Hugh Lam

5 minutes reading time

Making the case for Chinese equities has not been easy for some time.

Having experienced multiple boom and bust cycles over the past two decades, the world’s second largest economy continues to grapple with a mercantilist Trump and a domestic economy that’s been weakening in recent years.

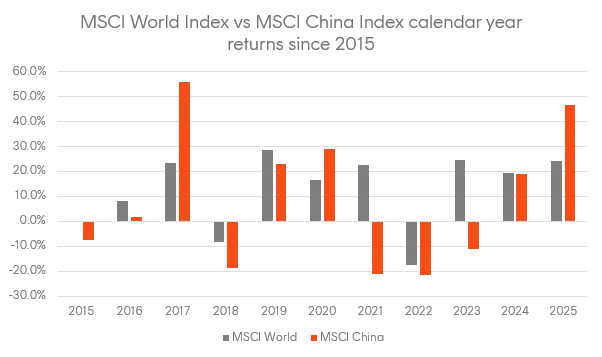

But despite these challenges, Chinese stocks are having their best year and outperforming global peers by the widest margin since 2017.

Source: Bloomberg. 2025 figure is year to date (as at 12 November), annualised.

What was once considered an ‘uninvestable’ region just last year, investors are now re-engaging with China’s stock market following a positive shift in sentiment that’s been driven by the government’s renewed focus on pursuing long-term structural changes, including but not limited to:

- Positioning manufacturing capabilities around higher-value, technology-intensive, and innovation-driven industries (e.g., AI, electric vehicles, solar panels, semiconductors)

- Expanding domestic demand and shifting toward a consumption-led growth model

- Pushing reforms in the financial sector and across state owned enterprises to improve governance (boosting shareholder returns and eliminating excess capacity)

Alongside this push, Beijing’s embrace of its vibrant private sector has seen local technology giants such as Alibaba, Tencent and Baidu spearheading the rally in Chinese stocks this year, backed by strong AI-driven earnings growth.

But while structural economic challenges remain, the key question that remains top of mind for investors is whether the rally in Chinese stocks can continue?

Is this time different?

Any investor familiar with China would be familiar with the “3D” challenge the country has been facing:

- A high level of debt from local governments and the property sector,

- Deflation driven by weak consumer demand and excess capacity,

- and a challenging demographic picture with a rapidly aging population placing pressure on a shrinking workforce

While there are concerns this could drive China’s economy to end up like that of Japan in the early 1990s, could the worst already be priced in?

To address its falling property market, China has implemented a combination of targeted policy measures including lowering down payment requirements for first-home buyers and establishing a central fund of RMB 300 billion to ease the financial burden of troubled developers and clear excess inventory.

Additionally, after years of hypercompetition that’s led to overcapacity in certain industries like solar panels and electric vehicles, China’s ‘anti-involution’ campaign is aimed to reduce excess production capacity in a bid to restore profitability. That should support corporate earnings and help reflate the economy out of a prolonged period of deflation.

While the longer-term outcomes of these reforms are yet to be seen, the important takeaway is that the Chinese government is very much focused on stabilising its economy across different channels by implementing policy in a timely and targeted manner.

With a ‘policy put’ effectively in place and valuations trading lower than most other markets, continued marginal improvements in the outlook for China’s economy could lead to a sustained recovery in both the local stock market and consumer sentiment.

Winning the AI race

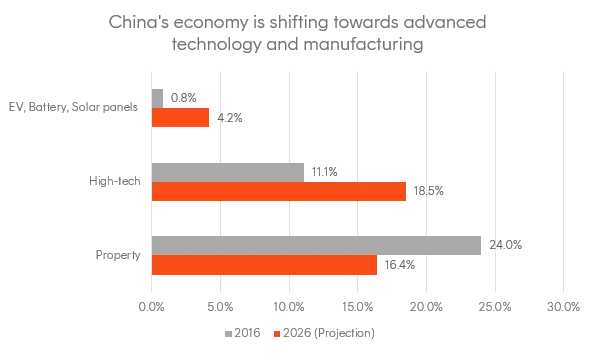

Beyond these reforms, China’s pivot toward high-tech manufacturing will be essential in transforming the longer-term trajectory of its economy. Generative AI is estimated to start raising potential growth by 2026 and provide a 0.2-0.3 percentage point boost to China’s GDP by 2030, according to Goldman Sachs Research1.

Of course, that depends on the future path of AI development and adoption; but given China’s access to cheap, abundant energy resources and its ability to innovate with less resource-intensive models following the release of DeepSeek, their pathway to build out AI compute appears more economically viable than that of the US.

To that end, we think investors may find value by being more selective within Chinese equities. The local technology sector has been a strong performer this year led by Beijing’s national championing of local AI leaders, whilst more cyclically oriented and tariff-exposed industries such as energy, real estate and segments of renewables have lagged due to industry-specific headwinds and broader weakness in the economy.

Source: As at July 2024. Bloomberg Economics

The bottom line

We think now is the time for investors to re-engage with China, particularly towards sectors like technology that are deemed a strategic priority for the nation.

With that said, more work needs to be done in addressing high levels of indebtedness in the property market, stimulating consumer demand, and bringing supply back in balance. Some progress has been made in these areas, but any sustained recovery will likely be driven by Beijing’s commitment to reforming industrial policy in the coming years.

Overall, the current backdrop is compelling with local AI developments and focus on improving corporate profitability providing a healthy backdrop for upward revisions to earnings growth estimates – a key driver of stock market returns.

Additionally, underweight global investor positioning, falling US interest rates and a weaker dollar provide tailwinds for further capital inflows into China.

1. Source: https://www.goldmansachs.com/insights/articles/what-advanced-ai-means-for-chinas-economic-outlook