Reading time: 4 minutes

In the vast universe of investment approaches, perhaps the largest divide is between growth investors and value investors.

Growth investors are willing to pay a premium for earnings, sales or revenue growth, while value investors target companies, sectors or even regions that they believe are being undervalued by the market based on their fundamental value, often relying on the power of mean reversion to deliver outsized returns.

Reflation and revival of value

Since the GFC, growth strategies, which over this period have been heavily weighted towards technology businesses, have notably outperformed their more cyclical value counterparts, driven by low interest rates and increasing momentum around their long-term secular growth outlooks.

One thing to understand about the relationship between interest rates, economic expectations and equities is this: when the near-term economic outlook is poor, investors typically are willing to pay a premium for long term growth, with cash flows priced further into the future. As the outlook for the economy improves and expectations for normalisation of interest rates emerge, more economically sensitive companies with near-term cash flows become increasingly attractive to investors.

2020 is a great illustration of this dynamic in action.

Against the backdrop of a dire near-term economic outlook, the early stages of the recovery in equities were fuelled by low interest rates and concentrated almost exclusively to technology and long-term secular growth businesses, with ‘bifurcated market’ becoming a favoured catchphrase of market commentators.

As optimism around the recovery, positive vaccine news, and fiscal stimulus have gathered momentum, we’ve seen a notable shift away from secular growth and high quality names, into early-cycle sectors like financials, traditional retail and energy, where COVID-induced headwinds had seen relative valuations severely depressed.

Where to from here?

Whether this recent rotation represents a structural change in market leadership from growth to value as we enter a new cycle remains to be seen.

The domestic and U.S. economy appear as though they have recovered better than initially expected, and are anticipated to remain healthy for an extended period. And while it’s widely viewed that the biggest risk to equities markets and growth valuations is the emergence of inflation and a sharp rise in interest rates, central banks in key developed markets have reiterated their commitment to keeping rates low for years (even in the face of inflation) until they reach their targets for unemployment and wages growth.

In addition, many argue that disinflationary pressures are now more structural in nature (increases in productivity, automation, decreased labour market bargaining power) and may prevent inflation from re-emerging the way it has in the past.

The question it appears is ultimately whether the recovery continues at the pace central banks are hoping, whether it falters, or whether developed market economies have been over stimulated – with disposable incomes and cash savings for many actually rising significantly, combined with the wealth effect from asset price appreciation in equities and homes, potentially contributing to a sharp rise in near term economic growth.

The answer? As is often the case – we don’t know.

Positioning equities portfolios with Barbells

Periods of change and heightened uncertainty, as we’re arguably in now, may reward portfolio construction strategies which look to target and blend specific factors in markets, over strategies that attempt to act as a single ‘all weather’ core allocation.

Such strategies are sometimes referred to as ‘barbells’, and involve combining and balancing assets that each provide exposure to specific investment factors, and that are generally uncorrelated, but when held together, seek to complement one another to improve portfolio outcomes.

If we look at U.S. equities specifically:

- Arguably the two most powerful forces in equity returns are momentum and mean reversion

- Growth investors historically have benefitted from momentum, while value investors look to mean reversion to deliver alpha

- By combining growth exposures with strong momentum properties, such as NDQ Nasdaq 100 ETF or technology-focused sector/thematic exposures such as HACK Global Cybersecurity ETF , CLDD Cloud Computing ETF or RBTZ Global Robotics and Artificial Intelligence ETF , with exposures that seek to benefit from periodic mean reversion and rotation to mid-cap and smaller large cap stocks, such as QUS S&P 500 Equal Weight ETF , investors can attempt to position portfolios to have relative performance benefits across the range of scenarios discussed above and limit volatility from interest rate-induced rotations

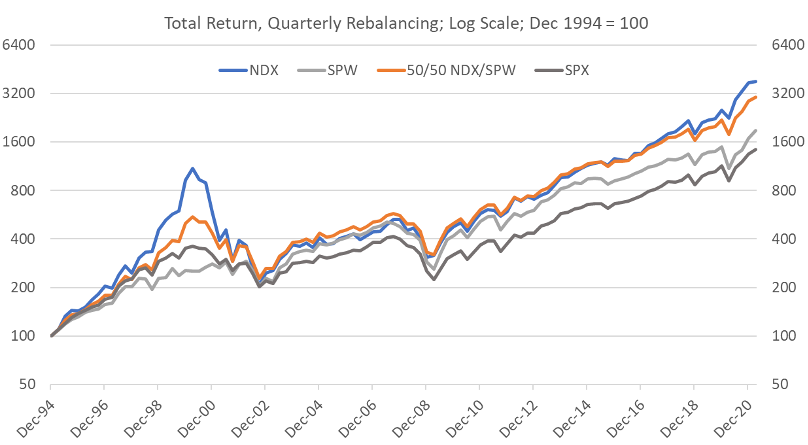

- Evidence suggests that such combinations can potentially capture the ‘best of both worlds’ over the long run, with a blend of NDQ and QUS having outperformed the more vanilla S&P 500 market cap-weighted index over the long term – demonstrating the potential long-run power of the barbell strategy when applied to U.S. equities

The Nasdaq 100 + S&P 500 Equal Weight Barbell – as at 31/3/2021

Source: Bloomberg; BetaShares Capital. Provided for illustrative purposes only. Not a recommendation to make any investment decision or adopt any investment strategy. Total returns for index exposures are for the period 31 December 1994 to 31 March 2021, displayed in a log scale. The Nasdaq 100/S&P 500 Equal Weight Blend returns assume a hypothetical monthly rebalancing to a target 50:50 allocation. All series are rebased to have a starting value of 100. You cannot invest directly in an index. Index performance does not take into account any fund fees and costs. Past performance is not an indicator of future performance of any index, fund or investment strategy

Written by

Adam O'Connor

National Head of Wealth Distribution