David Bassanese

3 minutes reading time

The US Supreme Court’s decision to invalidate many of President Trump’s tariff hikes suggests some of America’s famed political checks and balances remain alive and well.

The reality was that Trump’s long held desire to assault the global trading system through the weapon of tariffs was always legally dubious.

US Presidents simply don’t have the legal power to wield tariffs as a weapon of global coercion in the way Trump desires – the only question is whether the Supreme Court would be cowered into letting Trump get his way. It was not.

Although Trump has quickly used other legal pretexts to reinstitute a 15% across the board tariff, the Supreme Court’s ruling has effectively dealt a body blow to Trump’s tariff strategy.

Even the latest lift in tariffs requires Congressional approval within five months. With Republicans only having a slim majority, the omens are not good. It will only require a few Congressional members to find their backbone in the same way that a majority of Supreme Court judges have done.

Going forward, Trump may well go down the path of implementing a range of sector specific tariffs to address perceived unfair trade practices abroad – as these appear to be on legally firmer ground. But this may well be more piecemeal – and would seem to rule out the continued use of national tariff threats across the board for pure political coercion.

What’s more, as we’ve seen with the Greenland threats earlier this year, Trump may well face greater global retaliation if he seeks to reopen trade deals through the launch of more tariff threats.

Unlike last year, Europe did not roll over in the face of renewed US tariffs threats last month – but instead threatened tariff retaliation and even reduced purchases of US Treasuries. Trump backed down, and we’ve heard little of the Greenland issue ever since.

Of some relief to markets, for the moment at least, the Supreme Court’s decision is not a threat to US budget revenues.

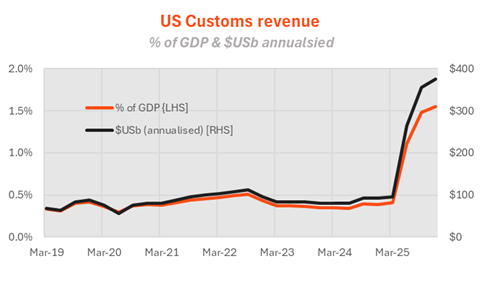

Whether the US Government will need to pay back the billions in tariff revenue it has already collected will likely depend on further court disputation. An extra $US187b in customs revenues was collected in 2025 compared to 2024.

As evident in the chart below, the increase in total US tariffs this year has lifted annualised customs duties collections by $US 280b, or around 1% of GDP.

And the new 15% global tariff – even if only temporary – will make up for revenue shortfalls for the next few months.

But over the longer run, it now seems likely that tariff revenue will not be able to offset the budget revenue loss from Trump’s other key policy since his return to office – the Big Beautiful Bill. This will leave the US budget position as perilous as ever.

The other key market implication is that Trump’s likely efforts to reinstitute his tariff strategy – one way or another – risks re-stoking global trade tensions, and in an environment in which trading partners may now feel more emboldened to threaten retaliation.

It’s worth remembering that tariffs represent an ‘own goal’ for the US economy. Given that US wholesale import prices have not dropped by much, most independent economic studies suggest that the vast bulk of tariff revenue (~80-90%) has been paid for by US businesses and consumers.

US inflation is about 0.5% higher than it would otherwise be and tariff uncertainty likely contributed to a US corporate hiring freeze last year – with no net job gains in the second half of last year.