David Bassanese

7 minutes reading time

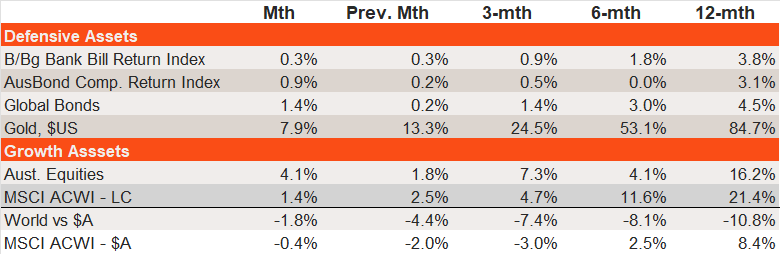

Major asset class performance

- Global equities inched further ahead in February with weakness in US equities (reflecting AI concerns) offset by solid gains in non-US markets. However, reflecting Australian dollar strength, global equities posted a small decline in unhedged AUD terms.

- Australian equities also saw solid gains, despite a local interest rate hike, a rising Australian dollar (which hurts offshore earnings) and weakness in the technology and consumer discretionary areas. Solid earnings reports helped the major financial and resource sectors, with potentially greater foreign interest also emerging in the local market.

- Among defensive assets, gold shone brightly once again, while easing bond yields produced modest positive returns for Australian and global bonds.

Source: Bloomberg, Betashares. Cash: Bloomberg Australian Bank Bill Index; Australian Bonds: Bloomberg AusBond Composite Index; Global Bonds: Bloomberg Global Aggregate Bond Index ($A hedged); Gold: Spot Gold Price in $US; Australian Equities: S&P/ASX 200 Index; Global Equities: MSCI All-Country World Index in local currency and $A currency (unhedged) terms. Past performance is not indicative of future performance.

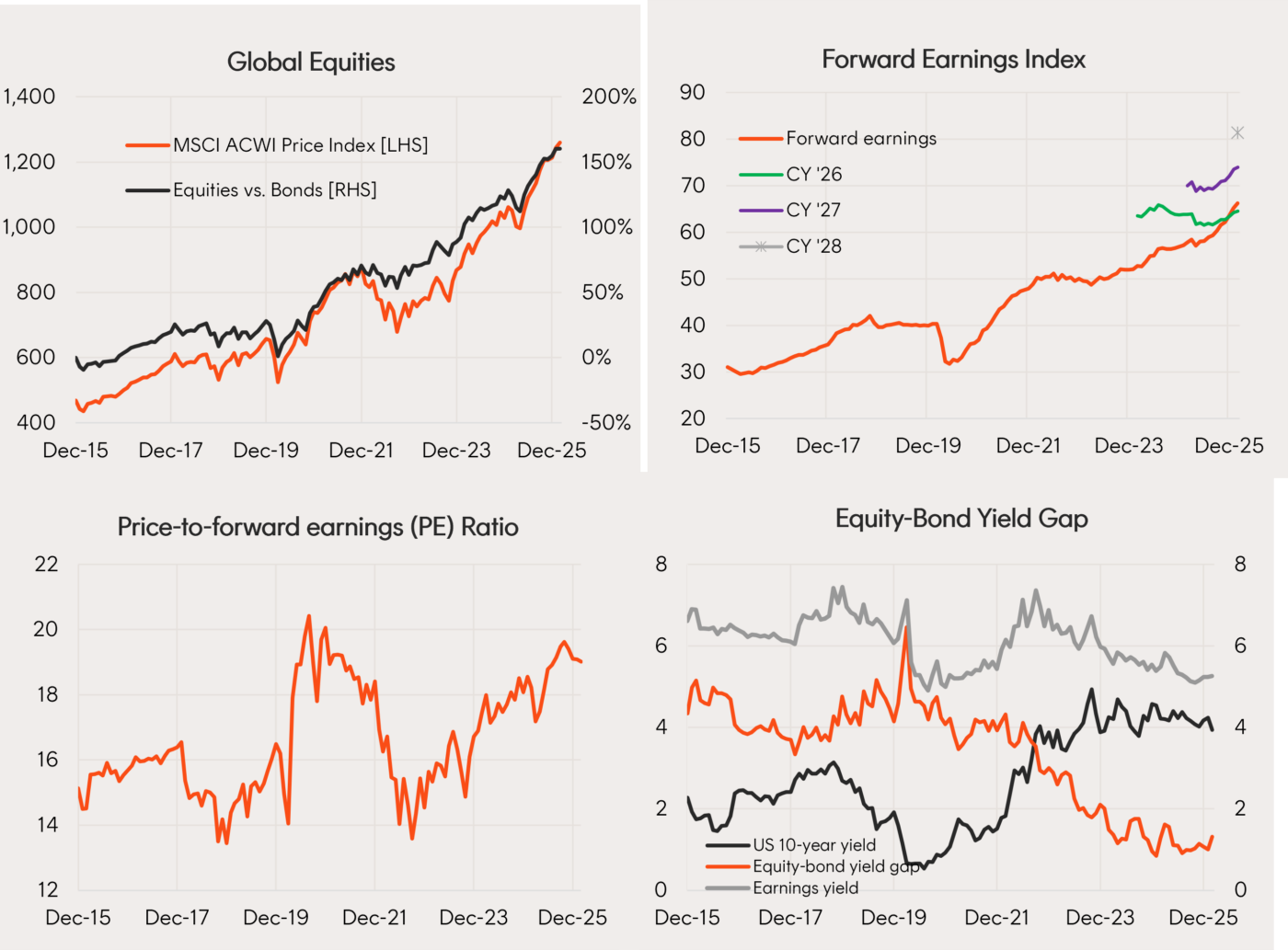

Global equities

- Global equities continue to grind higher despite a pullback in valuations since October last year, underpinned by continued growth in corporate earnings.

- The MSCI All-World Equity Index returned 1.4% in local currency terms, after a 2.5% gain in January. This reflected 1.7% growth in forward earnings, partly offset by a slight 0.4% decline in the price-to-forward earnings ratio to 19.0.

- While easing bond yields supported equity valuations (US 10-year yields dropped 0.30% to 3.94%) this was offset by a spike higher in the equity risk premium.

- Earnings expectations remain upbeat, with 11.4% expected growth in forward earnings by end-2026.

- With valuations elevated, continued market gains are still possible, provided bond yields don’t rise much and/or the current bullish earnings outlook remains in place.

Source: Bloomberg, LSEG, Betashares. Global Equities: MSCI All-Country World Index. Global Bonds: Bloomberg Global Aggregate Bond Index ($A hedged). You cannot invest directly in an index. Past performance is not an indicator of future performance.

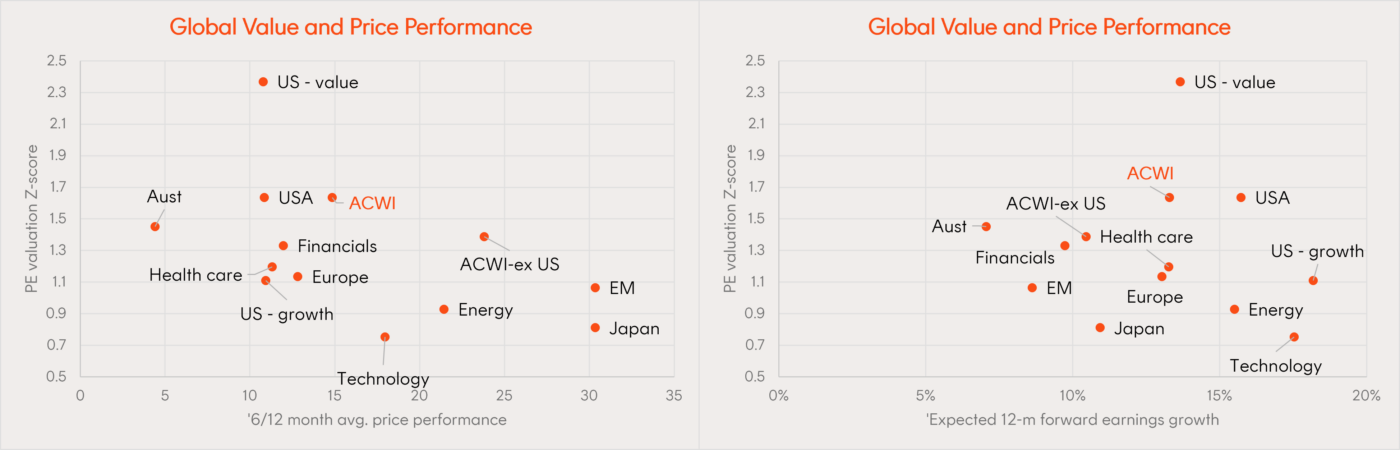

- Relative performance within global equities is tending to favour cheaper non-US exposures such as Japan and emerging markets. Energy shares are also performing well. Global technology is no longer a standout performer, although given ongoing solid earnings growth, it has improved in relative valuation terms.

- Energy, technology and the US market retain relatively strong earnings growth expectations, although companies in non-US markets are still forecast to deliver 10% forward earnings growth over the next 12 months.

Source: Bloomberg, LSEG, Betashares. Relative performance versus the MSCI All-Country World Index (local currency terms) for the indices which the relative ETFs track. You cannot invest directly in an index. Past performance is not an indicator of future performance.

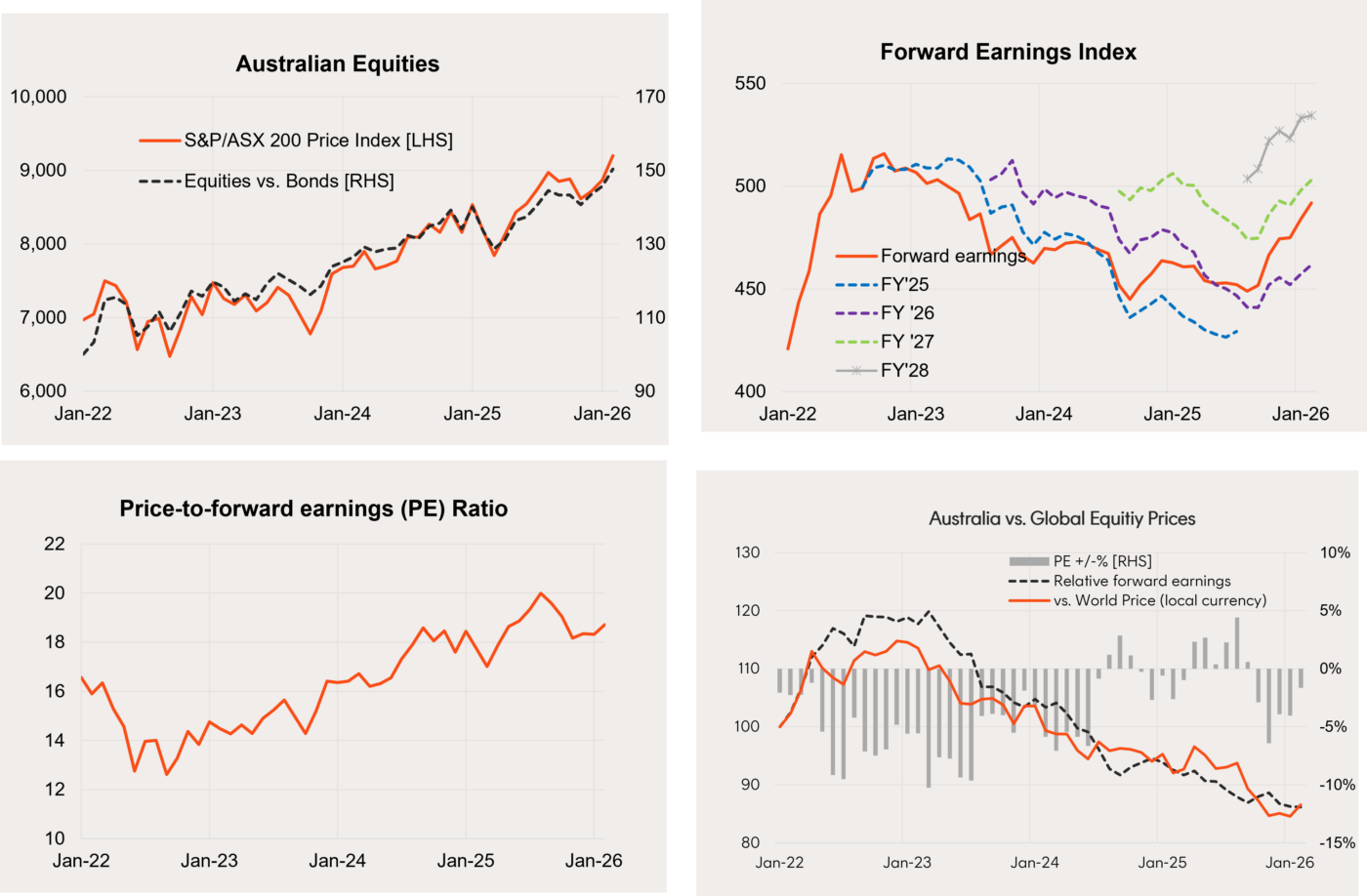

Australian shares

- As has been the case globally, earnings have largely led the Australian equity market higher since late 2025, although a modest uplift in P/E valuations has been evident in recent months.

- The S&P/ASX 200 returned 4.1% in February, reflecting a 1.6% gain in forward earnings and a 2.1% gain in the price-to-forward earnings ratio to 18.7. The stronger lift in P/E valuations of late has largely erased the Australian equity discount to global equities which emerged late last year.

- Encouragingly, local earnings expectations continue to rise. Even so, the implied 5.5% growth in Australian forward earnings by the end of 2026 is still less than that expected for global earnings. Weaker expected earnings growth in the financials and energy/materials sectors (compared to global peers) are the main local drags.

Source: Bloomberg, LSEG, Betashares. Australian Equities: S&P/ASX 200 Index. Australian Bonds: Bloomberg AusBond Composite Index. You cannot invest directly in an index. Past performance is not an indicator of future performance.

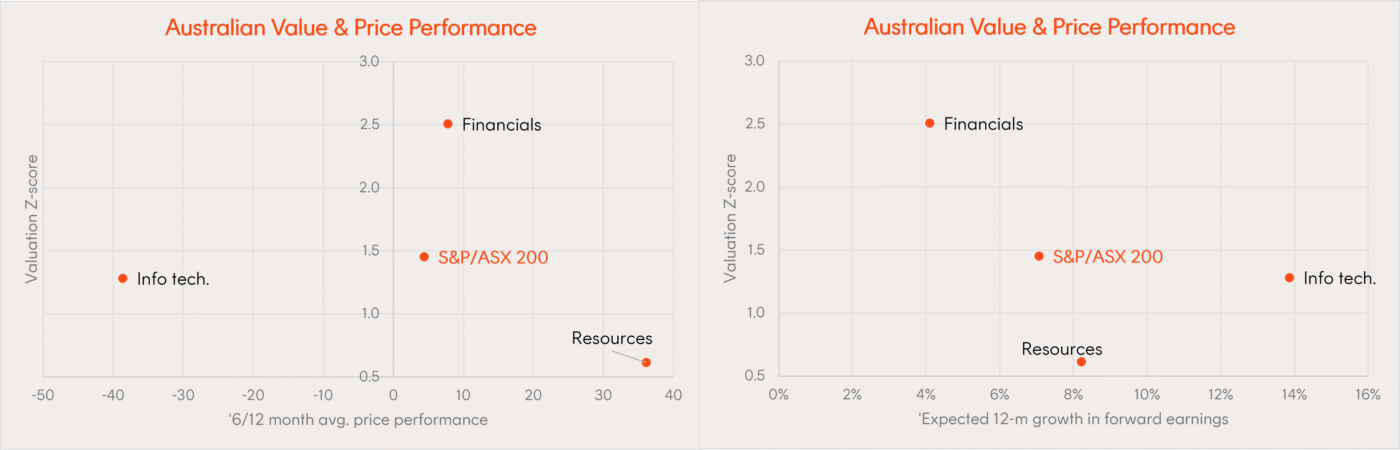

- Among the key sectors tracked below, resources remains a standout performer. Along with solid relative performance, resources remain both relatively cheap (to the broader market) and have solid earnings growth expectations.

- The recent underperformance of information technology now means the sector is also relatively cheap (in terms of its relative degree of P/E valuation premium to its own 20-year average) while retaining solid earnings growth expectations.

Source: Bloomberg, LSEG, Betashares. Relative performance versus the S&P/ASX 200 Index for the indices which the relative ETFs track. You cannot invest directly in an index. Past performance is not an indicator of future performance.

Fixed-rate bond trends

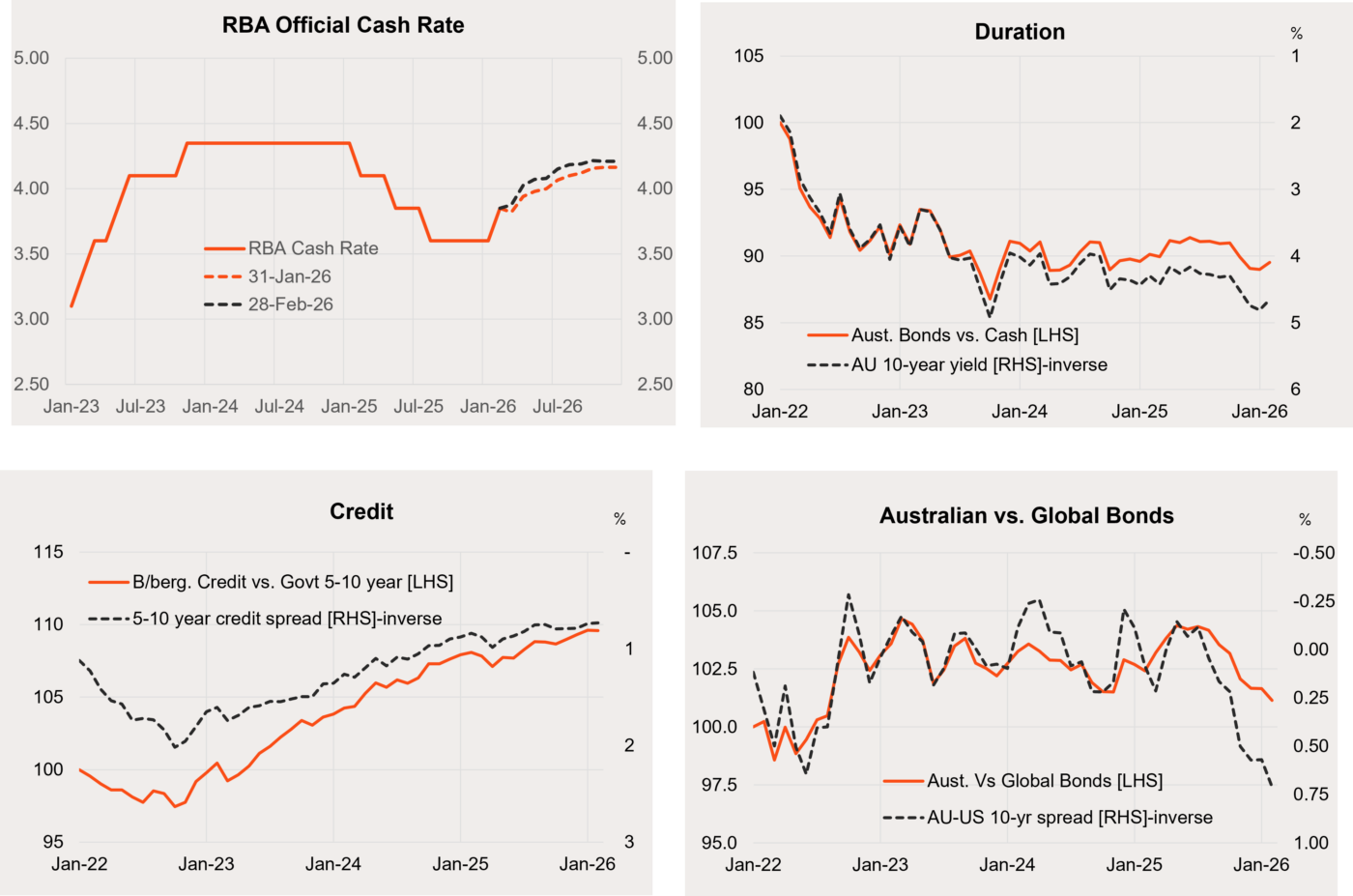

- Local rate hike expectations edged up a little further in February, reflecting a firm January monthly CPI report. Almost two rate hikes are currently priced for this year, with a full rate hike priced by May. Markets are also attaching some risk (30%) to a rate hike later this month.

- In the US, by contrast, rate cut expectations shifted only marginally, with two cuts still expected this year. US bond yields fell, reflecting risk-off sentiment in equity markets around AI disruption.

- Easing US bond yields helped lower local 10-year bond yields in February by 0.16% to 4.65% – following their rise from late last year and over January.

- Longer-term credit spreads have levelled out in recent months, allowing corporate bonds to continue to modestly outperform government bonds.

- A widening in Australian versus global bond yields in recent months has seen local bonds underperform their global peers.

Source: Bloomberg, Betashares. Australian bonds: Bloomberg AusBond Composite Bond Index; Global Bonds: Bloomberg Global Aggregate Bond Index ($A hedged).

Australian dollar

- The Australian dollar rose a further 2.3% in February against the US dollar, from US 69.6c to US 71.2c – largely reflecting widening short-term interest rate differentials.

- Firmer iron ore prices, a weaker US dollar and a notable widening in the short-term interest rate differential against the US have all helped push up the Australian dollar over recent months.

- Although iron ore prices and the US dollar have broadly stabilised in recent months, the 12-month forward expected cash rate in Australia (relative to that expected in the United States) has continued to widen. It is now at 1.19%, as at the end of February 2026.

- The divergent central bank outlook, greater US-centric AI concerns and the still relatively expensive US dollar suggest the Australian dollar could strengthen further in coming months.

Source: Bloomberg, LSEG, Betashares. Australian Equities: S&P/ASX 200 Index. Australian Bonds: Bloomberg AusBond Composite Index. You cannot invest directly in an index. Past performance is not an indicator of future performance.