devices they purchased. The game has changed, and cloud computing represents a foray into a truly digital age.

Think Netflix, Salesforce, Zoom

The rise of ‘as a service’ businesses has revolutionised the way consumers interact with businesses and turned ‘boring’ software development companies into household names.

Software businesses such as Netflix, Salesforce and Zoom have captured the imagination of investors over the last few years, whilst cloud infrastructure services like Amazon and Microsoft have successfully diversified their businesses into the cloud ecosystem.

These companies command attention by operating business models of the future, innovating and using technology that seek to revolutionise the way we interact and do business.

Revenues for the cloud ecosystem currently top US$371 billion, and are forecast to reach US$832 billion by 20251 – presenting an exciting investment opportunity, given the rapid growth in the sector since 2010, when over 90% of data was held only on local servers2.

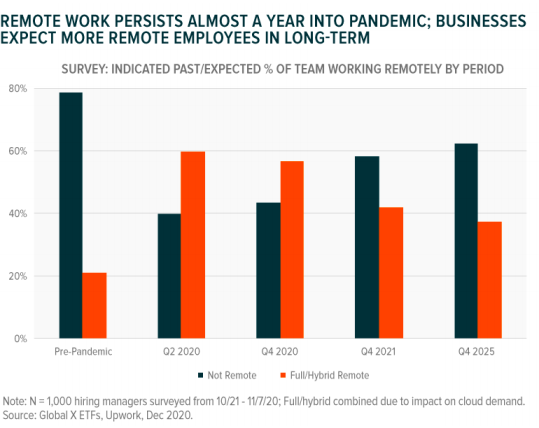

Cloud computing has enabled 2020’s successful work-from-home experiment

Demand for cloud computing services has grown strongly because of the added flexibility and cost savings the technology offers.

Through the cloud, at-home employees can virtually access their regular suite of applications and files and collaborate with their colleagues. It is likely that enterprises will further embrace cloud-based Software as a Service (SAAS), with many employees still working remotely and organisations embracing remote work as part of the new normal. As the chart below shows, the number of employees working from home is likely to stay elevated from pre-pandemic levels.

Subscription-based IT opens the door for large scalability

For the companies involved in the provision of cloud computing services, their initial concepts have developed into an appealing business model.

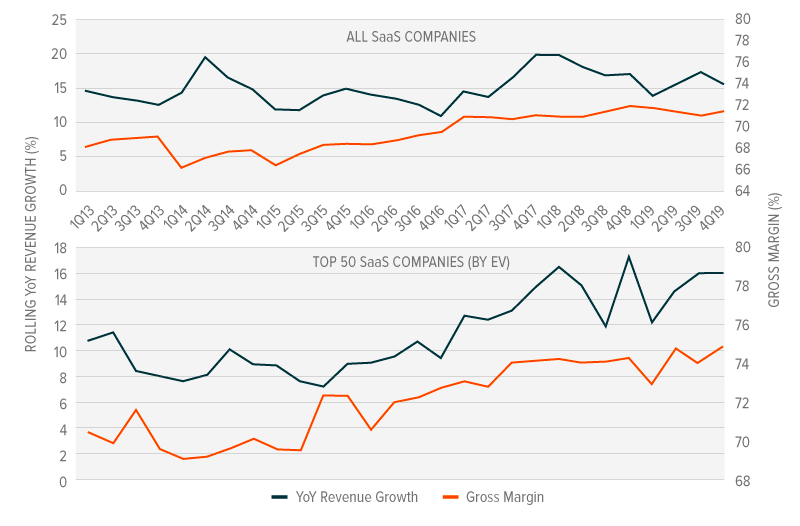

Subscription fees generate recurring, relatively sticky, and projectable cash flow. Once companies integrate software into their processes and their employees become accustomed to it, replacing the provider becomes difficult – even if fees are increased. The ingrained nature of this relationship creates direct-to-consumer marketing channels through which they can upsell product, further driving potential revenues3. Furthermore, centralised data storage facilities and software applications naturally lend themselves to strong scale economies – whereby the costs per unit of service fall as the number of customers grow.

As the chart below shows, SaaS companies have been delivering strong YoY revenue growth, but more strikingly, large gross margin performance – which allows key players to remain dominant whilst delivering strong shareholder returns.

SaaS companies revenues have grown in the double digits, margins have expanded

Source: Bloomberg, Global X ETFs, March 27, 2020. Past performance is not indicative of future performance.

Thematic trade allows for industry-specific exposure

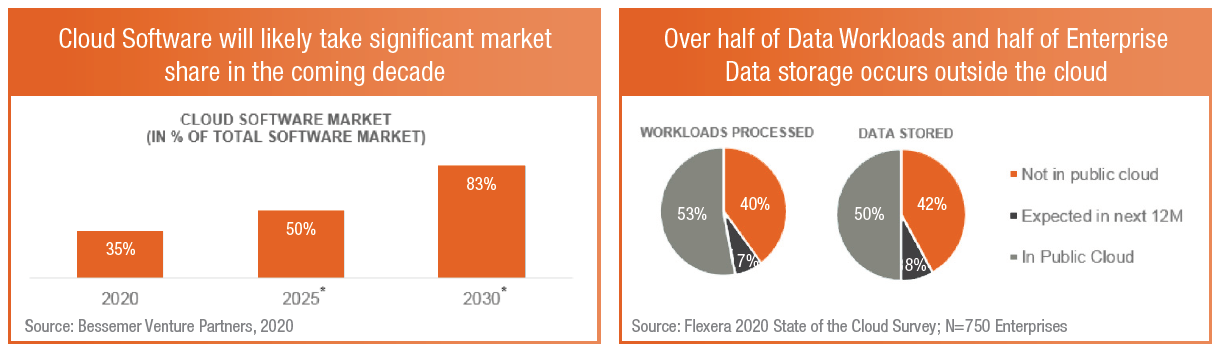

The cloud market potentially benefits from numerous tailwinds, which are generating attractive return prospects vs. the wider technology ecosystem. Indeed, the widespread adoption of 5G represents an opportunity for cloud businesses to store and manage the abundance of data that the 5G network will create. Meanwhile, cloud components can be used in network infrastructure and artificial intelligence as edge computing takes off4.

Technology surveys suggest that around half of enterprise data processing and storage was conducted outside of cloud facilities last year, and cloud-based software still accounted for only 35% of the total software market – this is projected to increase to 83% by 20305.

Note: Actual outcomes may differ materially from forecasts.

Combined with the step change in the market due to COVID-19, this sector has the potential to generate good returns compared to the wider technology market. As the table below shows, 12-month forward revenue (as represented by the index CLDD aims to track) is projected to outstrip more diversified indexes, and could represent an exciting opportunity to participate in a longer-term growth story. 12-month forward earnings per share growth also looks attractive when compared to broad based technology as well as the global market, supporting the case for investment.

| CLDD’s index | NDX 100 | S&P 500 | MSCI World | |

| 12-month forward EPS growth | 26.0% | 13.5% | 15.5% | 6.0% |

| 12-month forward revenue growth | 15.6% | 8.8% | 6.2% | 4.3% |

Source: Bloomberg. As at 18 February 2021. Actual outcomes may differ materially from forecasts.

How can investors gain exposure to cloud computing?

Investors seeking to gain exposure to cloud computing can consider CLDD Cloud Computing ETF .

CLDD is the first ETF traded on the ASX to focus on the cloud computing market, providing convenient, cost-effective access to a diversified portfolio of leading companies in the global cloud computing industry.

The Index that CLDD aims to track currently comprises 36 leading cloud computing businesses, all of which derive significant revenue from the cloud ecosystem.

To be eligible for inclusion in CLDD’s index, a company’s share of revenue from cloud computing services must meet a minimum threshold. The index that CLDD aims to track is constructed so that it prioritises companies that generate the majority of their revenues from cloud-based services, making CLDD a more ‘pure play’ exposure.

Major holdings currently include Xero, Shopify, Dropbox, Fastly and Netflix. Diversified technology staples such as Amazon and Microsoft also make up a part of the portfolio, given the sheer size of the cloud associated revenue they generate.

From inception in 2013 to 31 January 2021, CLDD’s index returned 33.3% p.a. compared with 11.5% p.a. for the MSCI World Index. CLDD’s index has also outperformed the more technology-focused NASDAQ-100 Index, which delivered returns of 24.1% p.a. over this period6.

| There are risks associated with an investment in CLDD, including market risk, technology sector risk, international investment risk and concentration risk. CLDD’s returns can be expected to be more volatile (i.e. vary up and down) than a broad global shares exposure, given its concentrated sector exposure. CLDD should only be considered as a component of a diversified portfolio. For more information on risks and other features of the Fund, please see the Product Disclosure Statement. |

The Fund is not sponsored, endorsed, sold or promoted by Indxx, LLC (Indxx), the index provider. Indxx makes no representation or warranty, express or implied, to the owners of the Fund or any member of the public regarding the advisability of investing in securities generally or in the Fund particularly. Indxx has no obligation to take the needs of the Responsible Entity or the unitholders of the Fund into consideration in determining, composing or calculating the Underlying Index. Indxx is not responsible for and has not participated in the determination of the timing, amount or pricing of the Fund units to be issued or in the determination or calculation of the equation by which the Fund units are to be converted into cash. Indxx has no obligation or liability in connection with the administration, marketing or trading of the Fund.

1. Source: Research and Markets, “Cloud Computing Market by Service Model (Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS)), Deployment Model (Public and Private), Organization Size, Vertical, and Region – Global Forecast to 2025”, August, 2020. Actual outcomes may differ materially from forecasts.

2. https://www.globalxetfs.com/a-decade-of-change-how-tech-evolved-in-the-2010s-and-whats-in-store-for-the-2020s/

3. https://www.globalxetfs.com/mapping-the-cloud-a-look-at-the-segments-driving-growth/

4. https://www.networkworld.com/article/3224893/what-is-edge-computing-and-how-it-s-changing-the-network.html; https://www.globalxetfs.com/a-decade-of-change-how-tech-evolved-in-the-2010s-and-whats-in-store-for-the-2020s/

5. Bessemer Venture Partners, 2020

6. Source: BetaShares, Bloomberg. Past performance is not an indicator of future performance of the Index or CLDD. Does not take into account CLDD’s fees and costs. You cannot invest directly in an index.

Written by

Blair Modica