David Bassanese

4 minutes reading time

Week in review

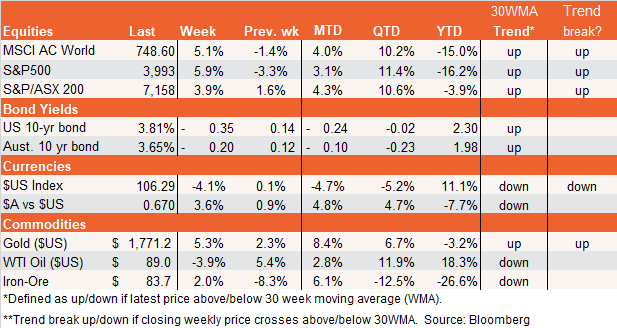

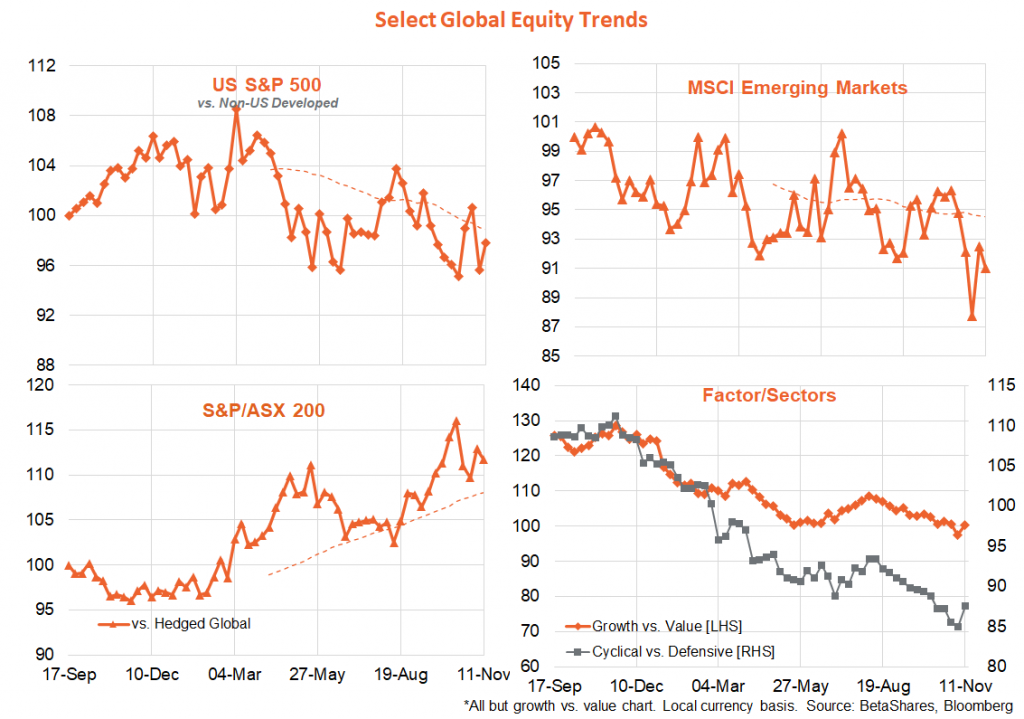

By far, the key market highlight over the past week was the lower-than-expected October US Consumer Price Index (CPI) report. Core inflation (excluding food and energy) rose by only 0.3% over the month compared with market expectations of 0.5%. After a number of higher-than-expected results in recent months, this was enough to send stock and bond prices flying higher. The US Dollar also slumped while the Australian Dollar surged.

At the very least, the result virtually cements the case for the US Federal Reserve (the Fed) to only raise rates by 0.5% at its December policy meeting. But it does not necessarily lower the likely peak Federal Funds Rate of around 5% next year – or mean that the US can get inflation down without a recession after all. Sifting through the entrails of the CPI report, it’s clear that the COVID-related surge in the prices of some goods and services (like used cars and airline rates) is abating and there’s a quirk that helped reduce healthcare costs in the month that won’t be reflected in the Fed’s preferred inflation measure – the private consumption deflator. Housing costs are also likely to remain firm, though, over coming months – though many have noted this reflects lags before easing house prices help to bring down measured rents within the CPI.

What’s less clear is whether a still very tight labour market and rising labour costs can contain service sector prices more broadly, which still make up around 75% of consumer inflation. Do we still need a material slowdown in US consumer spending and employment demand? Is what’s been dubbed the “immaculate disinflation” scenario really possible?

History, at least, suggests it’s not. Indeed, there’s never been a material slowdown in US inflation after a surge as big as seen recently without a recession, but of course – as the saying goes – this time could be different.

In other news, Democrats performed better than expected in the US mid-term elections, retaining control of at least the Senate – with the House of Representatives still up for grabs. If the Democrats do gain control of both Houses it will deny markets the Washington “gridlock” they tend to prefer – though I don’t anticipate this would be a major sustained negative for stocks, especially if inflation news remains positive.

In Australia, the biggest news last week was a surprise slump in consumer confidence and a surge in near-term consumer inflation expectations, which together have mixed implications for the RBA. On balance, it still seems likely the central bank will press ahead with a 0.25% rate increase next month – especially if this Thursday’s labour market report remains fairly strong.

Week ahead

While equities and bonds may well want to continue basking in the warm afterglow of last week’s benign US CPI report for at least a few more days, of interest will be how the range of Fed officials due to speak this week interpret the result. Will they remain resoundingly hawkish, or express hope that it could mean rates won’t need to rise much further? I think they will continue their tough talk, though I don’t think markets will be in the mood to listen.

Also of interest will be US retail sales and producer prices out mid-week. Signs of slowing in US consumer spending (US consumer sentiment slumped on Friday) and/or lower producer prices pressures would likely be greeted as further good news for both equity and bond markets.

In Australia, minutes from the latest RBA meeting are released tomorrow and the October labour market report is due on Thursday. But perhaps of most interest will be the wage price index report on Wednesday. Market expectations are that annual wage growth will lift from a very benign 2.6% to a still benign 3.0% despite unemployment remaining at generational lows of 3.5%. If so, this will be consistent with the RBA’s expectation of a modest acceleration in wages inflation over the coming year, though not to a pace too threatening to the inflation outlook.

Have a great week!