David Bassanese

7 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the below player:

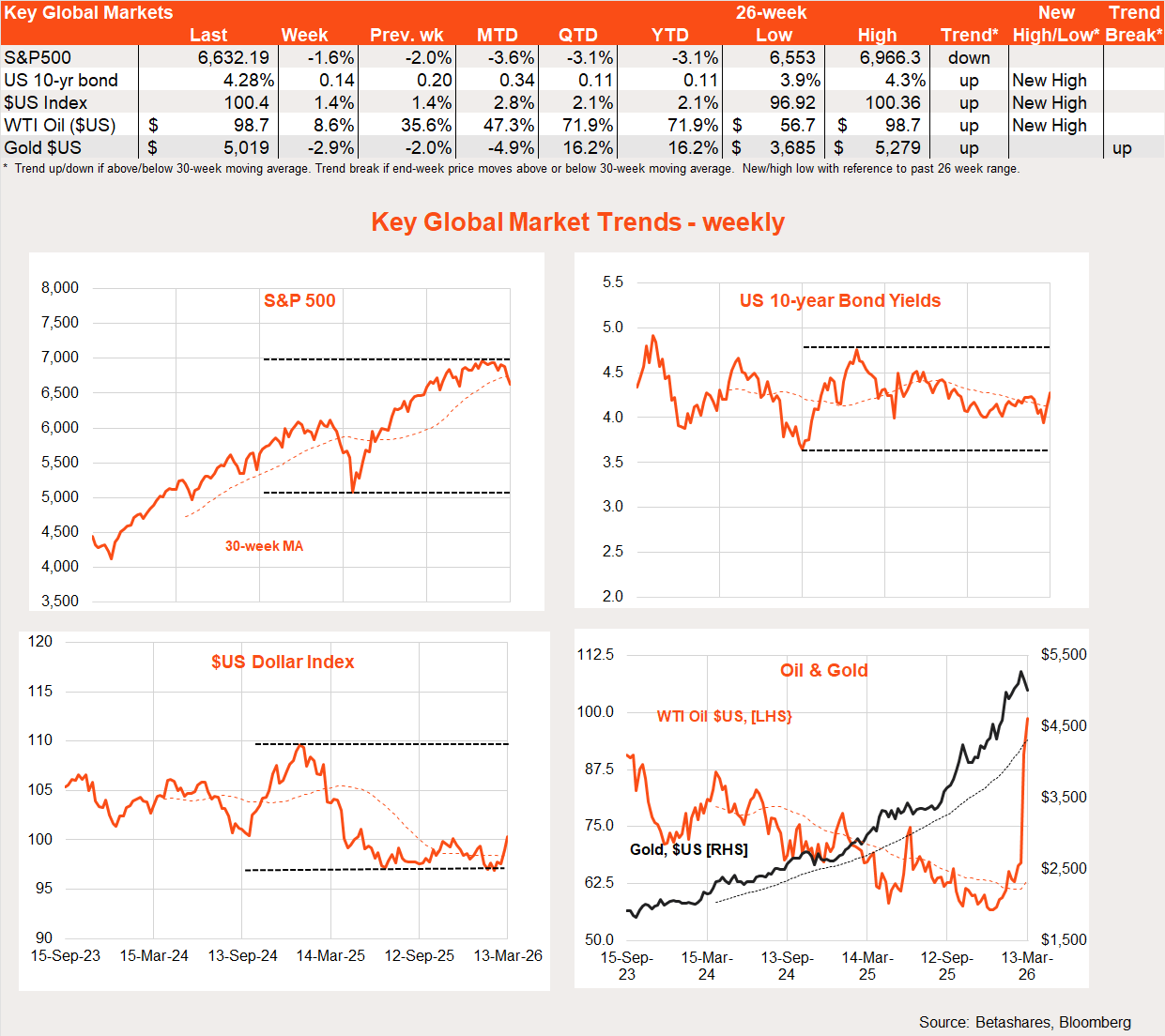

Global stocks continued to weaken last week, as the ongoing war in Iran kept oil prices high.

Global week in review: stalemate

Global stocks remained under pressure last week, with the Iran war pushing oil prices higher. Despite extensive bombing, the Iranian regime remains in place and the conflict has effectively blocked the Strait of Hormuz.

With equities down and bond yields up, pressure is seemingly mounting on US President Donald Trump to declare victory and walk away. Markets thought the TACO (‘Trump Always Chickens Out’) moment had come early last week when Trump declared the war was “very complete, pretty much”. But like the Iranians, he then spent the rest of the week digging in, with Iranian taunts on social media hardly helping if he was looking for a face-saving exit.

Meanwhile, the International Energy Agency’s (IEA) announcement of the largest ever release of strategic oil reserves (400 million barrels) helped calm markets momentarily – until investors realised that this only amounts to an incremental 1-2 million barrel per day (mb/d) increase in the flow of new supply available. For context, Iran’s blockage of the Strait of Hormuz is blocking up to 15 mb/d of oil supply.

The US’ promise to offer naval protection for ships daring to cross the Strait has also come to naught so far, with officials conceding it’s still not safe enough to try. By the weekend, Trump was left pleading for international naval support, although the response so far has been tepid.

So far, however, the disruption to oil supply is only short-term and could be resolved very quickly if hostilities ceased and the Strait was reopened. But the US bombing of Iran’s Kharg Island, through which most of Iran’s oil exports flow, represents a much more serious risk. Although the US has, so far at least, not bombed Iran’s oil processing facilities, it has indicated that it might.

Were it to do so, Iran has threatened to attack oil facilities across the Middle East in turn, which would lead to a more enduring disruption to oil production and supply.

We are left waiting for a solution. A negotiated settlement remains the great hope, but it’s less clear that the seemingly emboldened Iranian regime would accept terms that demanded an end to its nuclear activities. If it only stopped taunting Trump on social media, he might – as I suggested last week – ‘do a Greenland’ (claim victory and walk away).

In other news, both key measures of US inflation came in line with market expectations. At 3.1%, however, annual growth in the core personal consumption expenditure deflator (PCED) remains uncomfortably high, even before the expected flow-through of higher energy costs.

Global week ahead: Iran & the Fed

The coming week will again be dominated by the Iran conflict. Who will blink first and will it happen as early as this week? Markets are hoping for their TACO.

The US Federal Reserve also meets this week, but rates are expected to remain firmly on hold.

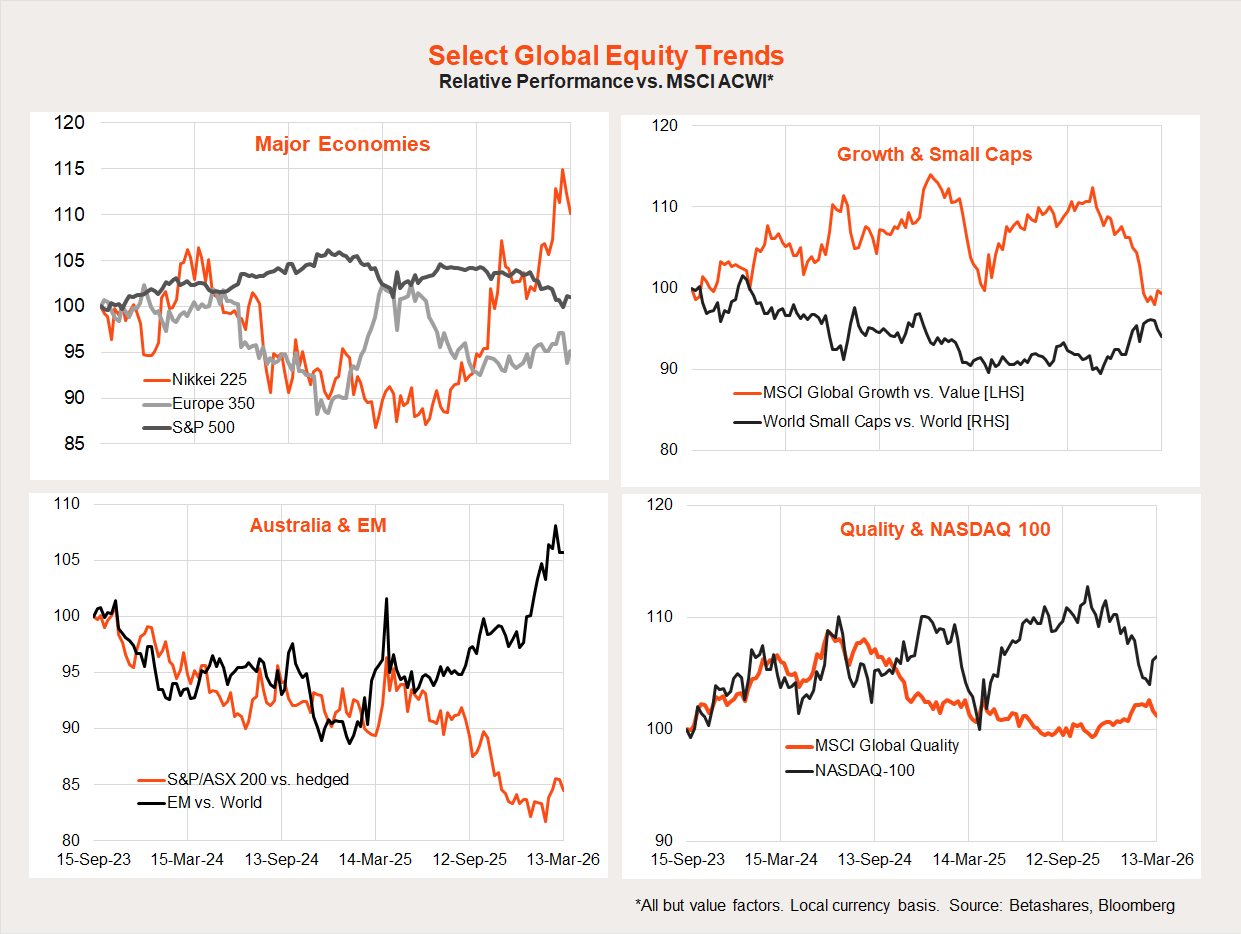

Global equity trends: the great rotation continues

The MSCI All-Country World Equity Index dropped 1.4% last week, modestly outperforming the S&P 500’s drop of 1.6%. Recent position squaring likely accounts for heavier falls among recent popular trades, such as Japan, although this does not necessarily suggest a shift in the underlying trends.

As we saw in 2022, if a global energy shock plays out, there may be a further rotation from interest rate-sensitive cyclical and technology sectors into more value-orientated defensives and resources.

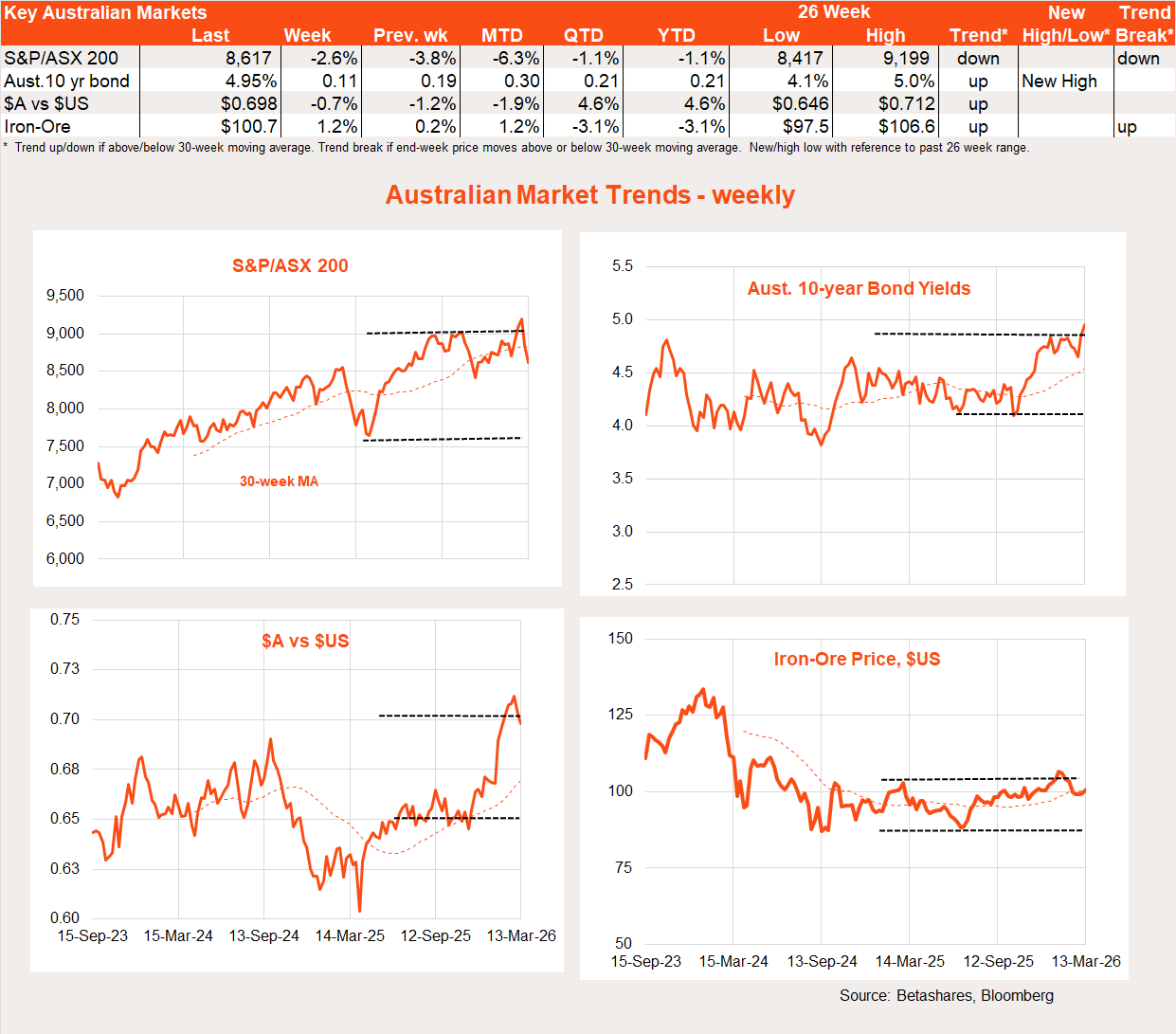

Australian week in review: RBA speak

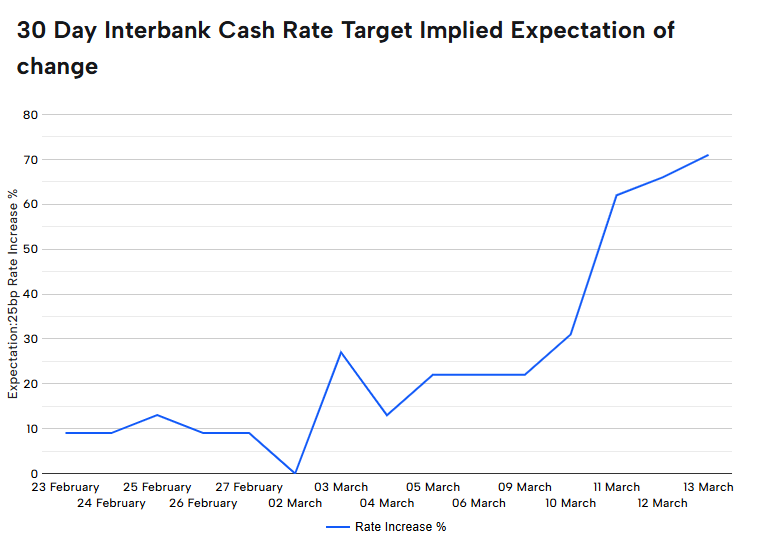

The major local highlight last week was further hawkish commentary from the Reserve Bank which has left the market all but convinced of a rate hike this week.

Following on from RBA Governor Michele Bullock’s warning two weeks ago that the March meeting was “live”, we got further comments from Deputy Governor Andrew Hauser last week emphasising upside inflation risks from the energy price spike and war in Iran.

This is interesting for several reasons. If this is “market signalling”, it’s a direct counter to what the Governor pledged last year – namely no more forward guidance which would undermine the role of the newly installed independent RBA board members. If the decision is already made, what’s the point of these people bothering to show up?

Last year, the market was completely blindsided by the RBA’s decision to leave rates on hold. Even if the market was completely wrong in not expecting a March rate hike, why did they warn them this time around?

It is also interesting in that a rate hike would be counter to the general inclination of central banks not to react to supply-side shocks, as they both put upward pressure on near-term inflation but pose downside risks to economic growth.

As seen in the chart below, the market probability of a rate hike this week has lifted from near-zero to 70% over the past month.

Source: ASX

In other news, consumer confidence actually lifted a little in March despite rate hike fears, likely reflecting labour market strength. The NAB measure of business conditions also held steady at around long-run average levels. In short, neither was weak enough to dent the chances of a rate hike this week.

Australian week ahead: RBA to hike

Although my long-held inclination has been that the RBA would hold rates steady this month and hike again in May (after the late-April Q1 CPI), it’s hard to ignore recent RBA signalling.

It seems the view of RBA officials is to hike this week, with the upside energy price risks arising from the war in Iran adding to their existing angst over the inflation outlook against the backdrop of a still-firm economy.

Indeed, although energy price shocks have mixed effects on the economy, with the labour market already tight and inflation high the RBA appears to be focusing more on the added upside inflation risks than the downside risks to growth. To the extent higher energy prices hurt economic growth, the RBA would likely judge that to be a good thing given the current circumstances.

Also arguing for a rate hike this week is the fact that the next meeting is not until May. Were there an April meeting, as was usual before recent changes, the RBA might have been more willing to wait a little longer and see how the Iran war plays out.

Of course, a rate hike will still depend on what other board members think – some may push back on what is likely to be an RBA recommendation to hike rates.

All up, my call is the RBA will hike rates this week. I also expect a follow up hike in May, to truly squeeze down on the economy and hopefully have inflation easing later this year. Indeed, it’s not out of the question that the RBA could hike twice more this year and be cutting rates again by November or December!

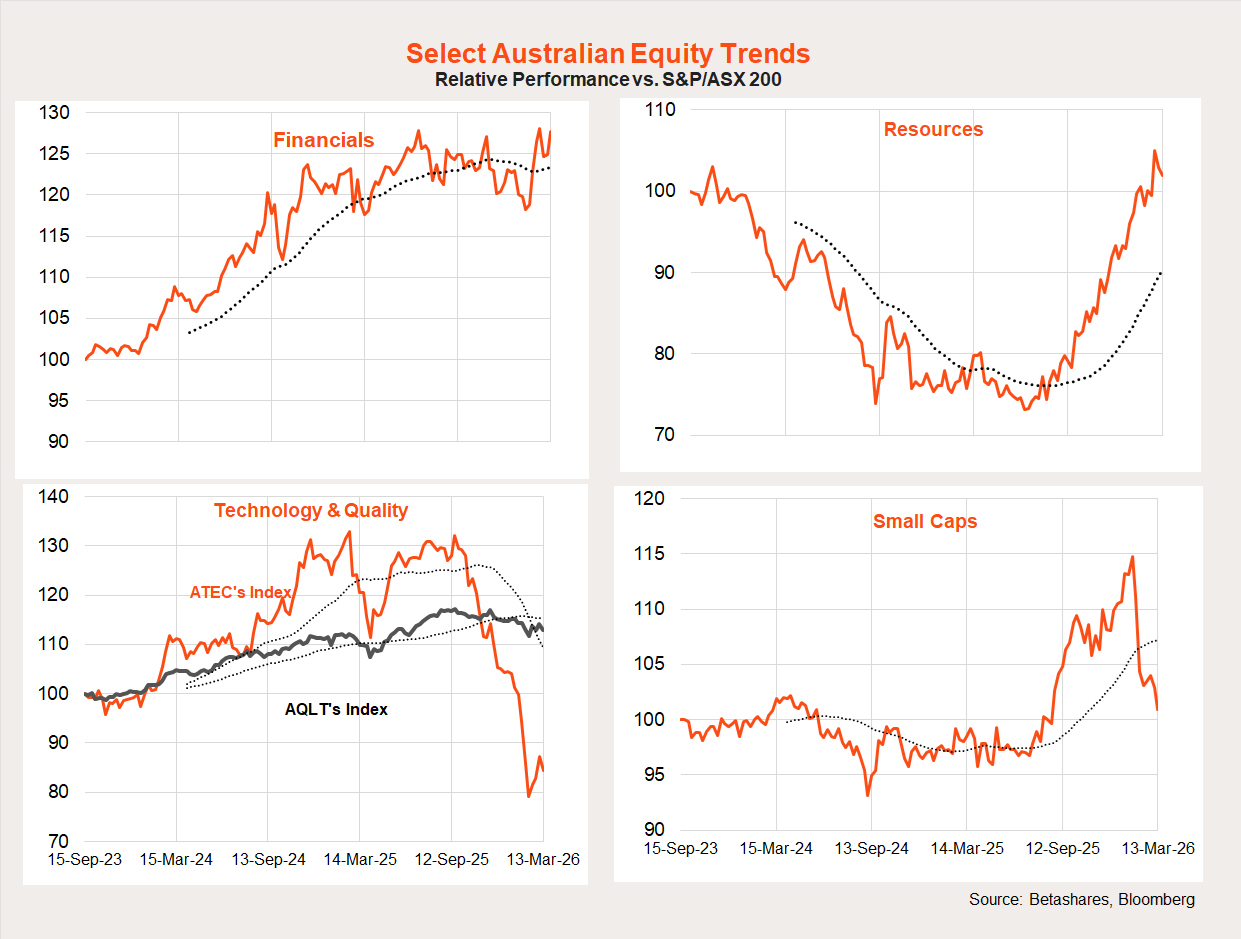

Australian equity trends

Materials were again a major loser on the Australian market last week, declining 4.7% while the energy sector rose a further 1.8%. Technology moved back into the red though, declining by 6.9%.

Given position squaring, the Iran war will naturally play havoc with recent trends over the short run, although energy stocks are a clear winner for now.

Have a great week!

1 comment on this

David,

Thanks for your contributions to economic debates. Regarding the expectation that the Reserve Bank will lift interest rates this afternoon, I would like to say that I do not believe that a rise is justified. The petrol price rise is a supply issue and as you say the “general inclination of central banks not to react to supply side shocks”. The measure of inflation for interest rate considerations should not include the impact of supply side shocks. The petrol price rise is itself a dampener on demand by decreasing disposable incomes so what is the justification for an interest rate hike? And what if the price increase is sustained. Why the double whammy. Things are not that much out of control (except for the Iran war and you know who). You say it is “hard to ignore the recent RBA signalling” but I would like to see leading economists like yourself explain why they agree (or disagree) with the Reserve Bank position and/or publicly push back on what may be illogical Reserve Bank signals. Now some signals may have been before the Iran war, but when circumstances change so should the rhetoric and decisions. I will be disappointed if interest rates go up today. Purely academic as I don’t have a mortgage or loans and may benefit from higher interest rates. Just love a debate. Cheers.