India: The market's hidden giant

David Bassanese

5 minutes reading time

- Global shares

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Global markets – week in review

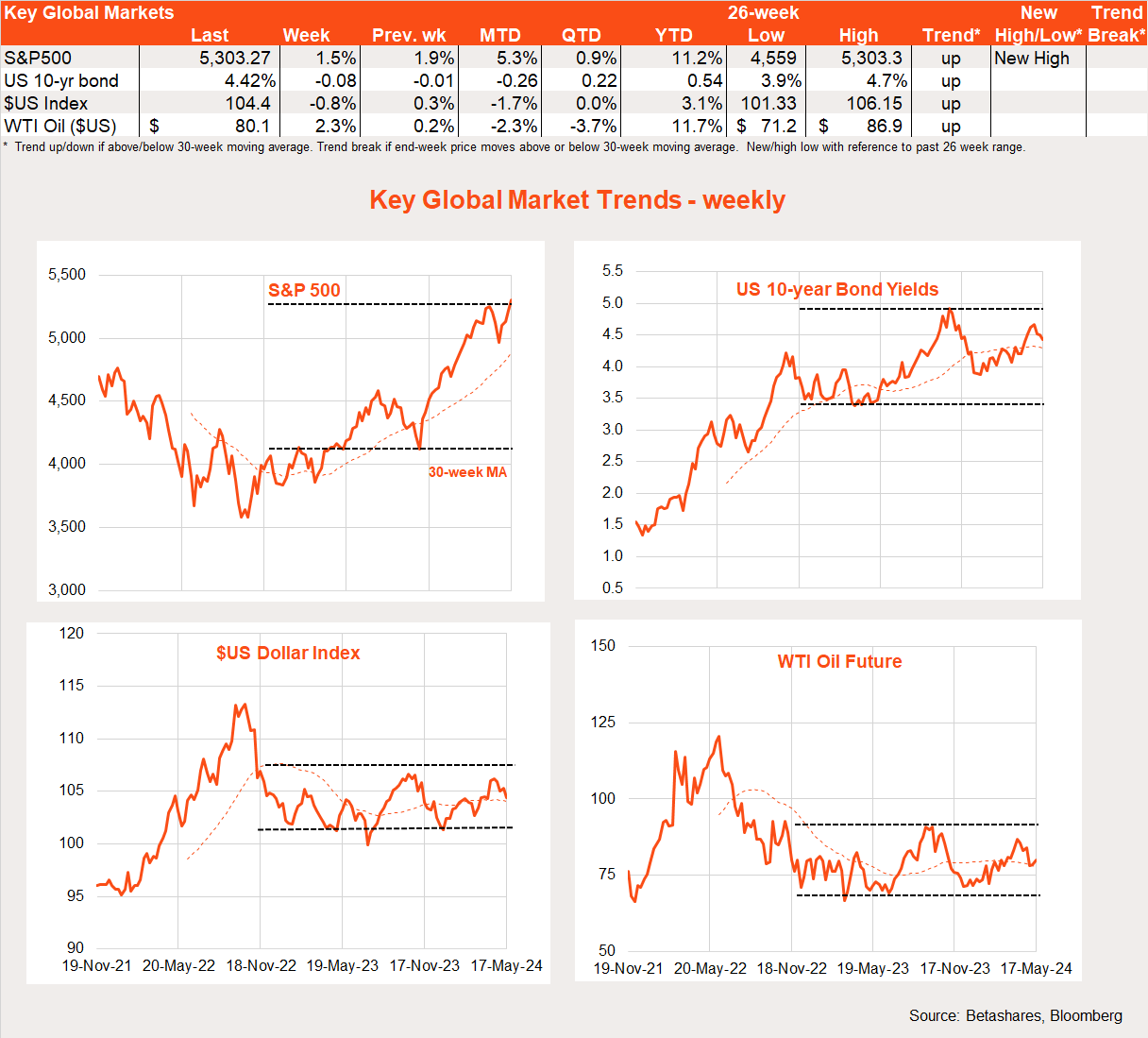

The global equity market rebound continued into its fourth week thanks to a US CPI inflation report which – for the first time in several months – failed to surprise on the upside. Softer retail spending and a patient Fed chair Jerome Powell further reassured markets that the next move in US rates would likely be down.

As a result, the US S&P 500 unwound all of its recent mini-correction to reach a new record high.

The global market highlight last week was the April US consumer price index report, with headline prices rising a less-than-expected 0.3% (market 0.4%). Core CPI inflation, excluding food and energy, also rose by 0.3% – though this was in line with market expectations – allowing annual core inflation to ease to 3.6% from 3.8%.

Despite a flattening in house prices and rents over the past year, housing inflation in the official CPI statistics remains disappointingly firm – which hopefully just reflects longer the usual lags. Otherwise, the details of the CPI report – along with those of producer prices also released last week – suggest the more important Fed’s preferred measure of inflation (the PCE) is shaping up to be fairly benign later this month, with a gain in core prices of potentially only 0.2%.

In other news, Fed chair Powell remained fairly relaxed and comfortable about the upside inflation misses in Q1, noting that policy is restrictive and we likely just need to be patient. Also helping Wall Street sentiment was a surprisingly soft April retail sales report, with flat spending (market +0.4%).

Outside the US, China’s monthly ‘data dump’ was mixed, with solid industrial production yet soft retail spending – the latter likely not helped by ongoing woes in the property sector. China’s solution so far is to place band-aids over the housing problem and keep the economy ticking over through higher exports. The latter, in turn, could lead to renewed trade tensions if China is accused of dumping cheap exports – like steel, electric cars and solar panels – onto world markets. The US has already responded though a lift in tariffs.

Last Friday, China announced further dubious measures to support the housing sector, such as allowing local governments to buy excess apartments and further help for builders to finish uncomplete projects.

The week ahead

It’s fairly light in terms of key global events in the week ahead. Minutes from the latest Fed meeting will likely show most members comfortable about keeping rates “higher for longer” but not really considering another rate hike. A host of Fed speakers will likely reiterate the “wait and see” sentiments of Powell over the past week.

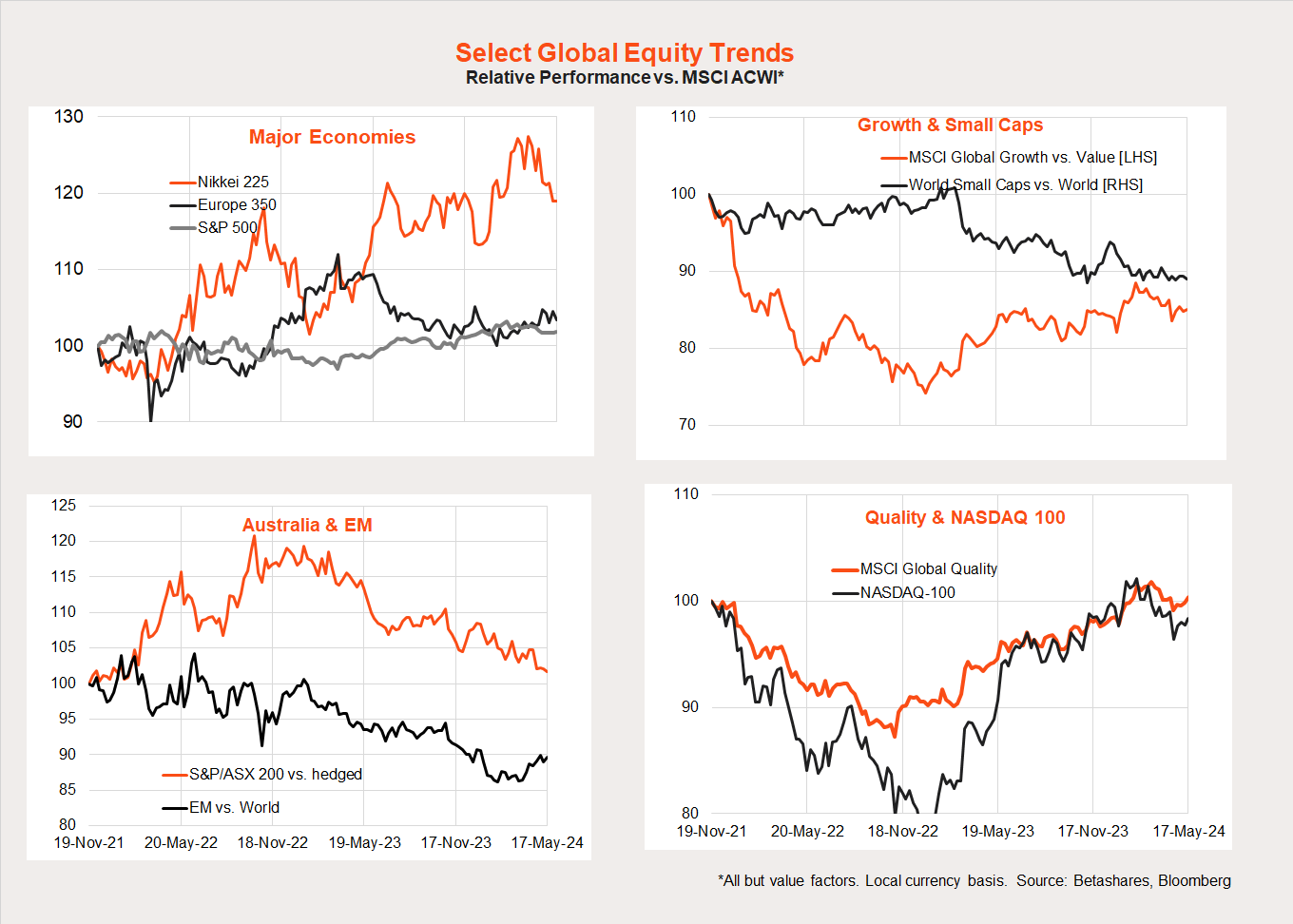

Global equity trends

Looking at global equity trends, the equity rebound over recent weeks – reflecting the more encouraging interest rate outlook – has favoured a bounce back in the relative performance of NASDAQ-100/global quality exposures – though a broader rebound in global growth over value is less evident.

China is also helping fuel a rebound in emerging markets, while Japan is enduring a relative performance correction. Australia and global small caps continue to underperform.

Australian markets

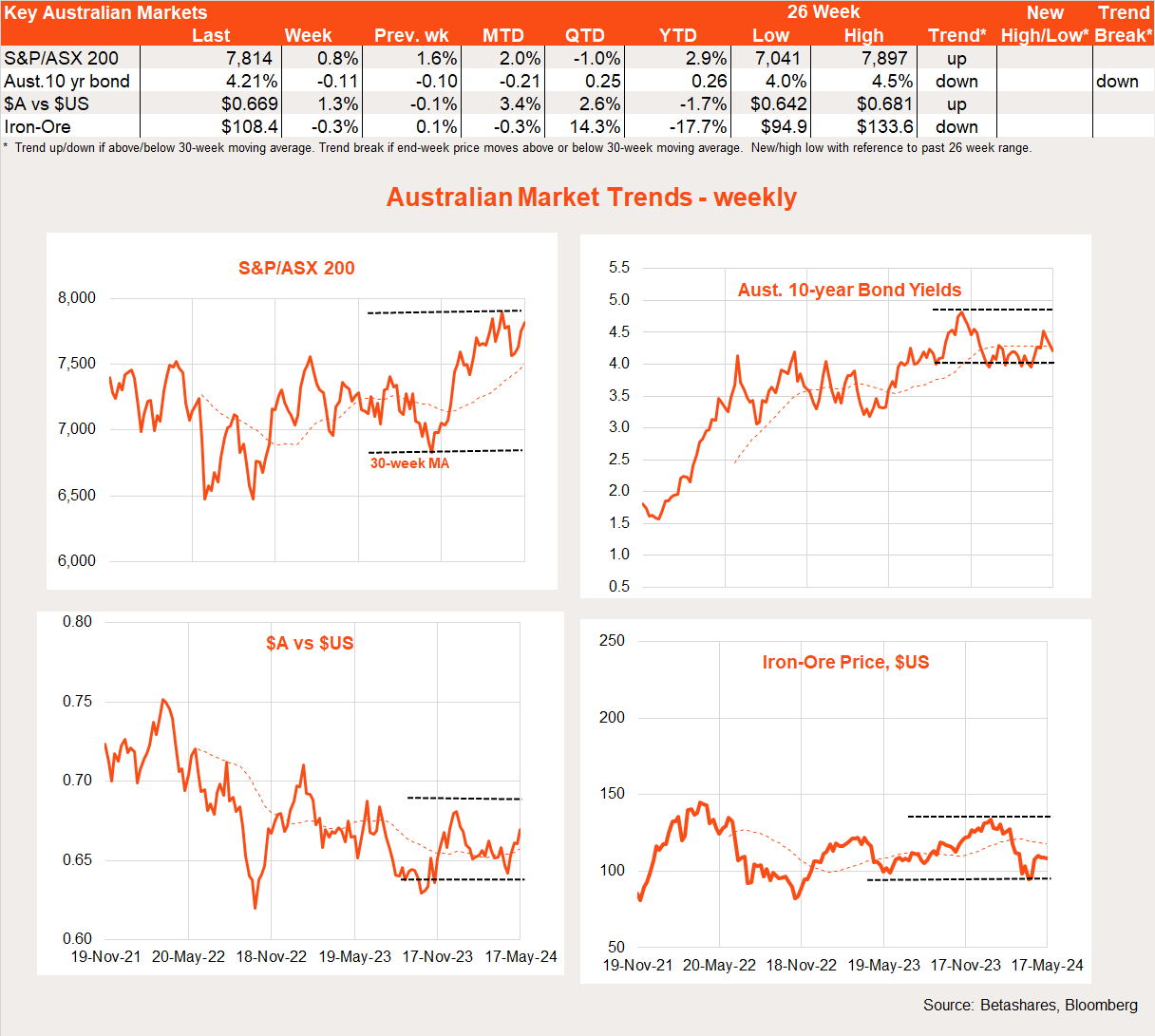

The S&P/ASX 200 lifted a further 0.8% last week, with an expansionary Federal Budget yet softer wage and employment data generally supporting the view that the RBA won’t need to raises rates again any time soon.

The main local highlight was the Federal Budget, with its key feature being rental and electricity cost of living relief structured in a way so as to lower CPI inflation by around 0.5% over the coming year. At the same time, the Budget contained significant new spending, resulting in an overall mixed impact on the interest rate outlook.

The big question for the coming year is how much of the anticipated solid 3.5% rebound in real household disposable income over the coming financial year will be spent or saved by households. Both Treasury and RBA anticipate a good chunk will be saved – with consumer spending only expected to rise by 2%. If consumers instead start to spend up, the economy could end up stronger than expected – which could be nice for corporate earnings though less so for the interest rate outlook and equity valuations.

Of course, the spending proclivities of households will also depend on the labour market. Last week we learnt that overall wage growth is starting to slow, with annual growth in the wage price index easing to 4.1% in the March quarter from 4.2%. Despite a solid 38K gain in employment, the unemployment rate also bounced back to 4.1% – suggesting the economy is slowly losing its ability to find jobs for the ongoing influx of new workers.

We’ll learn how households feel about the Budget with the Westpac/Melbourne Institute consumer sentiment report tomorrow. Also tomorrow will be minutes to the RBA’s last policy meeting – which should confirm the Bank at least had a rate hike (along with rates on hold) among its two policy options debated, though the former was likely not seriously considered.

Have a great week!

2 comments on this

Noted “a patient Fed chair Jerome Powell further reassured markets that the next move in US rates would likely be down”. This statement is completely contradictory on what is being reported worldwide… Let us all see what happens in September.

Council Rates, Fuel, Supermarket food, Meat, Fish, Electricity daily charge keeps rising. Servicing my car just got more expensive, clothing, hardware, building supplies, electrical supplies, plumbing supplies, car tyres, Everything is rising out of control, How, Oh How is inflation coming down, Please give us an example on how our lowering inflation is reducing our cost of living. You simply cannot.