David Bassanese

8 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the player below:

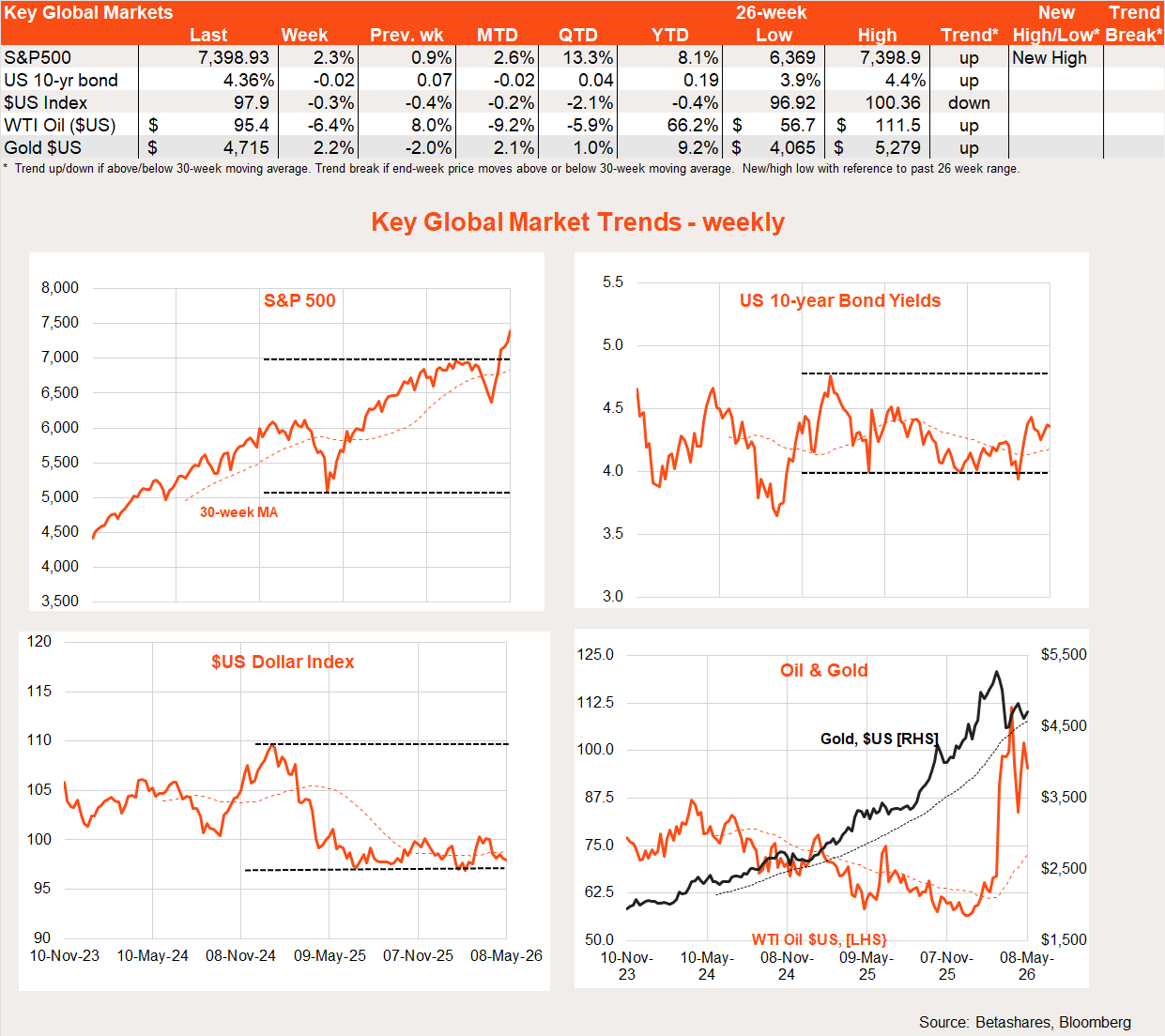

Global week in review: Hope reigns supreme!

US stocks rose further last week – the sixth weekly gain in a row – with ongoing hopes for a US-Iran peace deal despite continuing skirmishes in the Strait of Hormuz. One sign of optimism was the decline in oil prices. A stronger than expected US payrolls report on Friday also boosted stocks.

Yet another week in the lingering Iran war and hope springs eternal. As I’ve regularly noted, the global economy is facing a race against time – settle the Iran war and re-open the Strait before the lagged impact of the lack of new supply jacks up prices. So far at least, inventory run-down, some demand restricting measures across Asia and persistent hopes for a peace deal has limited lift in near-term oil price futures – but the clock is still ticking.

Both sides are exchanging peace proposals – at the same time as they’re firing on each other’s ships! But there seems enough wiggle room on both sides that hopefully a deal can be done soon – though the outcome is unlikely to be much better for the US than the Obama-era deal that Trump tore up in 2018.

The current environment reminds me of the COVID-crisis – after an initial sell-off due to lockdowns, markets kept rallying despite abysmal economic data, due to the ongoing hope of a vaccine and economic re-opening. Markets can endure near-term sticks it seems if there remains an attractive carrot ahead of them.

In other news, April US payrolls were better than expected with a 115k gain in jobs compared to a market expectation of 65k. The unemployment rate held steady at 4.3%. The resilience of the US economy remains impressive.

Global week ahead: Iran and CPI

Markets remain in limbo – waiting on a peace deal. As the consequences of no deal seem catastrophic for both sides, it’s hard to imagine they can’t/won’t agree.

Yet the week begins with news that Iran is refusing US demands to dismantle its nuclear facilities and suspend uranium enrichment for 20 years. Other sticking points are what to do with Iran’s stockpile of already high-enriched uranium (most of which was developed when Trump tore up the existing deal in his first term).

Key US economic data this week include the consumer price index (CPI) for April. Core prices are expected to lift 0.3%, which would see annual growth lift from 2.6% to 2.7%. The US CPI is currently running quite a bit lower than the Fed’s preferred measure of underlying inflation – the core consumption deflator (PCE) – due to the former’s higher weight to housing inflation, which is at present quite soft. Annual core PCE inflation is currently 3.2%.

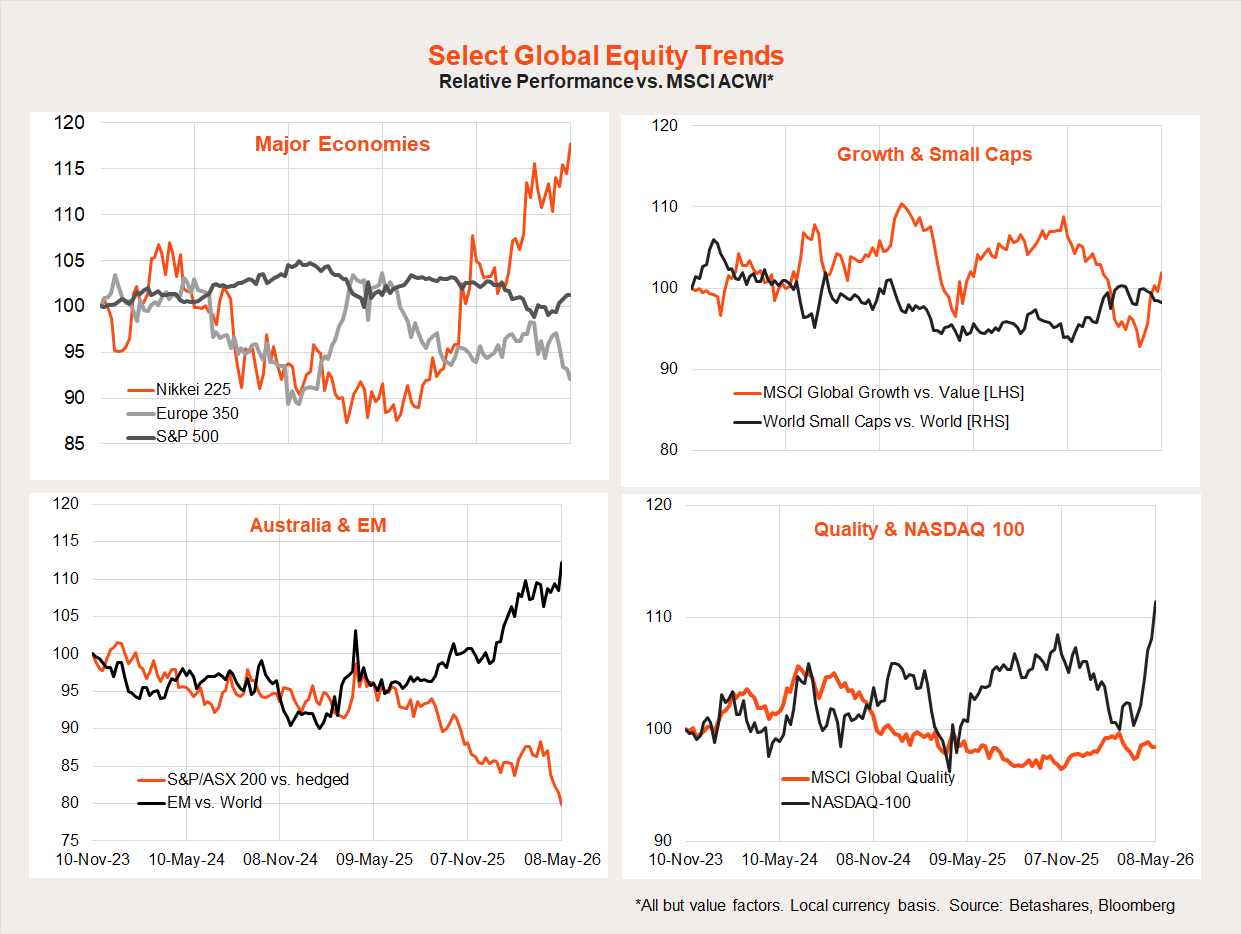

Global equity trends: US outperforms

Global equity markets have now staged a remarkable 6-week rebound on peace talk hopes. Overall global stocks and the S&P 500 are now trading comfortably above the levels prevailing just before the Iran war began. But it’s not just peace-talk hopes, but a renewed infatuation with the AI trade – especially hardware companies.

Accordingly, the US, Japan and emerging markets continue to do best in the rebound so far, whereas Europe, Australia and small caps have not. The Nasdaq 100 has shot the lights out. Korea is also soaring, thanks to the market’s love of hardware companies such as Samsung benefiting from the AI boom – as, unlike software companies, they’re at less apparent risk from disruption.

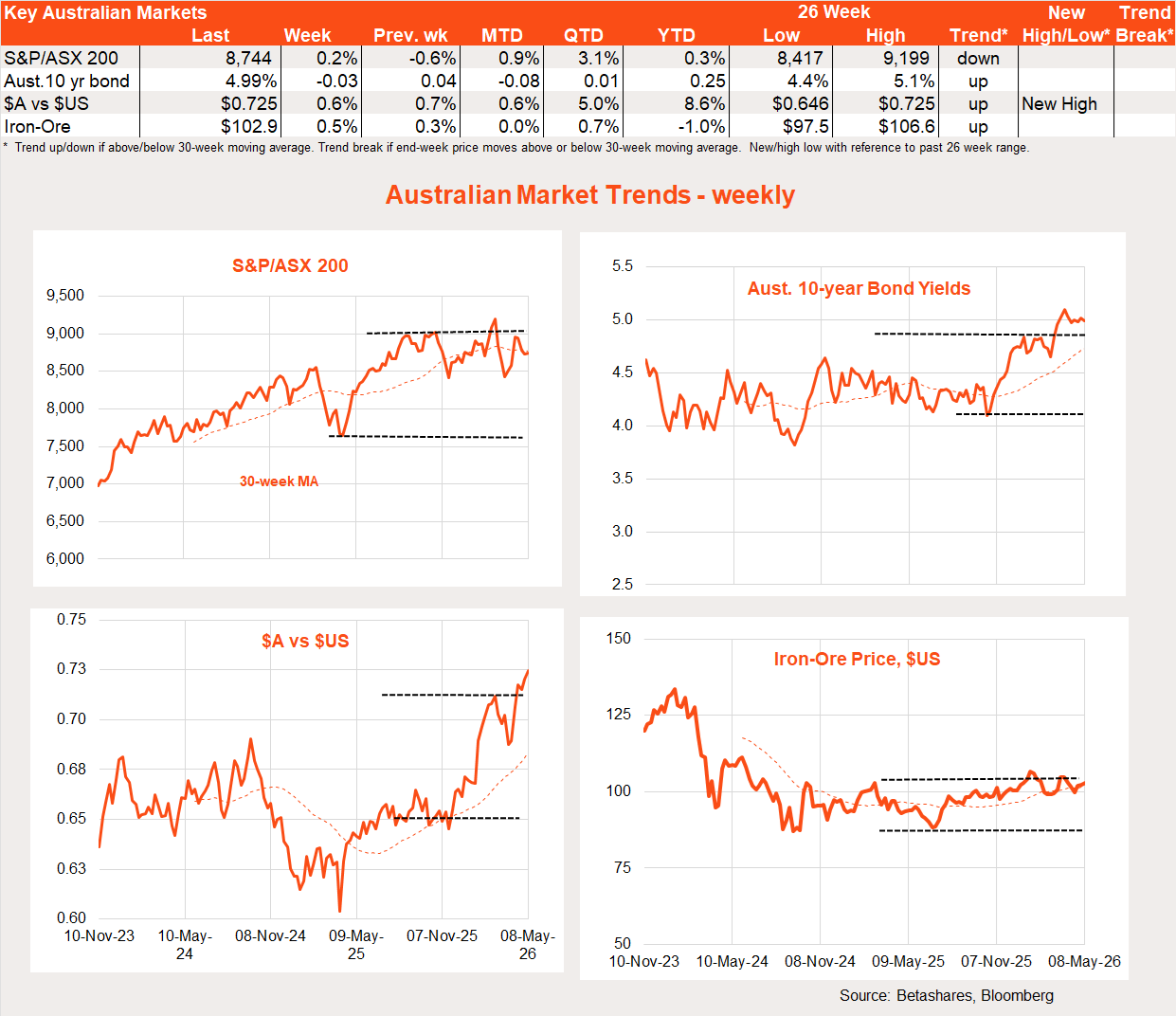

Australia review: RBA acts and Budget in focus

Local stocks underperformed global stocks again last week, with the RBA delivering on its threat to raise interest rates for the third time in a row. Concerns around capital gains tax increases in this week’s Federal Budget did not help.

It’s been a sorry tale for local stocks in recent weeks – which have failed to benefit all that much from the global market rebound. A low technology exposure, along with RBA and Federal Budget concerns, have been major drags.

If there was any solace in last week’s RBA rate hike news, it was that the Bank might be kind enough to pause at the next meeting in June – just to assess the impact of its work to date.

My base case is that by the time the August meeting comes around, the Iran war will have ended and oil prices will have retreated further, lessening the pressure on the RBA to hike further. Potential disruption in the property market following this week’s Federal Budget might also give the RBA reason to hold off.

Two threats to my view are:

- The RBA’s forecasts of weaker growth and easing inflation factor in market expectations for one to two further rate hikes.

- Due to a compression in banking margins, the average variable mortgage rate is now around 0.5% lower than it was the last time the cash rate was 4.35% in 2023 and 2024.

In good news for the RBA (albeit not retailers) last week’s household spending indicator suggested consumer spending was fairly subdued in the March quarter, with real growth of only 0.7%.

Budget – tax grab or boost for intergenerational equity?

I’ll do a full analysis of the Budget on Wednesday, but the rumours suggest a fairly aggressive attack on negative gearing and capital gains. This will apply to all assets it seems – such as property and shares – with an exemption only for new properties. At this stage, there appears no exemption for investments in entrepreneurial growth companies.

Modelling suggests that the shift to inflation-indexing of capital gains – rather than the 50% discount – will increase the effective capital gains tax the longer you hold an investment and the higher the return it attracts.

As an example, an investment returning 7% in capital gains each year held for 10 years will attract a 15% CGT under the current system, but 21.3% under inflation-indexing (assuming inflation of 2.5% p.a. and a marginal income tax rate of 30%).

- If the annual return was 10%, the CGT under the current system would remain 15% but lift to 24.7% under inflation-indexing.

- If the 7% returning investment is held for 30 years, the CGT under inflation-indexing rises to 25%, though stays at 15% under the current system.

Boomer investors will be hurt for sure, but so will younger investors – especially as they have longer investment timeframes and tend to hold higher-growth investments.

As for the property market, the expected tilt favouring new property will only succeed in driving up land values and developer profits (due to supply constraints, the more favourable tax benefits will be quickly capitalised into prices), while there’s also a risk of a leap in rents on existing properties as investors exit the market and demand higher compensation to offset the less favourable tax benefits.

Also getting media coverage is an effective doubling of the capital gains tax on entrepreneurial companies from 25% to a world-beating 50%!

All up, the idea that these changes will boost ‘intergenerational equity’ seems a stretch – there may be several unintended consequences that actually make economic conditions even harder for the young (higher rents, high new property prices, reduced returns on longer-term investments and the hobbling of the start-up/entrepreneurial sector).

It’s true that current tax incentives favour gearing up into property especially – but a key problem is the high 47% top marginal tax rate which kicks in at a relatively low income by global standards and is considerably higher than the corporate tax rate. That just invites creative tax planning – the impetus for which won’t change after tomorrow. True tax reform would have involved effective tax-base broadening (as we’re likely to see tomorrow) along with a reduction in marginal income tax rates.

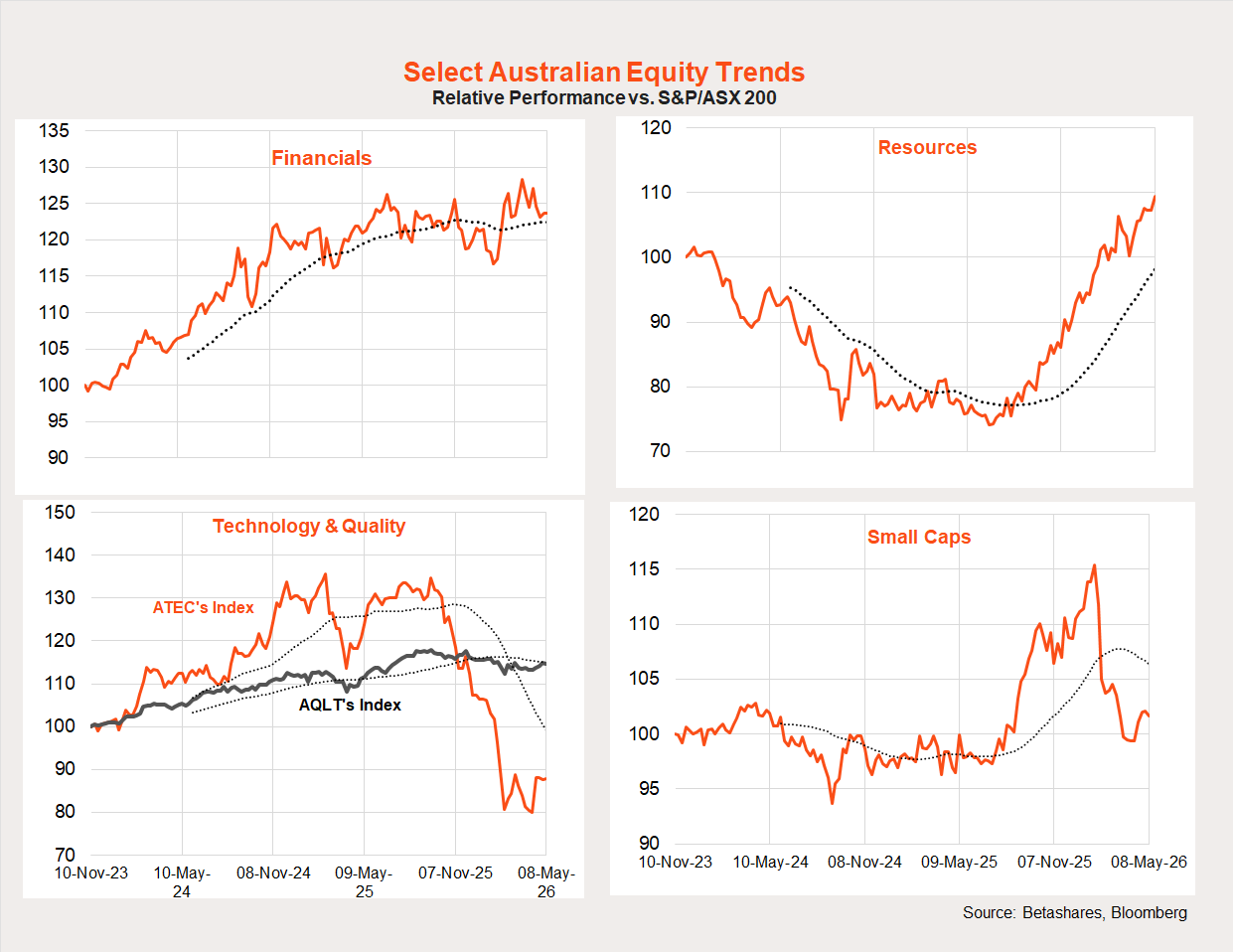

Local equity market trends: Technology/small caps bottoming out?

The Iran war initially was not kind to high-beta local exposures such as technology and small caps. That said, the relative performance of both these areas has bottomed out in recent weeks, while resource company relative performance has resumed at the expense of financials.

Australia week ahead: Budget

I’ve given my 2 cents on apparent key Budget changes above – we await the actual details tomorrow!

Other reports of note tomorrow include the National Australia Bank and Westpac surveys of business and consumer sentiment respectively. Both business and consumer confidence slumped in the previous reports and – apart from Iran peace-talk hopes – it’s hard to see much reason for a solid rebound anytime soon.

Also of note will be the Q1 wage price index on Wednesday. Given labour market tightness and inflation concerns, there’s an understandable interest in what wage growth is doing. Bottom line: it’s firm but not red hot. A quarterly wage gain of 0.8% is expected, in line with that of recent quarters and keeping annual growth at just over 3%. That said, wage growth at this modest pace would be more tolerable were labour productivity growth not so weak.

Have a great week!