David Bassanese

5 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the below player:

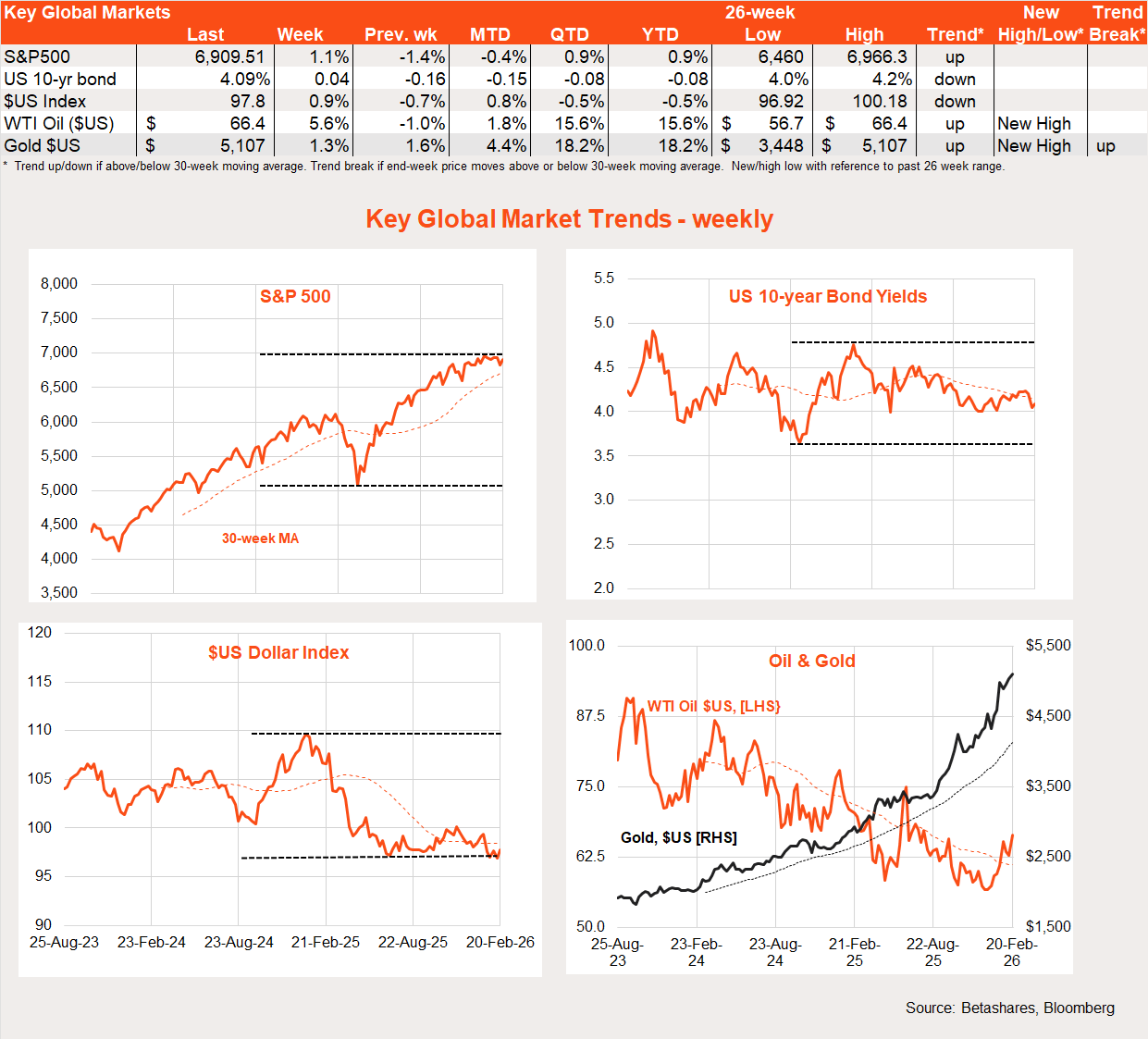

US stocks rebounded a touch last week given the absence of major new AI disruption fears.

Global week in review: Supreme Court body blow

There was little in the way of major global economic news during the week, allowing equity markets scope to stage a modest recovery after the previous week’s decline. Although AI disruption jitters remain, the impact on overall markets was relatively calm last week. That said, there was a late-week announcement from Anthropic on new cybersecurity tools which did sent a shudder through that part of the technology sector.

Of some interest, minutes from the recent Fed meeting were a bit more hawkish than expected – some voting members suggested the next move in rates could actually be up rather than down. US economic data also remained on the firm side, with durable goods, industrial production and housing starts all coming in stronger than expected. Bond markets wobbled, but rate cut expectations for later this year remained in place.

Also keeping upward pressure on oil prices were continued US-Iran tensions, with markets still wondering when and if Trump will launch missile strikes.

But the biggest news came on the weekend, with a majority of US Supreme Court judges deciding Trump’s use of emergency powers to implement across-the-board tariff hikes last year was invalid, as only Congress ultimately has the power to raise tariffs for revenue purposes. That said, Trump’s other tariffs, which were initiated on the grounds of national security and unfair trade practices, remain in effect. Trump also responded by announcing a temporary across-the-board 15% global tariff – which he can do – to shore up any loss in revenue in the short term.

More of my analysis on this outcome can be found here.

Global week ahead: Iran & tariff fallout

There is only limited US economic data this week, including regional manufacturing surveys, consumer confidence and producer prices.

What will likely attract more focus will be the fallout from the US Supreme Court decision on tariffs: for example, how will the decision affect the range of trade deals the US has in place?

Iran tensions and AI disruption concerns will also stalk investors.

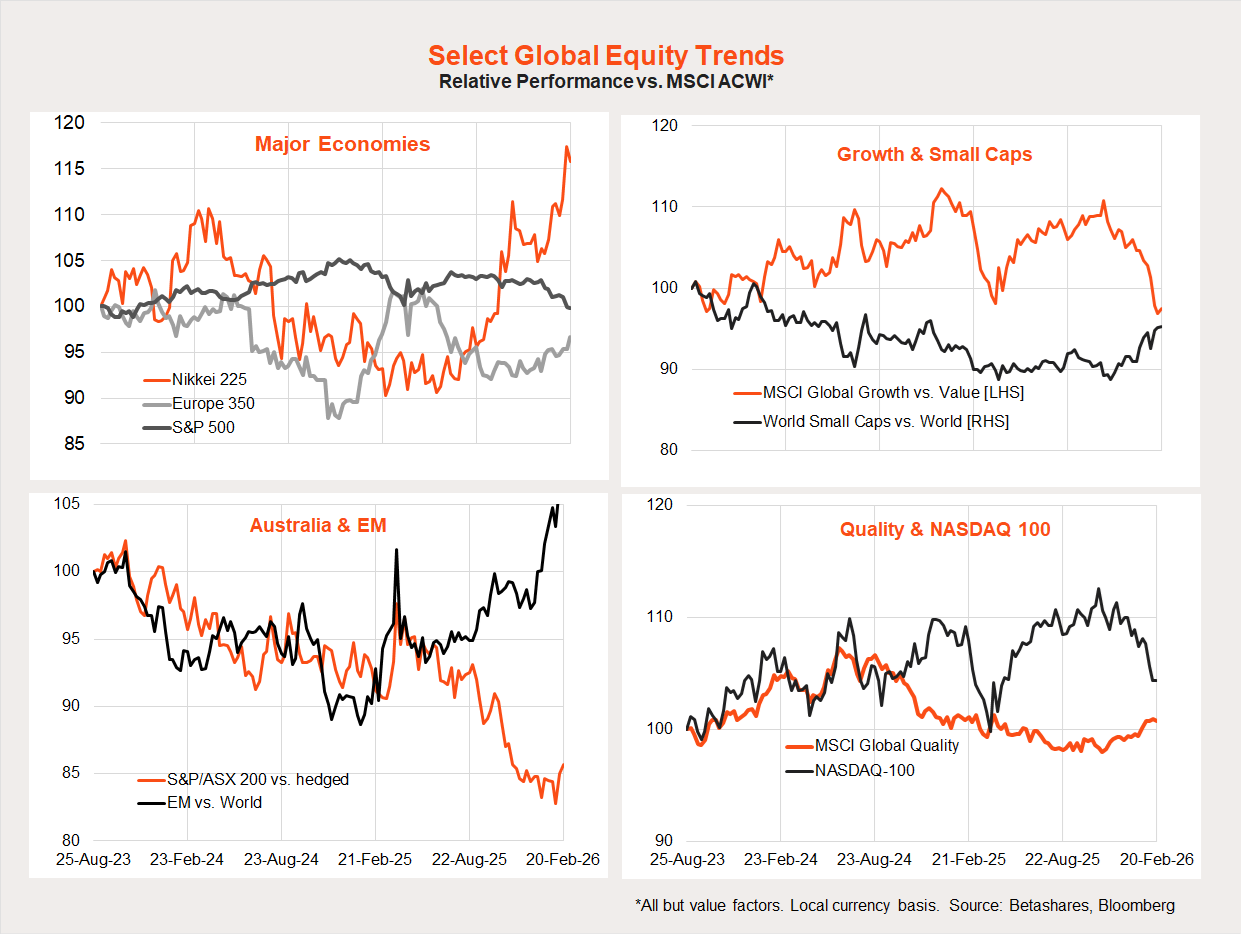

Global equity trends: the great rotation continues

The MSCI All-Country World Equity Index rose 1.2% last week, broadly in line with the US market. Relatively weaker performances in Japan and emerging markets were offset by strength in Europe.

At this stage, however, the great rotation remains in place. Since the end of October 2025, we’ve seen underperformance of US/growth/technology, replaced by strength in Japan, emerging markets and small caps. There are also tentative signs of a bottoming out in the underperformance of the Australian market.

Australian week in review: still firm employment

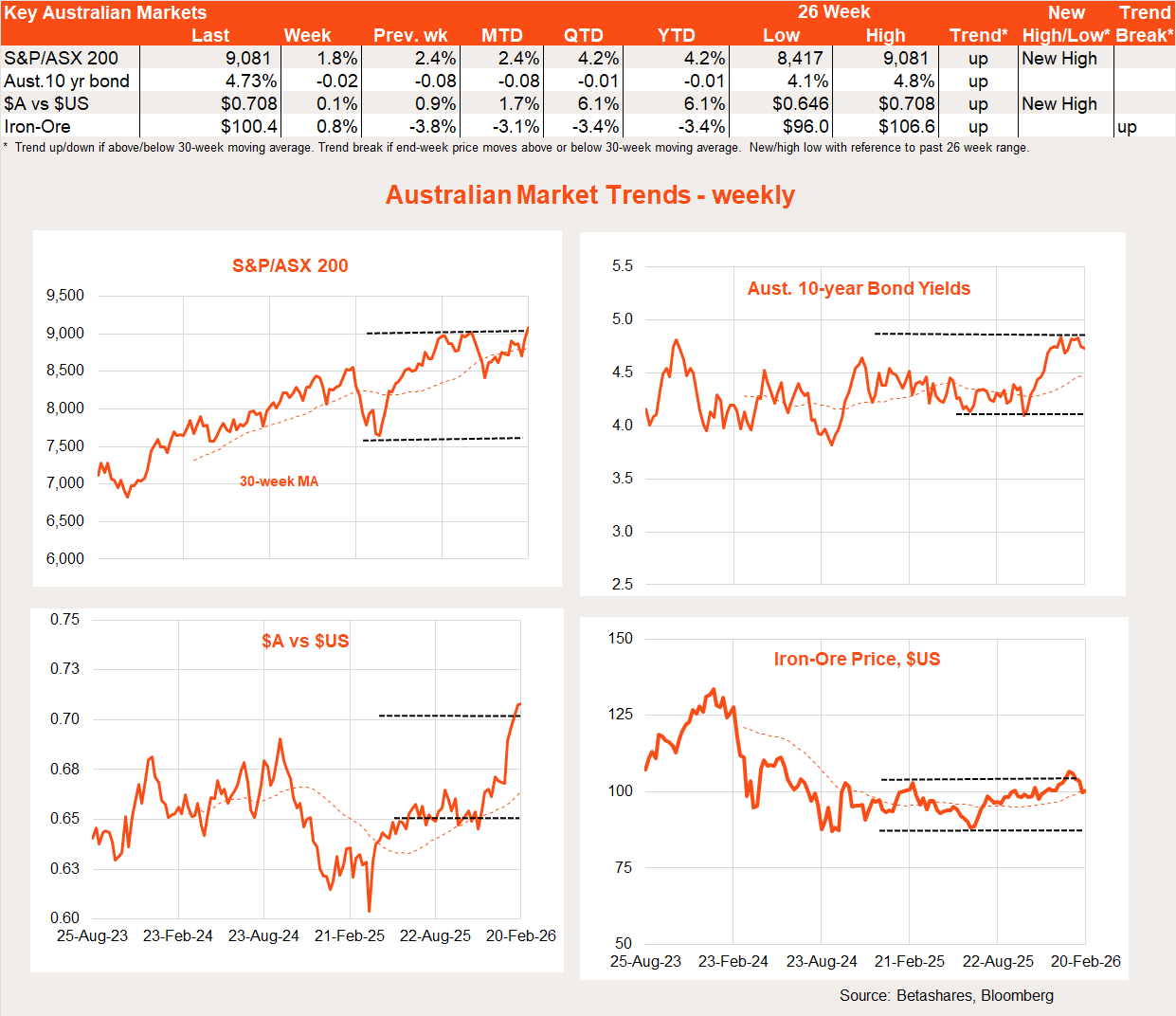

Australian shares enjoyed another decent bounce last week, ending the week above the 9,000 level for the first time since late October 2025. Energy and the beaten-up technology sector were the best performers.

The main news last week was another solid labour market report, with a 17k gain in employment during January, which was enough to keep the unemployment rate steady at 4.1%. Such strength suggests the RBA can afford to remain laser focused on the inflation outlook, with a potential rate hike in May on the cards if Q1 CPI remains on the high side.

Australian week ahead: January CPI and CAPEX

Although the RBA has downplayed its significance, markets won’t be able to resist focusing on Wednesday’s January consumer price index (CPI) report. Annual trimmed mean inflation will be the focus, which ended last year at 3.3% – a big jump in either direction will be market moving.

We also get the early ‘building blocks’ of Q4 GDP, with the private investment survey and building construction out on Wednesday and Thursday respectively. Looking through quarterly volatility, there’s been an encouraging lift in investment and various forms of construction over the past year – although the outlook is now at risk from RBA tightening fears.

RBA Governor Bullock also delivers a “fireside chat” in Melbourne on Wednesday evening. After extensive recent commentary, I doubt the chat will offer much new on the interest rate outlook.

Australian equity trends

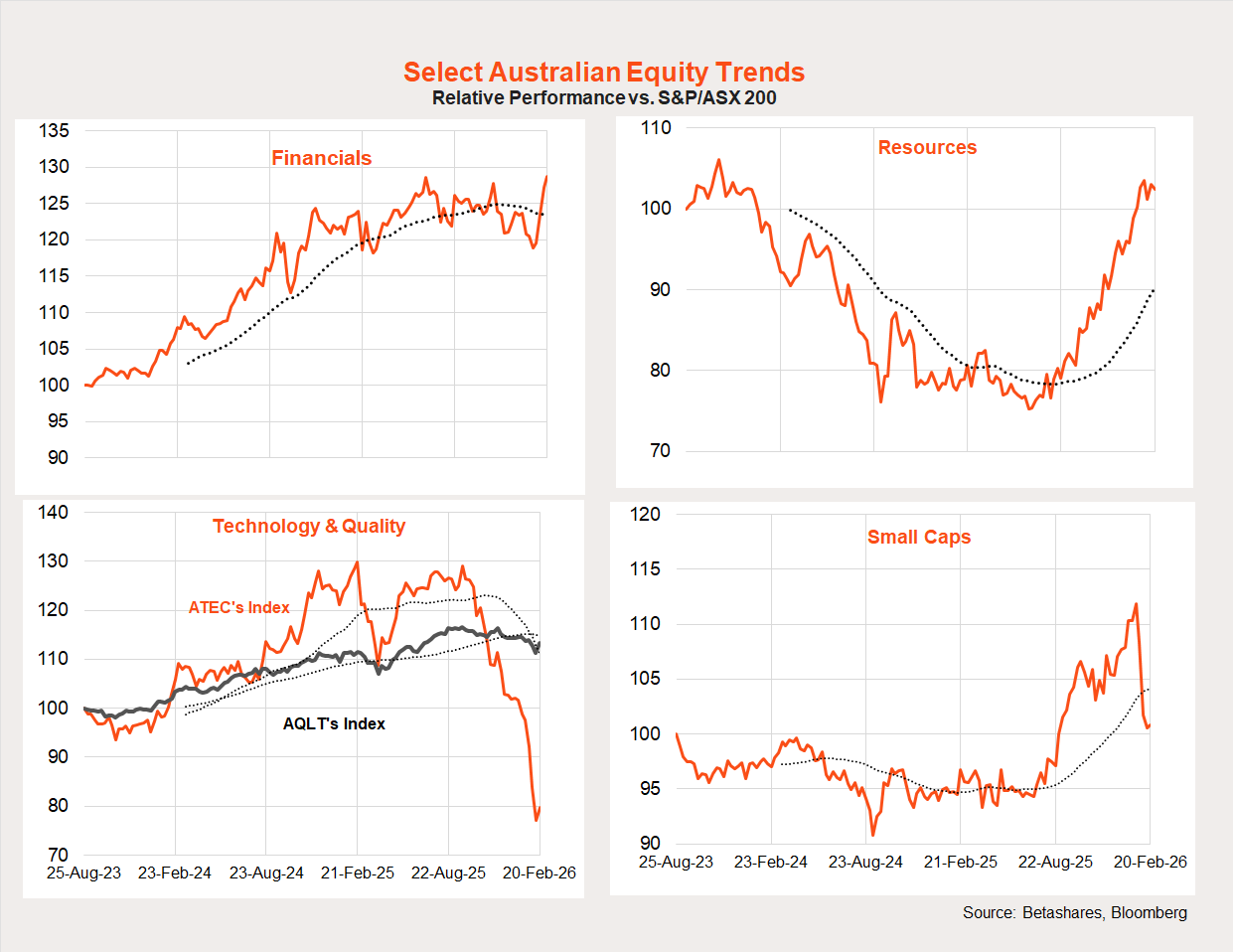

The local technology sector and small caps enjoyed a reprieve last week, with a bounce from what appears to be deeply oversold levels. More broadly, recent trends remain in place, with a rotation from financials and technology into resources.

Have a great week!