David Bassanese

6 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the player below:

Global week in review: Good profits, but the Strait is still closed

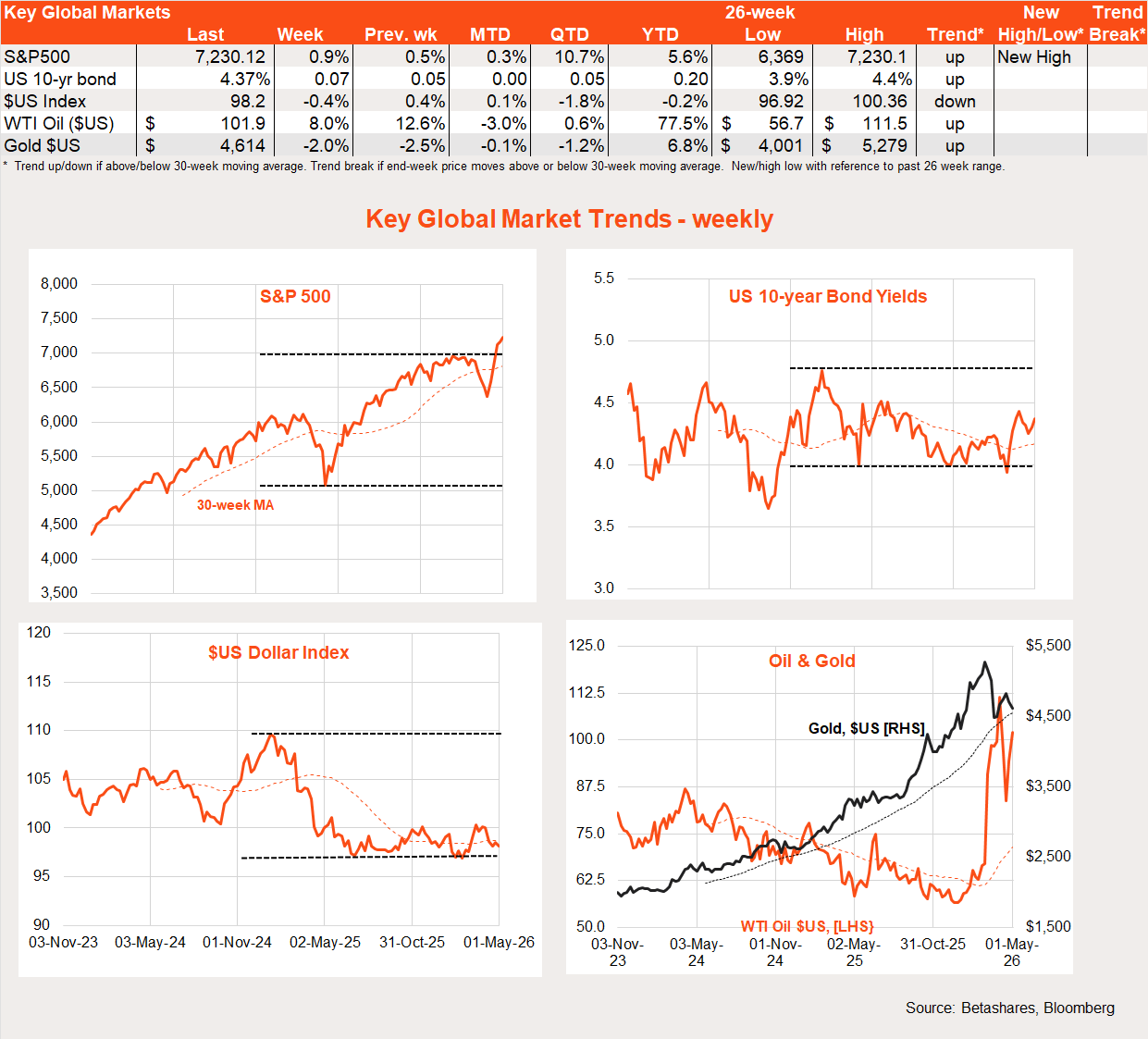

US stocks rose further last week – the 5th weekly gain in a row – despite a rebound in oil prices and the continued closure of the Strait of Hormuz. Strong Q1 corporate earnings and ongoing hopes for a US-Iran peace deal supported stocks.

US economic data took a back seat again last week, although the results were generally market supportive.

At 2.0% annualised, US Q1 GDP growth came in a little weaker-than-expected – but still not bad. Consumer spending remained subdued at a below 2% annualised pace, though GDP growth picked up from the 0.5% annualised rate in Q4, thanks to a rebound in public spending (with a re-opening of the Federal Government) and a further ramp-up in business investment due to the AI boom.

March consumer prices – as measured by the consumption deflator – were in line with market expectations, with core prices up 0.3% in the month and 3.2% over the year.

Other key news related to Iran and earnings. The bad news is that the Strait of Hormuz is still closed, with no peace deal in sight. The looming reality of a supply-side crunch led to a rebound in oil prices last week. Indeed, as noted, the longer the Strait stays closed, the greater the inevitability of a major supply-side energy crunch as remaining inventories are run down. The clock is ticking.

But the good news is that peace proposals are at least being bandied about – the US blockage of Iranian ships seems to be encouraging Iran to want to make a deal. Yet so far at least, Trump does not seem under sufficient political pressure to make a less-than-perfect deal – maybe higher oil prices in the coming weeks could change his mind. The costs of continuing the war are mounting for both sides, and markets are just waiting for one side to blink first.

More good news came from the US earnings reporting season. Most of the major Mag-7 results pleased investors last week. Their sales and profits were all generally still strong, despite the heavy ongoing investments in AI. According to FactSet, 84% of the 63% of S&P 500 companies that have reported Q1’26 earnings so far have beaten market estimates, which is above the long-run average of around 75%.

As expected, all of the major central banks that met last week decided to leave interest rates on hold. Yet while the US Federal Reserve left rates steady, markets were knocked momentarily by a shift in language towards a more neutral rather than easing policy bias. Yet even though the Fed concedes US inflation is “elevated”, it’s still debating if and when to cut rates further rather than raise them!

Global week ahead: Iran and payrolls

As stated above, markets are essentially in limbo – there’s no clear pathway to a ceasefire deal which could open the Strait of Hormuz, which means global supply pressures are only likely to intensify in the weeks ahead. Markets will continue to hold out hope for a peace deal soon.

Other key news will be US payroll data on Friday. A moderate 70k April gain in employment is expected, which should keep the unemployment rate steady at 4.3%.

Global equity trends: US outperforms

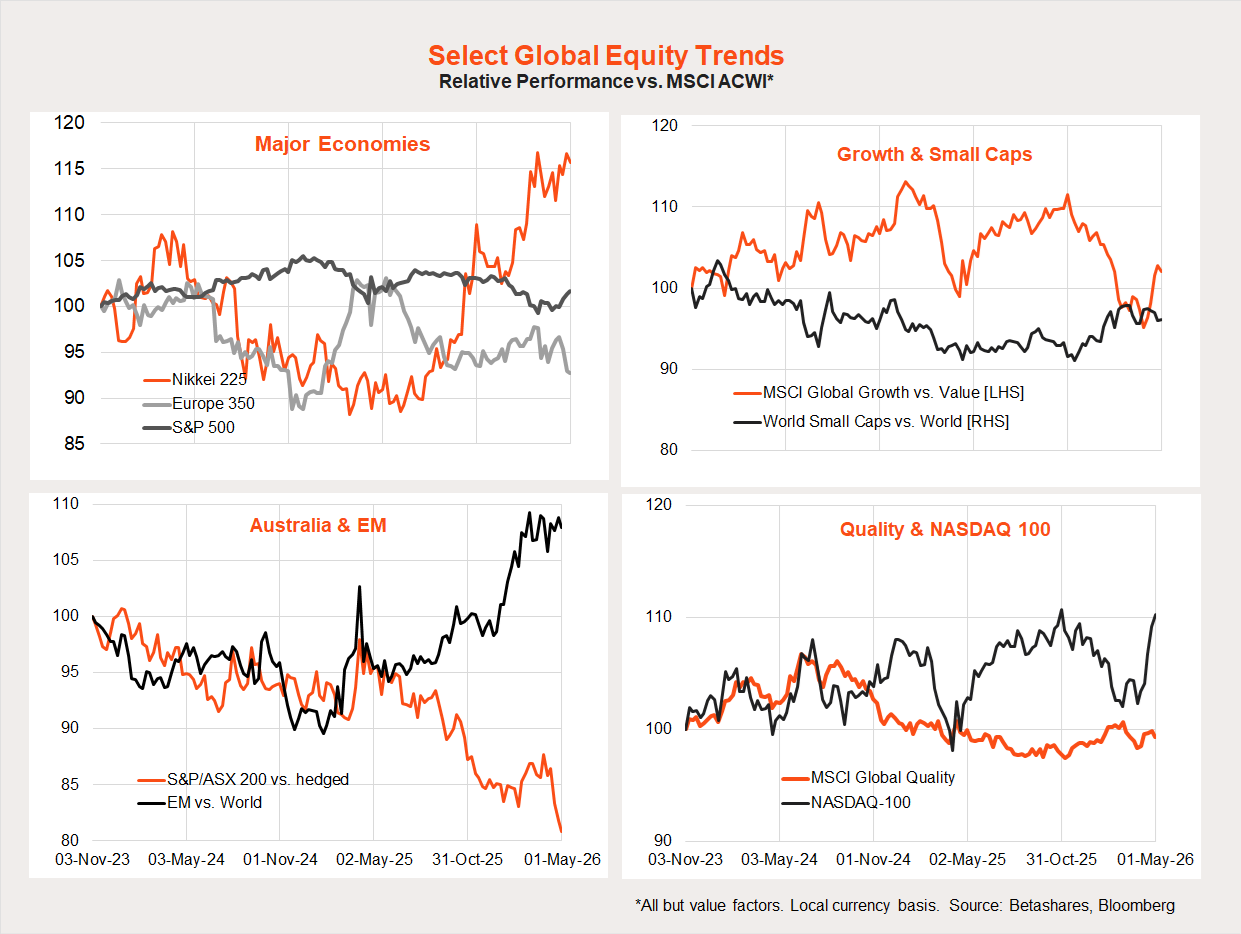

Global equity markets have now staged a remarkable 5-week rebound on peace talk hopes. Indeed, overall global stocks and the S&P 500 are now trading above the levels prevailing just before the Iran war began.

The US, Japan and emerging markets have done reasonably well in this rebound so far, whereas Europe, Australia and small caps have not. The Nasdaq 100 has shot the lights out.

Australia in review: Inflation fear

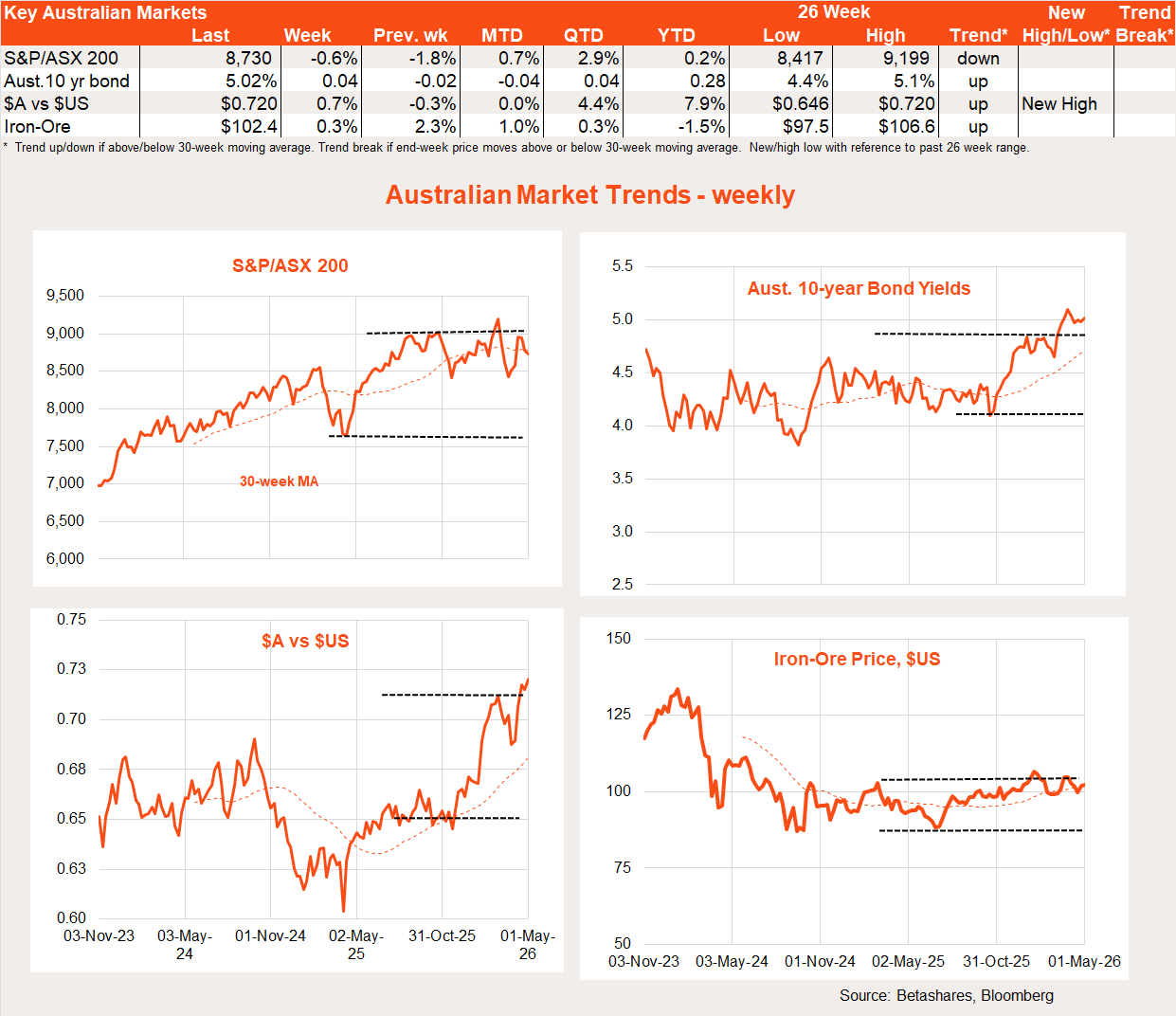

Local stocks underperformed global stocks again last week, with a firm Q1 inflation report adding to concern over an RBA rate hike tomorrow.

Although the March quarter consumer price index (CPI) report was a touch softer than feared, it was not good enough to convincingly rule out the risk of an RBA rate hike this week. The all-important trimmed mean measure of underlying inflation rose 0.8% in the quarter (market 0.9%), which dragged up the annual rate from 3.4% to 3.5%.

One encouraging sign is that the rate of growth in quarterly trimmed mean inflation has at least decelerated over the past three quarters – from 1.0% in Q3 ’25, 0.9% in Q4 ’25, to 0.8% in Q1’26. And that’s despite a 35% surge in petrol prices in the month of March.

Local equity market trends: Technology/small caps bottoming out?

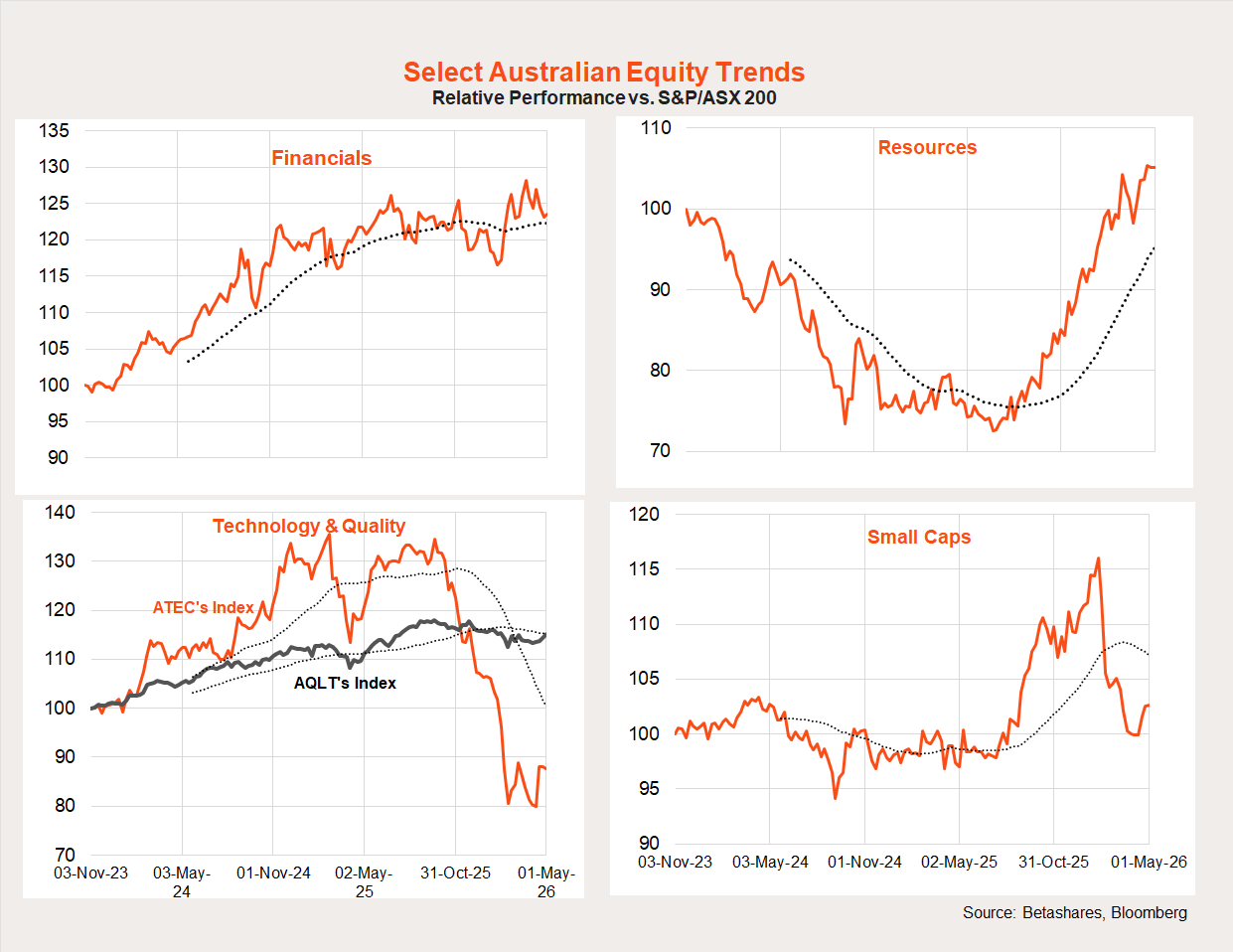

The Iran war had initially not been kind to high-beta local exposures such as technology and small caps. That said, the relative performance of both these areas has bottomed out in recent weeks, while resource company relative performance has resumed at the expense of financials.

Australia week ahead: RBA to likely hike

With underlying inflation still running above the RBA’s 2-3% target, tight labour and product markets, and the ever-present risk of higher petrol prices, the RBA still seems likely to raise rates this week.

Of course, it’s not a done deal however, there is uncertainty of how the gaggle of independent Board members will vote. Recall that back in March, several Board members voted to delay a rate hike until May – they may feel a rate hike is now not needed given the March move. The slump in both business and consumer confidence last month could also weigh on RBA thinking.

My view, however, is that the added upside inflation risk from the extended Iran war means most Board members will now concede the need for another rate hike – even though they may not have felt that a month ago. Weak confidence is regrettable but necessary if the economy is to slow down again and help rein in inflation.

Have a great week!