All in on AI? 3 ways to reduce concentration risk

David Bassanese

4 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Week in review

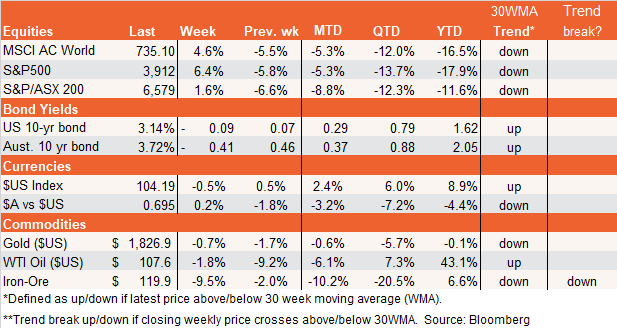

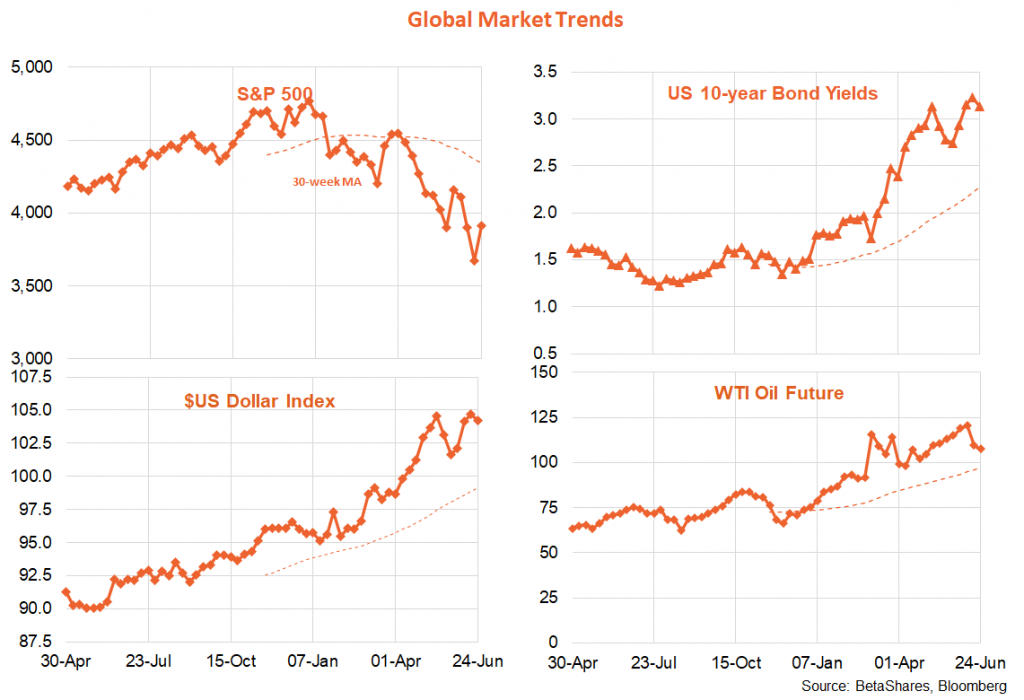

A feisty 6.4% rebound in the S&P 500 was the major market highlight of the past week, supported by declining bond yields and commodity prices.

With aggressive interest rate hikes slowly but surely starting to take the edge off global growth, equity investors are unsure whether to laugh or cry. Last week, they were trying to find comfort in the hope that slowing growth may mean central banks need not be too aggressive and a hard landing can be avoided. Signs of softening in some US growth indicators, along with some tempering in consumer and financial market inflation expectations are helping in this regard. Oil and iron-ore prices have dropped over 10% in the past two weeks, and the expected peak in US and Australian policy rates has been revised down somewhat.

Whether global markets can seamlessly transition from recent stagflationary concerns (where both bond and equity values are falling) to a positive disinflationary story (where both bond and equity values can rise) remains to be seen. Assuming inflation numbers over coming months remain uncomfortably high, we’re likely to either stay in a stagflationary environment or transition to a negative disinflationary one (where bond values rally on recession risks, but equities weaken due to a poorer earnings outlook).

That said, it all depends on how quickly wage and price inflationary pressures ease as growth slows. One possibility Fed chair Powell has discussed is that just as strong demand hitting inelastic supply has caused a sharp spike in many prices over the past year, prices could drop equally sharply as that strong demand pressure eventually subsides (and without necessarily hurting output). Last week I produced a detailed analysis of the US inflation outlook.

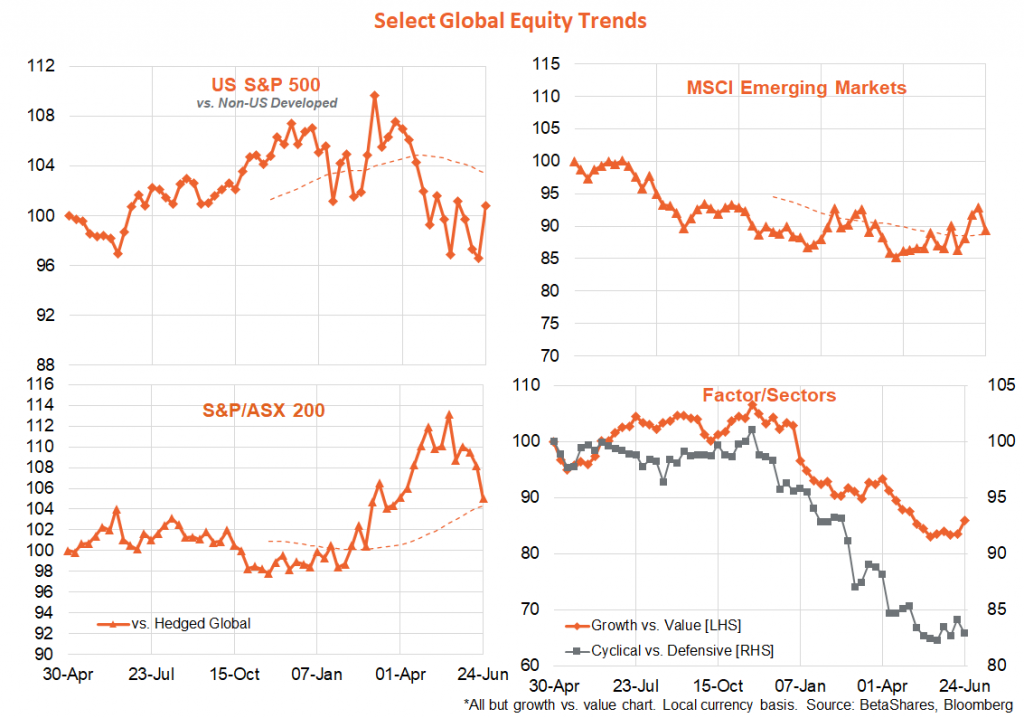

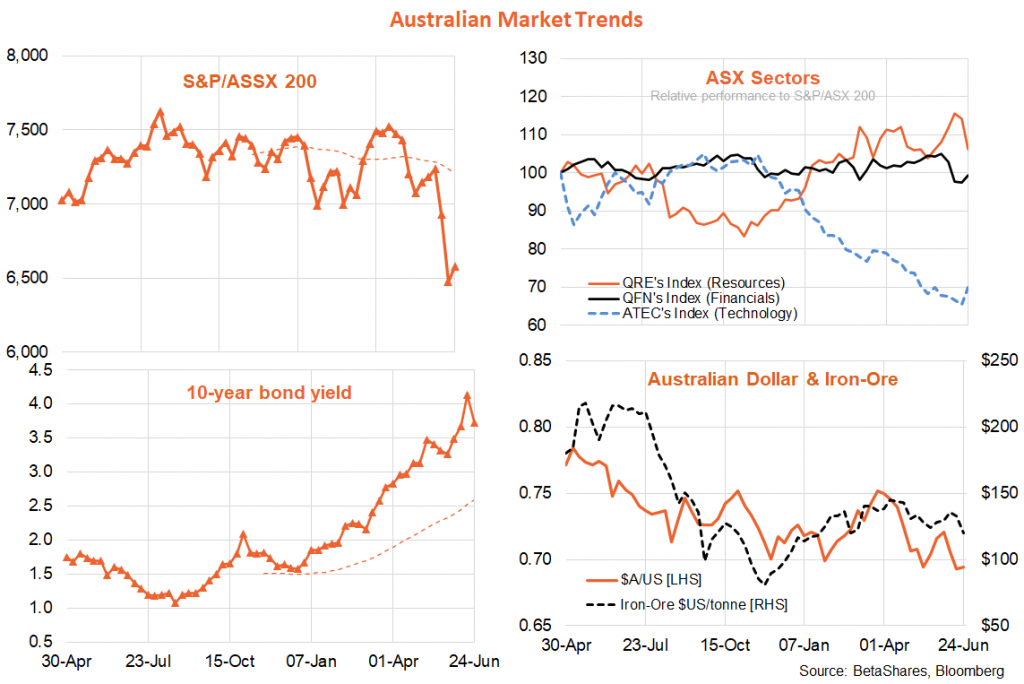

As would be expected given an easing in bond yields, growth sectors generally beat value sectors over the week, with the NASDAQ-100 up a stunning 7.5%. Weakness in energy and material stocks constrained the rise in the S&P/ASX 200 to 1.6%, though the local market was up this morning a further 1.4% reflecting Wall Street’s strong gain on Friday.

The local highlights last week were a speech by RBA Governor Phil Lowe and minutes to the recent policy meeting in which the cash rate was hiked by 0.5%. Neither, sadly, shed much light on whether the RBA will hike by another 0.5% next week. As it stands, the market attaches an 80% probability to a 0.5% hike next week – and barring a well-sourced media leak to the contrary, that remains the more likely outcome. As regards the Fed, the market still sees a 0.75% rate hike next month as a 90% probability!

Week ahead

We get a smattering of real activity data in the US this week, covering durable goods orders, consumer confidence and surveys of manufacturing and services. As regards activity data, we’re probably now in the period where “bad news is good news” i.e. early signs of economic slowing (which don’t yet spark recession fears) ease rate hike fears and cause equities to rally.

Of even more importance, we get an updated US private consumption deflator report on Thursday, with annual growth in core prices (i.e. excluding food and energy) expected to ease only modestly from 4.9% to 4.8%. Such is the market’s sensitivity to inflation, any larger or smaller than expected result could have a notable market impact.

In Australia, highlights this week include May retail sales on Wednesday and June’s Core-Logic estimate of house prices on Friday. After recent strong growth, retail spending is likely to slow but remain firm, while we’re also likely to see the second successive monthly decline in national house prices following their peak in April.

Have a great week!