Parker Guan

6 minutes reading time

Meeting highlights

- The FOMC voted 11-1 to hold rates unchanged for the second consecutive meeting, citing the “uncertain” impact of the Middle East conflict on the economy.

- The decision saw only 1 dissent, Governor Stephen Miran, who voted for a 25bp cut. Notably, Governor Waller, who was a dissenter at the last meeting, moved in line with the majority camp.

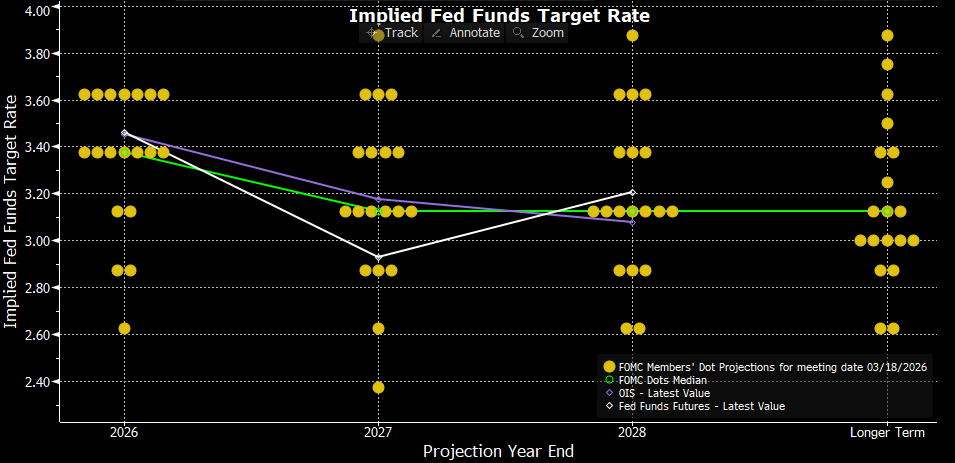

- Updated “Dot-plot” and economic projections:

- The median forecast from the “Dot-plot” still pencils in one cut for 2026 and another for 2027; however, there is at least one member considering a rate hike next year.

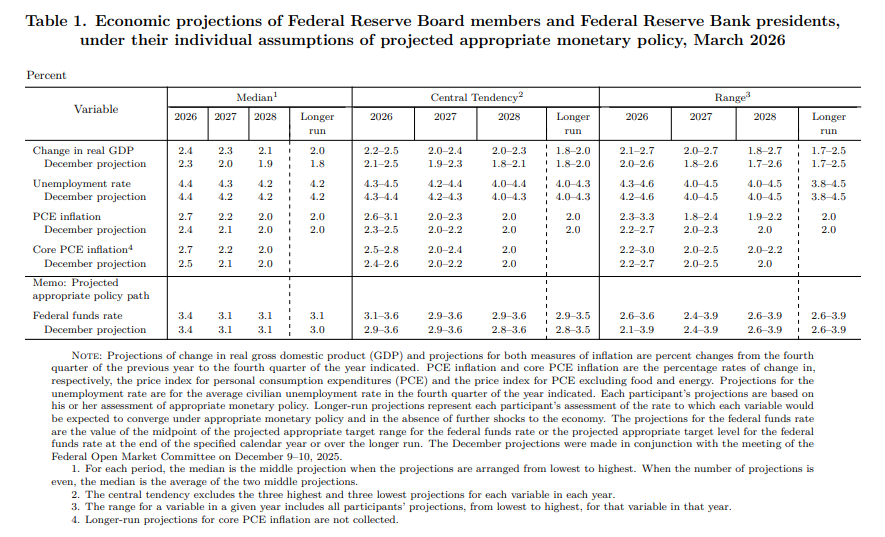

- Inflation: The most noticeable change in the economic projections is that 2026 core PCE inflation was revised up to 2.7% (from 2.5%), reflecting the potential impact of the oil price surge and ongoing tariff effects.

- GDP: The forecast for 2026 GDP growth also increased to 2.4% (from 2.3%), despite the higher inflation forecast and a weaker job market. The basis of the forecast may reflect an assumed productivity gain from AI adoption in the wider economy.

- The terminal rate: The median estimate for the longer-run rate rose to 3.1% (up from 3.0%), the highest in a decade, likely also reflecting possible AI-related productivity gains.

- Notably, the Fed’s view is that inflation is being driven by external shocks, mostly from tariff impacts on goods prices, which the Fed estimated will pass through by mid-2026. With recent weak data in the jobs market, the Fed also removed language around stabilisation and acknowledged that inflation is not coming from wages.

- The Fed avoided making too many comments on the oil shock coming from the Middle East conflict and cautioned about the uncertainty. It is expected that oil prices have caused near-term inflation expectations to rise, but the Fed will likely only look at the second-order effects from higher fuel and energy costs when and if that transmits through the economy.

- Powell confirmed during the press conference that he will serve as “Chairman pro-tem” until a successor is named, ensuring continuity during the ongoing Justice Department investigation into Fed personnel.

Market reaction

Market reaction was “hawkish” to the press conference. While bond and equity prices were already softer to begin the day, 2-year bond yields jumped and equities sold off further as the press conference progressed. Notably, there was a big move when Powell mentioned his ‘Chairman pro tem’ position.

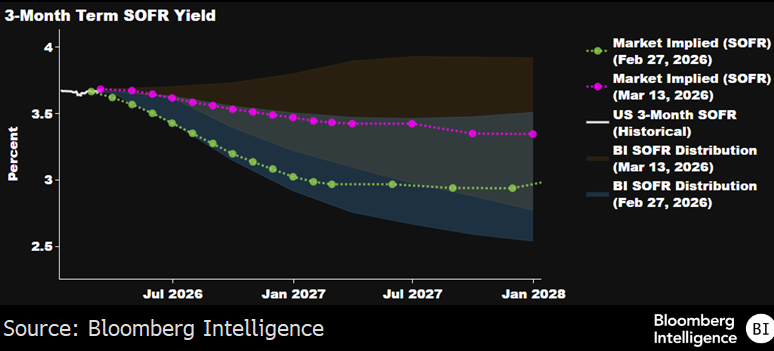

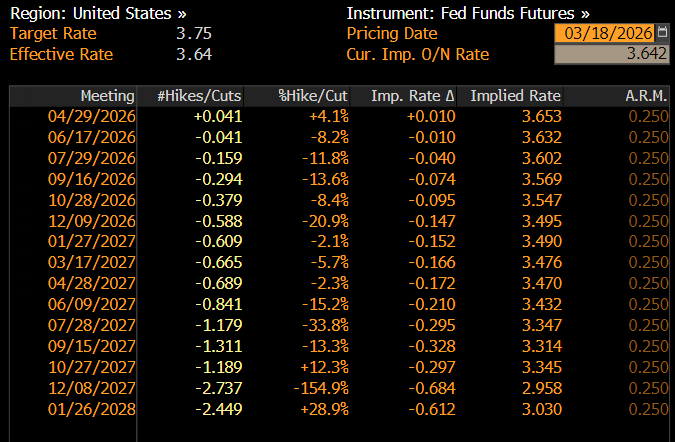

Market pricing for rate-cut probabilities significantly unwound, which is at odds with the Fed’s projections. Before the meeting, Fed funds futures were pricing in around one rate cut this year, but that was pared back further during the press conference, with traders continuing to price in less than one cut this year. By the end of the press conference, December Fed funds futures was implying only around 15bps of easing, with the first full 25bp cut not fully priced until July-2027 (Table 2). The distribution for 3-month SOFR rates also shifted up significantly relative to end-February data, with options markets showing some hedging for a potential rate hike over the next 2 years (Chart 1).

Table 1: Key market movers, as at 18 Mar 2026

|

Equities |

Current level |

Prior close level |

1d change |

Last FOMC (Jan 28) level |

Changes between FOMC meetings |

|

|

SPX Index |

S&P 500 |

6629.57 |

6716.09 |

-1.29% |

6978.03 |

-4.99% |

|

NDQ Index |

NASDAQ |

24419.08 |

24780.42 |

-1.46% |

26022.79 |

-6.16% |

|

XPA Index |

ASX 200 SPI futures |

8545.00 |

8689.00 |

-1.66% |

8956.00 |

-4.59% |

|

RTY Index |

Russell 2000 Index |

2483.76 |

2519.99 |

-1.44% |

2653.55 |

-6.40% |

|

Bonds |

Current level |

Prior close level |

1d change |

Last FOMC |

Changes between FOMC meetings |

|

|

USGG2YR Index |

UST 2-year yield |

3.77 |

3.67 |

10 bps |

3.57 |

20 bps |

|

USGG10YR Index |

UST 10-year yield |

4.26 |

4.20 |

6 bps |

4.24 |

2 bps |

|

USGGT10Y Index |

UST 10-year real yield |

1.84 |

1.81 |

3 bps |

1.88 |

-5 bps |

|

USGGBE10 Index |

UST 10-year inflation breakeven |

2.42 |

2.39 |

3 bps |

2.36 |

7 bps |

|

YMA Comdty |

AU 3y bond futures yield |

4.61 |

4.55 |

7 bps |

4.28 |

33 bps |

|

XMA Comdty |

AU 10y bond futures yield |

4.99 |

4.93 |

5 bps |

4.83 |

15 bps |

|

USOAIGTO Index |

US Investment Grade Credit Spread |

129.01 |

129.57 |

-0.55 bps |

102.39 |

26.62 bps |

|

Commodities & FX |

Current level |

Prior close level |

1d change |

Last FOMC |

Changes between FOMC meetings |

|

|

CL1 Comdty |

WTI Oil |

98.50 |

96.21 |

2.38% |

63.21 |

55.83% |

|

XAU Curncy |

Spot Gold |

4842.35 |

5005.61 |

-3.26% |

5417.21 |

-10.61% |

|

AUDUSD Curncy |

AUDUSD |

0.7036 |

0.7105 |

-0.97% |

0.7041 |

-0.07% |

|

XBTUSD Curncy |

Bitcoin |

71058.56 |

74540.10 |

-4.67% |

89277.17 |

-20.41% |

|

VIX Index |

VIX |

24.41 |

22.37 |

2.04 |

16.35 |

8.06 |

Chart 1: SOFR Options 30-70% Implied Probabilities vs. Spot

Source: Bloomberg Intelligence

Betashares Fixed Income Desk comments

In terms of the meeting outcome, this was an uneventful meeting in our view. However, we were able to confirm a few views from the Fed, especially around its economic forecasts and how it thinks about the uncertainty surrounding the conflict in the Middle East.

What’s interesting about the economic forecast is that both inflation and economic growth have been revised up from last year, while the labour market is expected to remain stable. Given the near-term oil shock and uncertainty around tariffs, the forecast feels too optimistic under a conventional framework. The missing piece may be AI-related productivity gains. Various Fed members have been in the media talking about AI, and now we can see that the Fed may be incorporating that aspect into its economic projections. This is likely also one reason the Fed is forecasting the highest neutral rate in a decade.

Fed watchers were eager to get some colour on its thinking around the current conflict in the Middle East, especially the potential implications of the oil shock for inflation. However, the Fed’s message avoided talking about the conflict as much as possible and instead pinned inflation primarily on tariffs. Powell’s forecast is that tariff-related inflation should come down around the middle of this year. While inflation expectations due to the oil shock have increased in the short term, the Fed will likely ignore the initial impact and wait until the second-order oil shock feeds into the real economy via higher fuel costs and energy prices.

Despite the Fed’s comments about uncertainty surrounding the conflict, the market is clearly pricing in a greater impact from oil shocks and higher inflation expectations. As mentioned, both Fed funds futures and SOFR futures options imply far fewer cuts this year, with some probability of hikes being priced into next year and beyond. If the conflict drags on, there is a risk that the Fed will have to materially revise its forecasts, and that is a risk we will be watching closely.

Chart 2: Implied Fed Funds Target Rate (the “Dot-plot”), as at 18 Mar 2026

Source: Bloomberg, Federal Reserve

Table 2: updated market pricing of Fed rate cuts probabilities, as at 18 Mar 2026

Source: Bloomberg

Table 3: Economic projections for Fed, as at 18 Mar 2026

Source: Federal Reserve