Hugh Lam

5 minutes reading time

Last Friday, the US Supreme Court ruled President Trump’s tariffs illegal, exceeding his authority under the 1977 International Emergency Economic Powers Act (IEEPA). Within hours of the ruling, Trump announced a 10% global tariff which would then be followed by an increase to 15% over the weekend.

With global trade under renewed uncertainty, US equity indices may face yet another challenge after the launch of new AI tools saw billions of dollars lost across software stocks earlier in the month.

As investors continue to assess which business models will prove most resilient to AI adoption, many are prudently looking for global equity diversification. Markets outside of the US such as Australia, Japan and Europe have all enjoyed solid gains year to date.

In this edition of Charts of the month, we take a look at the impact of potential tariff refunds, the rotation occurring within US tech and the Australian share market, why currency matters when investing in Japan, and the recent surge in German defence spending.

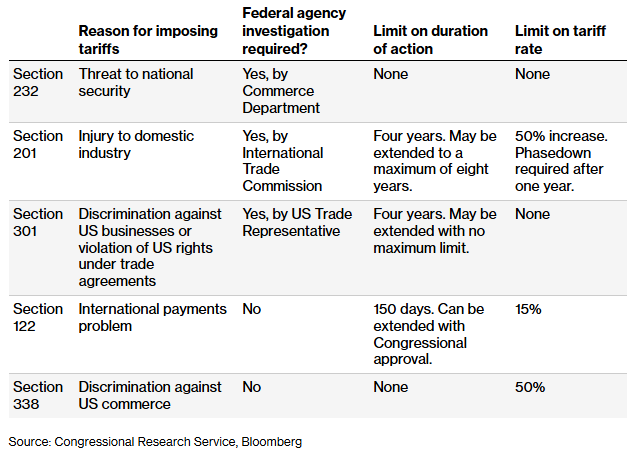

1 – US Supreme Court decision restokes global trade tensions

More than US$175 billion in US tariff collections are subject to refunds after the US Supreme Court ruled President Trump’s tariffs imposed under IEEPA unlawful. While Trump has used other legal pretexts to reinstitute a 15% across the board tariff, the Supreme Court’s ruling has effectively dealt a blow to Trump’s tariff strategy.

Even with alternative options available, the latest lift in tariffs requires Congressional approval within five months where Republicans currently hold a narrow majority.

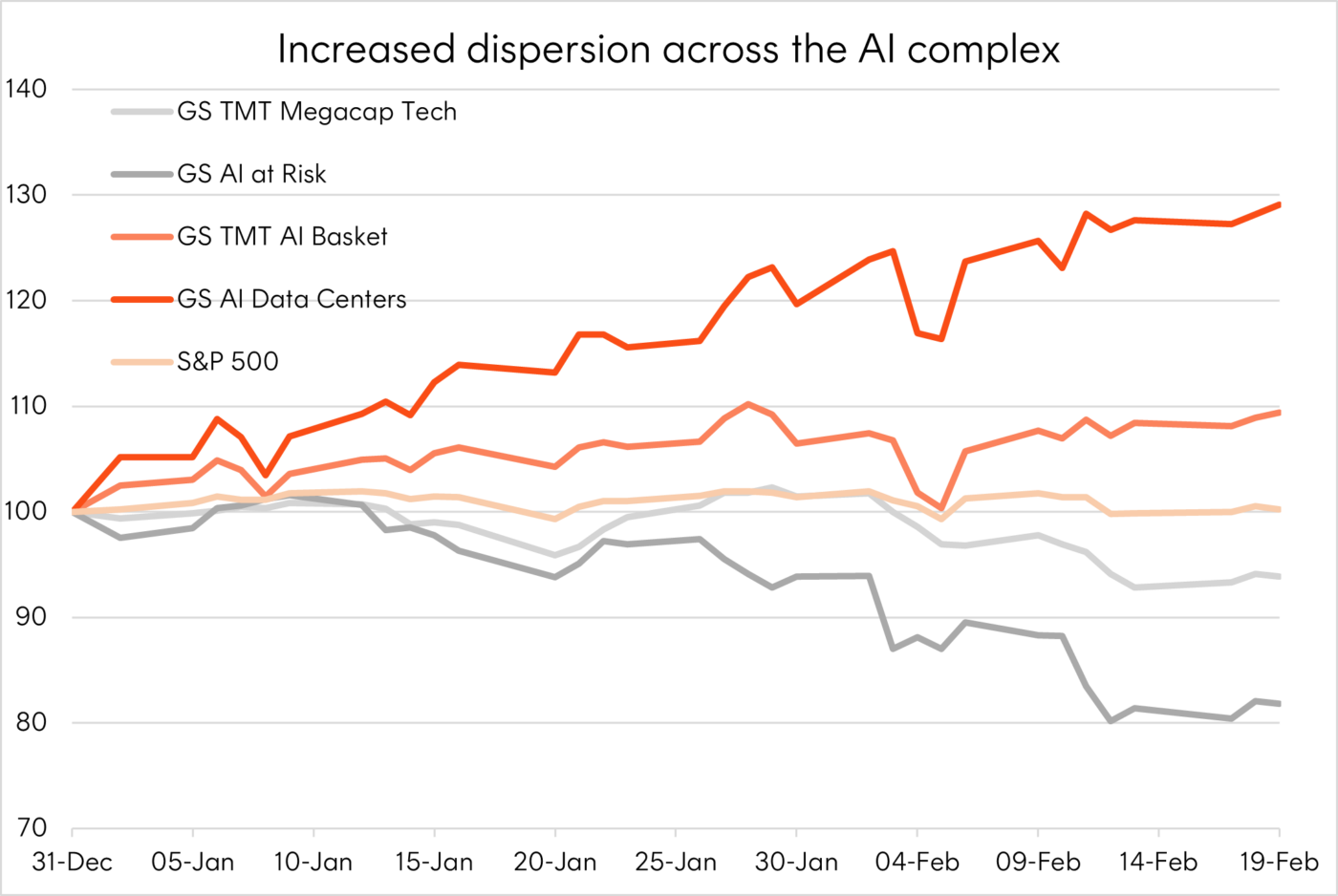

2 – Is SaaS trash?

Source: Goldman Sachs. As at 19 February 2026. Rebased to 100 as at 31 Dec 2025.

After years of gains, the backdrop for AI-related themes has become more challenging this year, with fears of rising hyperscaler capex projections and the disruption to software providers weighing on the broader tech sector.

But underneath the surface, there have been significant shifts in winners and losers.

Companies tied to the physical infrastructure (e.g., data centres, chip manufacturing) of the AI boom have become net beneficiaries relative to the broader software sector given their more insulated positions further up the supply chain, and stronger pricing power abilities. In comparison, the software sector has sold off considerably with investors reassessing commoditised categories in particular.

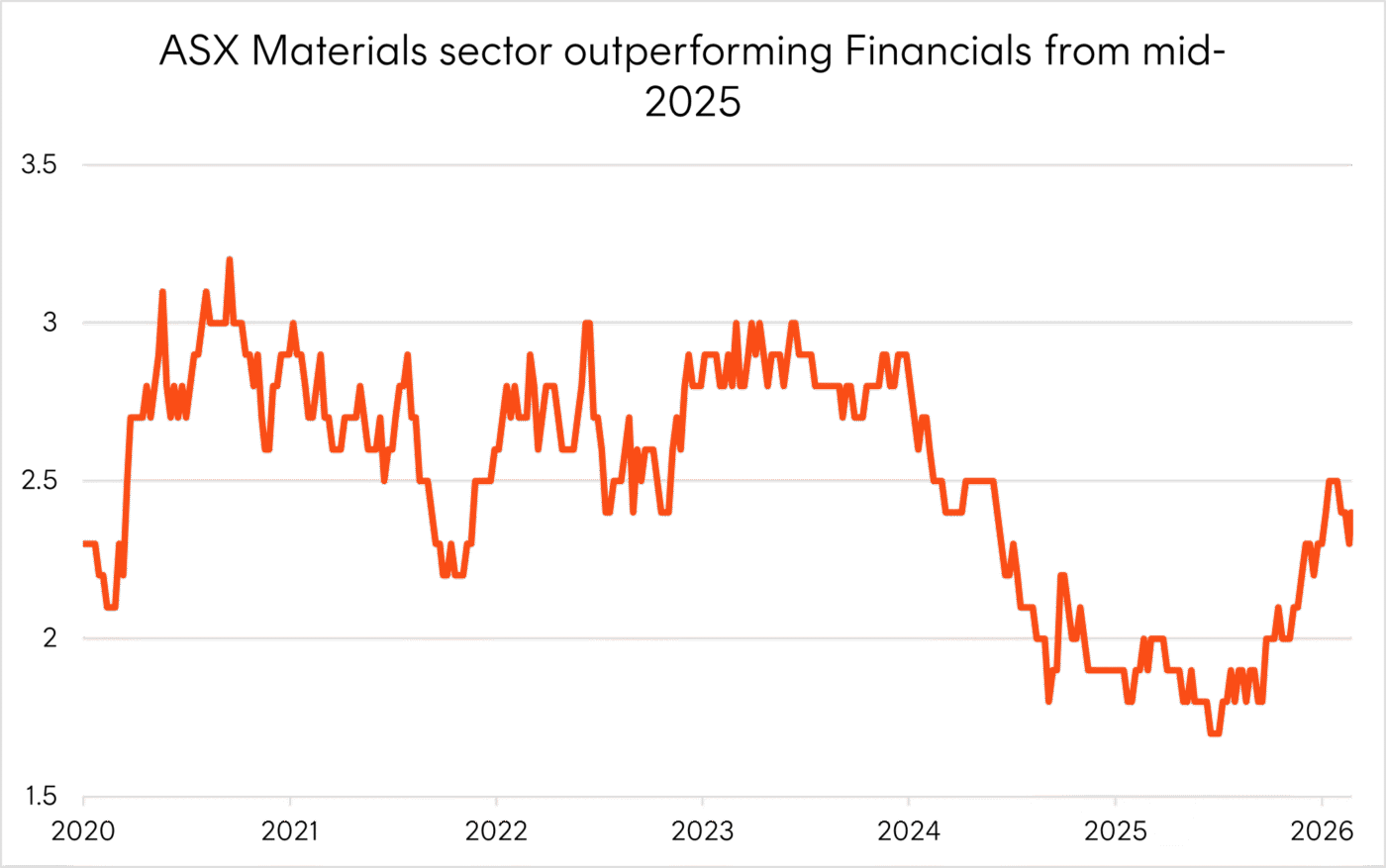

3 – Changing of the guard to drive Australian large caps forward

Source: Bloomberg. As at 23 February 2026. Series shows S&P/ASX 200 Materials sector divided by S&P/ASX 200 Financials sector from 1 January 2020 to 23 February 2026. Past performance is not an indicator of future performance. You cannot invest directly in an index.

In our view, the Materials sector is expected to drive Australian large-cap returns in 2026, underpinned by robust commodity demand and superior earnings growth projections. Companies in this sector have benefited from higher gold, copper and lithium prices. China’s exit from deflation and infrastructure stimulus could further boost demand for these metals, positioning Materials for leadership this year.

While Financials earnings expectations remain solid at 6.9% for FY2026, we see meaningfully greater upside in Materials given their earnings inflection from -18.0% in FY25 to 19.4% in FY261.

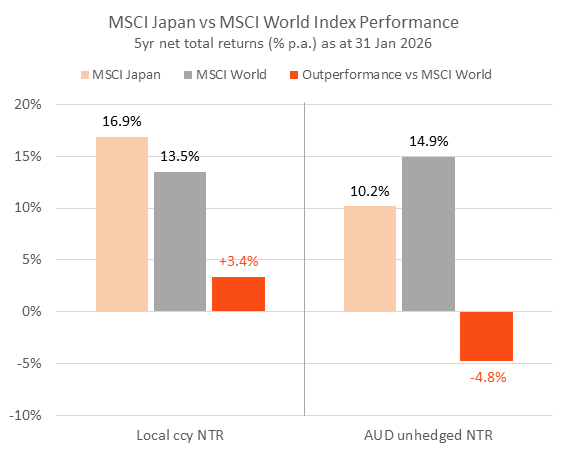

4 – A new dawn in the land of the rising sun

Source: Bloomberg. As at 31 January 2026.

Prime Minister Takaichi’s landslide victory in the recent lower house elections — the largest in Japan’s post-war history — gives her government the green light to push through further structural reforms and fiscal stimulus largely unobstructed. For Japanese equities, this is broadly positive, although less so for the yen.

Against this backdrop, a currency hedged Japanese equities exposure like the HJPN Japan Currency Hedged ETF may be a compelling exposure for investors. HJPN seeks to provide exposure to a portfolio of large Japanese exporters with the currency risk hedged back to Australian dollars, allowing investors to capture the Japanese equity story without the drag of unhedged yen exposure.

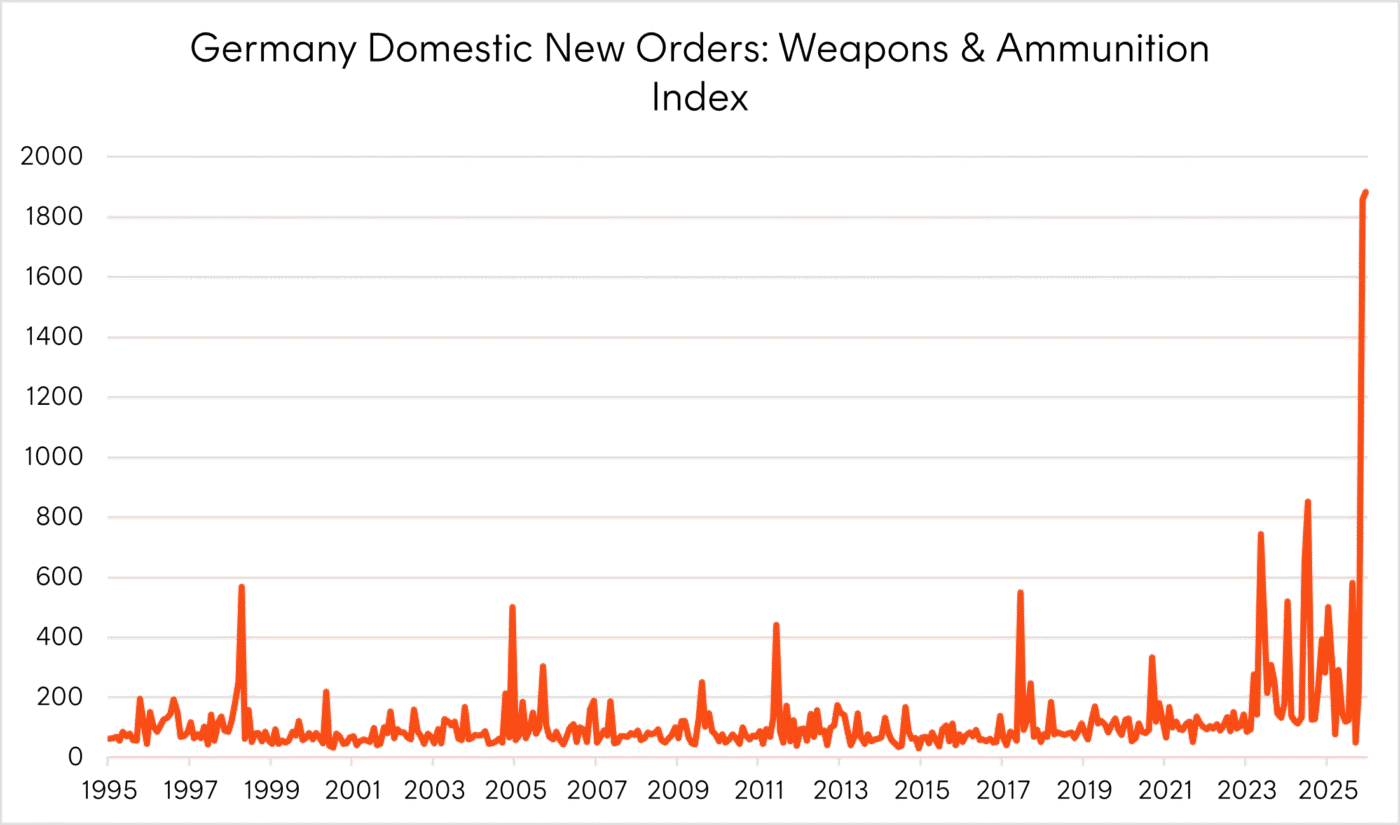

5 – German defence spending on the march

Source: BCA Research.

Germany has committed to substantial defence spending increases in 2026, approved by the Bundestag in late 2025, amid NATO goals and escalating geopolitical threats.

The 2026 regular defence budget stands at approximately €83 billion2, up significantly from 2025 levels (around €63 billion). Including the special Bundeswehr fund, total spending reaches over €108 billion, funding weapons systems, infrastructure, and up to 10,000 additional personnel.

This positions Germany to exceed NATO’s 2% GDP target early, aiming for 3.5% by 20293 — six years ahead of schedule — with projections rising to €152 billion annually by then4. Debt brake exemptions enable borrowing for defence, part of a broader €500+ billion federal budget.

Footnotes:

1. Source: Refinitiv. As at 13 January 2026. ↑

2. https://atlasinstitute.org/germanys-path-to-kriegstuchtigkeit-the-2026-defence-budget/ ↑

3. https://nordicdefencereview.com/germanys-historic-military-expansion-e83-billion-defence-budget-for-2026 ↑

4. https://www.dsei.co.uk/news/german-parliament-approves-2026-defence-budget ↑