David Bassanese

5 minutes reading time

If you’d prefer to listen to this week’s edition in podcast form, please click the below player:

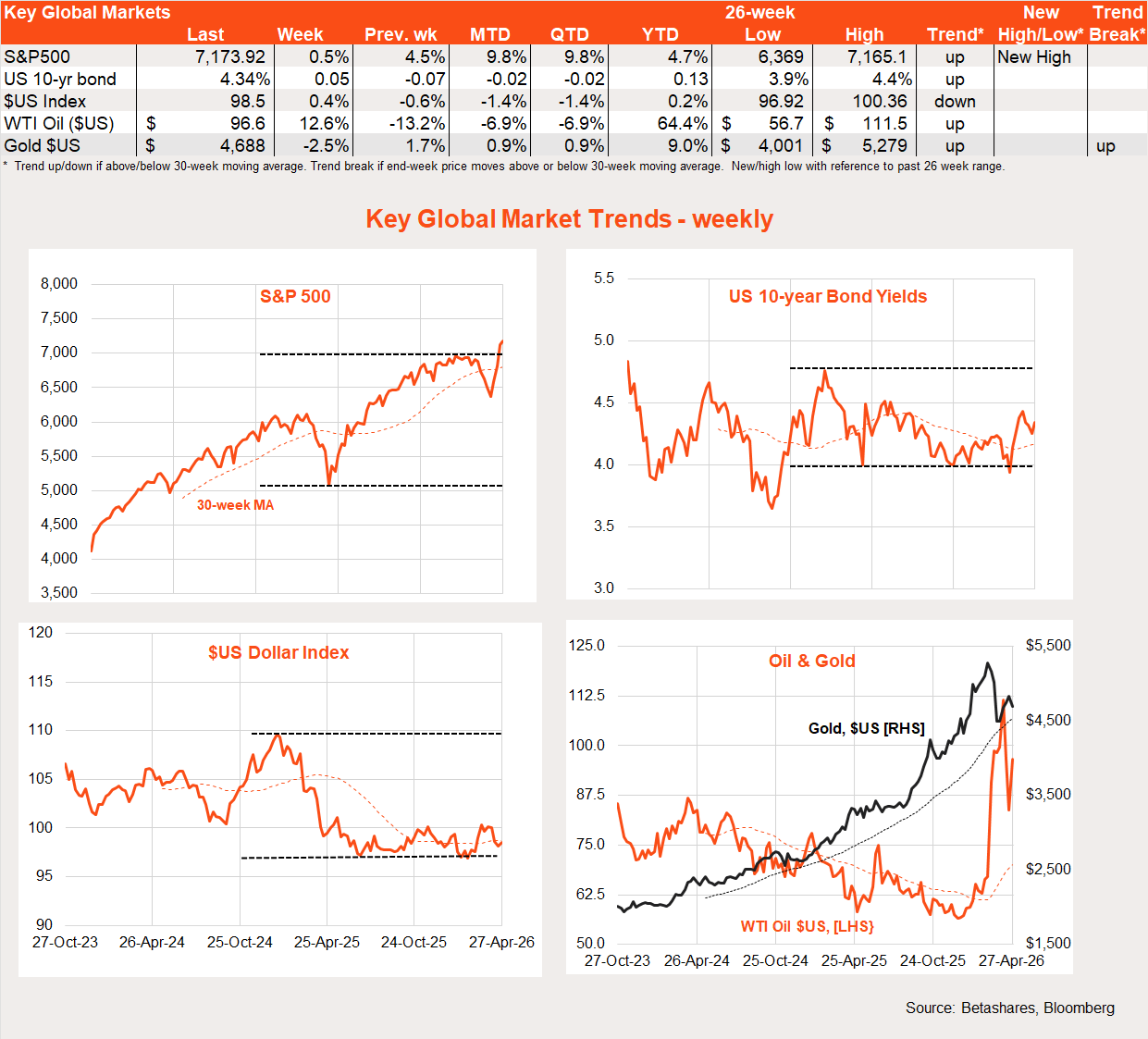

Global week in review: The Strait still closed

US stocks have on balance edged higher since Friday’s close on 17 April, reflecting US-Iran ceasefire hopes and a continued solid earnings outlook.

Global markets continued to be buffeted last week by on-again off-again peace talks. The major development was Trump’s announcement of an indefinite ceasefire (he’s grown tired of extending two-week deadlines!) due to an apparent fracturing of the Iranian negotiating team.

Fractured or not, Iran soon responded by offering a partial deal, whereby both sides agreed to unblock the Strait of Hormuz with an agreement on Iran’s nuclear activity negotiated later.

At the time of writing, the US appears to have rejected the deal. That’s perhaps not surprising, as this would only take us back to the pre-war position – with no other progress on the nuclear question despite decimation of Iran’s conventional military capacity.

So markets are left in limbo. The bad news is the Strait is still closed, with a major global supply side crunch looming once existing inventories are depleted. The good news is both sides still appear to want to make a deal, but the game of brinkmanship remains. It’s a question of which side will suffer the most pain from the Strait being closed – for Trump it may be a case that oil prices need to lurch higher and/or equity markets sink further before the TACO trade comes back into play.

Also helping support equity markets are early signs of another bumper US earnings reporting season. According to FactSet, 84% of the 28% of S&P 500 companies that have reported Q1’26 earnings so far have beaten market estimates, which is above the long-run average of around 75%.

As strange as this sounds, the weekend’s third apparent assassination attempt on President Trump should not cause too many ripples for markets. The would-be lone-wolf assassin was quickly subdued and business in Washington seems likely to return to normal fairly soon.

Global week ahead: Iran, earnings & inflation

As stated above, markets are essentially in limbo – there’s no clear pathway to a ceasefire deal which could open the Strait of Hormuz, which means global supply pressures are only likely to intensify in the weeks ahead.

So far at least, the rundown in existing inventories (from strategic reserves and ships already at sea before the Strait was closed), the deployment of alternate trade routes and some early demand destruction has limited upside pricing pressure. But, if nothing changes, higher prices and more demand destruction seem likely in the weeks ahead. This is true not just for oil but for a range of commodities, including LNG and fertilizer.

In other news, most of America’s major tech companies report earnings this week, including Alphabet, Microsoft, Meta, Amazon and Apple. My sense is that fears of massive AI disruption to the major players is dissipating, as AI is allowing them to cut costs (as evident from regular job cut announcements) while demand from their own customers is (so far at least) holding up.

On the economic front, US inflation data on Friday is likely to show this remain a simmering issue, albeit down the ranking of market worries at present. The core consumption deflator is expected to rise 0.3% in March, taking annual core inflation to 3.2% from 3.0%. The headline measure (which includes energy prices) will naturally be worse, with an expected monthly rise of 0.7%, lifting annual inflation from 2.8% to 3.5%.

The Fed also meets this week but is expected to leave rates firmly on hold. A range of other central banks also meet – in Europe, the UK, Japan and Canada – and are also expected to leave rates steady.

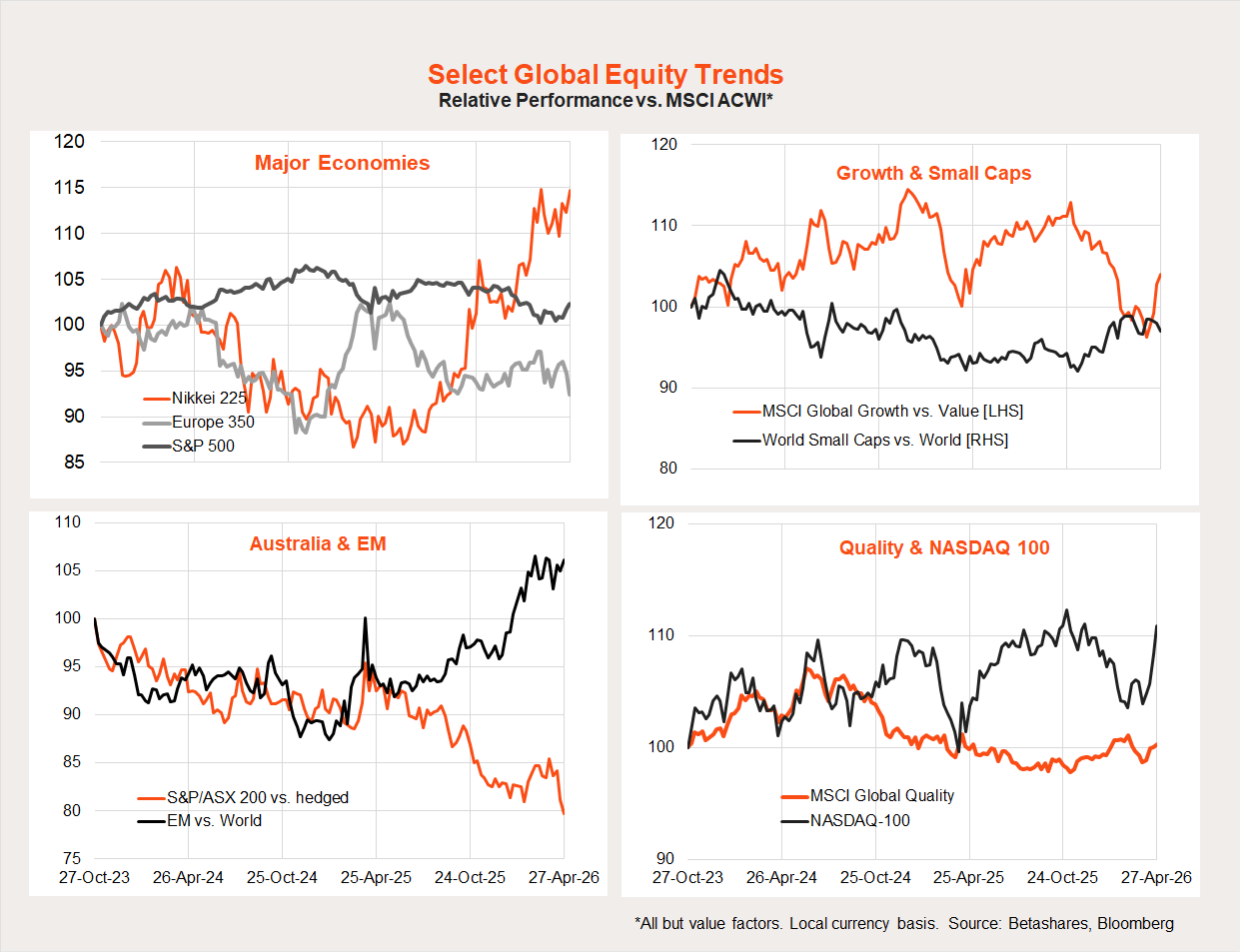

Global equity trends: US outperforms

Global equity markets have now staged a remarkable one month rebound on peace-talk hopes. Indeed, overall global stocks and the S&P 500 are now trading above the levels prevailing just before the Iran war began.

The US, Japan and emerging markets have done reasonably well in this rebound so far, whereas Europe and Australia have not. The NASDAQ-100 has shot the lights out.

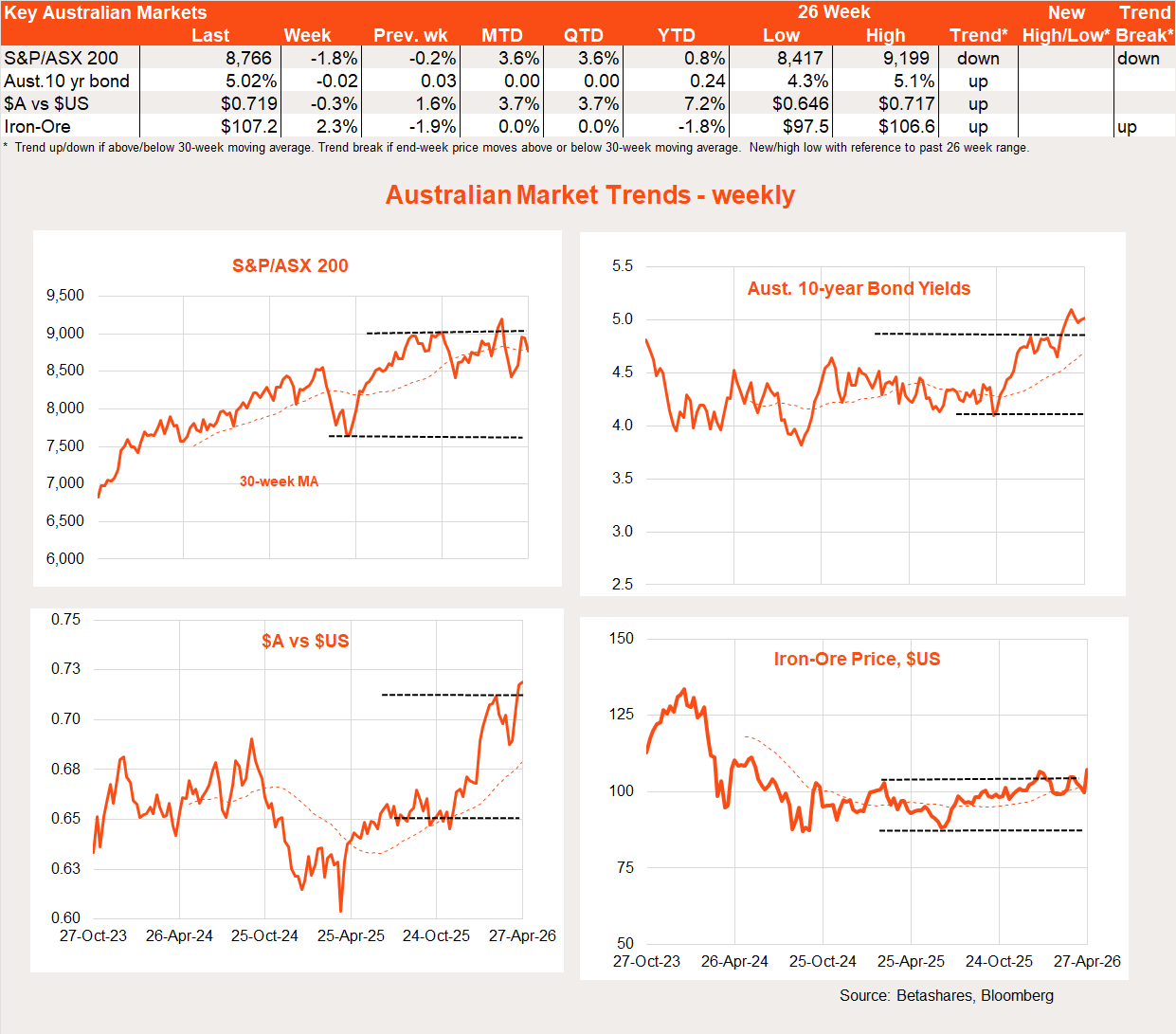

Australia in review: Inflation fear

With limited local economic news last week, local stocks sagged further.

With ongoing upward pressure on energy prices, the local market remains fearful of this week’s Q1 consumer price index report – which is likely to be uncomfortably high and confirm another likely rate hike by the RBA next month. In turn, this is hurting the local corporate earnings outlook.

At the same time, Federal budget speculation builds: recent reports suggest a new gas tax has been mothballed, whereas property investors remain in the government’s sights.

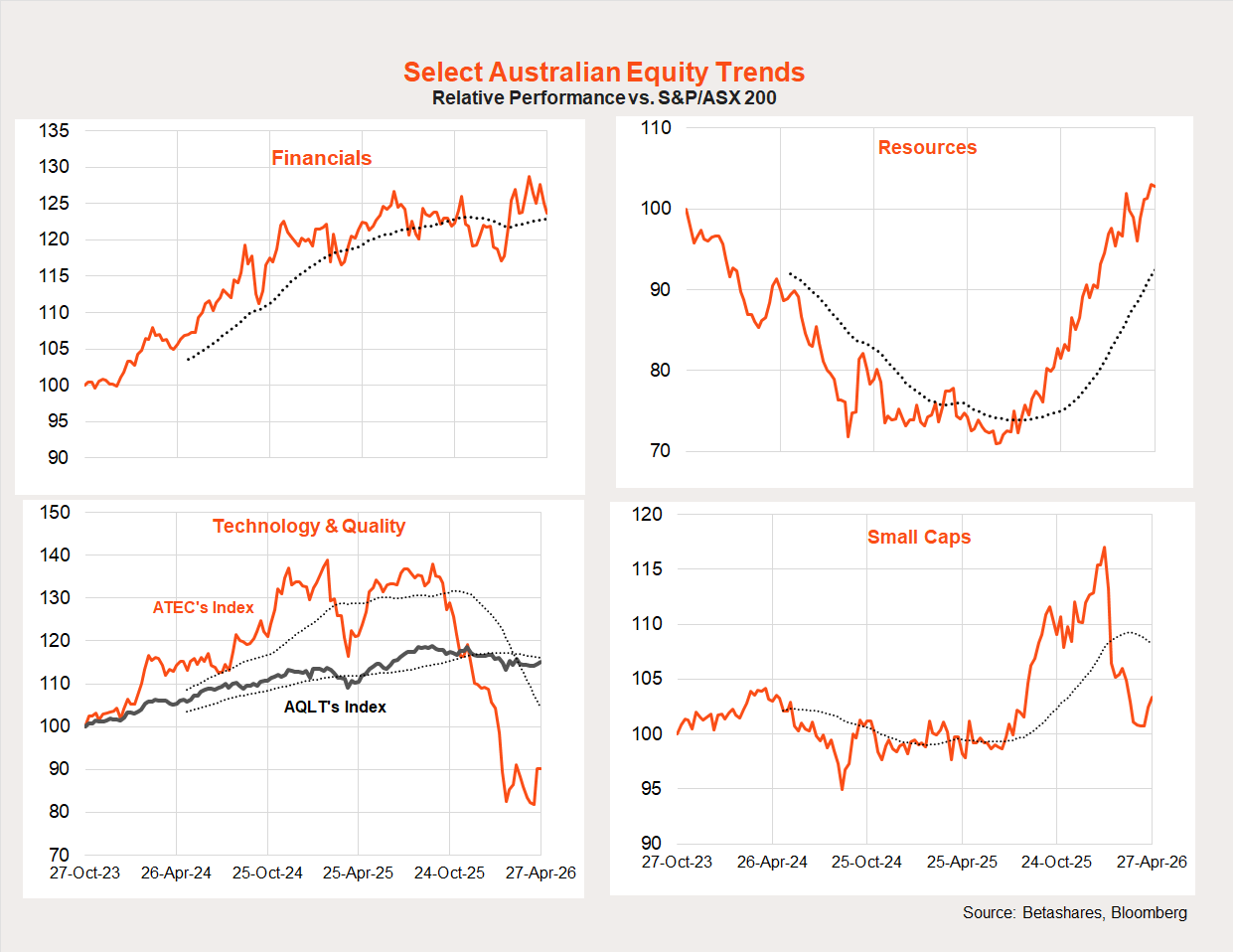

Local equity market trends: Technology/small caps bottoming out?

The Iran war had initially not been kind to high-beta local exposures such as technology and small caps. That said, the relative performance of both these areas has bottomed out in recent weeks, while resource company relative performance has resumed at the expense of financials.

Australia week ahead: Iran

Quarterly inflation tomorrow is the big story locally this week.

As it stands, the market expects a 0.9% quarterly gain in trimmed mean inflation, which would lift annual underlying inflation from 3.4% to 3.5%. The Australian Bureau of Statistics – now focused on the monthly report – may well take great delight in burying this one key statistic in an obscure spreadsheet once again.

Have a great week!