Southern route

David Bassanese

5 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

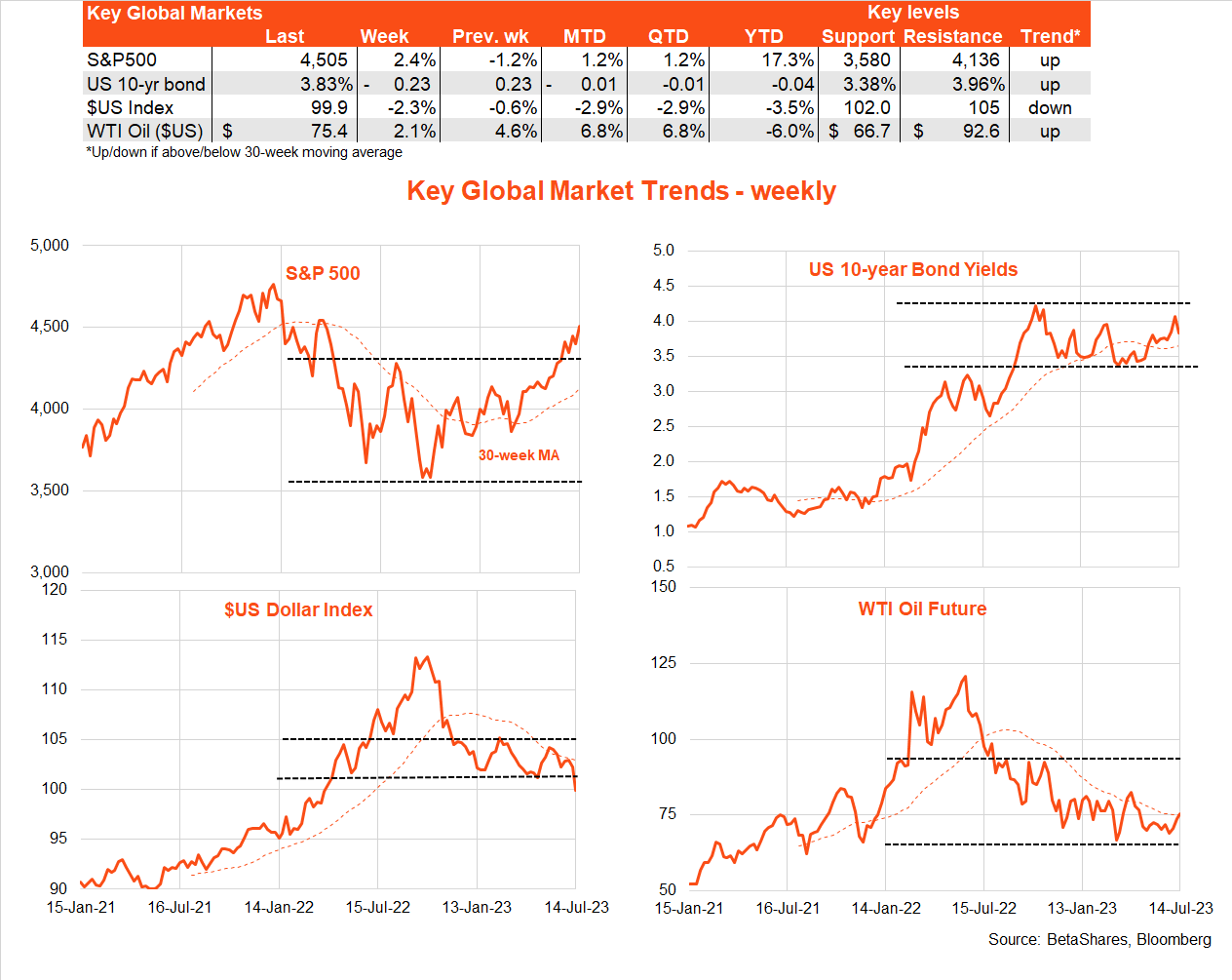

Global markets

The key development over the past week was the weaker-than-expected US CPI result, which has reduced the risk of further aggressive Fed action that ultimately pushes the economy into recession. According to Fed comments, it still seems likely the Fed will hike at next month’s policy meeting, though further rate hikes after that are now questionable provided inflation continues to ease. Most encouraging was an easing in core service sector inflation.

Of course, the US labour market remains tight and wage inflation uncomfortably high – suggesting the Fed might still require a period of below-trend economic growth (rising unemployment) to be sure inflation gets back to target. But with tentative signs of an easing in wage growth, the need for a hard landing is no longer as evident as it seemed only a few months ago. Indeed, there’s growing evidence that the lingering excess US labour demand gap is being met by an improved labour supply response (higher immigration and workforce participation) and some scaling back in corporate America’s hiring ambitions.

Likely encouraging Q2 earnings results and a likely solid US retail sales report are the key US events this week.

Elsewhere around the world, the Bank of Canada still saw fit to lift rates 0.25% last week, though the RBNZ left rates on hold. A key update on NZ inflation will be out this week. In China, lower-than-expected inflation data is instead giving rise to deflation scares amid a sluggish economic recovery. Chinese Q2 GDP is out today. UK CPI data will also reveal just how problematic inflation remains and whether the BOE needs to hike rates further even in the face of a weakening economy.

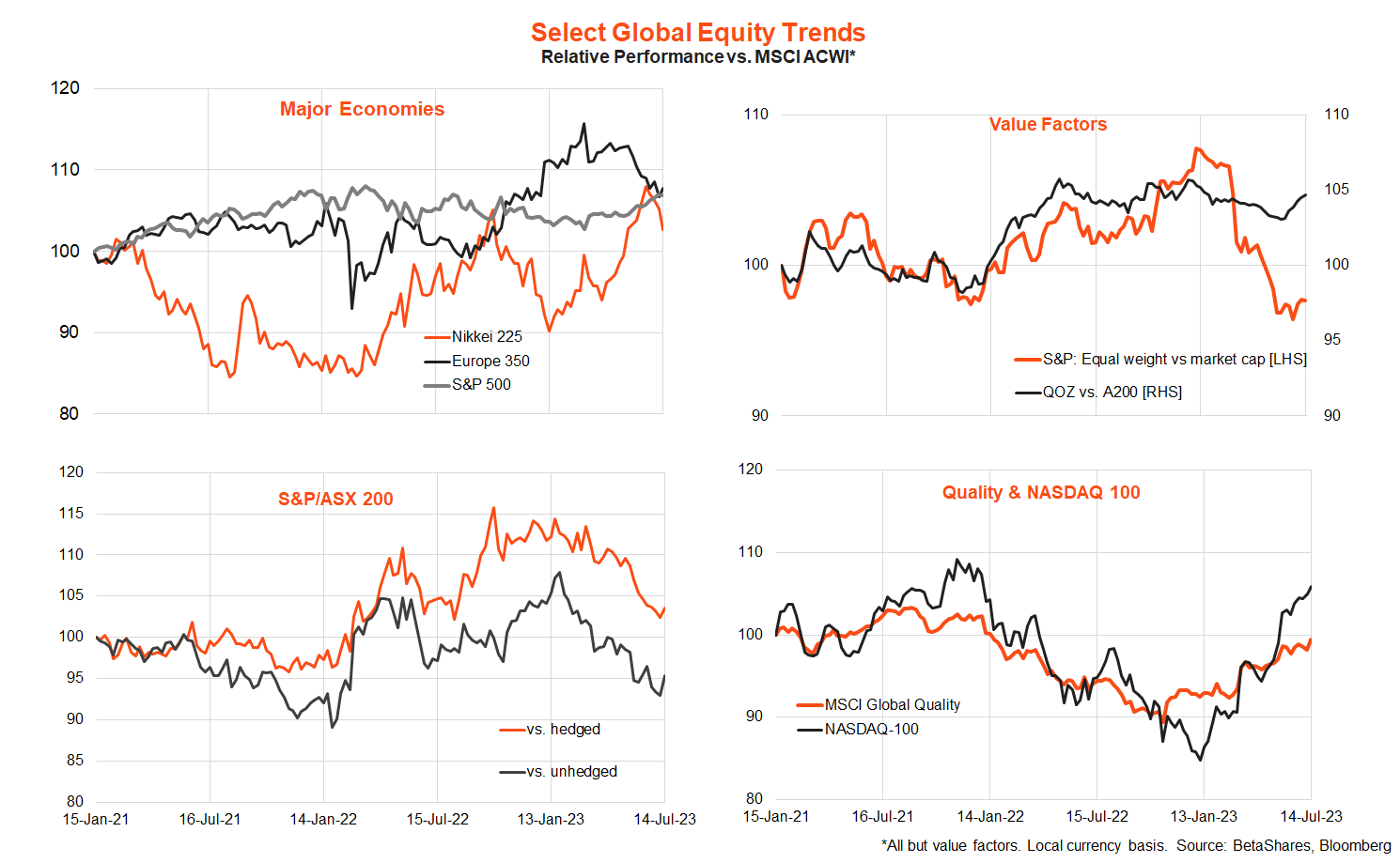

While soft landing hopes have so far favoured growth/technology/quality exposures, there is some evidence of a broadening in the equity recovery in recent weeks.

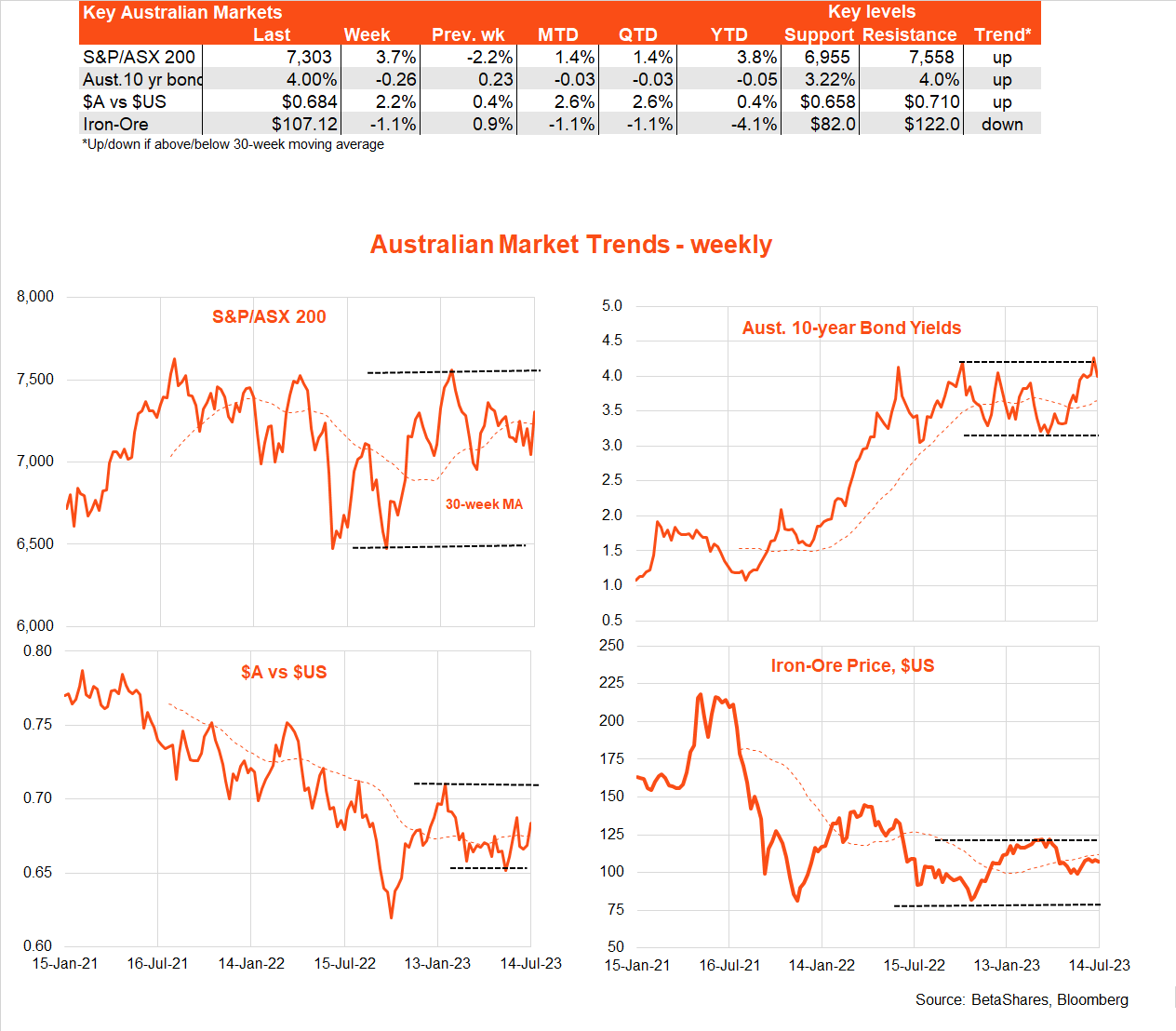

Australian market

There was mixed local economic data last week, with a bounce in consumer sentiment (albeit from low levels) and a steady NAB index of business conditions (which remain at above-average levels). One wrinkle in the NAB business survey was a modest rebound in wage and price pressures, which will likely keep the RBA on edge.

But the biggest news was the announcement of the new RBA Governor Michele Bullock and confirmation that new arrangements with regard to RBA meetings will begin next year. Being a long-established insider, the elevation of Bullock to the job suggests only incremental change at best to how the RBA thinks and acts. The biggest risk factor remains how having a new batch of ‘monetary experts’ on the Board will affect decisions over time.

Key highlights this week include minutes of the July RBA policy meeting (at which rates were left on hold) and Thursday’s labour market report. Insights from both will have a key bearing on whether the RBA raises rates next month.

Have a great week!

| Top events of the past week | Comment |

| Low US CPI and PPI | Both the headline and core June CPI results were a touch better than expected. Importantly, there are signs of an easing in long-sticky core service sector prices. Wholesale producer prices (PPI) were also softer than expected. US inflation remains too high but is moving in the right direction. |

| Soft Chinese inflation | By contrast, Chinese consumer and producer prices were softer than expected, with deflationary pressures and a sluggish economic recovery seen as bigger concerns than inflation. |

| Change at the RBA | RBA Deputy Governor Michele Bullock was named as the next RBA Governor, beginning in September. Following the RBA Review, Governor Lowe confirmed from 2024 there will be only eight policy meetings per year and a press conference after each. |

| Key events to watch this week | Comment |

| US earnings | The Q2 earnings season ramps up, with key reports from Tesla, Goldman Sachs, and Netflix. Overall earnings are expected to be down on the year, though there is a risk of upside surprises. |

| China GDP | Only 0.5% GDP growth is expected for Q2 after a solid 2.2% Q1 bounce following the easing of COVID restrictions. Such a result would confirm that China’s post-COVID recovery is faltering. |

| NZ Q2 CPI | The Q2 CPI is likely to reveal an easing in annual inflation from 6.7% to a (still high) 5.9%. Signs of sticky core inflation would raise the risk of an RBNZ rate hike next month. |

| RBA minutes | Minutes of the June meeting – at which the RBA left rates on hold – may reveal just how finely balanced the decision was, and hence influence thinking on the odds of a rate hike next month. |

| Australian employment | A modest 17k June gain in employment is expected after last month’s blockbuster 76k gain. The unemployment rate is expected to remain steady at 3.6%. |

Explore

Bassanese Bites