All in on AI? 3 ways to reduce concentration risk

David Bassanese

4 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

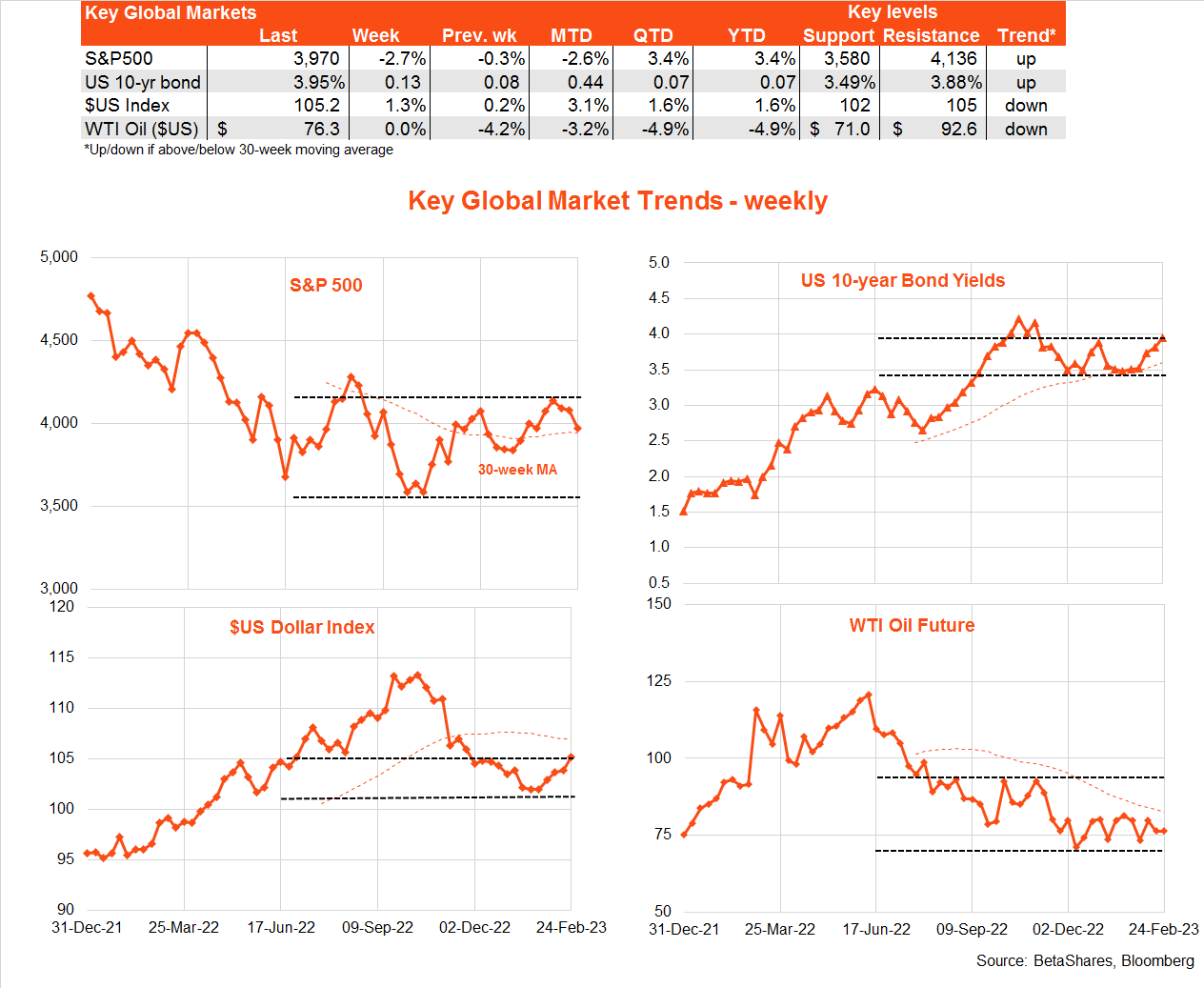

Global Markets

Stronger than expected activity data and stubbornly high consumer price inflation saw US stocks fall and bond yields rise for the third week in a row. Firm recent US activity and inflation data have markets fretting over a potential “no landing” economic scenario in which the Fed is forced to jack rates up even higher to slow the economy and bring down inflation.

A strong US S&P service sector reading for February, which also revealed a lift in price pressure, unnerved market sentiment last week. That was followed by hawkish Fed minutes which gave no hint at a pause in the rate hike cycle anytime soon – indeed, there was strong consensus behind another, but smaller, rate hike of 0.25% last month, though some Fed members wanted to continue with 0.5% hikes.

But the “coup de grâce” for souring market sentiment was Friday’s higher-than-expected core private consumption deflator. Excluding food and energy, core consumer prices rose 0.6%, compared with the already-elevated 0.4% market expectation. Excluding housing, core services (or the newly dubbed “super core” measure of inflation) also rose 0.6% in January, after a 0.4% gain in December. Also on Friday, it was reported that consumer spending rose a blistering 1.8% in January.

Despite solid consumer spending, both Walmart and Home Depot – two major US retailers – issued sombre sales outlooks when revealing their Q4 reports last week. This is in part because households are switching from COVID related goods purchases back to services.

Against this backdrop of “good news is bad news”, Wall Street will nervously await the key US ISM February manufacturing and services sector surveys on Wednesday and Friday respectively. As noted above, the already reported S&P February service sector survey was strong. A further rebound in US consumer confidence is also expected on Tuesday.

Also of interest this week will be Chinese manufacturing and service sector surveys for February – due on Wednesday – which are expected to confirm hopes of an ongoing rebound in the Chinese economy following the end of COVID restrictions.

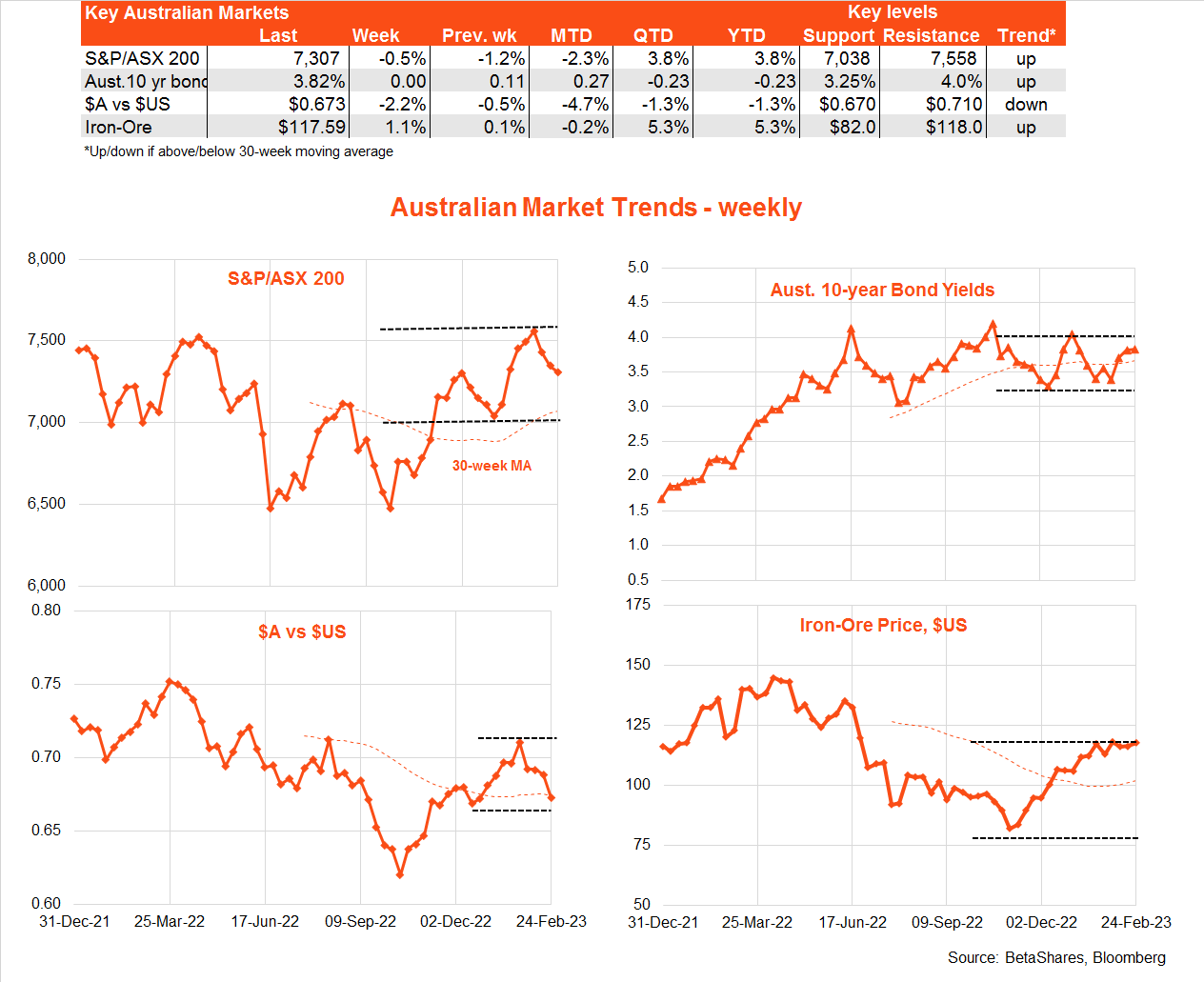

Australia

The major local highlight last week was the softer than expected Q4 wage price index, which threw a little cold water over the RBA’s concern that tight labour markets were already leading to run-away wage inflation. Instead, the WPI rose 0.8% in the quarter (versus market expected of a 1% gain) and 3.3% over the year.

Other activity data were mixed, with weak Q4 construction activity (held down by housing), though business capital spending was somewhat stronger than expected.

In line with Wall Street, local stocks fell last week, though 10-year bond yields – reflecting soft local wage data – ended the week steady. The AU$, however, had a notable fall reflecting US$ strength and softer local data.

Key highlights this week include Q4 GDP and the monthly CPI report for January – both on Wednesday. Underpinned by solid consumer spending (especially on services), GDP is expected to rise a moderate 0.7%, with annual growth slowing from 5.9% to 2.7%. Annual growth in the monthly CPI is expected to slow from 8.4% to 8%.

Also of interest will be the extent of the bounce in January retail sales on Tuesday, following the much larger than expected 3.9% drop in December. The market anticipates a feisty 1.5% rebound, though this would still be consistent with some slowing in the underlying momentum of retail spending in recent months (though in part, likely reflecting a switch toward non-retail services).

All up, however, nothing this week is likely to see the RBA back away from another 0.25% rate hike next week. My base case remains that there will be a final rate hike in April, though resilient consumer spending and/or a surprise bounce in house prices at the hint of an RBA pause could see the Bank push ahead with further rates hikes beyond April. Indeed, markets now reckon the Fed will hike rates at least three more times – which would increase the odds of an eventual hard landing.

Have a great week!

1 comment on this

We hear a lot about wage rises fueling inflation. They probably do to some extent, but they are not the main drivers of current Aus inflation. Our inflation is primarily caused by external factors (war, oil prices, air/sea transport problems, material and labour shortages, etc) which the RBA and Aus government have no control over.

However a local factor which can be moderated (but, so far, is not), is profiteering and price-gouging by some businesses. Many are reporting record (abnormaly high) profits from increasing income, derived from excessively higher prices. There are plenty of examples .. energy and mining companies being prime examples.

Some government response is called for.