David Bassanese

5 minutes reading time

Better investing starts here

Get Betashares Direct

Betashares Direct is the new investing platform designed to help you build wealth, your way.

Scan the code to download.

Learn more

Learn more

Key global developments in April

- Fear turned to hope with on-again/off-again cease fires and peace talks leading markets to anticipate a speedy end to the US-Iran war. Optimism prevailed despite the Strait of Hormuz remaining closed and oil prices lifting further.

- A strong Q1 US earnings reporting season also bolstered sentiment, with fears around the AI impact on Mag-7 stocks dissipating somewhat.

- In Australia, solid employment growth and high inflation readings – not helped by the Iran-related surge in oil prices – has markets fearing higher interest rates and weaker corporate earnings.

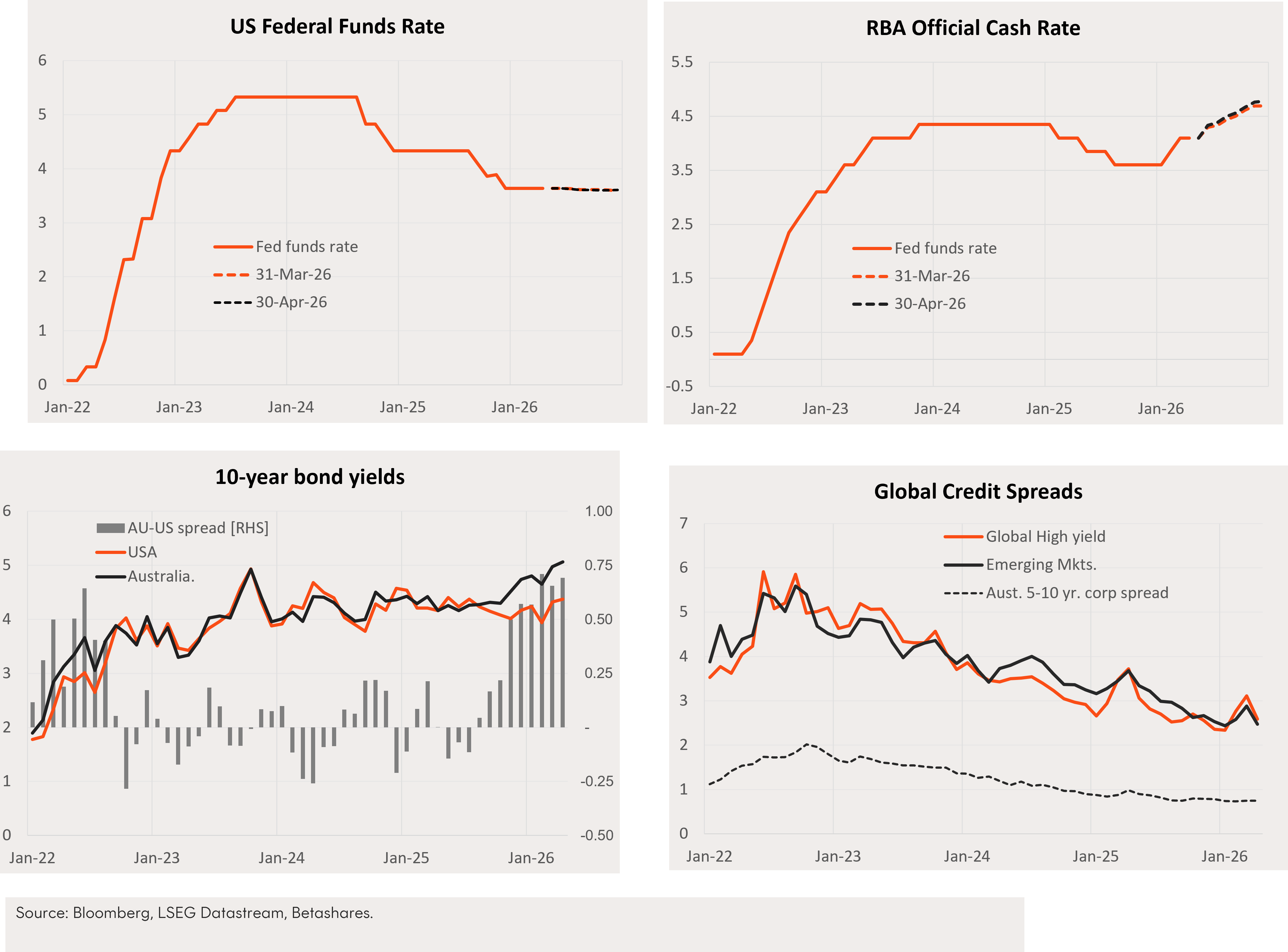

Interest rates

- There was little change in US policy expectations over April, though policy tightening expectations lifted slightly further in Australia. Markets still anticipate a steady policy outlook this year in the United States, yet one to two further rates hikes in Australia, beyond the recently-delivered May rate hike.

- US and Australian 10-year bond yields rose only modestly, by 0.05% in the US to 4.37% and 0.09% in Australia to 5.06%. Bond yields remain range bound in the US, but have been trending higher in Australia since late-2025.

- After widening in March, global credit spreads re-tightened in April and local credit spreads remain contained.

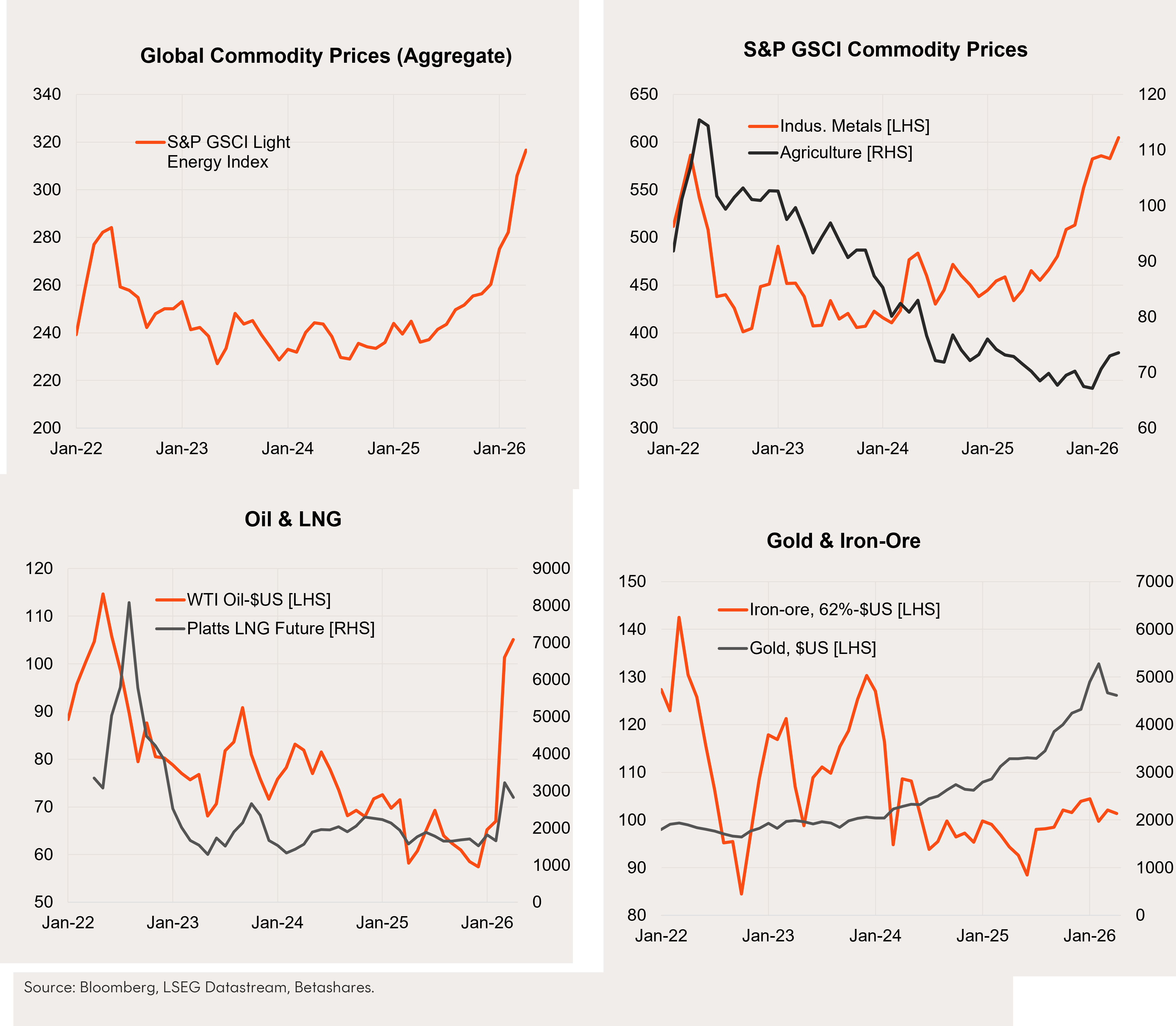

Commodity prices

- Commodity prices generally strengthened further in April, reflecting gains in oil and industrial metals. Gold prices fell back further, however, after also declining in March. LNG prices also eased back following their March surge. Iron-ore prices remained relatively steady.

Exchange rates

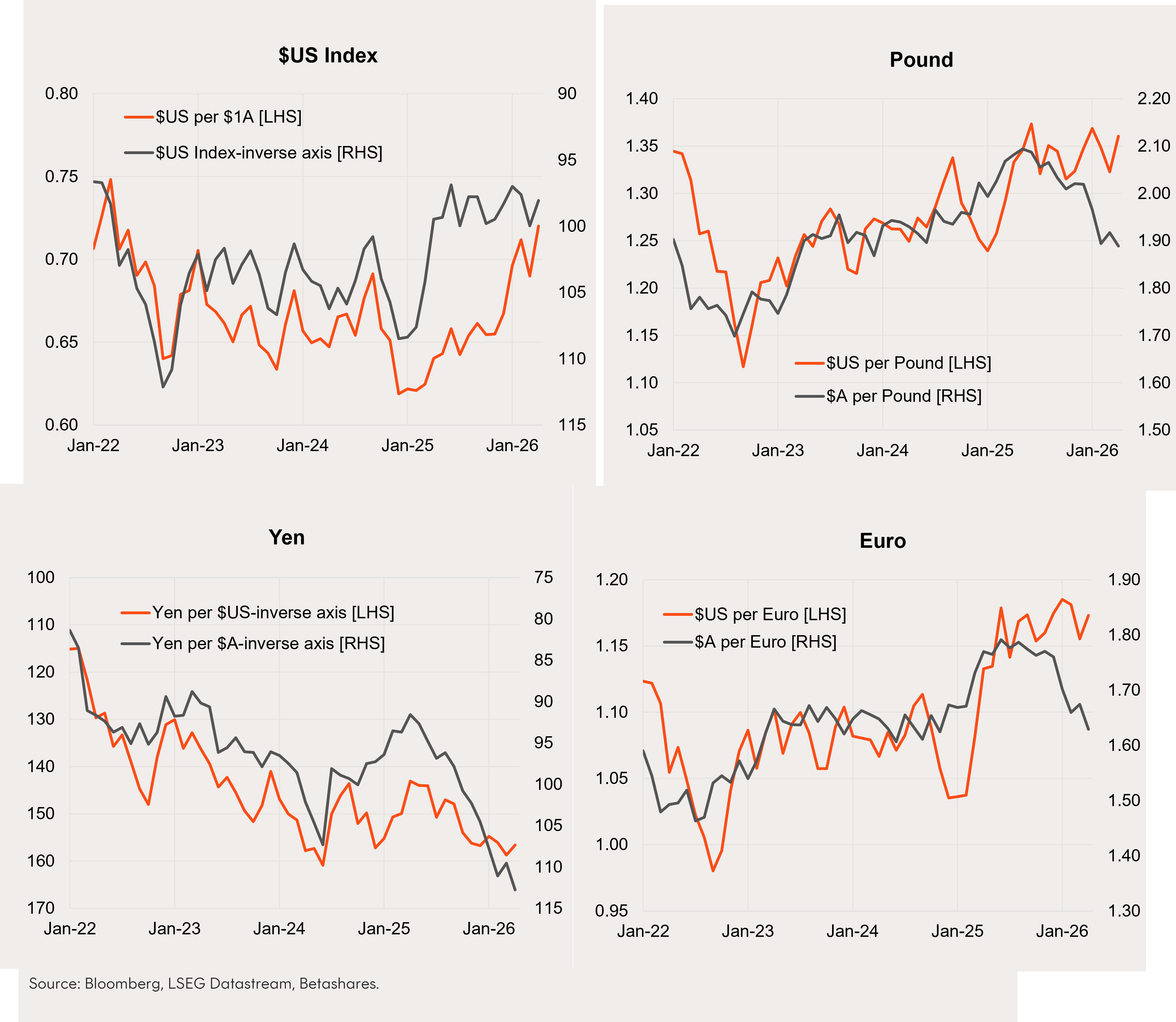

- The Australian dollar generally strengthened in April, lifting 4.3% against the $US to $US72c. The $A has been in a solid uptrend since early 2025 against most major currencies, reflecting both firmer commodity prices, a softer $US and local rate hike expectations.

- The $US Index eased back in April, although it’s been broadly range bound over the past year followings its decline in early 2025. While range bound against the Euro and Pound, the $US – like the $A – has been generally strengthening against the Yen.

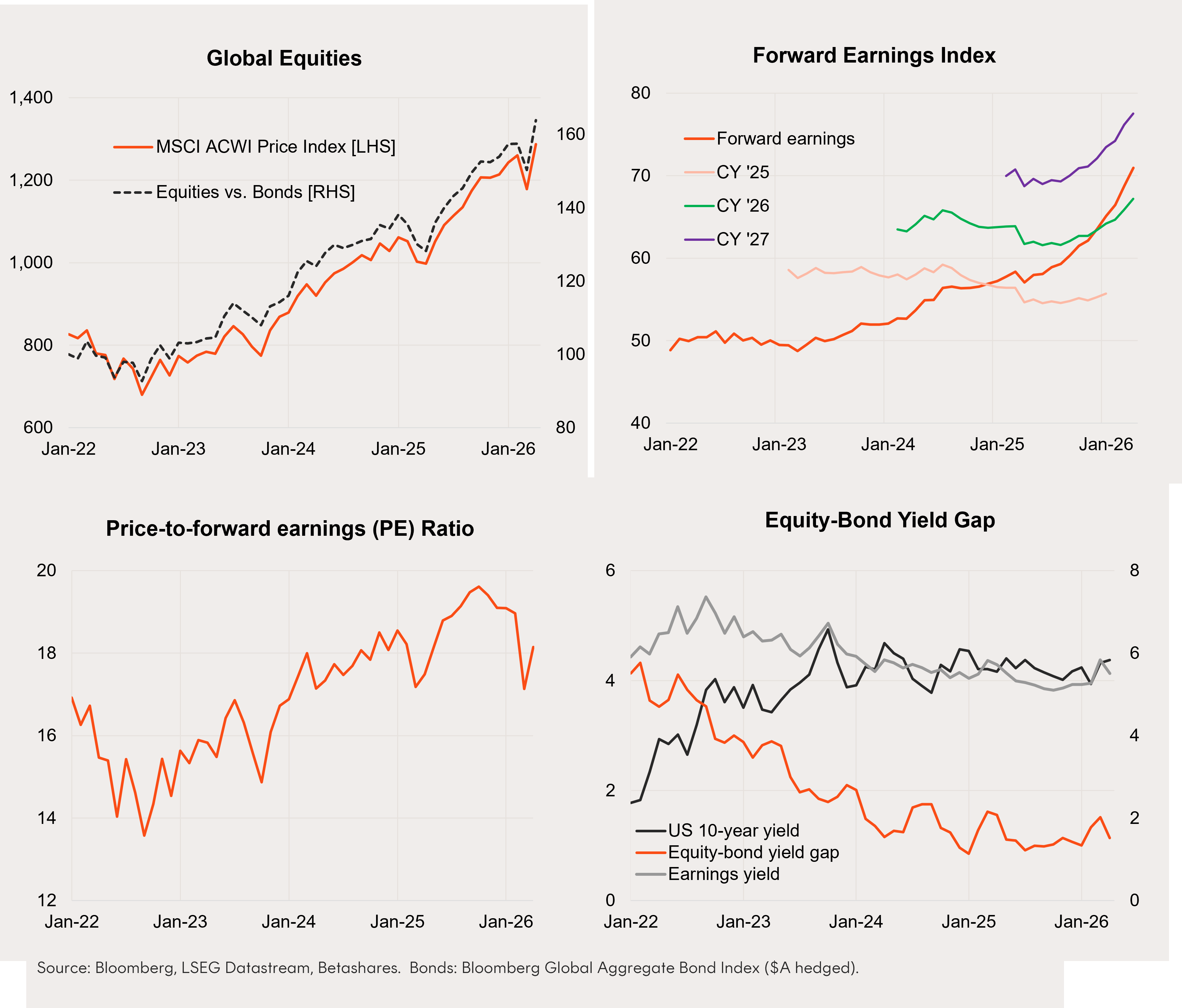

Global equities

- Global equities rebounded in April, reflecting hopes for a US-Iran peace deal and a solid US earnings reporting season. The MSCI ACWI Index returned 9.4% in local currency terms, following a decline of 6.3% in March.

- Despite war concerns, global earnings expectations remain upbeat and forward earnings continue to rise – with 14% expected growth over the next 12 months. The March sell-off, along with rising forward earnings, have helped improve global equity valuations, with the forward PE ratio ending April at 18.1 following a recent peak of 19.6 in October last year.

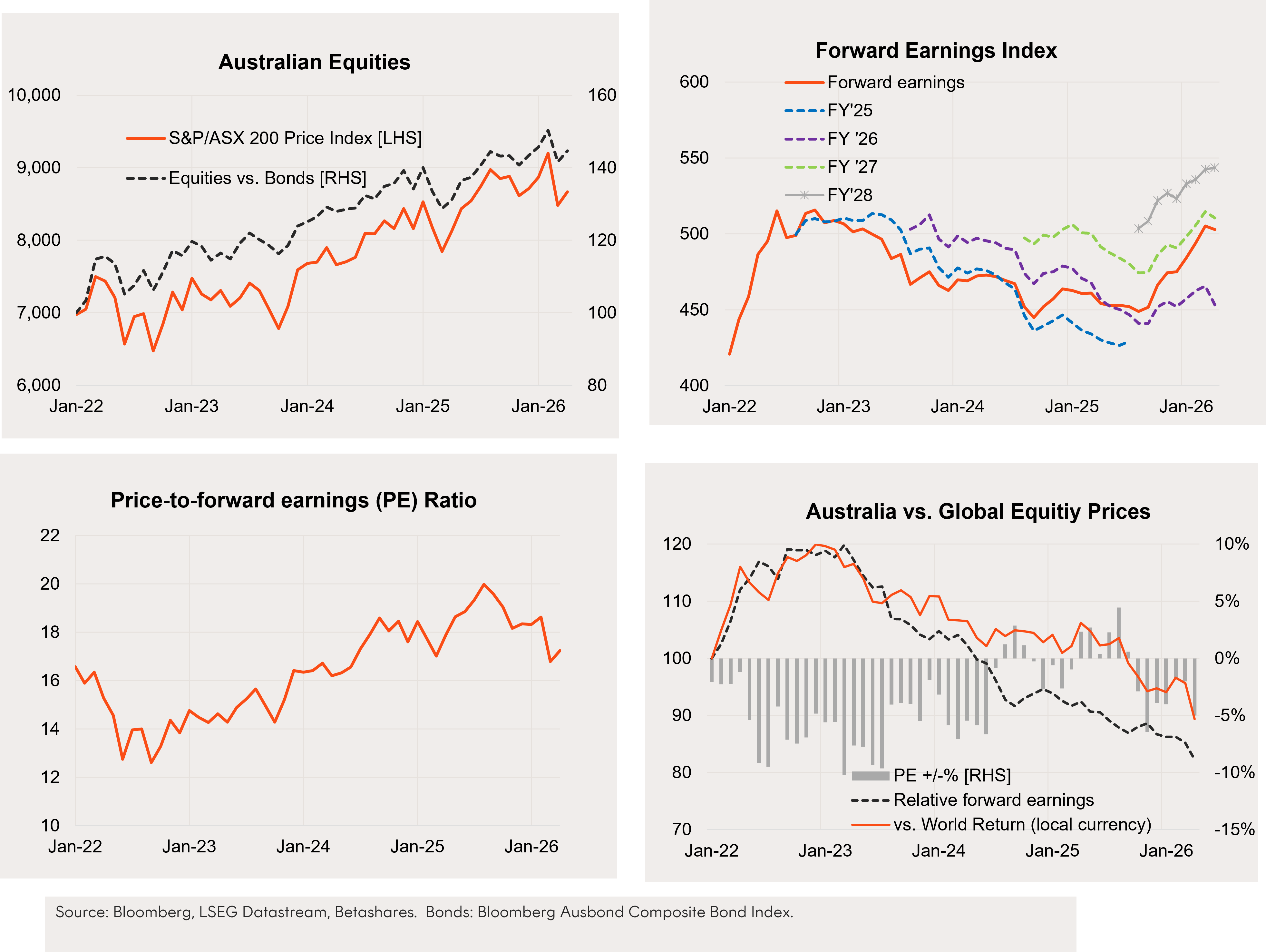

Australian equities

- Australian equities also rebounded in April, though a little less than global markets, with the S&P/ASX 200 returning 2.2% following a sharp 7.8% decline in March.

- Although earnings growth expectations remain positive, there was a modest downgrade to expectations in April due to local economic growth and interest rate concerns. Over the next 12 months, forward earnings are expected to grow by 8%, or modestly less than the global expectation.

- A solid upturn in forward earnings since mid-2025 has helped improve local equity valuations, with the forward PE ratio ending April at 17.2 – down from a recent peak of 20 in August last year. Local stocks are trading at a modest 5% discount to global stocks.

Equity themes/trends

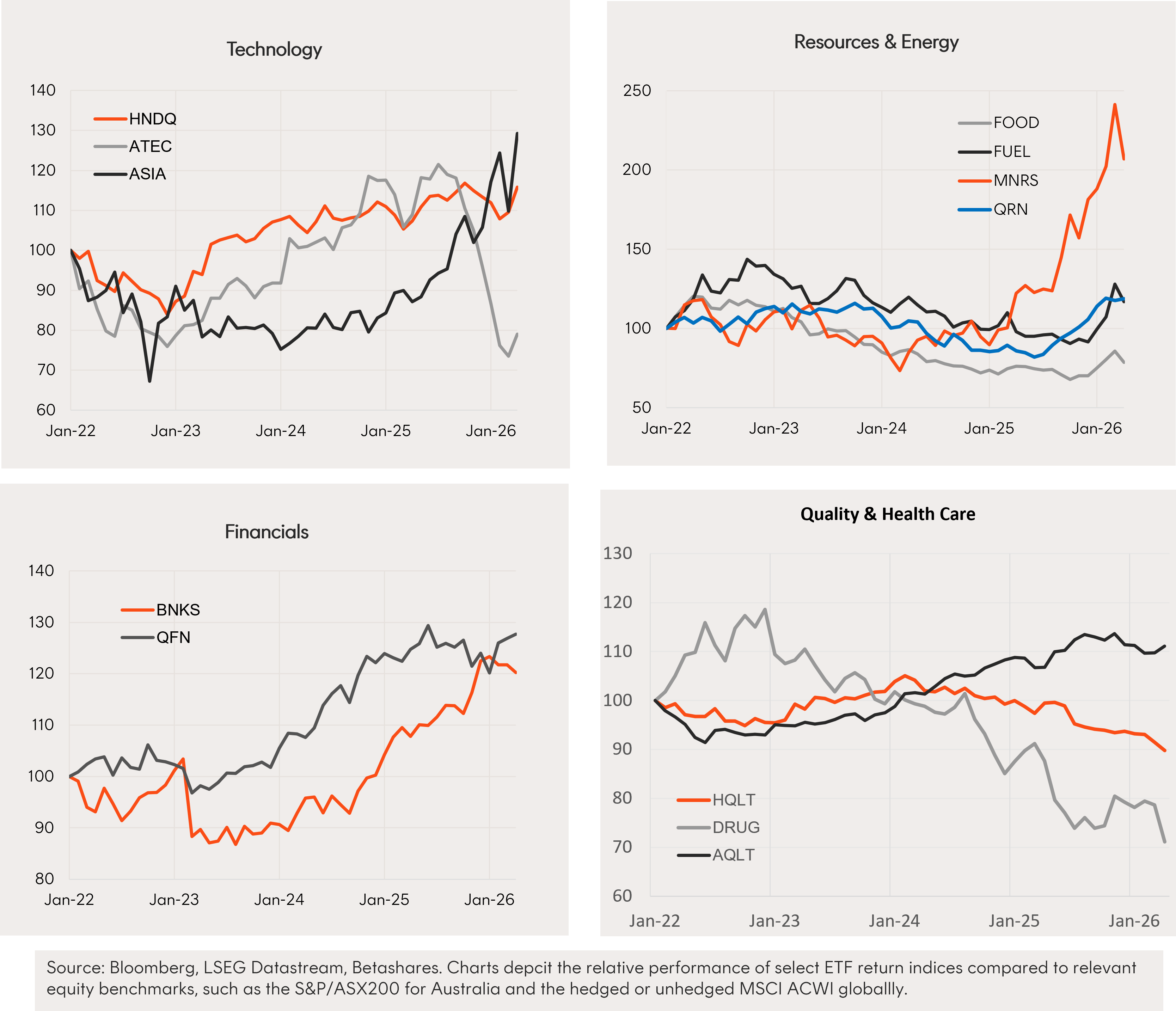

- Resources and energy related exposures have been generally performing well since mid-2025, reflecting strength in gold and metals prices over most of this period and the more recent surge in oil and LNG prices due to the Iran war. Relative performance in this area corrected back a little in April (especially MNRS) reflecting Iranian peace-talk hopes.

- Another area of note is the technology area, where divergent performance is evident between hardware producers (which are most evident in the ASIA ETF) and software producers (as evident in the ATEC ETF) with the former benefitting from the surge in AI-related demand for computer equipment, whereas the latter is being hurt by concerns over AI disruption.

- The relative performance of the NASDAQ-100 ETF (HNDQ) – containing both software and hardware exposures – has improved in recent months, though has been broadly choppy since mid-2025.