David Bassanese

Betashares Chief Economist David is responsible for developing economic insights and portfolio construction strategies for adviser and retail clients. He was previously an economic columnist for The Australian Financial Review and spent several years as a senior economist and interest rate strategist at Bankers Trust and Macquarie Bank. David also held roles at the Commonwealth Treasury and Organisation for Economic Co-operation and Development (OECD) in Paris, France.

4 minutes reading time

US technology stocks have corrected somewhat in recent weeks as concerns mount over possible overvaluation in the sector. This note suggests, however, that the strong performance of the NASDAQ-100 Index in recent times has continued to reflect solid underlying earnings growth, and that valuations remain far from stretched.

Nasdaq stumbles

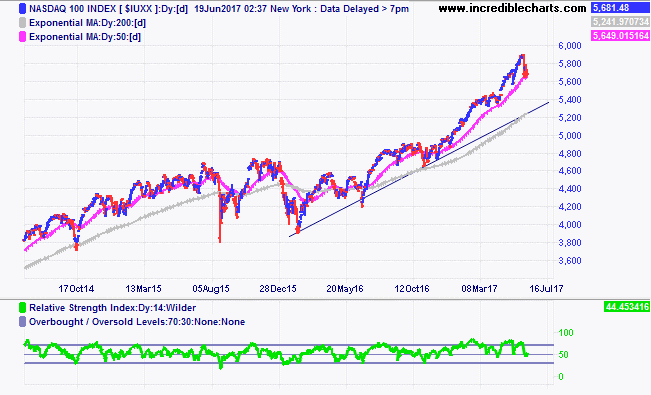

As seen in the chart below, the NASDAQ-100 Index has corrected back in recent weeks after posting strong gains since the election of US President Donald Trump late last year. The apparent catalysts for the latest move were concerns by some analysts that valuations were getting rich and that US market gains seemed increasingly narrowly based around the tech giants such as Apple, Alphabet (previously Google), Amazon and Facebook.

Past performance is not an indicator of future performance

That said, from a purely technical perspective, a pull back in the market in any case seemed overdue. As evident in the chart above, even with the solid uptrend in this Index in recent years, pullbacks are common once short-run overbought conditions emerge (technically, for example, when the RSI index hits 70 or more) – as has also become evident in recent weeks. So far at least, prices have only dropped to their 50-day moving average, and volatility in the Index suggests prices could drop somewhat more – potentially back to the 200-day moving average – before the correction is complete.

Valuations still not overly stretched

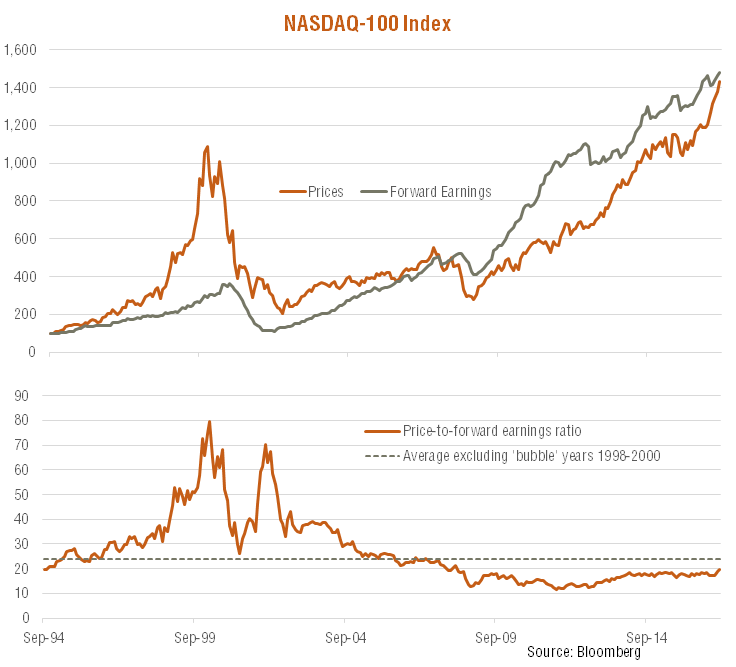

Back in June 2015, I assessed valuations for the Nasdaq-100 Index as it surpassed previous record highs. At the time, I concluded that despite the market’s solid gains since the financial crisis, “valuations do not appear stretched”, as due to ongoing solid growth in underlying earnings, the NASDAQ-100’s price-to-forward earnings ratio was still a little below its longer-run average.

Fast forward two years, and the picture remains similar. Indeed, despite the Index’s solid gains in recent years, this has been largely matched by growth in forward earnings – such that the forward PE ratio up until this year had barely changed. In 2017, so far, however, price gains have exceeded gains in earnings – such that the forward PE ratio has increased from around 18 to 20 by end-May. Note, however, that this remains below the market’s long-run average (since the mid-1990s) of 27.4. Even stripping out the “bubble” years of inflated PE valuations between 1998 to 2000, the average PE drops to 24 over this period. In other words, even today, the NASDAQ-100’s PE valuation is below its long-run average, despite the still historically low level of bond yields.

Note: relative to long-run average levels, moreover, the S&P 500 Index is more expensively priced than the NASDAQ-100 – at end-May, the S&P 500’s forward PE ratio was 17.7, compared with an average since the mid-1990s of 16.2.

If you can’t beat’em…

Particularly in the case of Australian investors, having some exposure to the world’s leading tech companies – as the NASDAQ-100 Index provides – can help provide useful diversification within one’s investment portfolio. After all, the Australian market’s weighting to technology shares is very low (less than 2% market capitalisation), and leading US tech companies such as Apple, Alphabet, Facebook and Amazon are continuing to wreak havoc across Australia’s consumer sector – from media to retail.

Indeed, Amazon’s recent $US13.7 billion purchase of US grocery chain Whole Foods saw the share prices of leading local grocery chains such as Woolworths, Wesfarmers (owner of Coles) and Metcash (owner of IGA) sold down. Whether or not Amazon is capable of successfully winning market share in the already fiercely contested local grocery sector remains to be seen – but either way, the intensification of competition could place further downward pressure on profit margins within the sector.

NASDAQ-100 now available on ASX

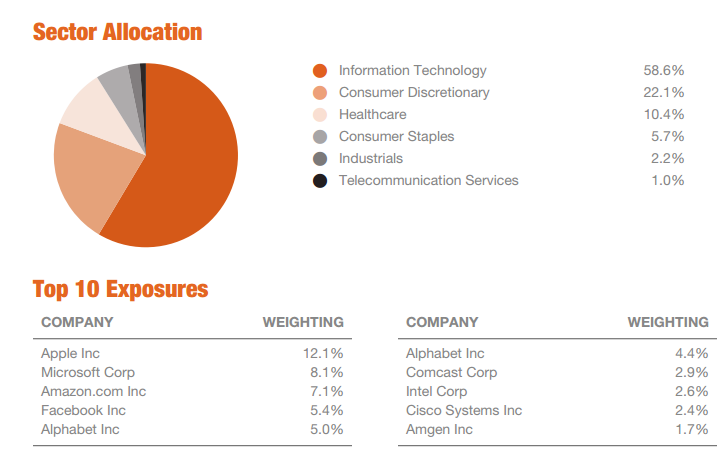

Australian investors now have simple access to the NASDAQ-100 Index via NDQ Nasdaq 100 ETF NDQ aims to track the NASDAQ 100 Index before fees and expenses and can be bought and sold like any share on the ASX. All up, NDQ gives investors access to the fast-growing technology sector without having to buy ETFs on exchanges outside of Australia. As seen below, the Index has a strong weighting to leading tech stocks such as Apple, Microsoft, Amazon, Facebook and Alphabet.

NASDAQ-100 Index: Sector Composition and Top 10 Company Exposures as at 31 May 2017

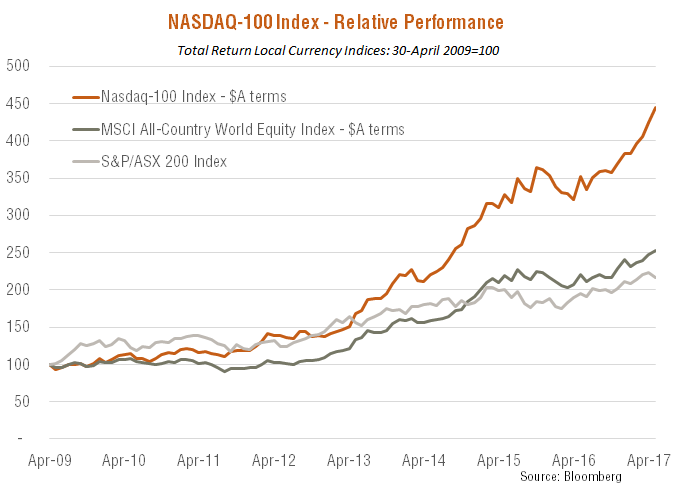

As seen in the chart below, the Index that NDQ aims to track has strongly outperformed the local S&P/ASX 200 Index and the currency unhedged World MSCI Equity Index since the global financial crisis to end May 2017.

Past performance is not an indicator of future performance. Graph shows performance of the index which NDQ aims to track, and does not take into account ETF fees and expenses. It is not possible to invest directly in an Index.

Nasdaq®, OMX®, Nasdaq-100®, and Nasdaq-100 Index®, are registered trademarks of The NASDAQ OMX Group, Inc. (which with its affiliates is referred to as the “Corporations”) and are licensed for use by BetaShares. The Fund has not been passed on by the Corporations as to its legality or suitability. The Fund is not issued, endorsed, sold, or promoted by the Corporations. The Corporations make no warranties and bear no liability with respect to the Fund.

David is responsible for developing economic insights and portfolio construction strategies for adviser and retail clients. He was previously an economic columnist for The Australian Financial Review and spent several years as a senior economist and interest rate strategist at Bankers Trust and Macquarie Bank. David also held roles at the Commonwealth Treasury and Organisation for Economic Co-operation and Development (OECD) in Paris, France.

Read more from David.