India: The market's hidden giant

David Bassanese

5 minutes reading time

- Global shares

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

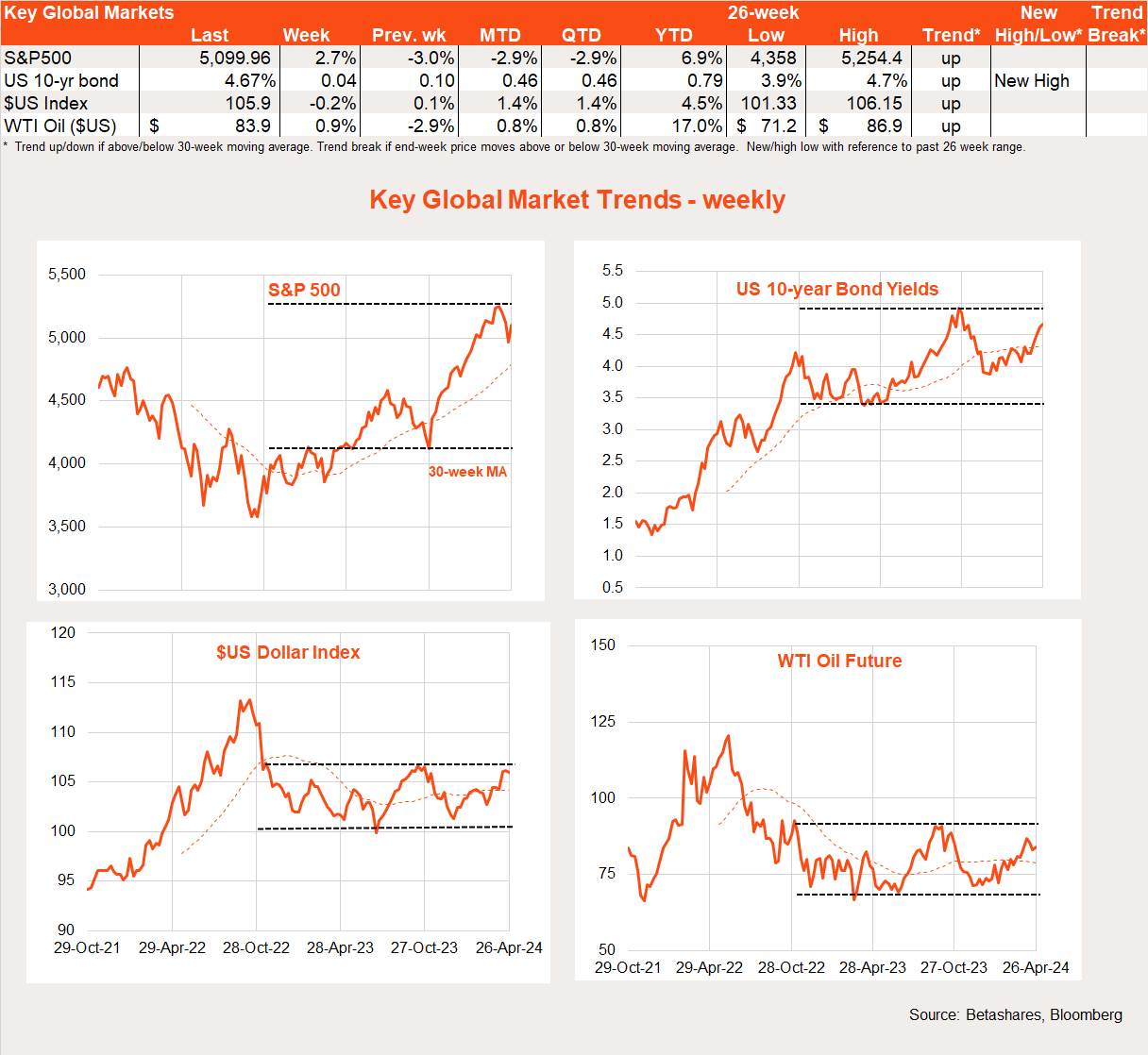

Global markets – week in review

Global equity markets rebounded last week after a few weeks of losses, thanks to easing Middle East tensions, generally upbeat Mag-7 earnings reports, and an inflation report that was no worse than feared.

Expectations for US rate cuts this year, however, continued to evaporate before our eyes. A Fed policy meeting looms large this week, which will keep interest rate concerns front and centre.

One of the key highlights last week was what did not happen – namely a further tit-for-tat exchange between Israel and Iran. This is encouraging, suggesting that neither side sees any upside in escalating tensions further. Oil prices have consolidated in recent weeks.

Also positive were good earnings reports from Microsoft and Alphabet, leading to unsurprising share price improvement. Of the other two Mag-7 that reported, fortunes varied. Tesla badly missed earnings expectations, but managed to leave investors upbeat by doubling down on plans to launch a cheaper car. Meta, by contrast, did beat earnings expectations – though its share price sank after it warned of further costly investment in AI projects. The fact that Tesla shares had been sold down in the weeks ahead of the earnings announcement, while Meta’s stock has been bid up, likely contributed to their disparate post-earnings performance.

The US headline and core consumption price deflators both rose 0.3% in March – in line with market expectations. These results did, however, result in small upticks in the annual rates of inflation for both measures – a trend we hope won’t continue!

The week ahead

Turning to the week ahead, the Fed meeting over Tuesday and Wednesday will be of most importance. Although there will be no update on the Fed “dot plot” of interest rate projections (that will come in June), the tone of the post-meeting rhetoric is likely to be more hawkish than we’ve seen in recent months. It’s still likely the Fed will signal the next move in rates will be down, although it’s likely to imply this year’s rate cuts will come later and be smaller in magnitude than the dot plot base case of three rate cuts currently implies. If there’s any consolation, it’s that such a hawkish pivot is now widely anticipated in the market.

Other highlights include another likely strong payrolls report on Friday, with 240k new jobs expected, underpinned by an ongoing strong rebound in labour force growth. The unemployment rate is expected to hold steady at 3.8%. A dip in the unemployment rate would likely hurt both bond and equity markets at this sensitive stage.

Apple and Amazon also report this week, with the last of the Mag-7 reports (from Nvidia) not due until May 22.

Outside of the US, key manufacturing and services PMI reports for China will be released tomorrow, with markets hoping for further signs of an economic improvement to justify the rebound in Chinese stocks since early February. In Europe, key GDP and CPI reports should be benign enough to keep alive hopes for an ECB rate cut in June (ahead of the Fed!).

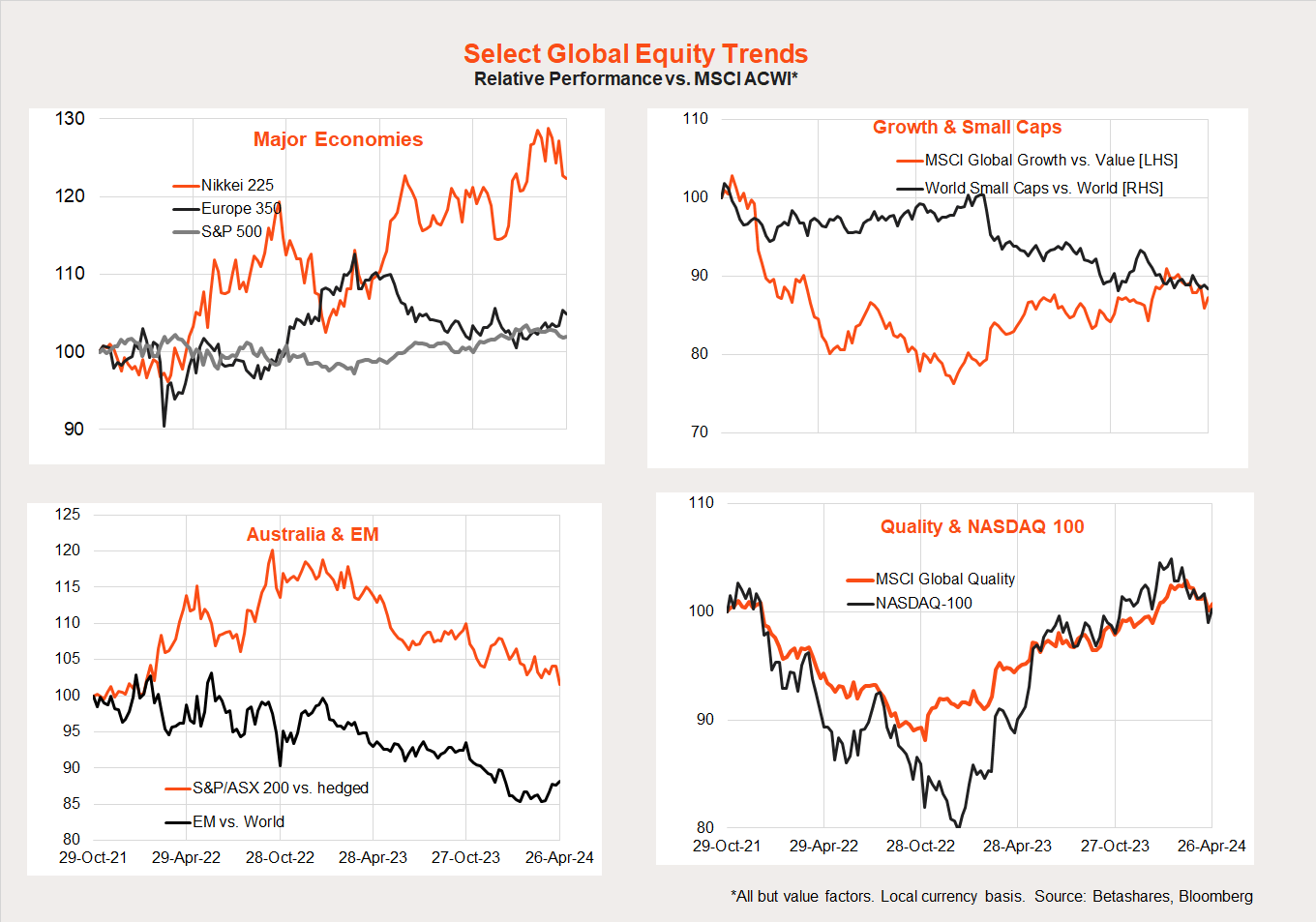

Global equity trends

Looking at global equity trends, the rebound in bond yields is helping drag back the relative performance of growth over value, as evident in the pullback in Nasdaq-100 relative performance. Japan has also pulled back, with Europe faring better. Helped by firmer Chinese stocks, emerging markets are showing tentative signs of relative improvement – though sadly this is less evident for Australia.

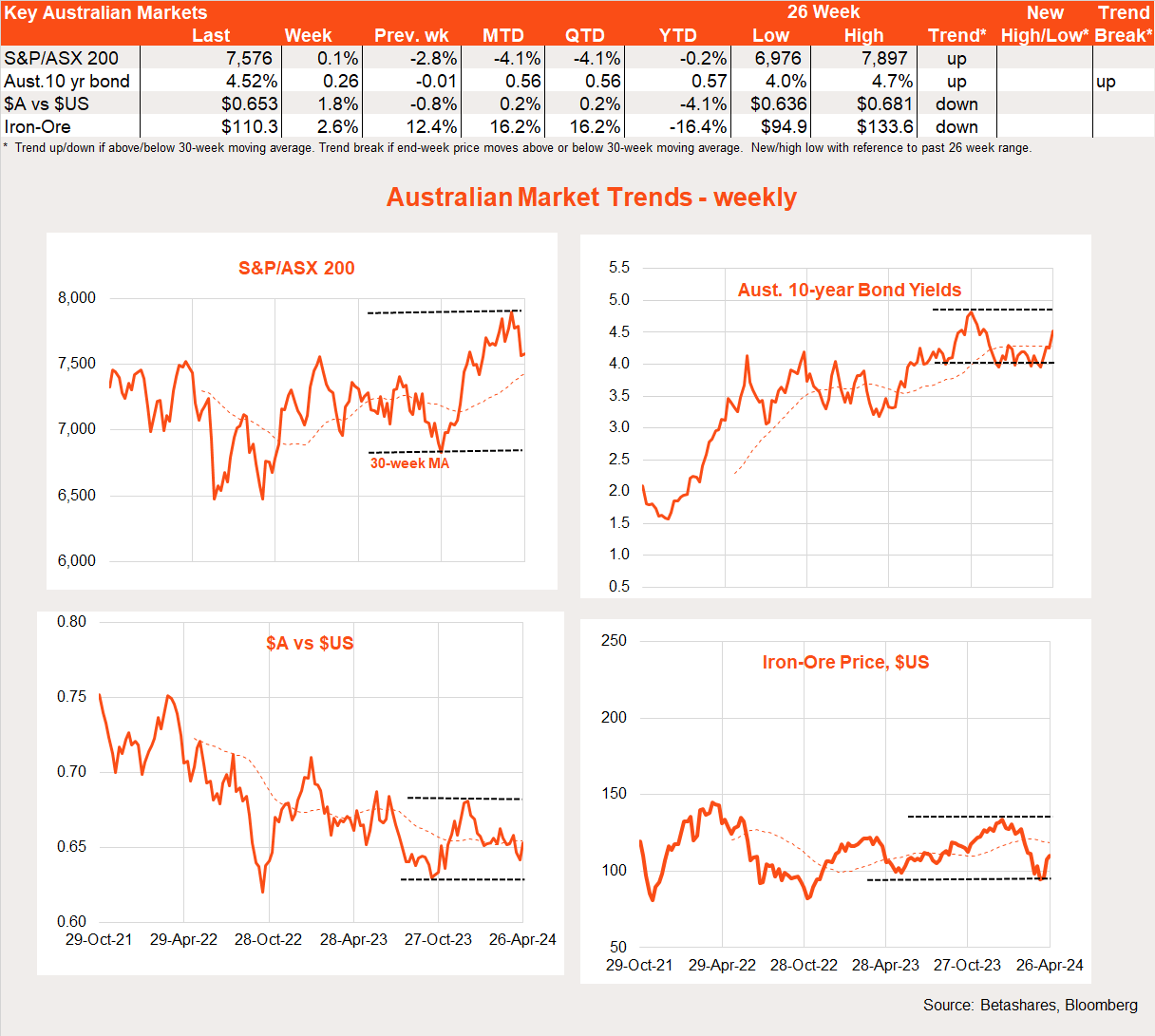

Australian markets

The S&P/ASX 200 was flat last week, though should benefit from Friday’s rebound on Wall Street. Bond yields continued to move higher, reflecting a stronger-than- expected Q1 CPI report. Firmer iron-ore prices and a softer $US also saw the $A lift back above US 65c.

The main local highlight last week was a modestly higher-than-expected Q1 CPI report. Both the headline and trimmed mean measures rose 1.0% in the quarter, compared to market estimates of around 0.8%/0.9%. Strong housing rents, insurance costs and prices for labour-intensive leisure-related services remain the major culprits helping hold up local inflation.

It was a small upside miss, though along with firmer US inflation reports and a resilient local labour market it was enough to further dent expectations for RBA rate cuts this year.

Indeed, talk of a potential rate hike has re-emerged and the market has now all but given up on a rate cut this year. For the record, I’ve shaved back my rate cut expectations for this year from two to one – I still expect a cut, but not before November/December.

The local highlight this week will be March retail sales tomorrow. Low consumer confidence and the real income squeeze is likely to leave spending relatively subdued. Sales rose a modest 0.3% in February even with a Taylor Swift bump, and a gain of only 0.2% is anticipated for March.

Have a great week!

2 comments on this

Great weekly summary – Thanks.

Like many economist, I simply cannot believe how often you all make statements which end up WRONG.

Current Australian inflation according to ABC reported News “Annual inflation slowed to 3.6 per cent in the year to March, down from 4.1 per cent in the 12 months to December”.

How does this make any sense when our shopping trolley has increased nearly 50%, fuel is now $2+ per litre. Council rates have increased significantly, cost of building materials is through the roof, wages are stagnant, rent has increased so much that people are screaming, and the list goes on and on with higher prices, AND YET OUR RESEVE BANK SAYS THAT INFLATION HAS SLOWED FROM 4.1% TO 3.6%.

WHAT A BUNCH OF FUCKING LIARS. Can’t you see how much pain people are in with these higher prices.