Hugh Lam

7 minutes reading time

Chinese equities have had one of their best years for some time, outperforming global peers by the widest margin since 2017.

However, the country’s stock market returns are not reflecting what’s happening in the real economy.

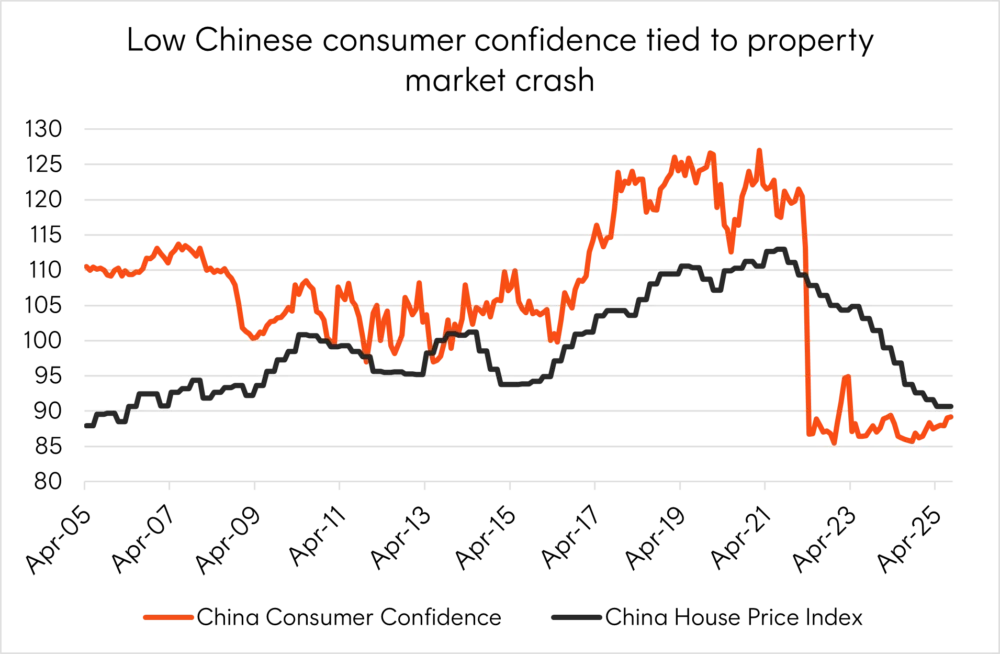

Consumer confidence levels are significantly lower than where they were prior to the Covid pandemic as property prices continue to fall in Tier-2 and Tier-3 cities like Chengdu and Dongguan. And given approximately 70% of household wealth is tied to the property market, consumer spending has also eroded as many Chinese citizens are feeling less financially secure.

Source: Bloomberg, FRED. April 2005 to December 2025.

To that end, reviving consumption has become a strong motivation for the Chinese government but this will likely take a great deal of effort before it becomes a reality.

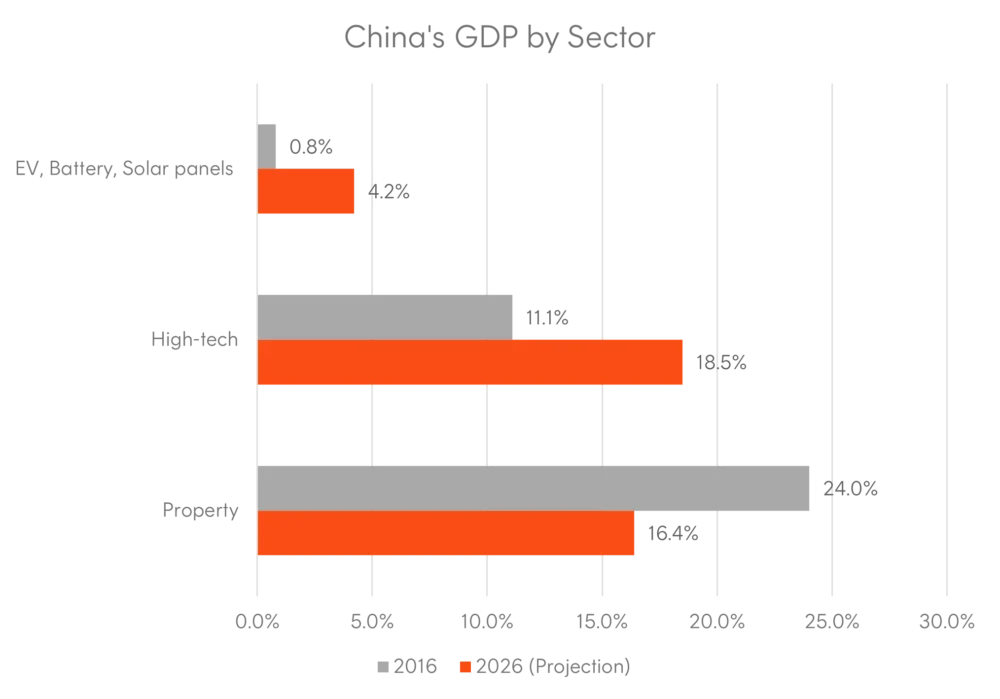

As a result, China has continued to lean heavily on export growth to meet its 5% GDP growth target despite recent initiatives to stamp out excess capacity in sectors like electric vehicles and solar panels under its “anti-involution” campaign.

While many acknowledge the structural weaknesses that the Chinese economy faces, President Xi has also expressed a clear pivot toward a more pro-growth stance including targeted fiscal measures and monetary easing. Together, these policies have driven a revival in risk sentiment and re-rating in valuations in 2025.

That said, we think investors should be more selective within Chinese equities and consider segments of the market delivering strong fundamental earnings growth such as the local tech sector which continues to be a key driver of local stock market returns.

Winning the AI race

With the US megacap hyperscalers ploughing billions of dollars into AI-related infrastructure to build leading edge frontier models, investors are now questioning whether this will pay off. As a result, evidence of AI monetisation will be ever more important this year which would favour companies that can demonstrate a clear path to profitability.

This trend is already playing out across China’s leading tech giants such as Alibaba who are using generative AI to improve the customer experience of its Taobao platform through personalised product recommendations and AI-driven search functions to assist with product discovery.

Merchants are also adopting an AI-powered marketing tool (Quanzhantui) which automates bidding and targeting across the entire platform, improving marketing efficiency. As a result, Alibaba’s AI-related product revenue continues to grow at triple digits for the eighth consecutive quarter1.

There are numerous other examples of AI monetisation occurring across China’s tech sector including Tencent which generates revenue from AI enhancements in gaming and advertising; and Baidu which has successfully integrated AI into their search and autonomous driving services.

China also has access to cheap, abundant energy resources which provide AI labs the capacity it needs to build larger, more power intensive GPU clusters that rival Nvidia’s accelerator chips. This, alongside rare earths, provide economic leverage against US export controls that have been aimed to curb the development of China’s local semiconductor ecosystem since 2022.

Source: Bloomberg Economics. As at July 2024.

From Seoul to Taipei: East Asia’s Semiconductor Powerhouses

Beyond the China tech sector, the AI capex juggernaut is supporting the broader semiconductor supply chain located across developed Asia, and includes companies such as Samsung, SK Hynix and Taiwan Semiconductor Manufacturing (TSMC).

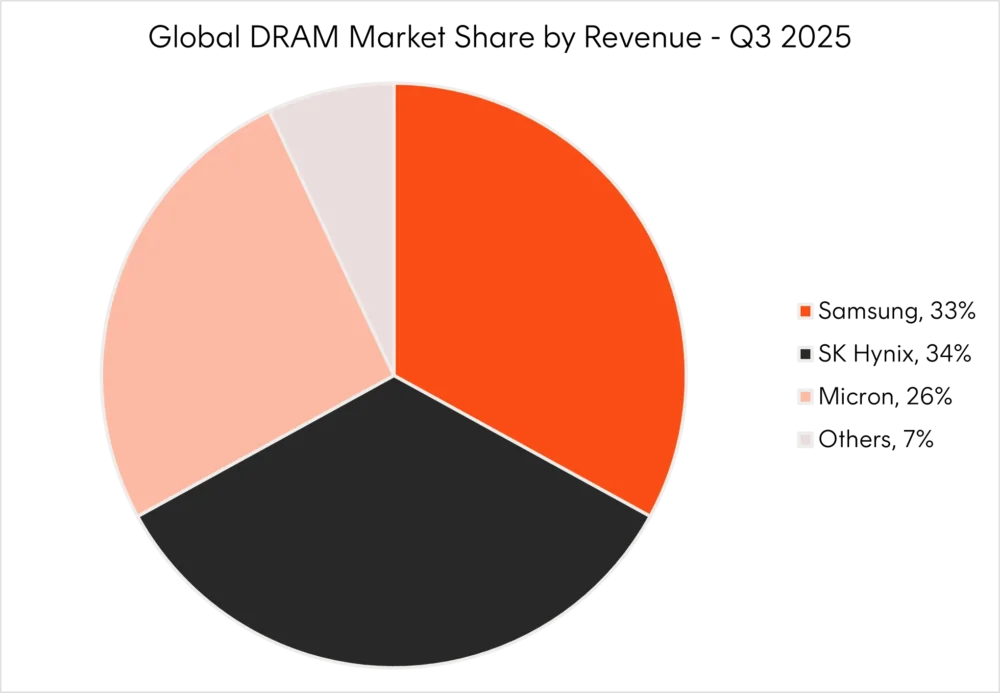

Samsung and SK Hynix are both leaders in memory chips – a critical component that sits within a graphics processing unit (GPU) to ensure huge amounts of data can be processed in a seamless manner. It is both the necessity of these chips and the relatively concentrated network of suppliers that have driven remarkable moves in memory prices, by some 40-50% in the final quarter of 20252.

Source: Counterpoint Research Memory Market Tracker and Forecast Report, Q3 2025

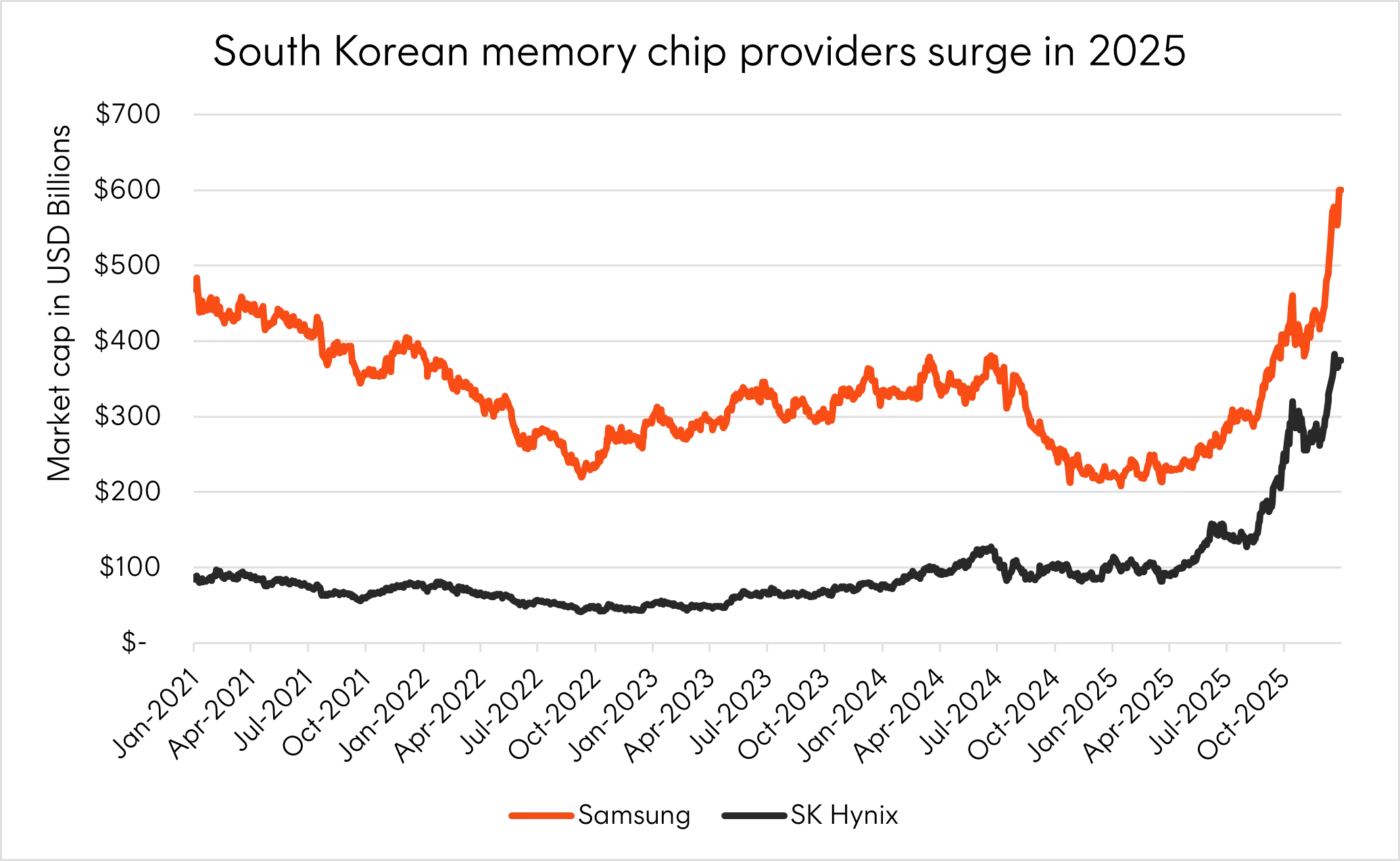

With supply scarce, company executives from major US tech giants are booking extended hotel stays in South Korea to negotiate critical HBM (high-bandwidth memory) supply, including Nvidia CEO Jensen Huang who inked a deal with Samsung boss Lee Jae-yong in October last year.

Source: Bloomberg. As at 19 January 2026.

TSMC is another important company in the supply chain that builds semiconductor chips based on designs provided by designers such as Nvidia and AMD. This model has allowed TSMC to refine its manufacturing capabilities over time and become the world’s leading foundry for AI accelerator chips, such as Nvidia’s Blackwell B200.

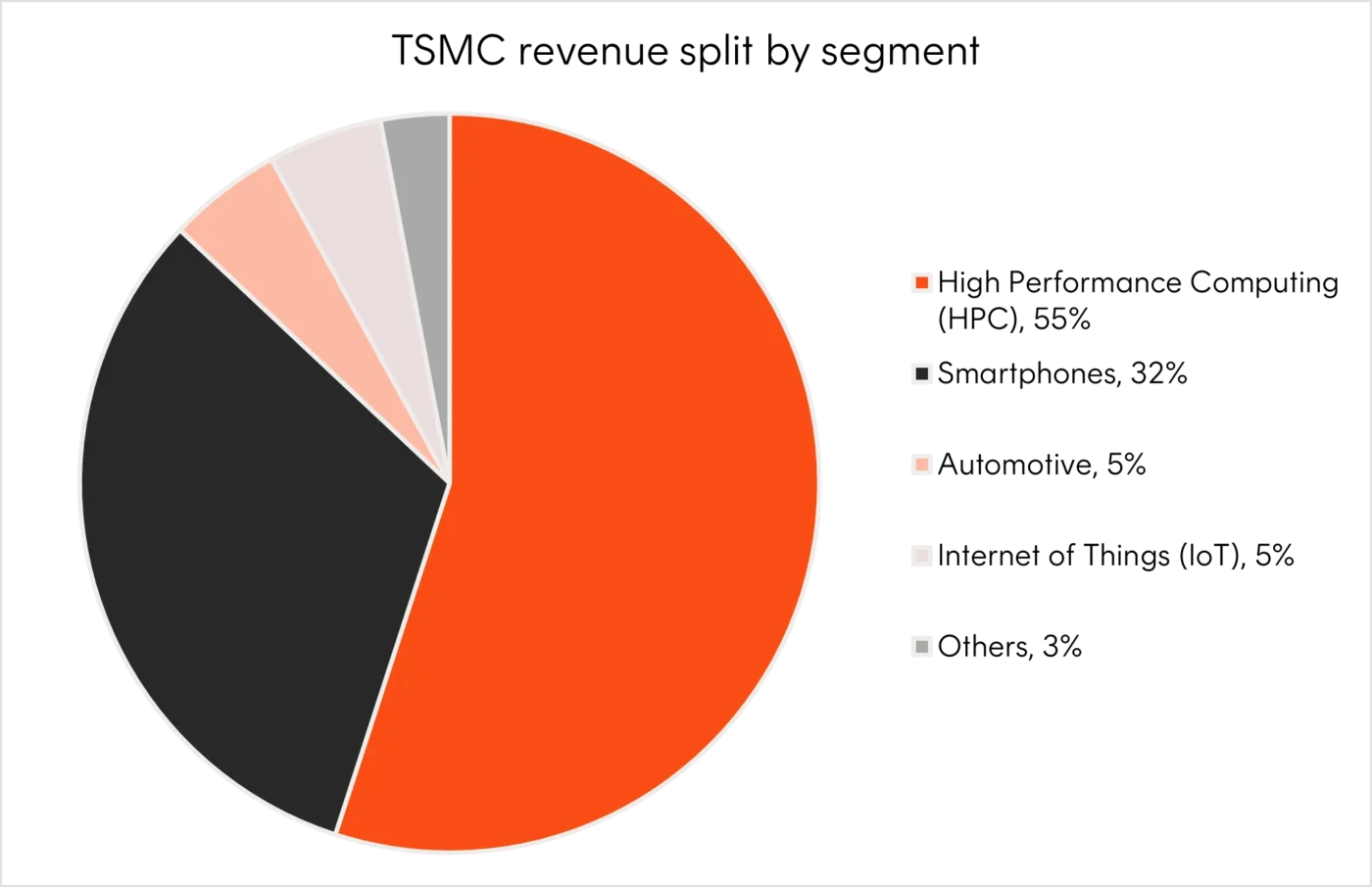

The Taiwan based company recently reported earnings growth of 35%3 year-over-year and higher than expected capex revisions, signalling clear underlying demand for AI. More than half of TSMC’s revenues are generated from high performance computing, which includes AI chips.

Source: TSMC Q4 2025 earnings report.

The recent US-Taiwan trade deal should also bolster the fundamental earnings of TSMC, with its chip exports receiving preferential treatment under the Section 232 tariff framework. In exchange, the company plans to invest US$250 billion in the US which would significantly enhance supply chain reliability for American tech giants.

Portfolio implications

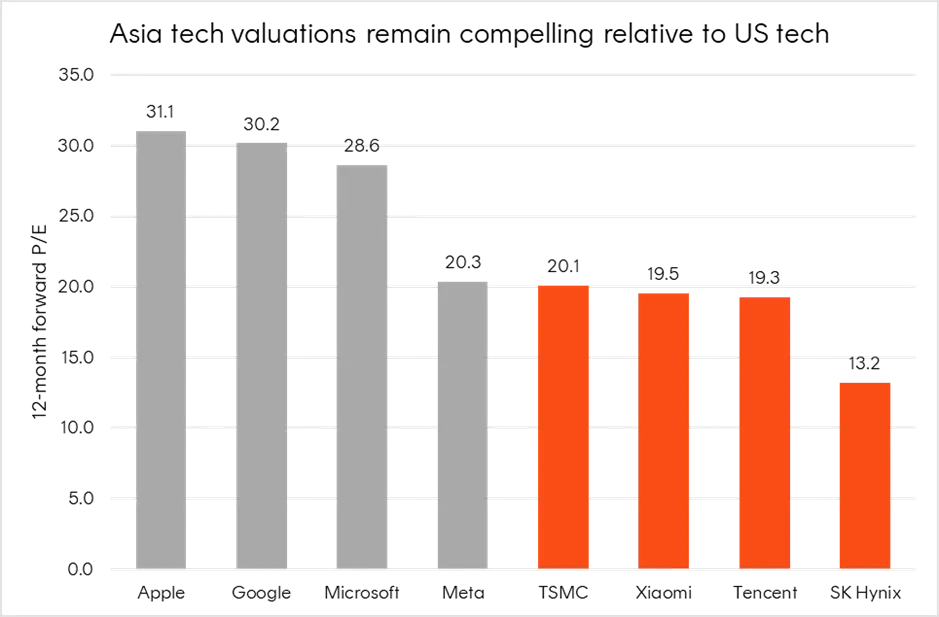

Importantly, many of these companies are currently trading at compelling valuation discounts relative to their US megacap tech counterparts, while delivering similar rates of earnings growth. Adding some exposure to Asian technology can also provide significant regional diversification benefits to US-centric investor portfolios.

Source: Bloomberg. As at 20 January 2026.

The bottom line

Technology and the rise of artificial intelligence have become a key driver of equity market returns for the last three years. Many megacap tech companies in the United States are ploughing billions of dollars into AI-related infrastructure capex to build frontier models.

While they remain key enablers of AI, we think investors should take a diversified approach to the global technology sector including leading companies across the Asian supply chain. As China’s AI capabilities continue to rise and the US seeks to bolster onshore semiconductor capabilities through strategic deals with Japan, South Korea and Taiwan; it is hard to deny the significance that this sector can provide for investor portfolios.

The Betashares Asia Technology Tigers ETF (ASX: ASIA) provides investors exposure to the 50 largest technology and online retail stocks in Asia (ex-Japan), including the companies mentioned in this article. ASIA has returned 43.73% over the 12 months ending 31 December 2025, and 14.32% p.a. since inception.

There are risks associated with an investment in ASIA, including information technology risk, concentration risk, emerging markets risk and currency risk. Investment value can go up and down. An investment in the Fund should only be considered as a part of a broader portfolio, taking into account your particular circumstances, including your tolerance for risk. For more information on risks and other features of the Fund, please see the Product Disclosure Statement and Target Market Determination, both available on this website.

This article may include opinions, views, estimates and other forward-looking statements which are subject to various risks and uncertainties. Actual results or events may differ materially. Any opinions expressed are not necessarily those of Betashares and are subject to change without notice. In preparing this information, Betashares has relied on, without verification, data sourced from external parties. Betashares does not warrant the accuracy or completeness of this information. To the extent permitted by law, Betashares accepts no liability for any loss arising from reliance on the information herein.

No assurance is given that any of the companies in the Fund’s portfolio will remain in the portfolio or will be profitable investments.

Sources:

1. https://www.alibabacloud.com/blog/alibaba-recognized-on-fortunes-2025-change-the-world-list-for-open-source-ai_602562 ↑

2. https://www.cnbc.com/2026/01/08/samsung-electronics-estimates-surge-skyrocket-profit-ai-memory-prices-q4.html ↑