All in on AI? 3 ways to reduce concentration risk

David Bassanese

5 minutes reading time

- Global shares

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Global markets

The US S&P 500 rose further last week – the fifth weekly gain in a row and a new record high, closing above the psychological 5,000 level. It remains in a strong uptrend.

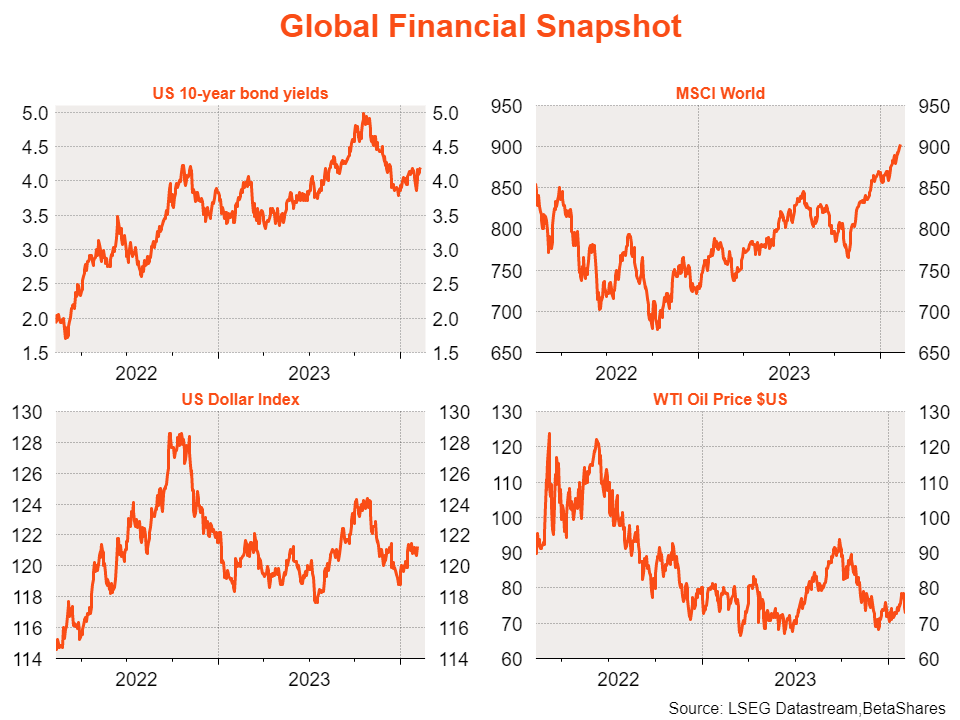

US 10-year bond yields ticked up from 4.02% to 4.17%, however, and remain in a gradual uptrend since bottoming at 3.86% in the week-ending December 25 – as strong US economic data has reduced the chance of a near-term US rate cut. Associated with the rebound in bond yields has been a firmer US dollar, which has lifted 2.8% since Christmas. In turn, that’s seen the $A drop from around US 68c to US65c.

The story of the past few months is as follows:

- US bond yields peaked and US equities bottomed in October. With growing evidence of falling US inflation without a recession, mid-year fears of ‘no landing’, which saw bond yields rise and equities fall from July to October, transformed into renewed hopes of a ‘soft landing’.

- This sentiment was validated by no less than US Fed chair Powell at the December policy meeting, who suggested the next move in official rates was down, but not any time soon.

- Markets being markets, the bond market went crazy and began to price in aggressive rate cuts this year – beginning as early as March.

- But the ongoing resilience of the US economy – along with Fed signalling – have forced markets to backtrack at least on the prospects of a March rate cut, though aggressive cuts are still expected later this year.

- So since late last year bond yields have lifted and the US dollar has firmed, though this has not stopped US equities from moving higher – helped by a solid US earnings outlook.

This past week was more of the same, with a strong US service sector report – though which also worryingly showed a lift in pricing pressures. The Q4 earnings season also rolled on, with continued good results.

The outlook remains encouraging – with two caveats.

First, there’s still a risk that the ‘no landing’ fear could re-appear if growth remains firm and, much more importantly, inflation – especially services inflation – fails to continue easing. There are a few worrying signs in the latter regard: the services price index released last week, an ongoing rebound in the small business pricing index and even a modest lift in the average hourly earnings growth in the recent payrolls report.

A second, less serious, risk is that the S&P 500 is back to trading at 20 times forward earnings – suggesting a lot of the good news is already priced in, at least in the near-term. The market – especially after five weekly gains – appears in need of at least a cleansing pull-back.

Against this backdrop, future US inflation reports will be critical – any upside surprise could hurt the current soft-landing narrative. The next test comes on Tuesday this week (US time) with the January CPI report, which is expected to reassuringly show core annual inflation easing a touch further from 3.9% to 3.8%. Fingers crossed!

Also of interest this week will be January US retail spending on Friday, which is expected to show more subdued spending after a strong December.

Countering these inflation concerns, China’s January consumer price report was weaker than expected last week, with annual deflation increasing to 0.8% from 0.5% in December.

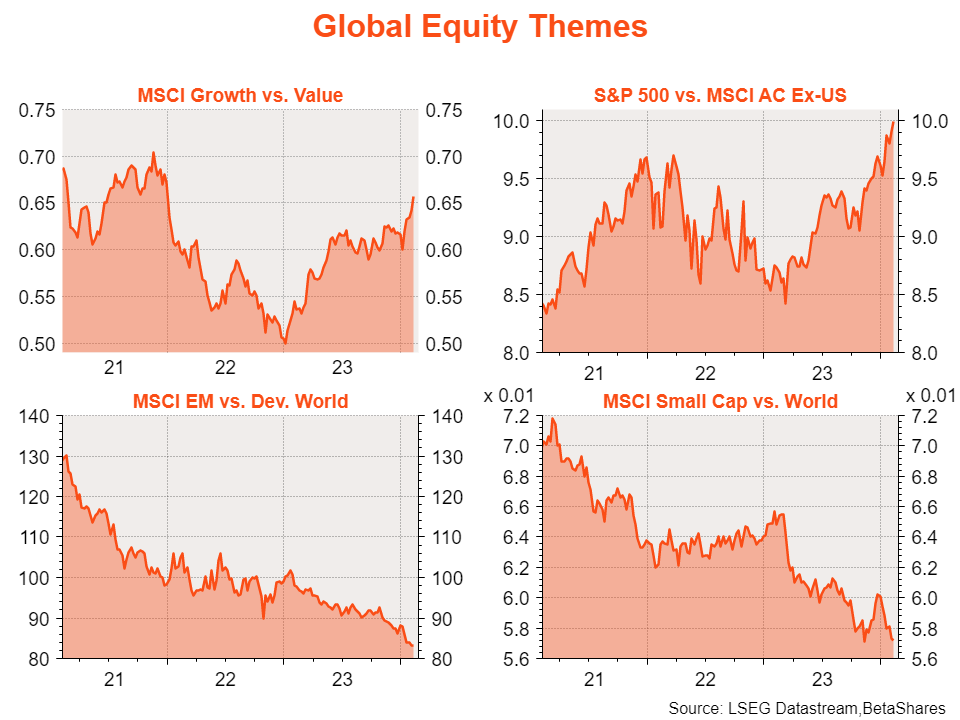

In terms of global equity themes, the late-23 ‘soft landing’ rotation towards cheaper non-US large-cap technology areas has been unwinding so far in 2024.

Australian markets

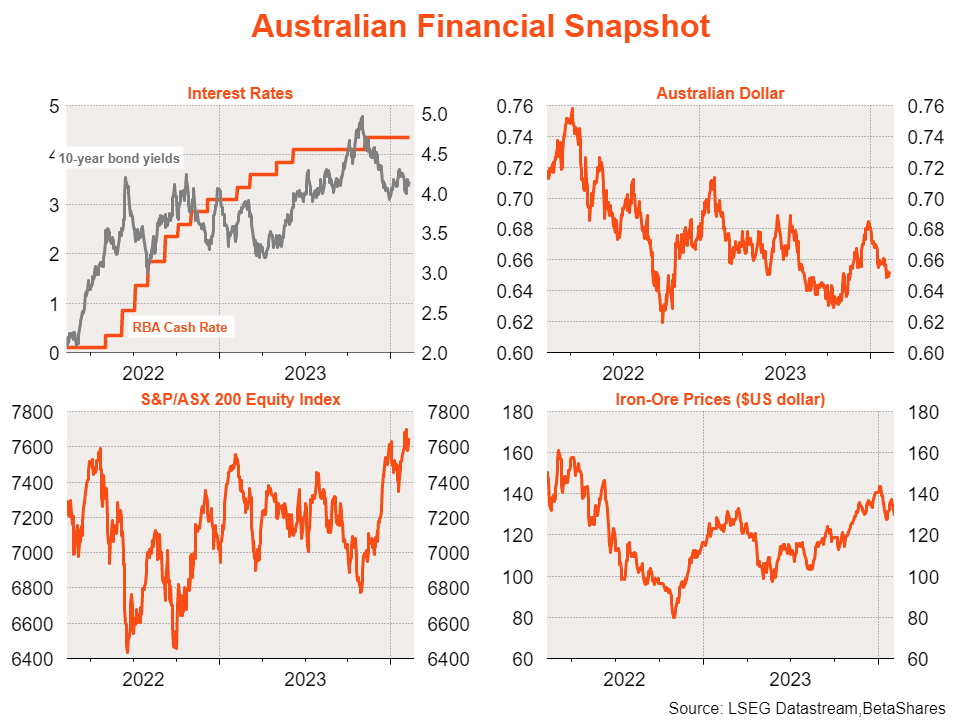

The S&P/ASX 200 pulled back 0.7% last week, not helped by a mixed early start to the local earnings reporting season and a less dovish than hoped RBA policy meeting. As in the US, 10-year bonds yields ticked higher from 4.08% to 4.16%. The $A held steady at just over US65c.

In terms of economic events, the quarterly retail sales report confirmed that spending in real terms remained soft in Q4, rising by a mere 0.3%.

The major highlight, however, was the RBA meeting, updated RBA economic forecasts and the all-new RBA Governor’s press conference.

The bottom line of the new RBA extravaganza is that the Bank is less inclined to signal a pivot to a policy easing bias, unlike in the US. That despite the RBA modestly reducing both its growth and inflation forecasts.

At best, the RBA seems to suggest a ‘neutral’ policy bias, with balanced risks around the next move in rates. The lingering RBA concern is the stickiness in service sector inflation, which as noted above could also re-appear as a problem in the US.

That said, markets – as do I – still anticipate the next local move in rates is down, starting around August.

Key local highlights this week are the January NAB business survey and official employment report on Tuesday and Thursday, respectively. Business conditions are likely to remain healthy, with a focus on the extent of lingering cost and price pressures.

After the extreme employment volatility over November and December (due to seasonal adjustment problems) a still firm 30k gain in jobs is expected for January, though with the unemployment rate expected to tick up to 4.0% from 3.9%. The latter would suggest the glacial easing in labour market tightness continues.

Have a great week!