Tom Wickenden

5 minutes reading time

This information is for the use of licensed financial advisers and other wholesale clients only.

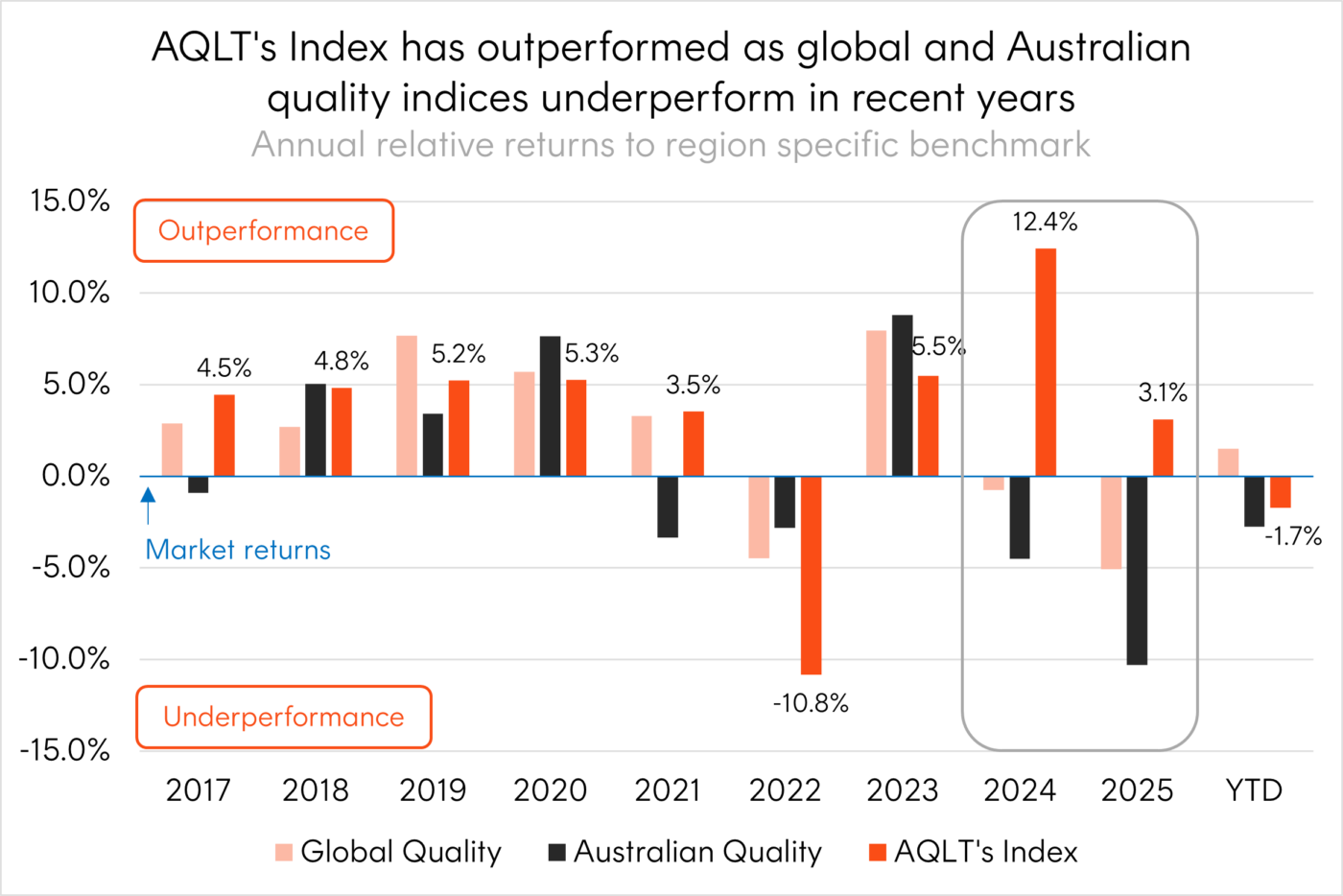

As the quality factor globally and standard quality indices in Australia suffer a period of underperformance, the approach behind AQLT Australian Quality ETF once again stands out.

Through 2024 and 2025, the MSCI World Quality and MSCI Australia Quality indices underperformed the MSCI World and S&P/ASX 200 by 5.9% and 14.8% respectively1.

Globally, strong returns from a small cohort of mega-cap companies followed by a rotation into value orientated regions and sectors has seen quality indices underperform broad market benchmarks.

In Australia strong returns from some companies in the financial and materials sectors have not been captured by standard quality indices, like the MSCI Australia Quality index, leading it to lag the market during periods of cyclical market leadership.

Source: Bloomberg. Annual returns from 2017 to 2025 and year to date returns from 31 Dec 2025 to 27 Feb 2026. AQLT’s index is the Solactive Australia Quality Select Index and benchmarked to the S&P/ASX 200. Global Quality represented by the MSCI World Quality Index and benchmarked to the MSCI World Index. Australian Quality represented by the MSCI Australia Quality Index and benchmarked to the S&P/ASX 200. You cannot invest directly in an index. Past performance is not an indicator of future performance.

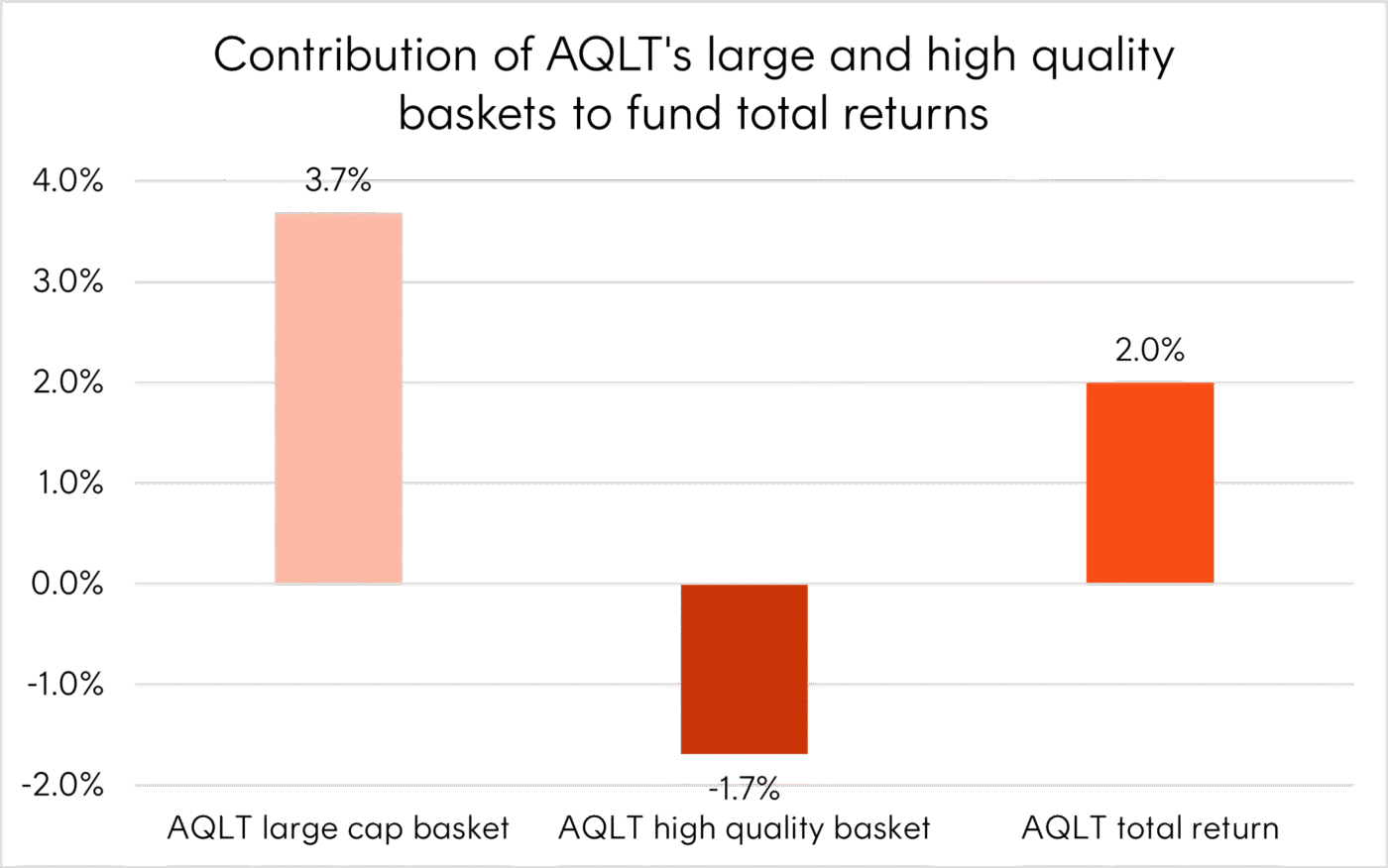

In constructing AQLT’s index we considered the fact that Australia’s market has inherently cyclical large caps and experiences periods of returns driven by these companies which are not considered high quality based on their fundamentals.

To overcome this challenge, AQLT still holds Australia’s largest companies, by market capitalisation, listed on the ASX and reweights them by their quality metrics. These include Australia’s ‘Big Four’ banks, along with cyclical resource companies like BHP and Woodside. The remainder of AQLT’s 40 stock portfolio is made up of the highest quality companies on the ASX.

Year to date, as Australia’s large cap banks and materials companies have outperformed, AQLT’s large cap basket has more than offset the underperformance of AQLT’s high quality basket2. High quality companies in Australia suffered from a volatile corporate reporting season as earnings were scrutinised and valuations came into question – particularly for software-based technology companies.

Source: Bloomberg. 31 Dec 2025 to 27 Feb 2026. Returns of Betashares Australian Quality ETF net of fees. performance is not an indicator of future performance.

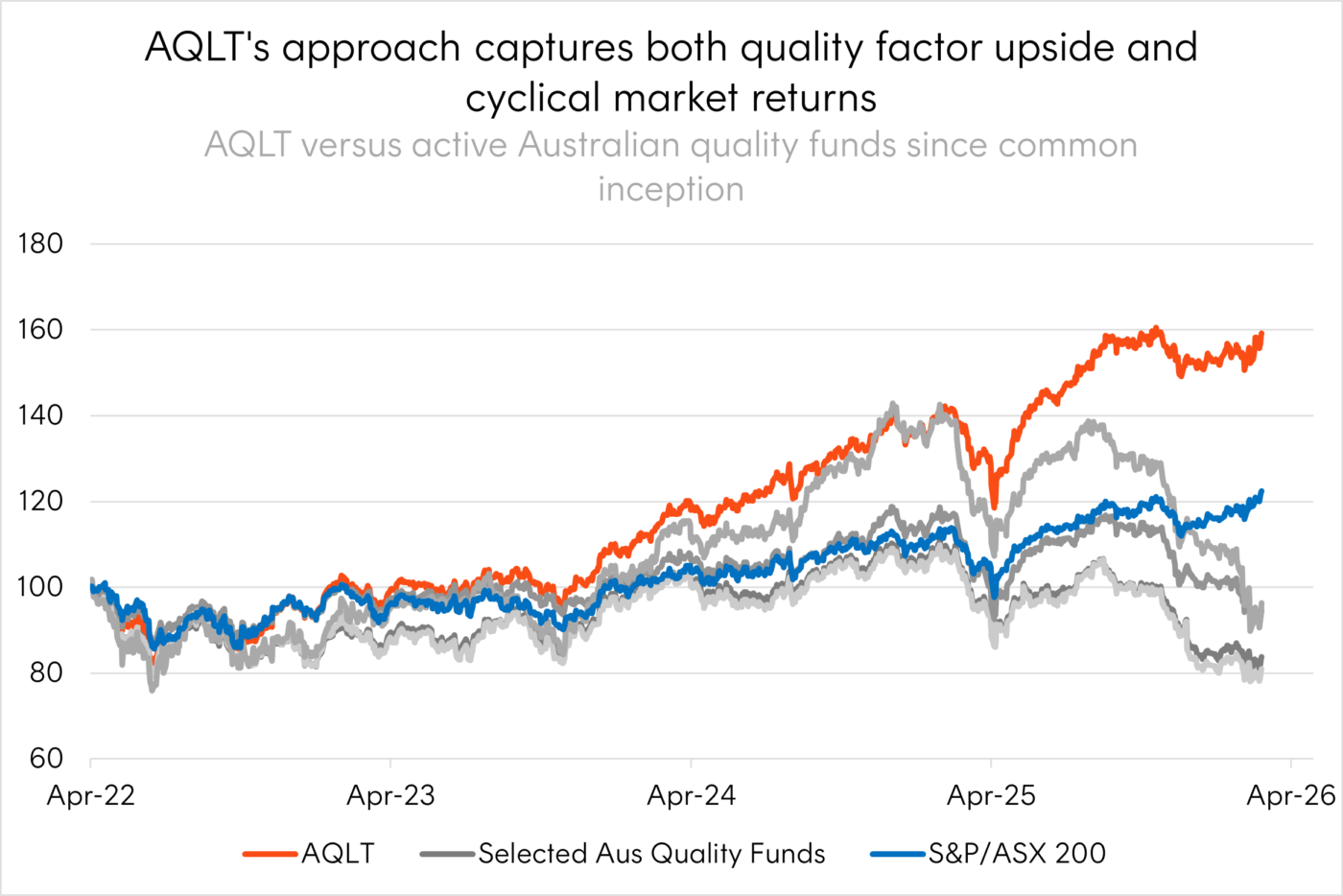

In this environment active Australian managers with a quality investing focus suffered a material drawdown driven by more concentrated positions.

Not only did AQLT’s approach capture upside similar to these funds during prior years when the quality factor was outperforming but it also protected investors from their recent downside as quality companies sold off. These factors have driven AQLT to outperform these funds and the S&P/ASX 200 since common inception3.

Source: Bloomberg. 4 Apr 2022 to 27 Feb 2026. Aus Quality Fund’ selected as the cohort of Australian active managers in the Morningstar large blend category with a high tilt to the quality factor – as determined by Morningstar Direct. Past performance is not an indicator of future performance.

Given its thoughtful construction AQLT can serve as the core of investor portfolios – balancing an allocation to Australia’s largest companies, re-weighted by their quality attributes, with a mix of Australia’s highest quality mid-caps.

AQLT is used as a core building block in Betashares Dynamic Managed Accounts blended with other select Australian smart beta ETFs with the aim of outperforming the broader market and improving risk adjusted returns.

Since its inception on 4 April 2022 AQLT has outperformed the S&P/ASX 200 by, on average, 3.4% p.a.4

You can find out more information about AQLT on the fund page here.

Sources:

1. Source: Bloomberg. 31 December 2023 to 31 December 2025. You cannot invest directly in an index. Past performance is not an indicator of future performance. ↑

2. Source: Bloomberg. 31 December 2025 to 27 Feb 2026. ↑

3. Source: Bloomberg. 4 Apr 2022 to 27 Feb 2026. Aus Quality Fund’s selected as the cohort of Australian active managers in the Morningstar large blend category with a high tilt to the quality factor – as determined by Morningstar Direct. Past performance is not an indicator of future performance. ↑

4. As at 27 Feb 2026. Past performance is not an indicator of future performance. ↑