Chamath De Silva

6 minutes reading time

- Global shares

Right idea, wrong execution

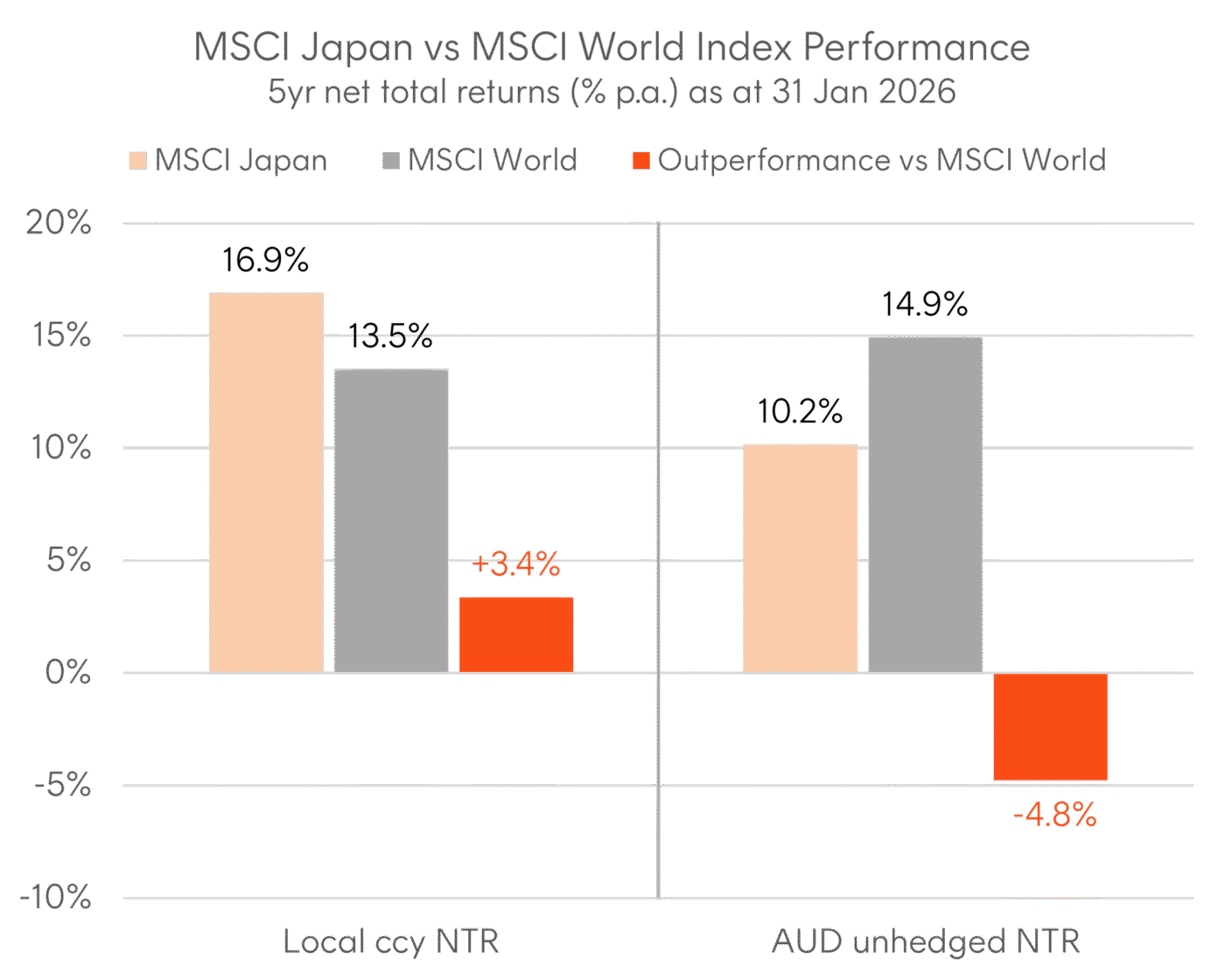

Japanese equities have been one of the standout stories in global markets over the past five years. The convergence of Abenomics-era structural reforms filtering through to corporate boardrooms, Warren Buffett’s high-profile accumulation of Japanese trading companies, and a major turn in global monetary policy coming out of the Pandemic created a compelling case for overweighting Japan. Many Australian investors agreed, and they were right to do so – in local currency terms, at least.

Figure 1: MSCI Japan vs MSCI World NTR Index Performance – 5yr local currency returns

Source: Bloomberg, MSCI. Past performance is not indicative of future performance. It is not possible to invest directly in an index.

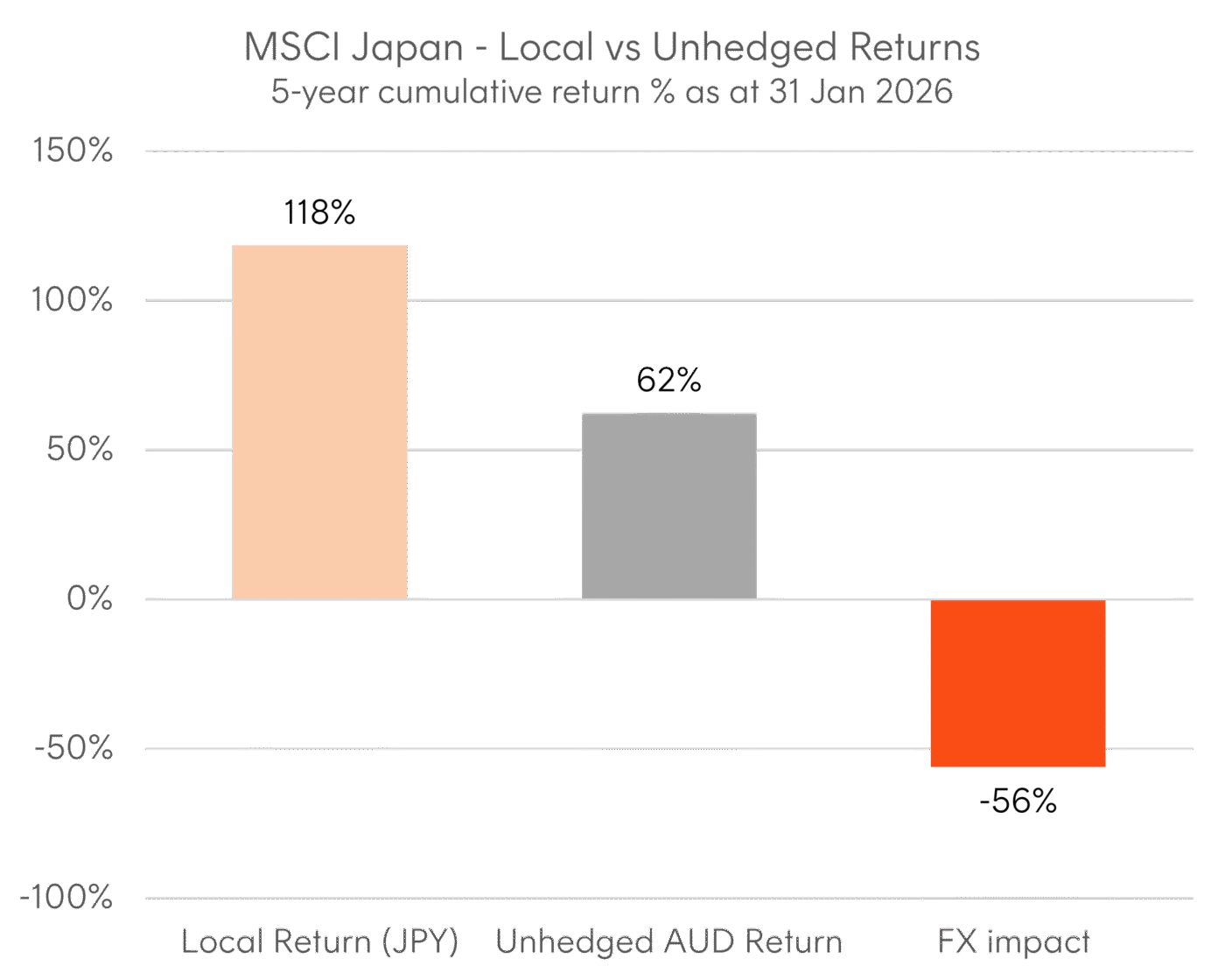

Over that five-year window, the yen weakened substantially against the Australian dollar, eroding 56 percentage points of cumulative return. An investment that returned 118% in local currency terms delivered just 62% in AUD after accounting for the FX impact – a staggering amount of value destroyed simply by being unhedged.

Figure 2: MSCI Japan – Local currency vs AUD unhedged returns – 5yr cumulative

Source: Bloomberg, MSCI. As at 31 January 2026. Past performance is not indicative of future performance. It is not possible to invest directly in an index.

The true cost of being unhedged

The opportunity cost of being unhedged in Japanese equities extends beyond just the spot currency movement. The unhedged investor not only suffers from yen depreciation but also foregoes the “carry” earned by the hedged investor – the additional return generated from the interest rate differential between Australia and Japan when rolling forward FX contracts. We unpack the mechanics of this carry in more detail below, but first, the numbers speak for themselves.

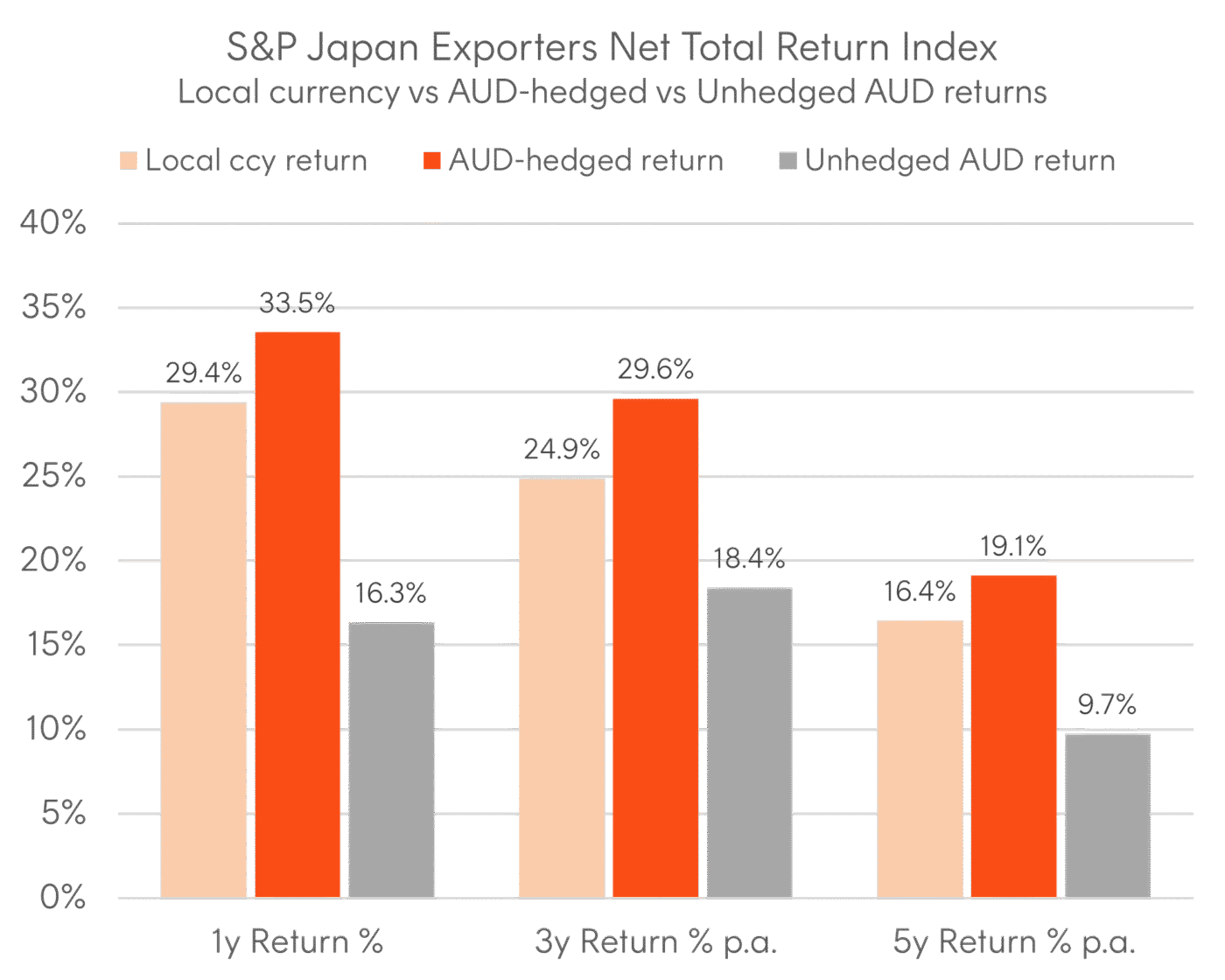

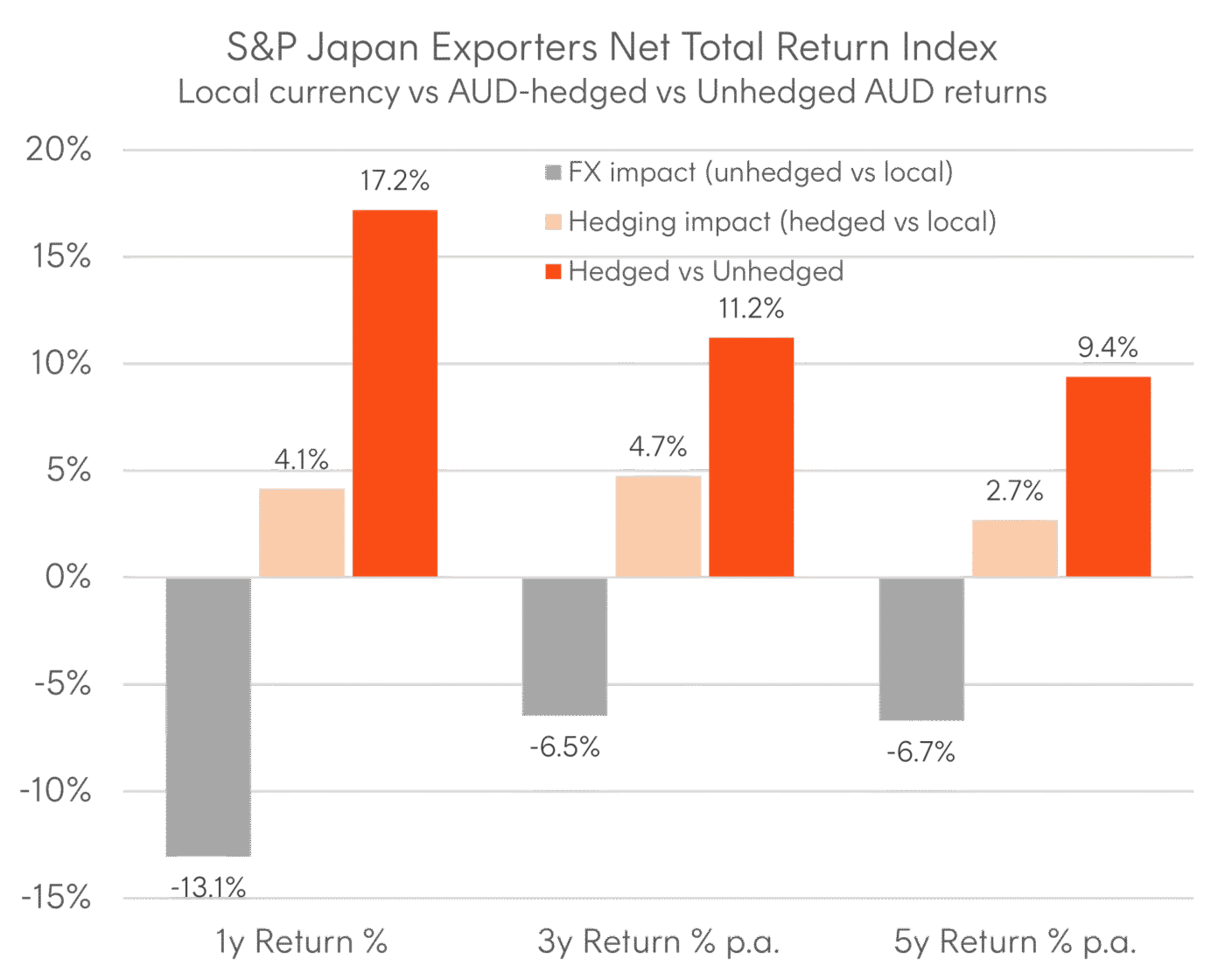

To illustrate, consider the S&P Japan Exporters Net Total Return Index, which can be decomposed into three return variants: local currency (JPY), AUD-hedged, and AUD unhedged. Over five years to January 2026, AUD-hedged returns came in at 19.1% per annum – nearly double the 9.7% per annum delivered unhedged, a difference of 9.4 percentage points per annum. The hedging carry added roughly 2.7 percentage points per annum on top of the local return, while the FX impact detracted approximately 6.7 percentage points per annum from unhedged returns.

This pattern has been consistent. Over one, three, and five-year horizons, the hedged variant has materially outperformed the unhedged equivalent. The gap isn’t trivial and it compounds meaningfully over time, driven by the dual headwind of yen depreciation and foregone carry.

Figure 3: S&P Japan Exporters NTR – Local currency vs AUD-hedged vs AUD unhedged

Source: Bloomberg, S&P. As at 31 January 2026. Past performance is not indicative of future performance. It is not possible to invest directly in an index.

Figure 4: S&P Japan Exporters NTR – Local currency vs AUD-hedged vs AUD unhedged

Source: Bloomberg, S&P. As at 31 January 2026. Past performance is not indicative of future performance. It is not possible to invest directly in an index.

Understanding currency hedging

When an Australian investor buys a Japanese equity fund without hedging, their return has two components: the performance of the underlying shares in yen (the “local currency return”), and the movement in the AUD/JPY exchange rate. If the yen weakens against the Australian dollar (i.e. AUD/JPY rises), the currency conversion erodes returns (the “AUD unhedged return”). Conversely, a strengthening yen would boost them.

Currency-hedged funds and the indices they track use forward foreign exchange contracts to neutralise this currency risk. A forward contract locks in an exchange rate for a future date (the “forward exchange rate”), and that forward rate’s difference to the spot rate reflects the interest rate differential between the two currencies over the contract tenor. This is a no-arbitrage condition known as interest rate parity. Intuitively, an investor with yen today has two equivalent ways to end up with Australian dollars in one month: convert at today’s spot rate and deposit AUD for a month or hold the yen for a month and convert at the forward rate. Because both paths must yield the same result, the forward rate adjusts to reflect the difference in deposit rates between the two currencies.

For AUD/JPY, Australian short-term interest rates have historically been well above Japanese rates. This means the AUD/JPY forward rate trades at a premium to spot – in other words, an Australian investor hedging yen exposure effectively earns a positive return simply from rolling forward contracts. This is the “hedging carry” referenced above, and it compounds over time, acting like an additional “yield” on top of the equity return.

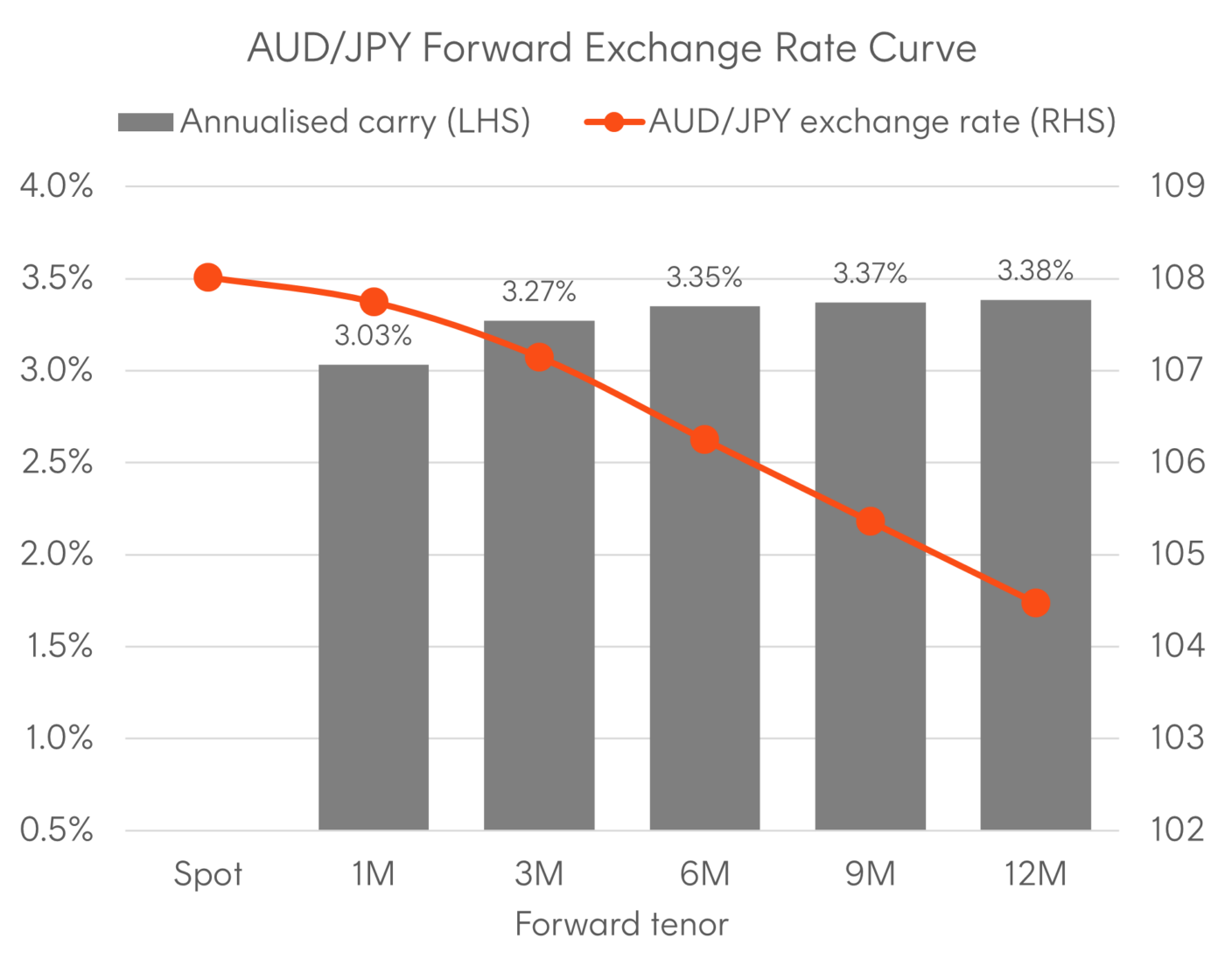

Figure 5: AUD/JPY Forward Exchange Rate Curve

Source: Bloomberg, S&P. As at 13 February 2026

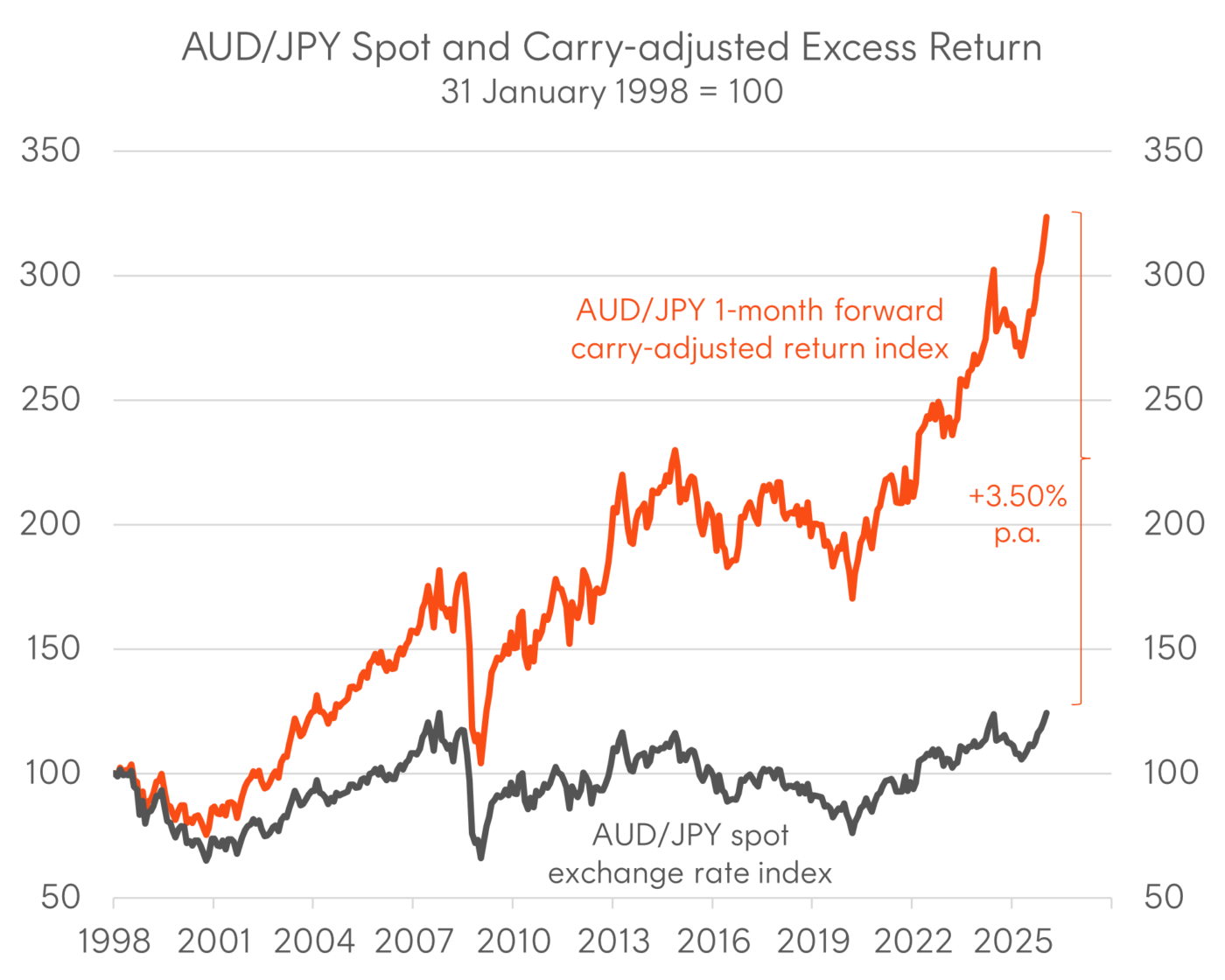

The long-term impact of this carry has been substantial. Since 1998, the AUD/JPY carry-adjusted return from rolling 1-month forward contracts has compounded at approximately 3.5% per annum above the spot return, demonstrating the persistent nature of this tailwind for hedged Australian investors.

Figure 6: AUD/JPY Spot and Carry-adjusted Excess Return

Source: Bloomberg. As at 31 January 2026

Looking ahead

The political backdrop reinforces the case for Japanese equities and AUD hedging. Prime Minister Takaichi’s landslide in the recent lower house elections — the largest victory in Japan’s post-war history — gives her government a mandate that her mentor Shinzo Abe might have envied. With a two-thirds supermajority, Takaichi can push through further structural reforms and fiscal stimulus largely unobstructed. For Japanese equities, this is broadly positive. For the yen, less so. Although the Bank of Japan is raising rates, it’s at a glacial pace, and real policy rates remain firmly in negative territory.

Against this backdrop, FX hedging carry remains attractive. With both the BoJ and the RBA expected to raise rates further in 2026, the AUD-JPY interest rate differential is likely to remain broadly unchanged over the medium term. At current pricing, annualised carry from 1-month AUD/JPY forwards sits around 3.0%, providing a meaningful hurdle that unhedged returns need to overcome, and for long-term investors, that hurdle compounds.

The HJPN Japan Currency Hedged ETF provides exposure to a portfolio of large Japanese exporters with the currency risk hedged back to Australian dollars, allowing investors to capture the Japanese equity story without the drag of unhedged yen exposure.