Rates relief

David Bassanese

4 minutes reading time

Related articles

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

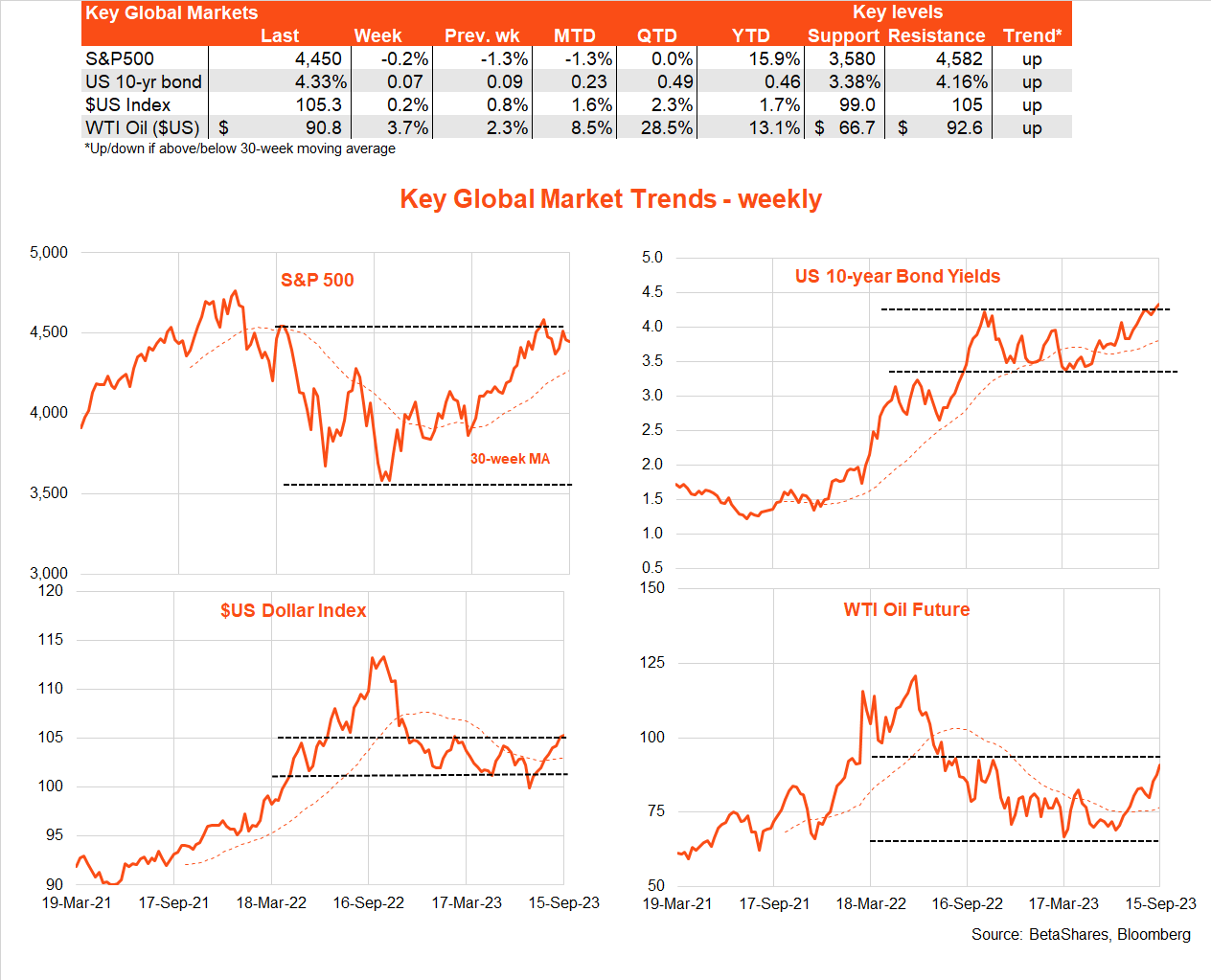

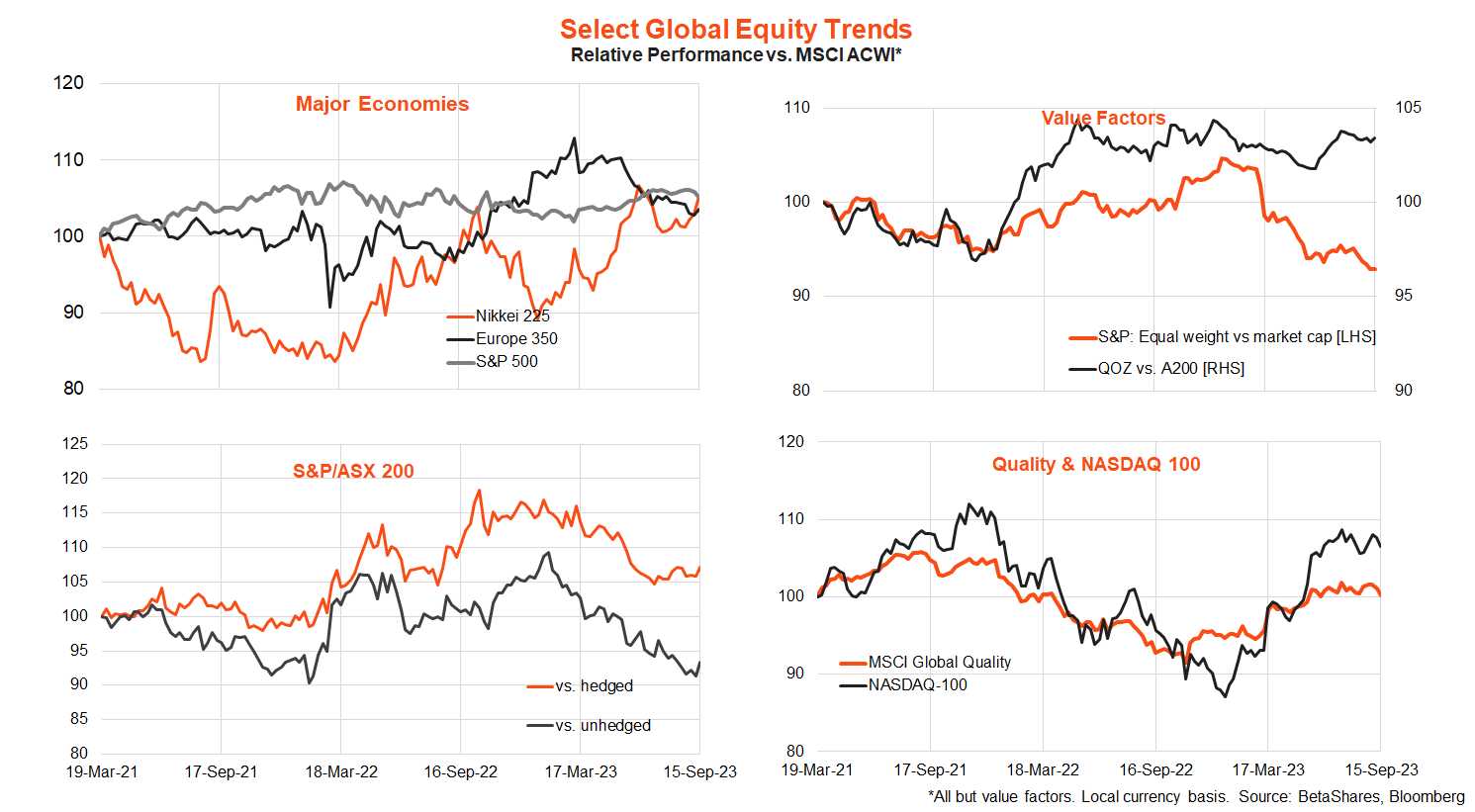

Global markets

Global equities consolidated last week despite a slightly higher-than-expected US core CPI and a further gain in bond yields. The ongoing rise in oil prices is emerging as a new market concern, while US activity data remained firm.

Reflecting higher energy costs, the headline US CPI rose 0.6% in August – in line with market expectations. This pushed annual headline inflation back up to 3.7% from 3.2% in July. Excluding food and energy costs, the core CPI rose 0.3%, or a touch above the 0.2% market expectation. Nonetheless, annual core inflation still fell to 4.3% from 4.7% in July.

In other news, US retail sales and industrial production remained firm, while headline producer prices were also a bit stronger than expected due to higher energy costs.

In other global news last week, the European Central Bank hiked rates again – in what was a mild surprise to the market, though the bond damage was limited due to ECB commentary suggesting it may have been the last rate hike in this cycle. Chinese economic data was also a bit better than feared – with a stronger-than-expected gain in retail sales and industrial production, though continued signs of weak fixed-asset investment and property prices.

The key global highlight this week will be the Fed meeting, which concludes on Wednesday (US time). Higher energy costs and still firm economic activity suggest the Fed is likely to retain a modest tightening bias at this week’s policy meeting. Specifically, however, market focus will be on the ‘dot plot’ of median expected future policy moves anticipated by the Fed Committee. Back in June, the last published dot plot implied two further 0.25% rate hikes by year-end – one of which was duly delivered in July. The Fed also forecast four 0.25% rate cuts in 2024.

The issue is whether the Fed retains the one further rate hike in these projections and/or scales back the extent of rate cuts next year. My base case expectation is the Fed will retain the current dot plot configuration, which could see a mild bond sell-off as it would heighten the risk of a November rate hike.

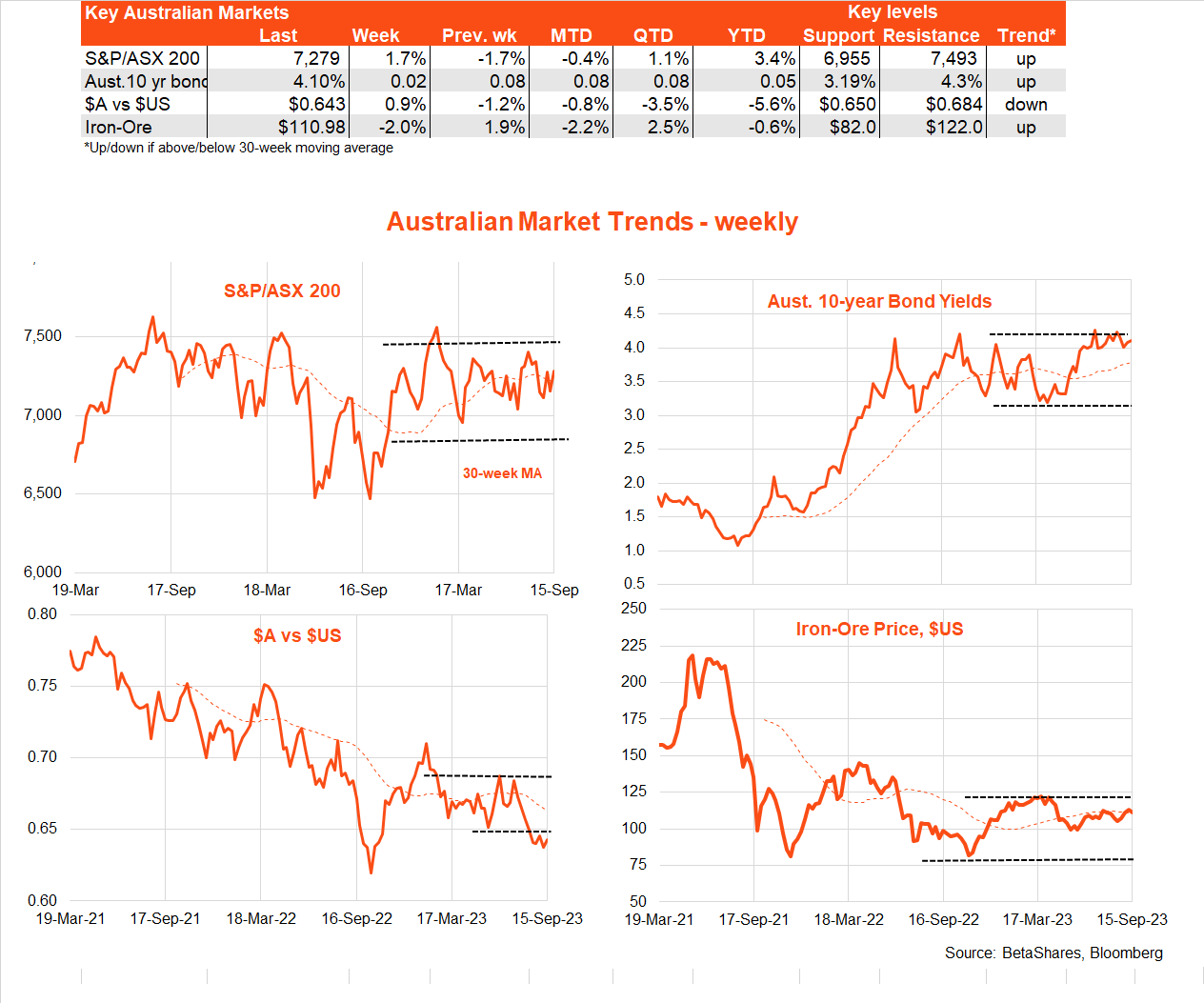

Australian market

Local equities remain trapped in a choppy sideways range – not helped by still high bond yields and a soft earnings outlook. Chinese optimism helped stocks bounce back last week after declining in the previous week.

Local economic data was also generally firm last week. The NAB index of business conditions lifted further to remain at above-average levels, and there was a reassuring easing back in price pressures – which had lifted in recent months. Employment also surged by 65k in August, likely reflecting seasonal distortions around school holidays (employment, unusually, fell a little in July) and a ‘Matildas effect’ in terms of extra activity in bars, restaurants and sports merchandise shops. The unemployment rate nonetheless held steady at 3.7%, reflecting the ongoing immigration-led growth in labour supply.

Running contrary to this optimism was consumer sentiment – which according to the Westpac/Melbourne Institute survey remains in the doldrums, despite steady RBA activity in recent months. Still-high inflation and interest rates continue to weigh on household sentiment and their spending proclivities.

There’s very little on the local calendar this week apart from minutes from the September RBA policy meeting tomorrow. As a result, most attention will be directed at the all-important US Fed meeting.

Have a great week!

Explore

Bassanese Bites