David Bassanese

4 minutes reading time

Bonds and equities are more correlated than generally assumed

Many investors who believed in the value of diversified portfolios, such as one comprising both equities and bonds, were deeply scarred by the experience of 2022.

In that year, global equities declined, with the MSCI All Country World Return Index down 16% in local currency terms. Ordinarily, in a period of equity market weakness, bonds tend to be relied on to provide offsetting positive returns – as weak equities are usually associated with weak economic growth and falling interest rates.

Yet in 2022, bond returns were also negative, with the Bloomberg Global Aggregate Bond Index (in $A hedged terms) down 12.3%. Where was the diversification!

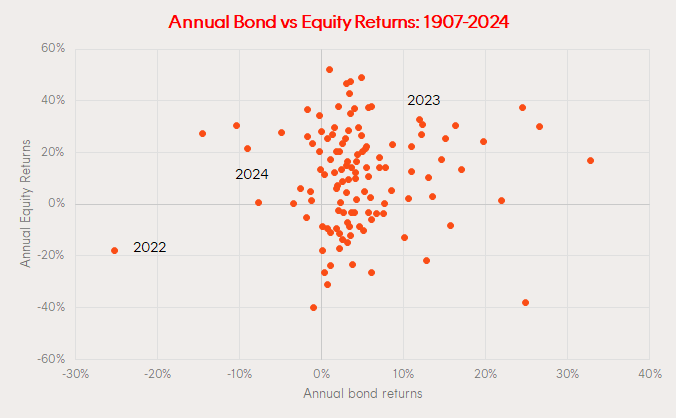

But wait, there’s more! Investors might be further concerned to know that the correlation between equity and bond returns has tended to be more positive than negative over time. As evident in the chart below, in the 118 years to 2024, the direction of global bond and equity returns (i.e. either positive or negative) were the same in 72 of those years or 61% of the time.

Source: Bloomberg, Lombard Odier. Bond and equity returns related to US markets, with global equity and bond benchmarks used updates in 2023 and 2024.

That said, in 69 of these 72 years (or 96% of the time), the positive correlation was because both bonds and equities delivered positive returns – as was the case, for example, in both 2023 and 2024.

It should not matter so much to investors if bond returns were correlated with equity returns – provided both are going up. Many of these years likely covered periods of declining inflation whilst growth remained solid.

But bonds usually provide diversification when you most need it

The key point for investors, however, is that bonds have usually provided diversification when you really need it – namely when equity markets are under downward pressure.

Indeed, in the 34 years in which equities suffered negative returns, bonds also produced negative returns in only three years – or just 9% of the time. Bonds produced positive returns in 31 of these years, or 91% of the time.

What this suggests is that when equity markets decline, usually due to negative economic shocks, bonds provide diversification, as central banks are often acting to cut interest rates and support the ailing economy.

118 Years of Bond & Equity Returns

|

Equities |

|||

|

Positive years |

Negative years |

||

|

Bonds |

Positive years |

69 |

31 |

|

Negative years |

15 |

3 |

|

Source: Bloomberg, Lombard Odier.

There are exceptions – and 2022 was an extreme one!

It is against this background that we can see that 2022 was such an outlier in terms of experience. This was the only year in this 118-year period in which both bonds and equities produced annual declines of more than 10%.

2022 was truly exceptional because of the extreme economic whiplash caused by the COVID crisis. COVID initially caused a slump in economic demand and supply over 2020 and 2021, which central banks responded to by slashing official interest rates to near-zero levels – and then promised to keep them there for some time. This sent bond yields to historic lows.

Yet in 2022, as demand rebounded ahead of supply capacity, inflation took off – which forced central banks into a massive U-turn and into aggressive policy tightening cycles. The surge in bond yields hurt equity markets by crushing valuations – which had become elevated during the initial V-shaped economic recovery over 2020 and 2021.

Given this context, it’s no surprise that both bond and equity returns in 2022 were negative – bonds sold off due to monetary policy tightening, with these high yields and associated concerns over the economic outlook hurting equity valuations.

In short, in periods in which inflation is rising and central banks embark on monetary tightening campaigns, it’s possible for both bond and equity returns to both be negative for a time – in these periods bonds, per se, can’t provide the diversification investors desire. That is when better inflation hedged assets, such as commodities, like gold, could provide greater portfolio diversification.

Indeed, a similar situation took place in the late 1960s, when US inflation lifted and the Federal Reserve had to embark on aggressive policy tightening – both US bond and equity returns were negative, for example, in 1969.

History suggests, however, that these periods tend to be fairly rare and often short-lived – and even then, once policy tightening has had its desired effect in slowing the economy, bonds returns can turn positive even as equity returns may remain negative for a while longer.

The bottom line

All up, 2022 was truly an exceptional period in terms of bond and equity performance – consistent with the exceptional economic period during the COVID crisis. But more often than not, bonds have provided investors diversification in time of equity market stress. And when they have not, the combination of negative returns in both bond and equity markets usually does not last long.