Cliffwater

9 minutes reading time

- Private assets

- Private credit

This article was written by Stephen Nesbitt, Cliffwater CEO and has been republished with Cliffwater’s permission. Cliffwater are the inaugural partners of Betashares Private Capital and manage the underlying fund into which the Betashares Private Capital | Cliffwater Private Credit Fund invests. Betashares has not verified and does not warrant the accuracy or completeness of the information, and the article does not necessarily represent the views or opinions of Betashares.

Recently, we also launched our new Betashares Private Capital newsletter. You can sign up for it at https://subscriptions.betashares.com.au/.

The investment press sees systemic risk in every default while lenders argue idiosyncratic circumstances. Who is right? Our research shows that the press commonly mistakes one-off defaults as something greater than what they are. A range of risks underlie defaults, which are catalogued below, but we believe the presence of systemic risk is generally exaggerated and, unfortunately, never predictable. Like much else in private debt, this means diversification and loan protection are top priorities across the market cycle.

High realised losses (aka write-offs) reported by the Cliffwater Direct Lending Index (CDLI) would be the best indication, in our view, that systemic risk is unfolding in the credit markets. That is not happening. Realised losses through September 2025 have been averaging an annualised 0.68% in recent years, well below the historical 1.00% realised loss rate. Even when recent vintage loans are excluded from CDLI, realised losses have been averaging at or below historical averages.

High unrealised losses (aka write-downs) reported by the CDLI would be the best indication from our research whether systemic risk is expected to unfold in the credit markets. That also is not happening. Unrealised losses have effectively been zero in recent years, even when recent loan vintages are excluded from the calculation.

The recent absence of unrealised market-wide losses (write-downs) is not a sign of poor valuation procedures. We have shown that CDLI unrealised losses have tended to reliably precede but overstate subsequent realised losses (defaults). Collectively, those overseeing loan valuations are doing their job.

Private debt investors get rewarded to absorb bad news, which comes from many sources. With roughly 10,000 unique middle market borrowers reflected in CDLI, 200 default-related news stories could be written each year.1 Most defaults reflect borrower idiosyncratic risk, unique to individual borrower circumstances. Industry risk ranks second in importance. In the last 10 years alone, energy, consumer, healthcare, and now software have temporarily elevated default levels. Manager risk ranks third, capturing the quality of underwriting on the part of lenders. Apollo, Blackstone, Monroe, Oaktree, Goldman, and others have endured short-term periods of above-average default losses, in part, due to poor underwriting. For a few other lenders, high default rates are persistent. Finally, there is recession risk, which is systemic across risky credits, public or private, and unforecastable. These four sources of risk can be amplified through financial risk when leverage or structuring are present.

What about falling prices for exchange-traded business development companies (BDCs)? Is that a potential canary? Our research shows that BDC pricing, represented by the Cliffwater BDC Index (www.bdcs.com), is a poor predictor of systemic risk ahead. For example, in 2011, public BDC prices dropped 30%, but subsequent CDLI values remained largely unchanged. However, BDC pricing is generally good at identifying manager and other risks, as the recently reported BlackRock write-downs demonstrated. BlackRock (formerly known as Tennenbaum) historically priced above net asset value, reflecting strong performance and a reliable investment team. After the BlackRock purchase, management changed, performance suffered, and the BDC began to consistently trade below net asset value, reaching a whopping 38% discount at year-end. The public BDC market clearly foreshadowed the subsequently announced write-downs (unrealised losses).

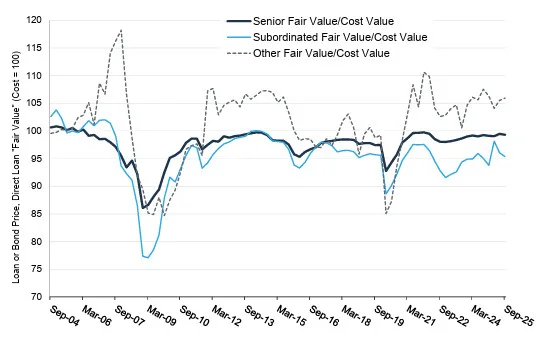

Financial risk, through subordinated debt and equity structuring, worsened BlackRock’s BDC losses. The exhibit below is one we regularly produce that shows how additional volatility is introduced when relatively-low volatility senior lending is replaced by higher-volatility subordinated (second lien) and other (equity-linked) lending. Compounding structuring risk, the BlackRock BDC deployed 50% more portfolio-level leverage than the average BDC, causing perhaps manageable problems to approach unsustainable levels.

Exhibit 1: Historical Price Volatility by Loan Seniority, September 2004 to September 2025

Past performance is not an indicator of future performance.

Private debt has the potential to deliver attractive and consistent returns when enhanced diversification, loan protection, cash yield, reasonable fees and prudent leverage levels are in place.

Footnote:

1: Assuming historical 2% annual default rate for CDLI.